program into law, July 30, 1965. Shown with the President (on the right in the photo) are (left to right) Mrs. Johnson; former President Harry Truman; Vice-President Hubert Humphrey; and Mrs. Truman. At the bill-signing ceremony President Johnson enrolled President Truman as the first Medicare beneficiary and presented him with the first Medicare card. This is President Truman's application for the optional Part B medical care coverage, which President Johnson signed as a witness. Back then: The average person retiring was male, and his average life expectancy was only 68 years! Part B cost just $3.00 a month! 19 million people signed up that first year.

benefits from Social Security or the Railroad Retirement Board (RRB), you’ll automatically get Part A and Part B starting the first day of the month you turn 65. (If your birthday is on the first day of the month, Part A and Part B will start the first day of the prior month.) If you’re under 65 and have a disability, you’ll automatically get Part A and Part B after you get disability benefits from Social Security or certain disability benefits from the RRB for 24 months. If you are not getting social security benefits currently, you should contact the Social Security administration 90 days before your eligible for benefits to start on time. *If your birthday is on the first of the month, your coverage will start on the first day of the month before your birthday month. For example, if you turn 65 on Aug. 1, your coverage will start July 1.

most cases, if you don't sign up for Part B when you're first eligible, you'll have to pay a late enrollment penalty for as long as you have Part B. Your monthly premium for Part B may go up 10% for each full 12-month period that you could have had Part B but didn't sign up for it. Also, you may have to wait until the General Enrollment Period (from January 1 to March 31) to enroll in Part B, and coverage will start July 1 of that year.

those that don’t get Part A at no cost, they pay $505.00/month Part B cost: Tax Filing Status 2022 Part B Premiums 2024 Single Married $102,000 or less $205,00 or less $174.80 Single Married $102,001 - $130,000 $205,001 - $260,000 $244.70 Single Married $130,001 - $162,000 $260,001 - $324,000 $349.60 Single Married $162,001 - $193,500 $324,001 - $387,000 $454.40 Single Married $193,501 – $500,000 $387,001 – $750,000 $559.52 Single Married $500,001 or above $750,001 or above $560.50

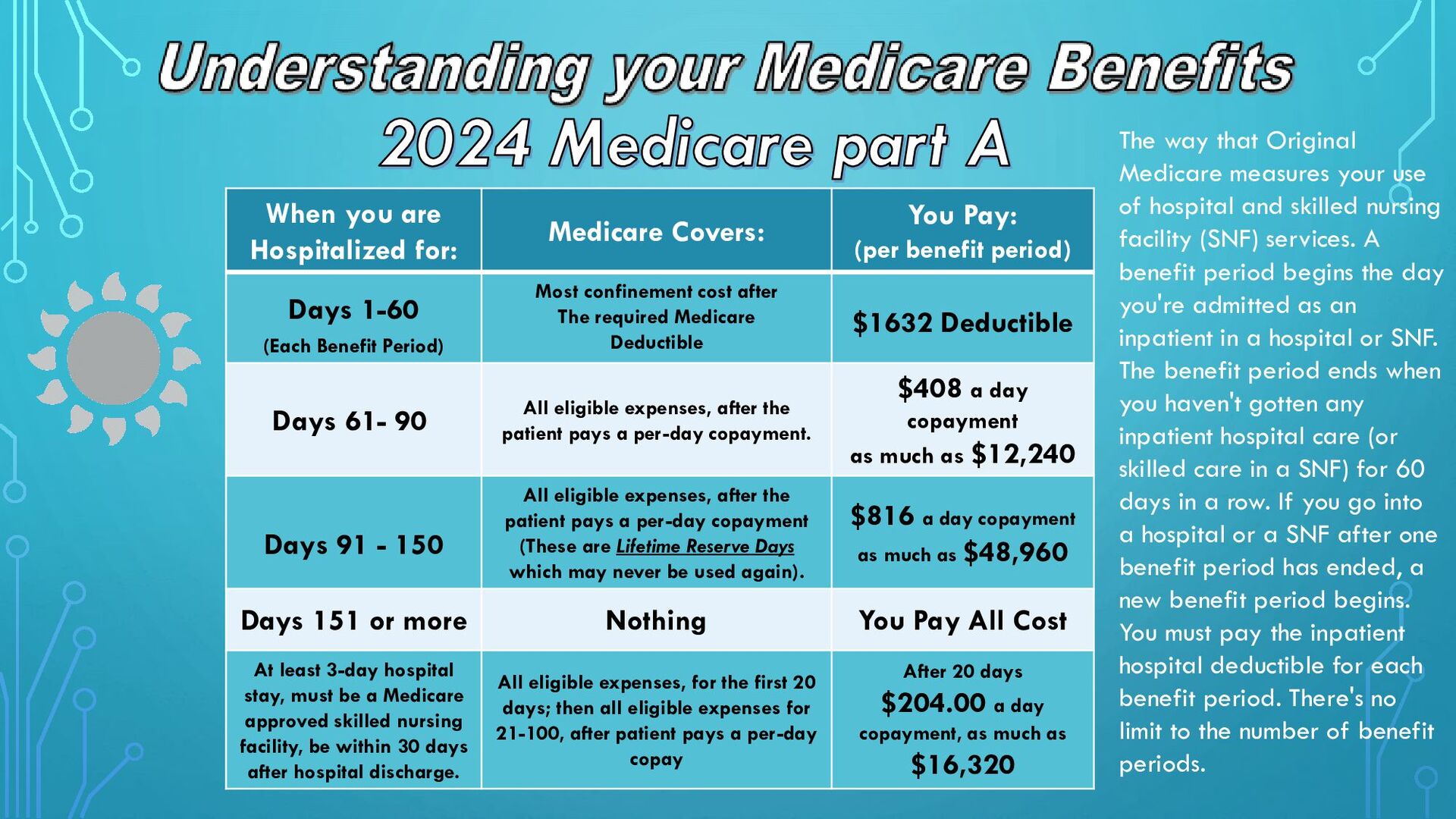

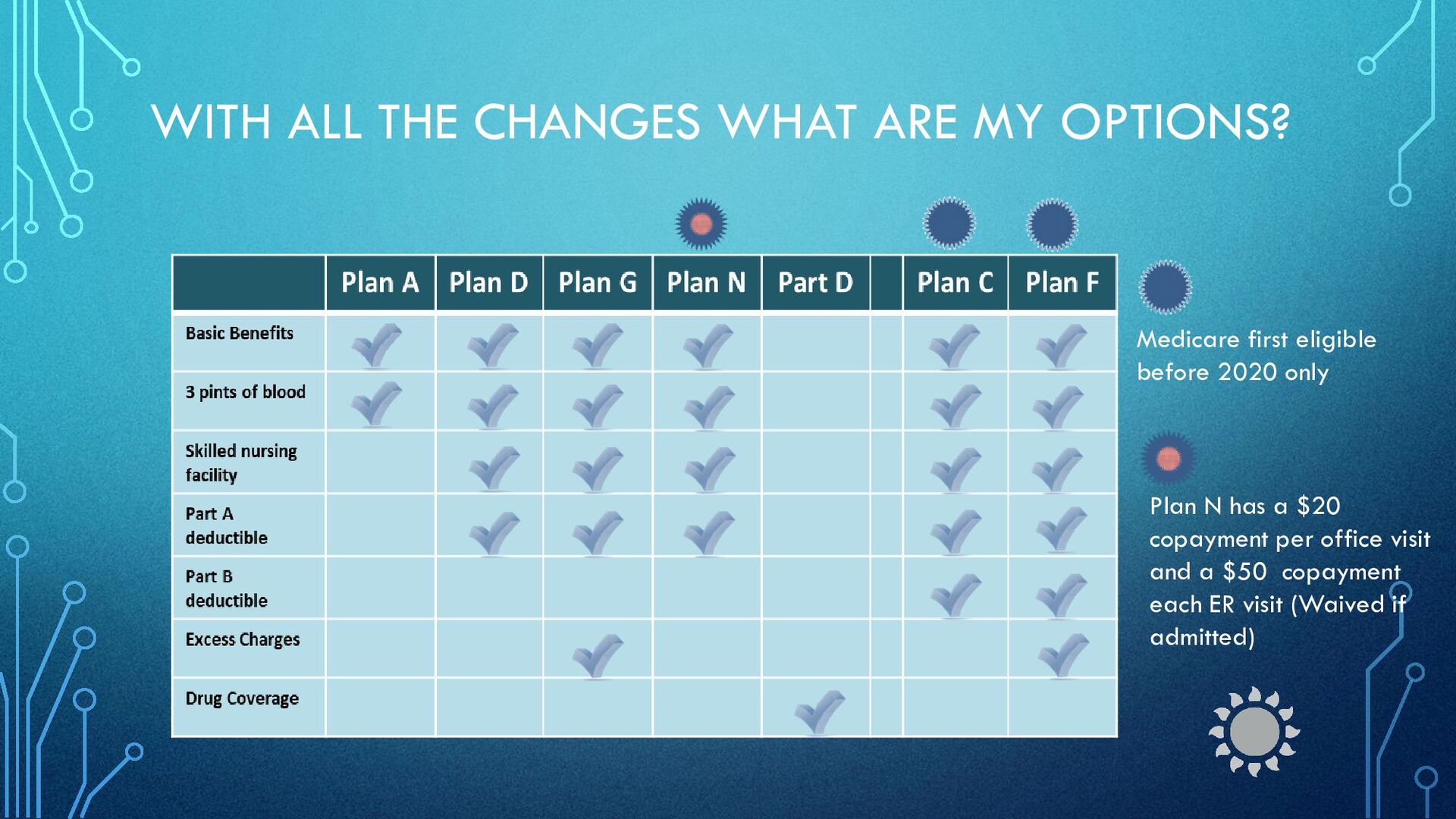

Covers: You Pay: (per benefit period) Days 1-60 (Each Benefit Period) Most confinement cost after The required Medicare Deductible $1632 Deductible Days 61- 90 All eligible expenses, after the patient pays a per-day copayment. $408 a day copayment as much as $12,240 Days 91 - 150 All eligible expenses, after the patient pays a per-day copayment (These are Lifetime Reserve Days which may never be used again). $816 a day copayment as much as $48,960 Days 151 or more Nothing You Pay All Cost At least 3-day hospital stay, must be a Medicare approved skilled nursing facility, be within 30 days after hospital discharge. All eligible expenses, for the first 20 days; then all eligible expenses for 21-100, after patient pays a per-day copay After 20 days $204.00 a day copayment, as much as $16,320 The way that Original Medicare measures your use of hospital and skilled nursing facility (SNF) services. A benefit period begins the day you're admitted as an inpatient in a hospital or SNF. The benefit period ends when you haven't gotten any inpatient hospital care (or skilled care in a SNF) for 60 days in a row. If you go into a hospital or a SNF after one benefit period has ended, a new benefit period begins. You must pay the inpatient hospital deductible for each benefit period. There's no limit to the number of benefit periods.

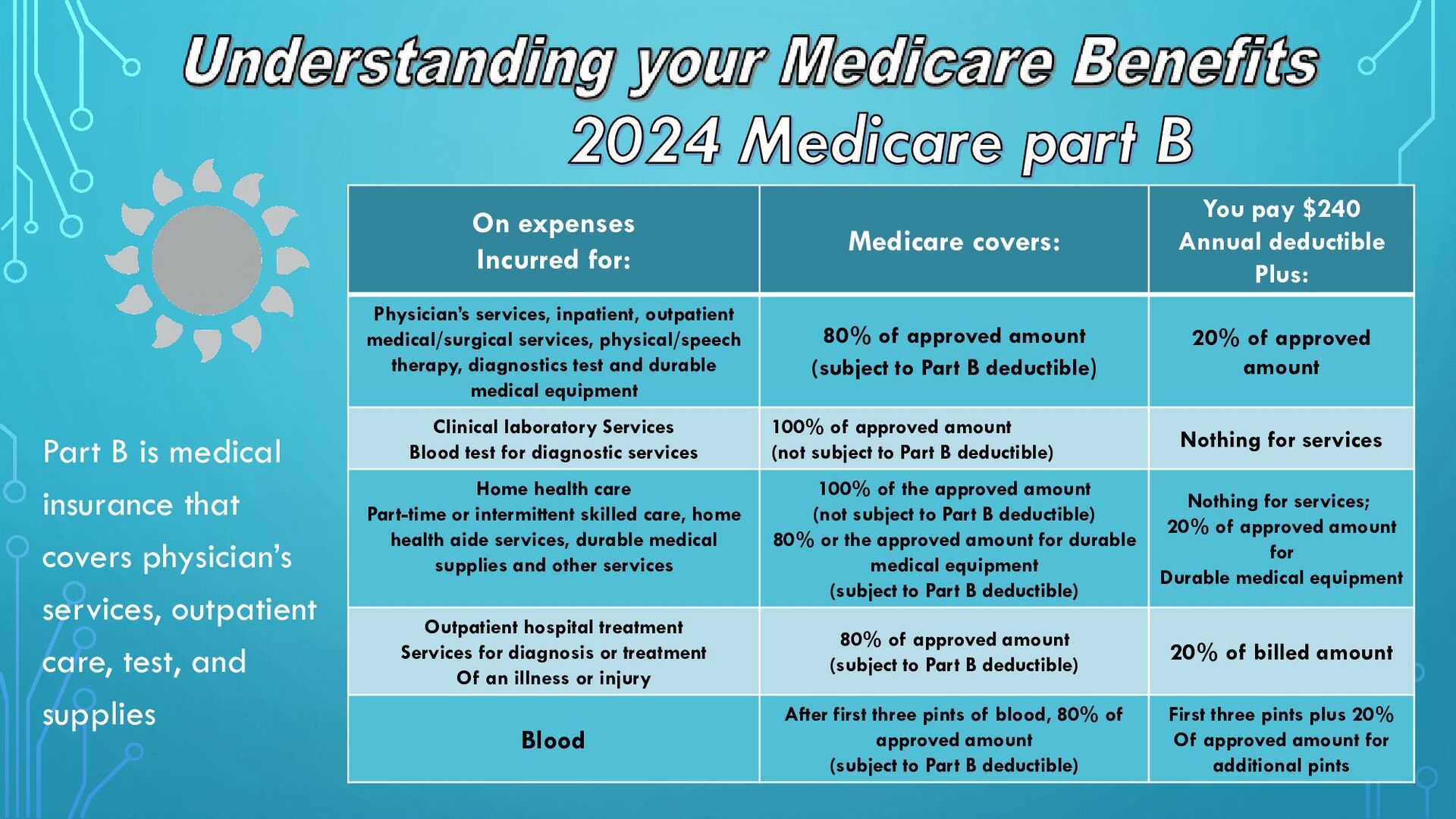

covers physician’s services, outpatient care, test, and supplies On expenses Incurred for: Medicare covers: You pay $240 Annual deductible Plus: Physician’s services, inpatient, outpatient medical/surgical services, physical/speech therapy, diagnostics test and durable medical equipment 80% of approved amount (subject to Part B deductible) 20% of approved amount Clinical laboratory Services Blood test for diagnostic services 100% of approved amount (not subject to Part B deductible) Nothing for services Home health care Part-time or intermittent skilled care, home health aide services, durable medical supplies and other services 100% of the approved amount (not subject to Part B deductible) 80% or the approved amount for durable medical equipment (subject to Part B deductible) Nothing for services; 20% of approved amount for Durable medical equipment Outpatient hospital treatment Services for diagnosis or treatment Of an illness or injury 80% of approved amount (subject to Part B deductible) 20% of billed amount Blood After first three pints of blood, 80% of approved amount (subject to Part B deductible) First three pints plus 20% Of approved amount for additional pints

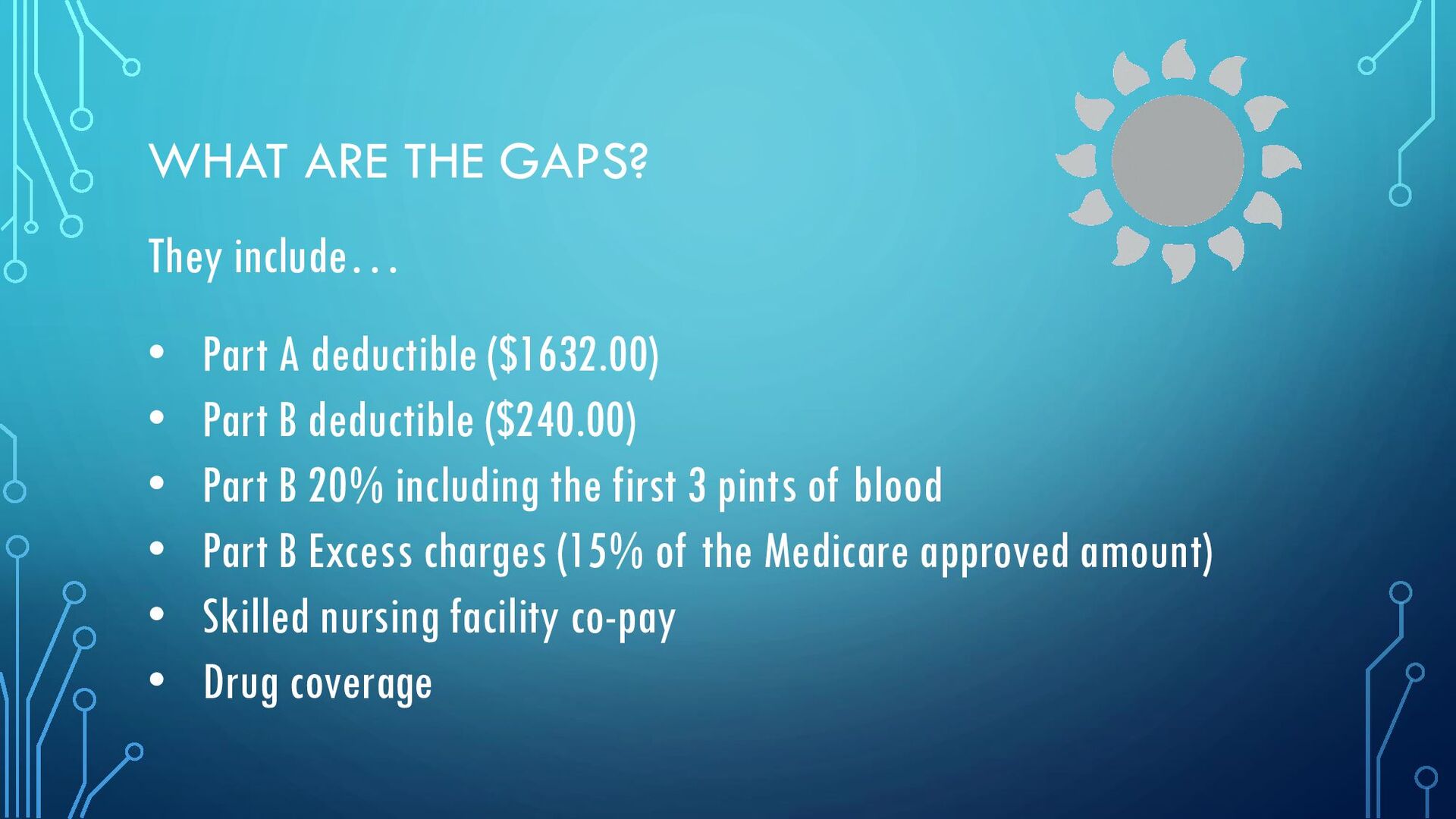

($1632.00) • Part B deductible ($240.00) • Part B 20% including the first 3 pints of blood • Part B Excess charges (15% of the Medicare approved amount) • Skilled nursing facility co-pay • Drug coverage

and code for any procedure you might have. If they accept the assigned price, they are “accepting assignment”, most places do. Some doctors and facilities, usually specialist and specialty hospitals, can charge 15% more than the Medicare approved amount. These charges are referred to as “excess charges”. If having the option to go to any facility you choose is important to you, make sure your plan covers this benefit.

ABOUT The White House Office of the Press Secretary For Immediate Release April 16, 2015 Statement by the Press Secretary on H.R. 2 On Thursday, April 16, 2015, the President signed into law: H.R. 2, the “Medicare Access and CHIP Reauthorization Act of 2015,” which permanently replaces Medicare's sustainable growth rate system for physician payments and reforms Medicare physician payment policies to encourage efficient, high-quality care; extends for two years funding for the Children's Health Insurance Program; extends numerous other expiring health provisions and the Secure Rural Schools program; and removes Social Security numbers from Medicare cards and makes other Medicare improvements.

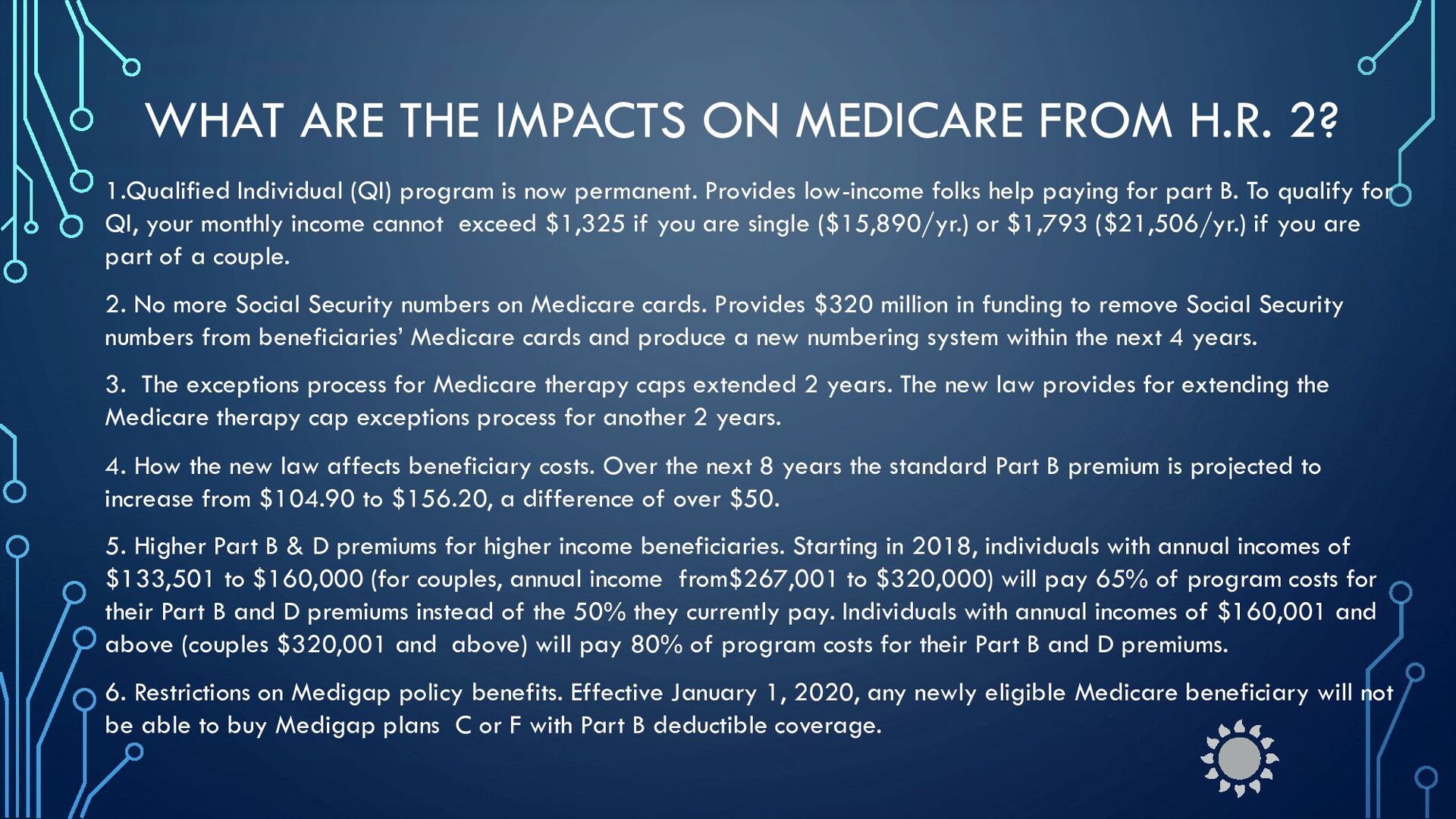

Individual (QI) program is now permanent. Provides low-income folks help paying for part B. To qualify for QI, your monthly income cannot exceed $1,325 if you are single ($15,890/yr.) or $1,793 ($21,506/yr.) if you are part of a couple. 2. No more Social Security numbers on Medicare cards. Provides $320 million in funding to remove Social Security numbers from beneficiaries’ Medicare cards and produce a new numbering system within the next 4 years. 3. The exceptions process for Medicare therapy caps extended 2 years. The new law provides for extending the Medicare therapy cap exceptions process for another 2 years. 4. How the new law affects beneficiary costs. Over the next 8 years the standard Part B premium is projected to increase from $104.90 to $156.20, a difference of over $50. 5. Higher Part B & D premiums for higher income beneficiaries. Starting in 2018, individuals with annual incomes of $133,501 to $160,000 (for couples, annual income from$267,001 to $320,000) will pay 65% of program costs for their Part B and D premiums instead of the 50% they currently pay. Individuals with annual incomes of $160,001 and above (couples $320,001 and above) will pay 80% of program costs for their Part B and D premiums. 6. Restrictions on Medigap policy benefits. Effective January 1, 2020, any newly eligible Medicare beneficiary will not be able to buy Medigap plans C or F with Part B deductible coverage.

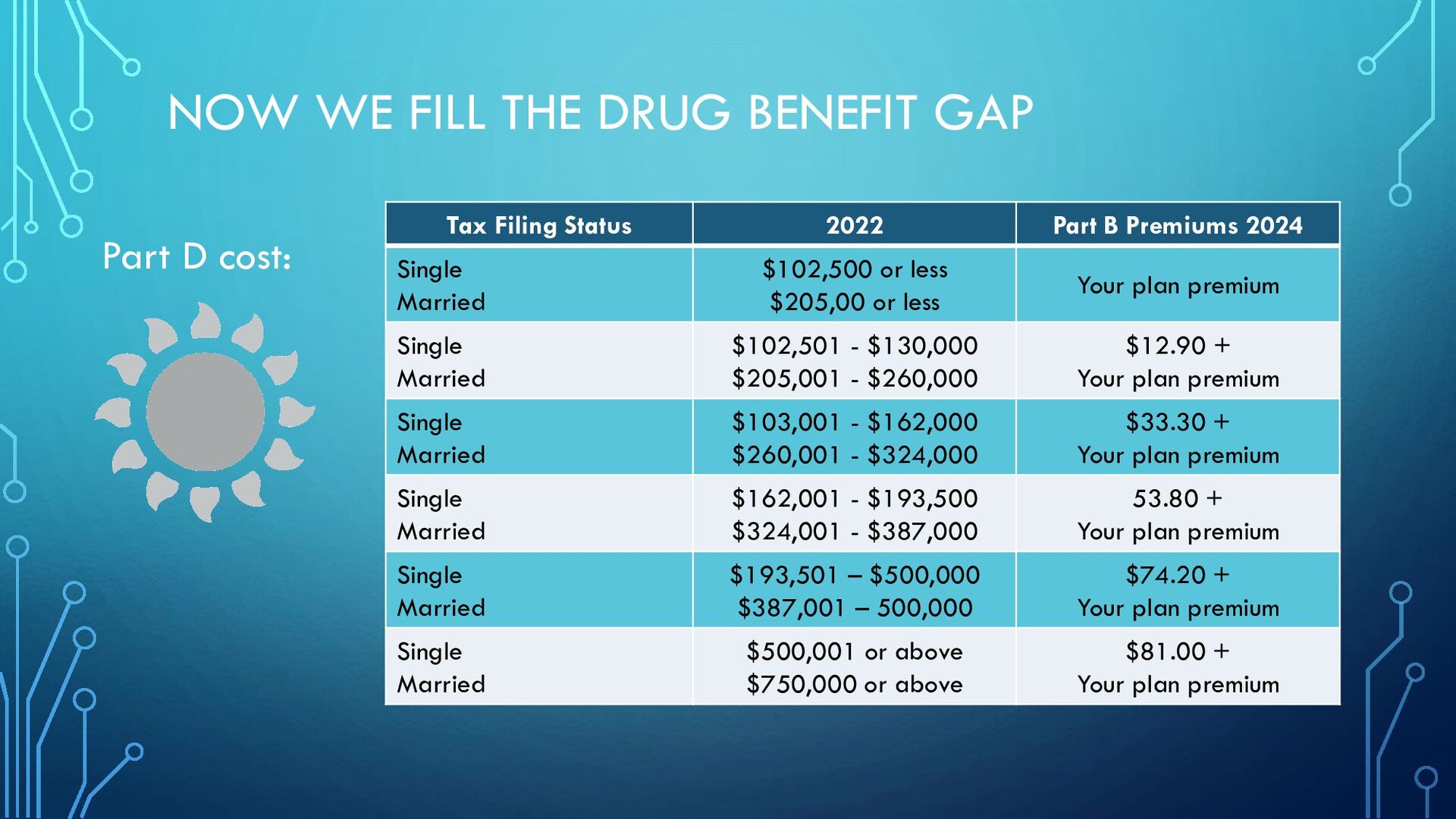

Tax Filing Status 2022 Part B Premiums 2024 Single Married $102,500 or less $205,00 or less Your plan premium Single Married $102,501 - $130,000 $205,001 - $260,000 $12.90 + Your plan premium Single Married $103,001 - $162,000 $260,001 - $324,000 $33.30 + Your plan premium Single Married $162,001 - $193,500 $324,001 - $387,000 53.80 + Your plan premium Single Married $193,501 – $500,000 $387,001 – 500,000 $74.20 + Your plan premium Single Married $500,001 or above $750,000 or above $81.00 + Your plan premium

the late enrollment penalty depends on how long you went without Part D or creditable prescription drug coverage. Medicare calculates the penalty by multiplying 1% of the "national base beneficiary premium" ($34.70 in 2024) times the number of full, uncovered months you didn't have Part D or creditable coverage. The monthly premium is rounded to the nearest $.10 and added to your monthly Part D premium. The national base beneficiary premium may increase each year, so your penalty amount may also increase each year.

2023 Basic Benefits You Pay Deductible $505 100% of first $505 Initial Coverage Limit $4,660 Various co-pays Coverage Gap $7,400 25% of the drug cost Catastrophic coverage Medicare and Plan pays 95% The greater of 5% or $10.35 for Brand name $4.15 for generic “ Keep in mind, this is the minimum coverage a plan has to include as required by the government, MOST do better in this competitive market”

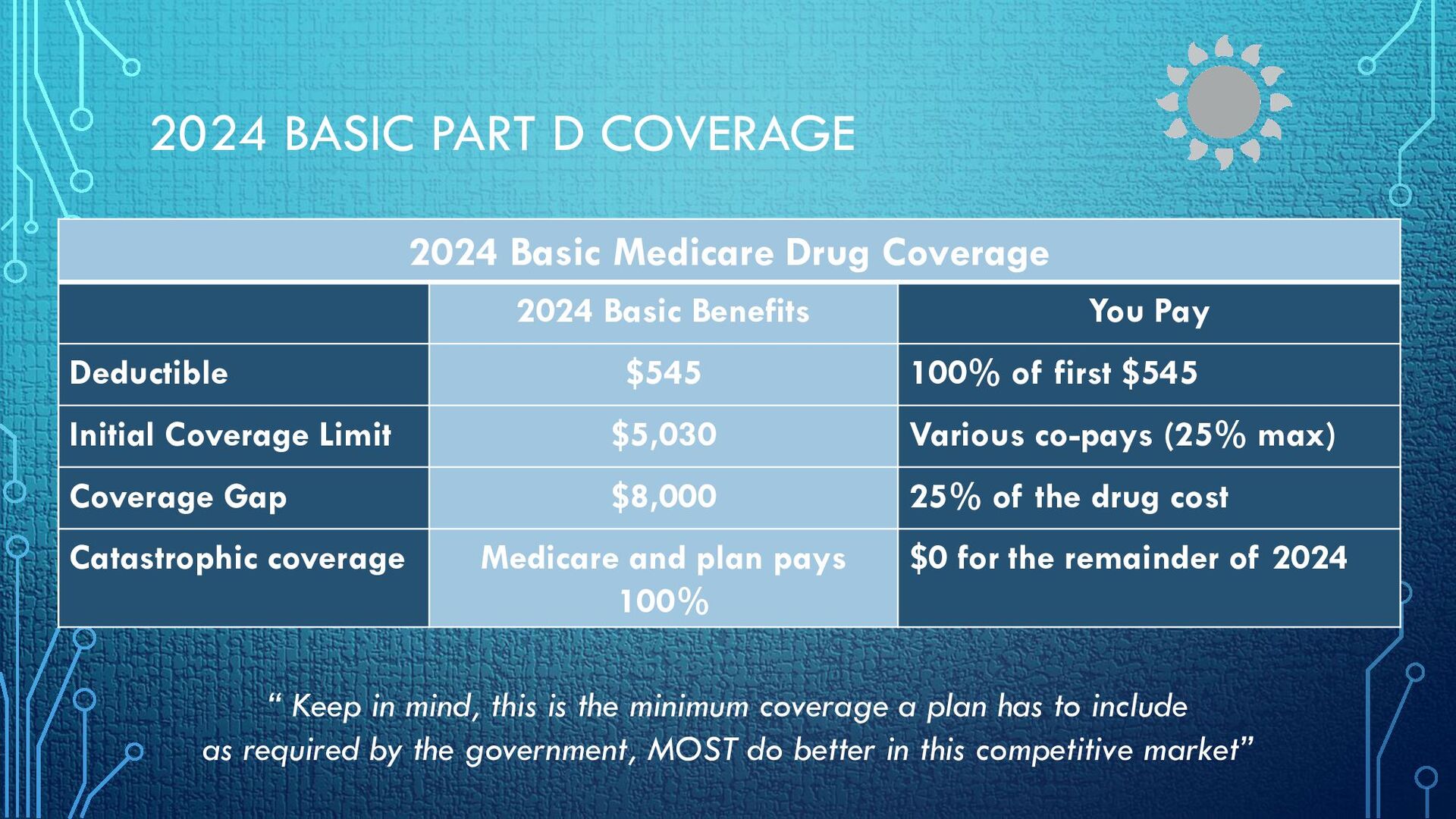

2024 Basic Benefits You Pay Deductible $545 100% of first $545 Initial Coverage Limit $5,030 Various co-pays (25% max) Coverage Gap $8,000 25% of the drug cost Catastrophic coverage Medicare and plan pays 100% $0 for the remainder of 2024 “ Keep in mind, this is the minimum coverage a plan has to include as required by the government, MOST do better in this competitive market”

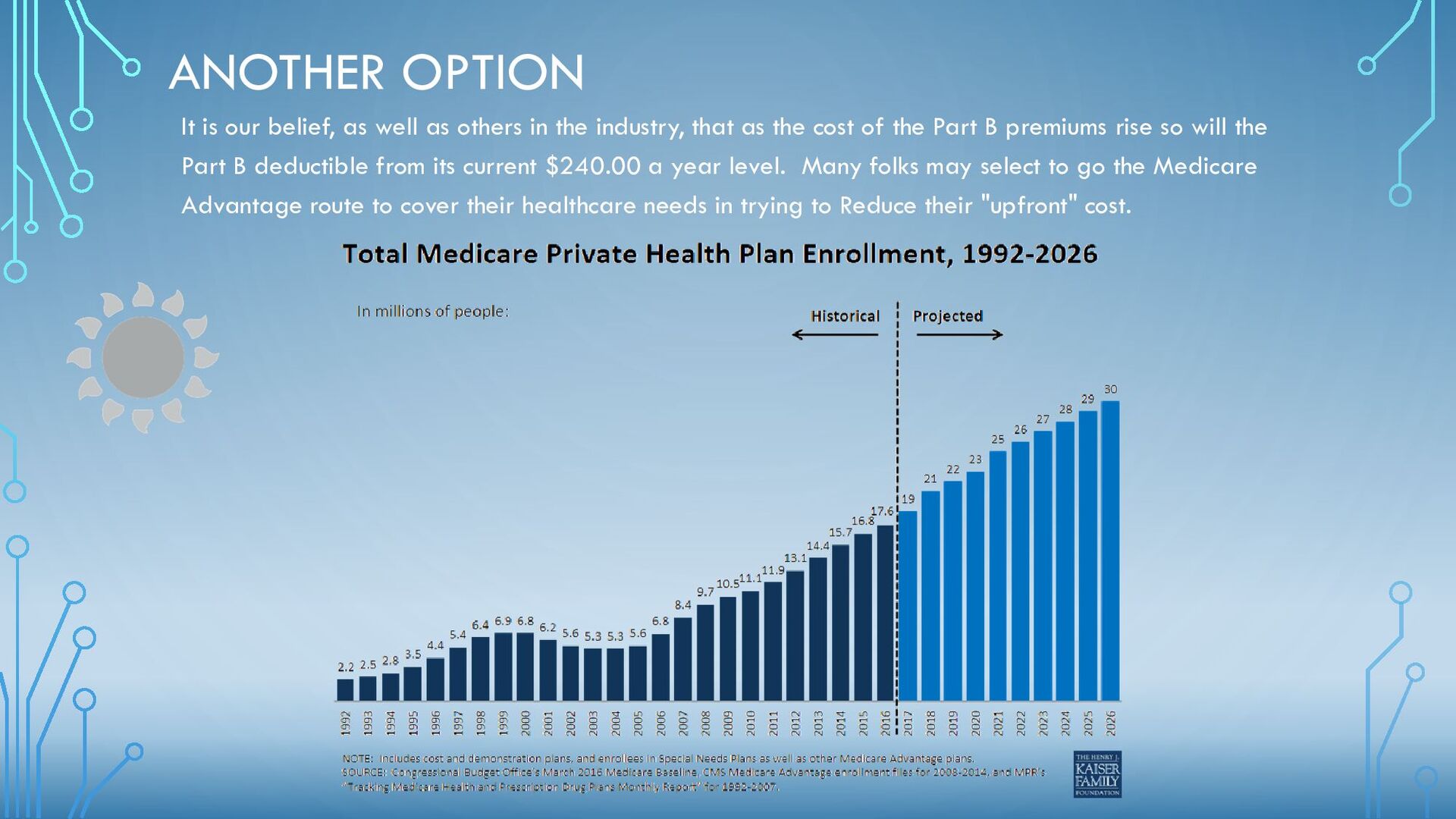

in the industry, that as the cost of the Part B premiums rise so will the Part B deductible from its current $240.00 a year level. Many folks may select to go the Medicare Advantage route to cover their healthcare needs in trying to Reduce their "upfront" cost.

Plans (cont.) • Most plans offer health and drug coverage, as well as extra benefits • Most have lower out-of-pocket costs than with Original Medicare • You may have to use certain healthcare providers • You do not need a Medicare Supplement

Plans? • Medicare Advantage (MA) plans are health plan options that are part of the Medicare program. • MA plans are not the same as Medicare Supplement insurance. • Medicare pays the plan (the insurance company) a set amount every month for your care. • MA plans must offer all benefits of Original Medicare and can include Part D prescription drug coverage.

before deciding on an Advantage Plan • What is the current state of your health? • How often do you visit the doctor or hospital? • Will the cost savings in monthly premium offset the co-pays? • Where is the plan coverage area? • Are the added benefits important to you? • Can you return to “traditional Medicare” if you are not happy? **Remember, in most cases, you must use the card from your Medicare Advantage Plan to get your Medicare-covered services. Keep your Medicare card in a safe place because you’ll need it if you ever switch back to Original Medicare. **2021 Medicare and you pg.57

• Medicare Advantage Plans • Part D Drug Cards • Dental, Vison, and Hearing • Life Insurance • Annuities • Short Term Care • Long Term Care Insurance • Supplemental Health • Travel Insurance

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}