- Think about financial wellness in the context of ERISA

- Identify the components of a successful financial wellness program

- Understand how a financial wellness program can be paid for

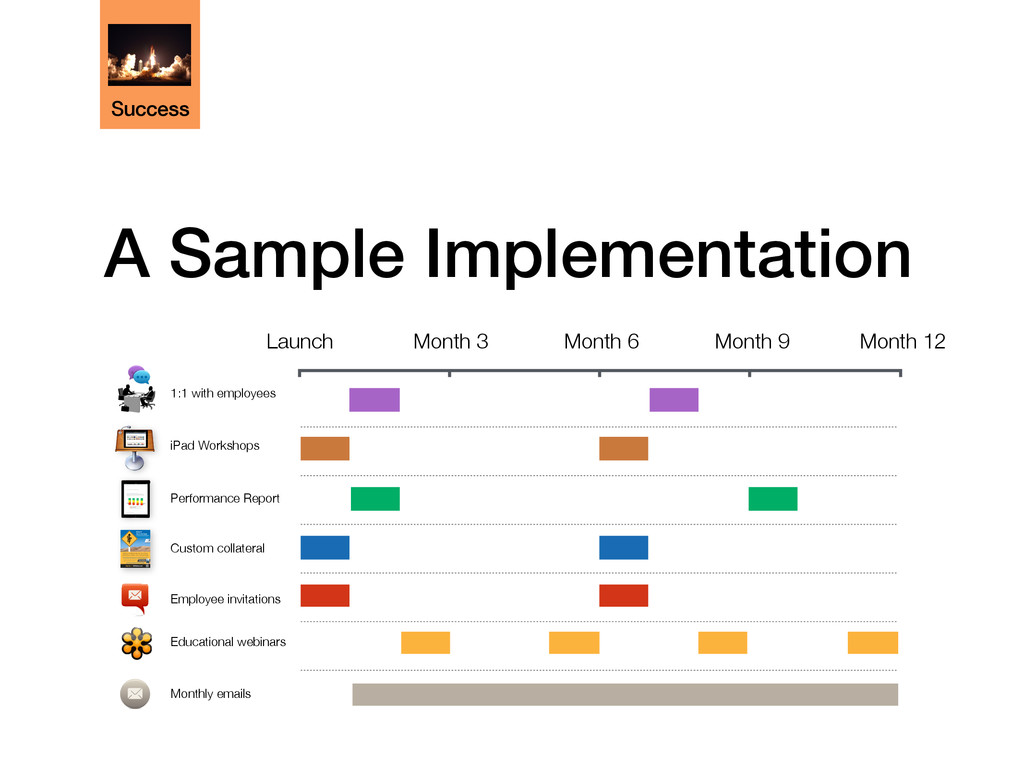

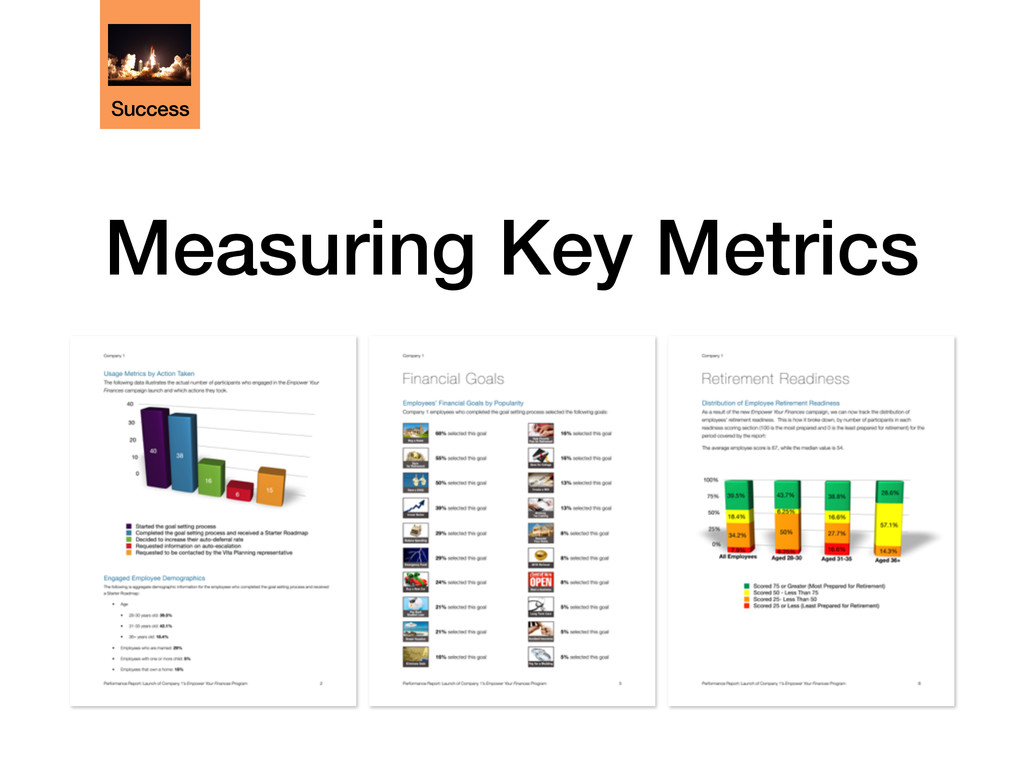

and puts them on a path to achieving their financial goals. What Does Success Look Like? Key success metrics include: ✓ Behavior change (reduction in debt, increased savings) ✓ Employee engagement at months: 1 | 6 | 12 | 24 | 36 ✓ Requests and fulfillment of assistance ✓ Completion rate ✓ Employee evaluations Overview

prudently and must act solely in the interest of participants when making decisions for the plan. ✓ Financial wellness programs for participants are a valuable risk mitigation tool for plan sponsors ✓ Offering a wellness program is like adopting an IPS or hiring a TPA - a good idea for plan sponsors even if not mandated under ERISA ✓ Fiduciary risk is mitigated when participants are informed and able to make prudent investment decisions under the plan ✓ Improving retirement outcomes can significantly reduce the likelihood of complaints to regulators and plan-related litigation Risk

do not officially offer wellness programs may not realize that participant education is probably already being provided. ✓ The plan recordkeeper may be posting website content that is not engaging, or answering important questions without all the facts ✓ HR and co-workers may be acting as de facto advisors to participants, even though they may not be qualified ✓ The plan’s advisor may be unable to track individual participants and follow up in a regular and systematic way ✓ Plan sponsors must keep in mind they have a duty of loyalty to participants and a duty to monitor the plan’s education providers Risk

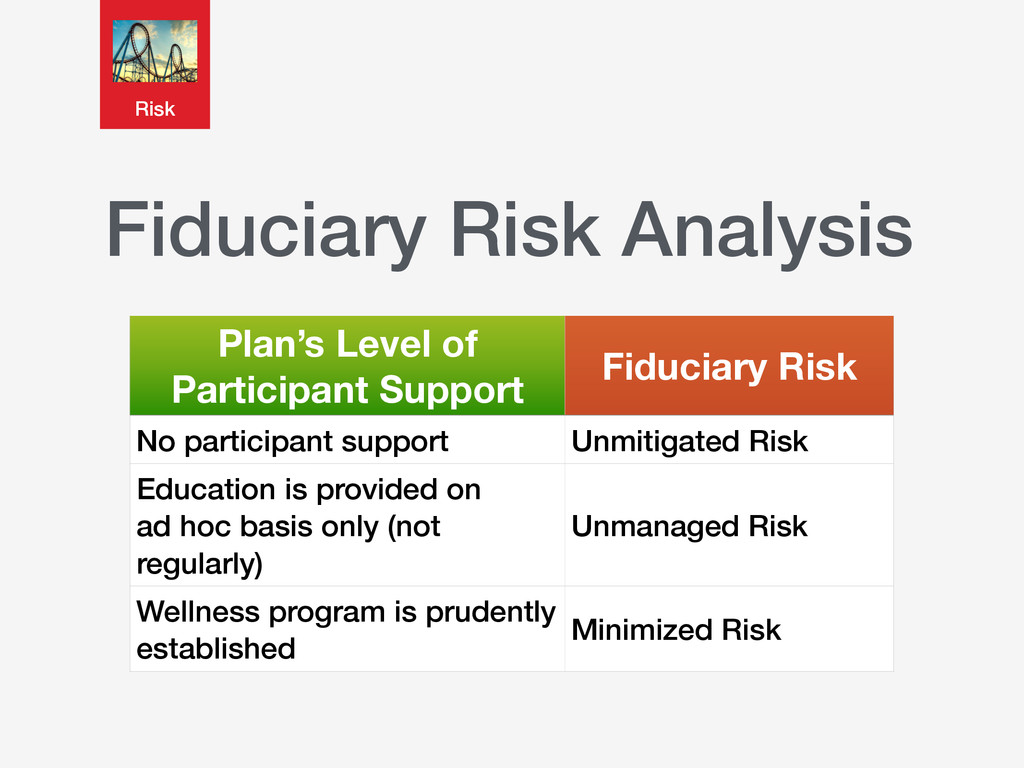

No participant support Unmitigated Risk Education is provided on ad hoc basis only (not regularly) Unmanaged Risk Wellness program is prudently established Minimized Risk Risk

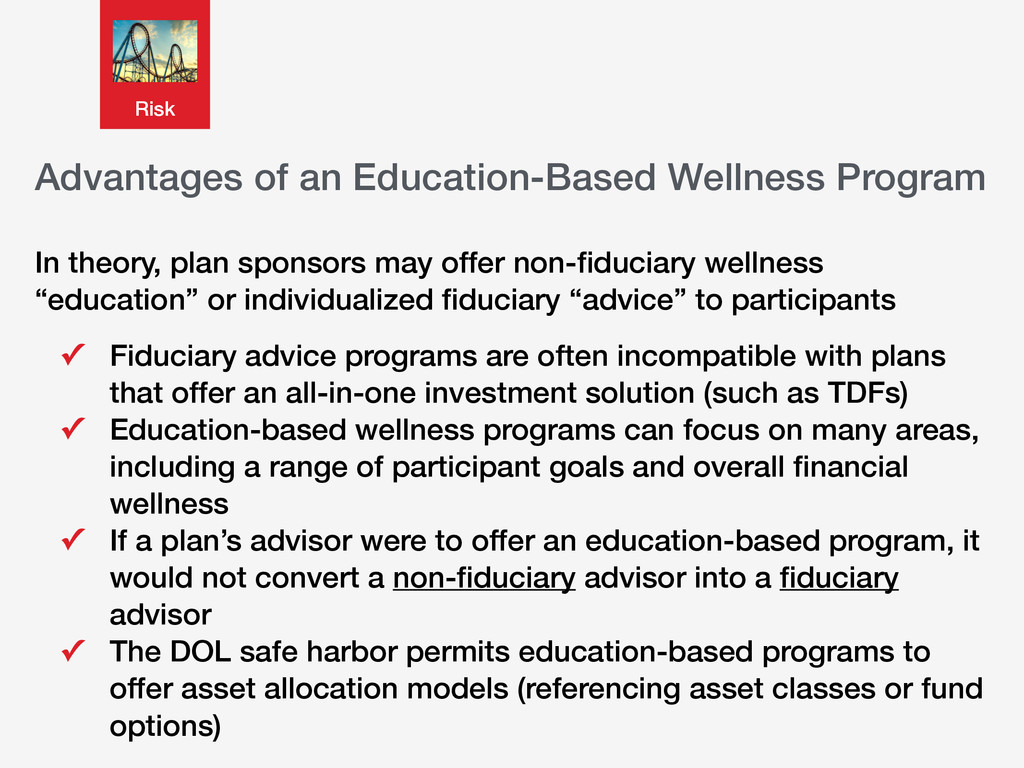

may offer non-fiduciary wellness “education” or individualized fiduciary “advice” to participants ✓ Fiduciary advice programs are often incompatible with plans that offer an all-in-one investment solution (such as TDFs) ✓ Education-based wellness programs can focus on many areas, including a range of participant goals and overall financial wellness ✓ If a plan’s advisor were to offer an education-based program, it would not convert a non-fiduciary advisor into a fiduciary advisor ✓ The DOL safe harbor permits education-based programs to offer asset allocation models (referencing asset classes or fund options) Risk

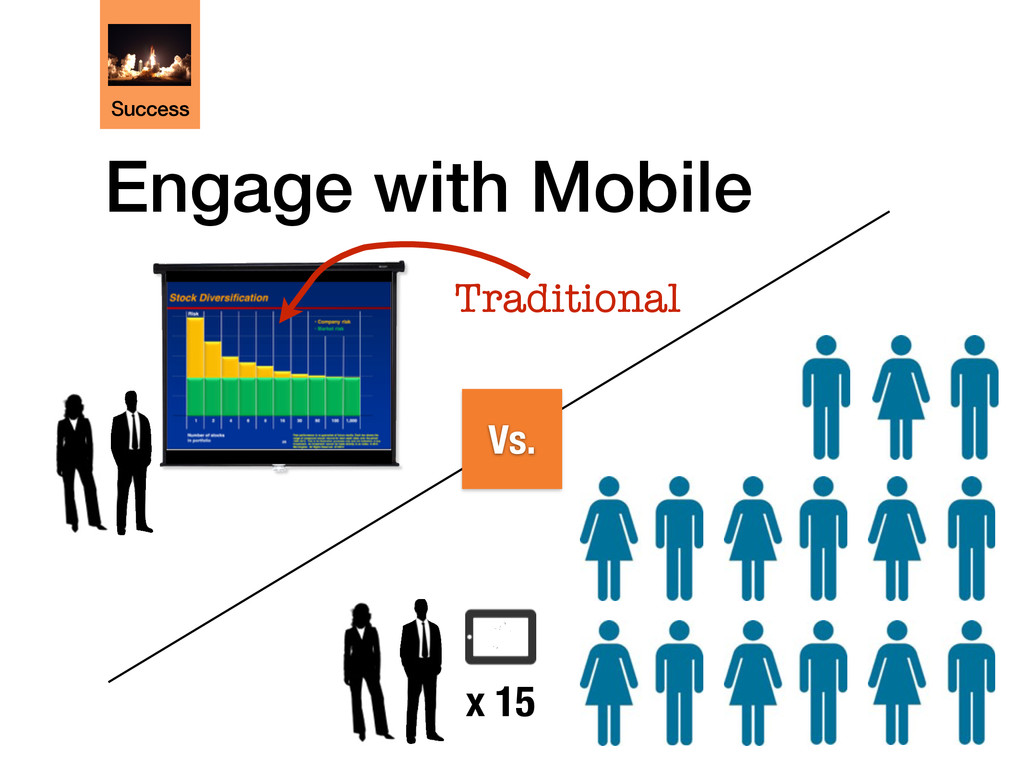

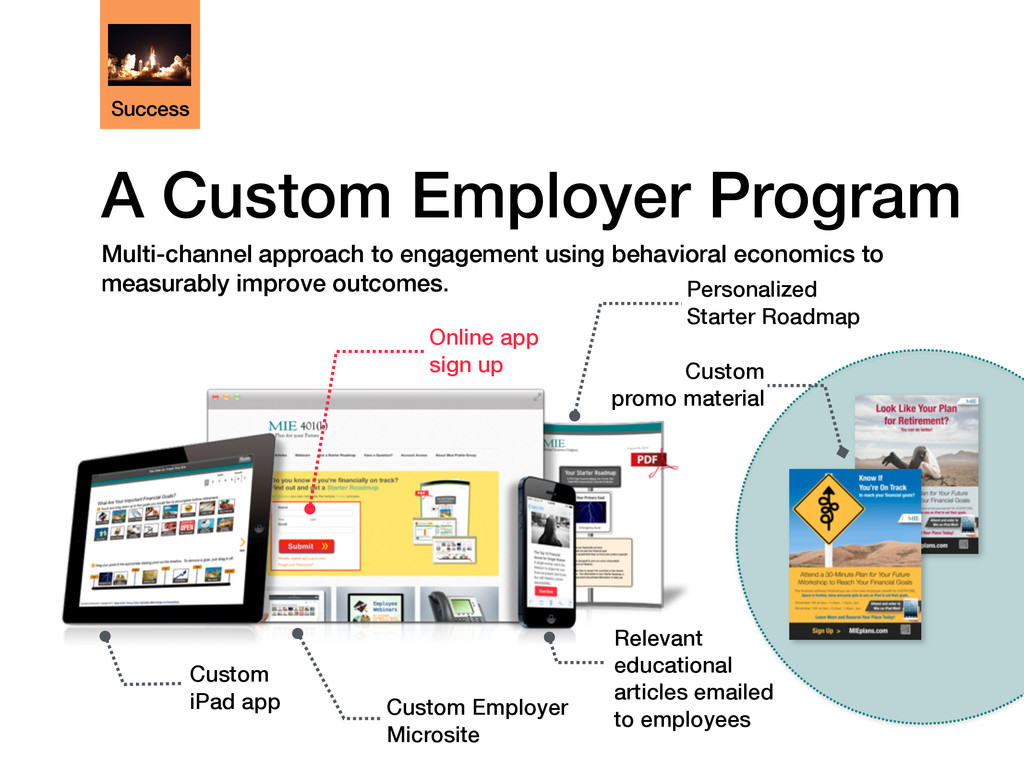

key communication strategies: ✓Multi-channel (web, mobile, onsite workshops) ✓Collateral with calls to action ✓Email ✓Social media promotion (optional) ✓Benefits events

action ✓Highlight employee challenges and show a way out ✓Make it easy to get help from a real person ✓Provide holistic solutions: Budgeting, financial planning, voluntary benefits, consolidate assets, investment advice, debt reduction

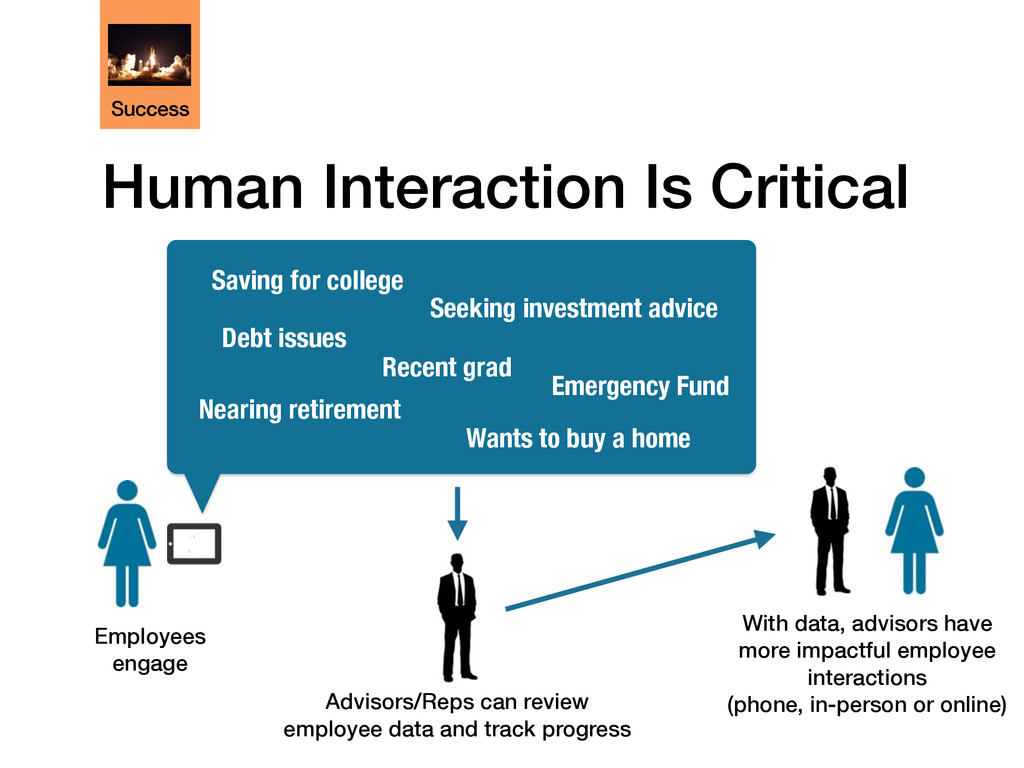

employee data and track progress With data, advisors have more impactful employee interactions (phone, in-person or online) Employees engage Saving for college Seeking investment advice Recent grad Nearing retirement Wants to buy a home Emergency Fund

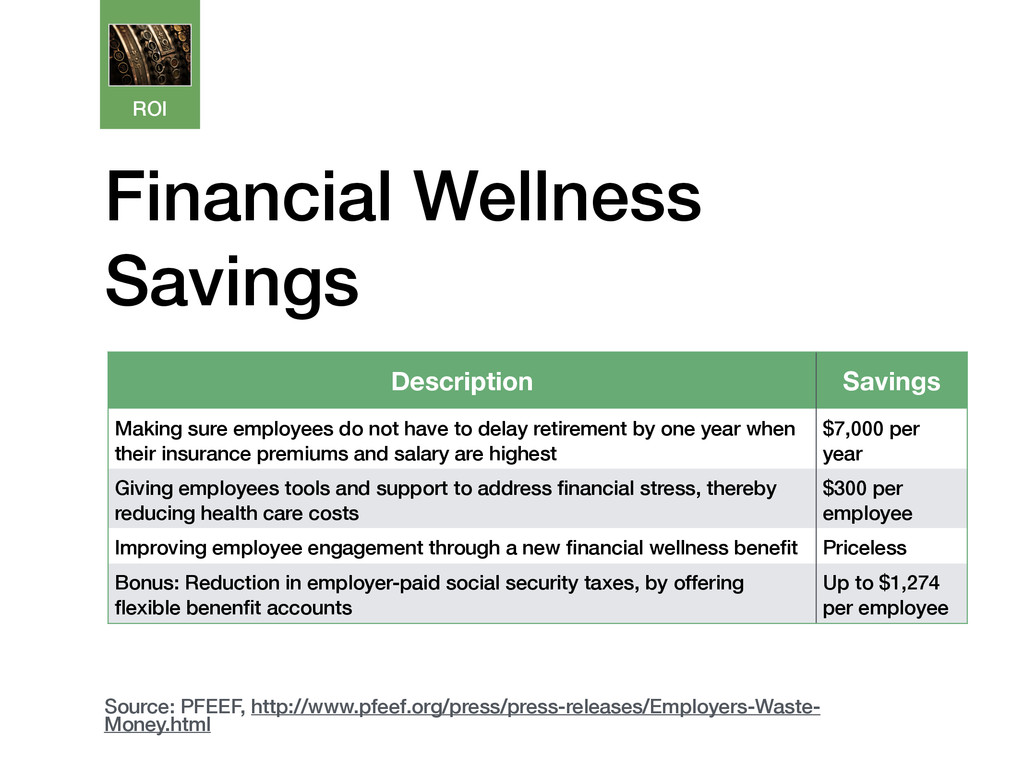

not have to delay retirement by one year when their insurance premiums and salary are highest $7,000 per year Giving employees tools and support to address financial stress, thereby reducing health care costs $300 per employee Improving employee engagement through a new financial wellness benefit Priceless Bonus: Reduction in employer-paid social security taxes, by offering flexible benenfit accounts Up to $1,274 per employee Source: PFEEF, http://www.pfeef.org/press/press-releases/Employers-Waste- Money.html

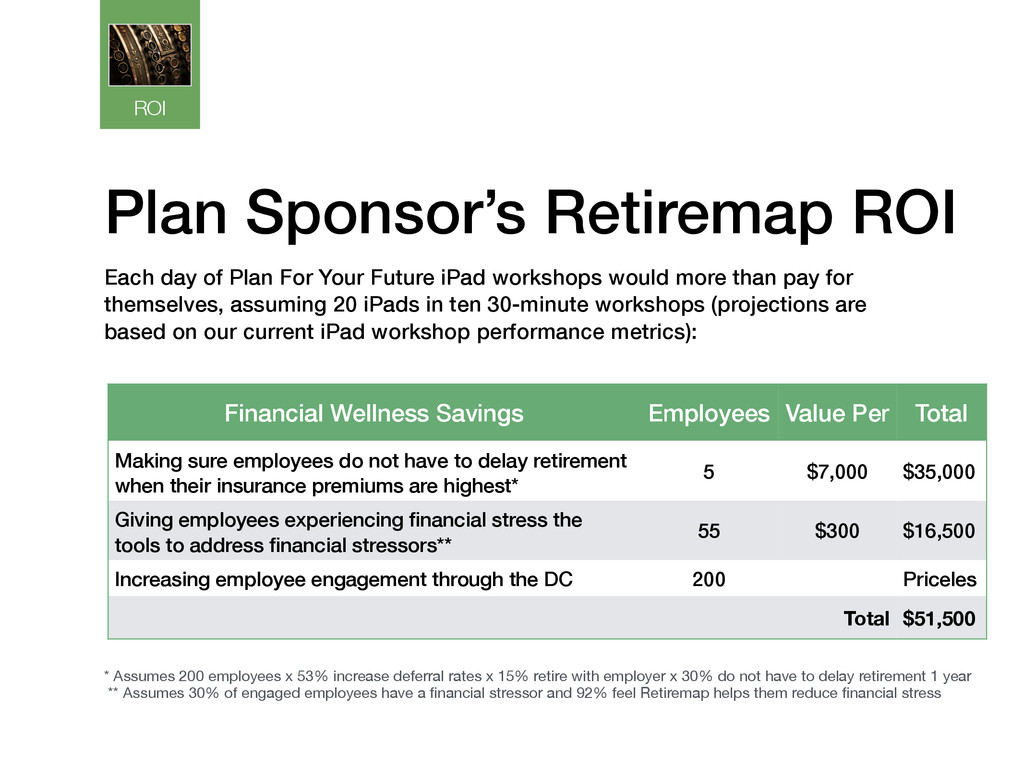

Per Total Making sure employees do not have to delay retirement when their insurance premiums are highest* 5 $7,000 $35,000 Giving employees experiencing financial stress the tools to address financial stressors** 55 $300 $16,500 Increasing employee engagement through the DC benefit 200 $ Priceles s Total $51,500 * Assumes 200 employees x 53% increase deferral rates x 15% retire with employer x 30% do not have to delay retirement 1 year ** Assumes 30% of engaged employees have a financial stressor and 92% feel Retiremap helps them reduce financial stress Each day of Plan For Your Future iPad workshops would more than pay for themselves, assuming 20 iPads in ten 30-minute workshops (projections are based on our current iPad workshop performance metrics):

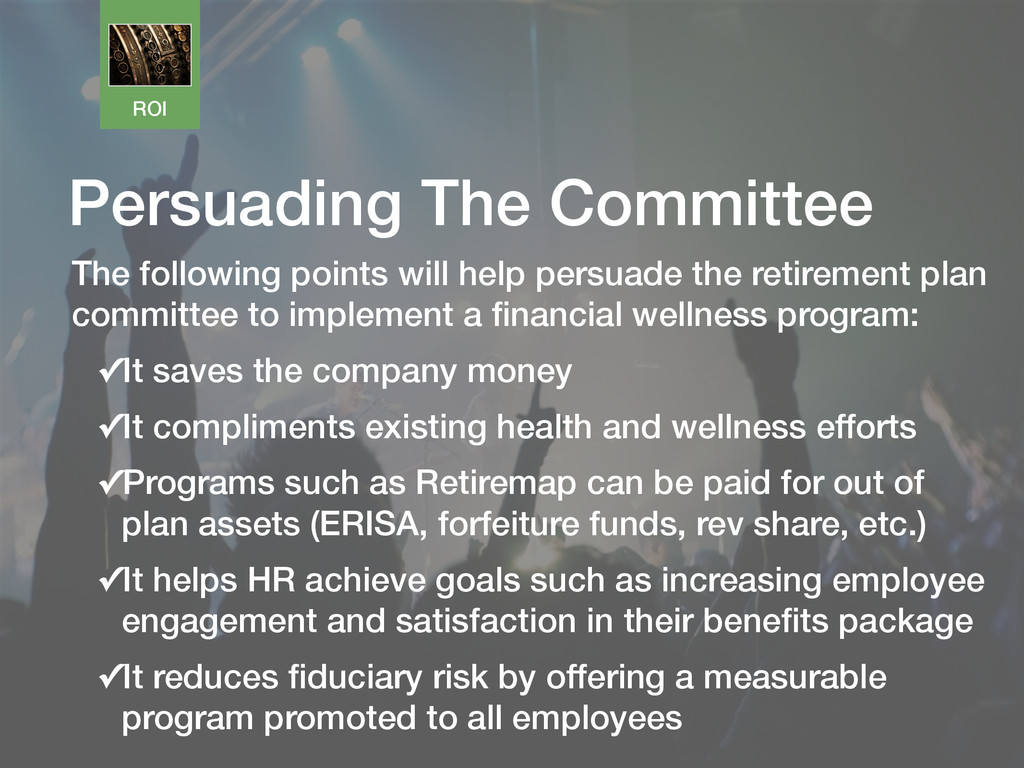

the retirement plan committee to implement a financial wellness program: ✓It saves the company money ✓It compliments existing health and wellness efforts ✓Programs such as Retiremap can be paid for out of plan assets (ERISA, forfeiture funds, rev share, etc.) ✓It helps HR achieve goals such as increasing employee engagement and satisfaction in their benefits package ✓It reduces fiduciary risk by offering a measurable program promoted to all employees

wellness education is treated like any other plan service provider under ERISA. ✓ Provider must deliver 408(b)(2) fee disclosures to plan sponsor ✓ Compensation must be reasonable ✓ Wellness education would be viewed as a “necessary service” that is appropriate and helpful to participants ✓ Service agreement must not have an unreasonable lock-in period ✓ Wellness provider can contract with plan sponsor directly, or serve as subcontractor to another provider (e.g., plan’s advisor) Contracts

can be paid and processed like any other fee for plan-related services. ✓ Fees may be invoiced to plan sponsor or charged against plan assets ✓ In addition to compliance with ERISA Section 408(b)(2), be sure plan’s governing document permits payment from plan assets ✓ Fees may also be paid from plan’s fee recapture account (ERISA budget account or plan expense reimbursement arrangement) ✓ To charge against plan assets, the plan’s recordkeeper/ custodian may ask for a direction letter from the sponsor authorizing payment Contracts

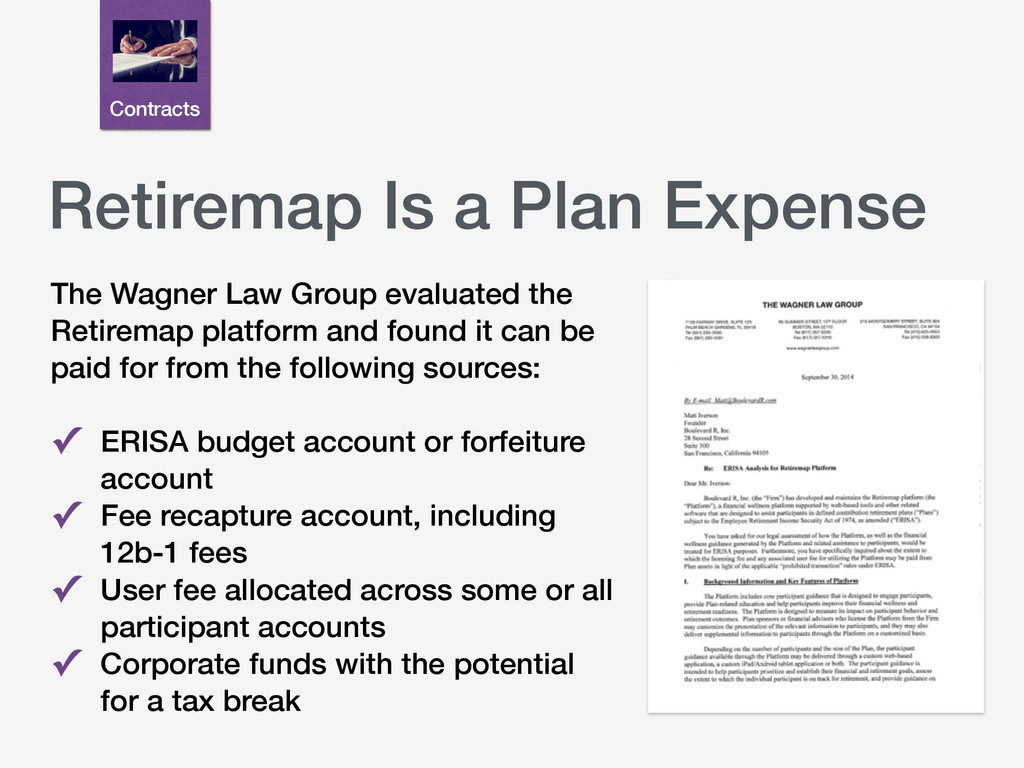

the Retiremap platform and found it can be paid for from the following sources: ✓ ERISA budget account or forfeiture account ✓ Fee recapture account, including 12b-1 fees ✓ User fee allocated across some or all participant accounts ✓ Corporate funds with the potential for a tax break Contracts

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}