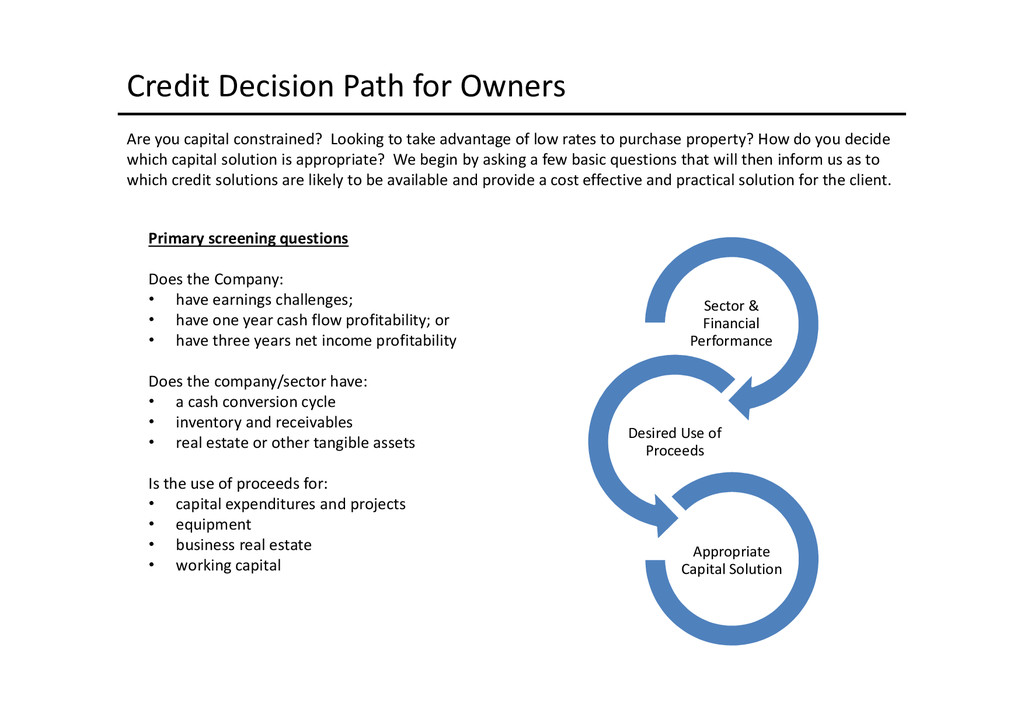

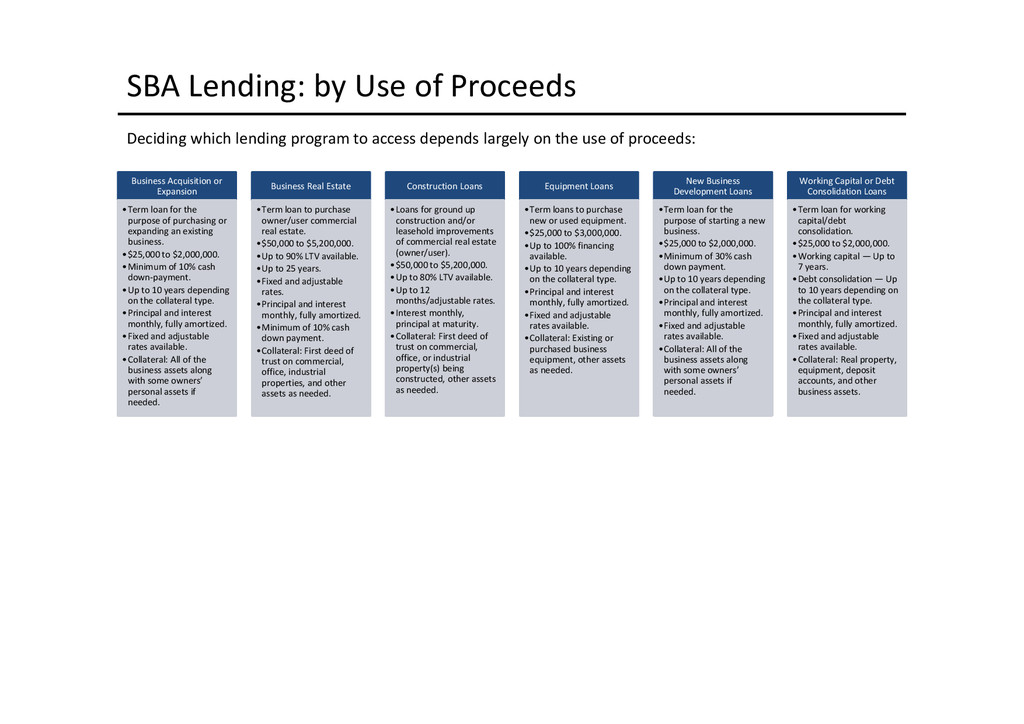

to access depends largely on the use of proceeds: Business Acquisition or Expansion •Term loan for the purpose of purchasing or expanding an existing business. •$25,000 to $2,000,000. •Minimum of 10% cash down-payment. •Up to 10 years depending on the collateral type. •Principal and interest monthly, fully amortized. •Fixed and adjustable rates available. •Collateral: All of the business assets along with some owners’ personal assets if needed. Business Real Estate •Term loan to purchase owner/user commercial real estate. •$50,000 to $5,200,000. •Up to 90% LTV available. •Up to 25 years. •Fixed and adjustable rates. •Principal and interest monthly, fully amortized. •Minimum of 10% cash down payment. •Collateral: First deed of trust on commercial, office, industrial properties, and other assets as needed. Construction Loans •Loans for ground up construction and/or leasehold improvements of commercial real estate (owner/user). •$50,000 to $5,200,000. •Up to 80% LTV available. •Up to 12 months/adjustable rates. •Interest monthly, principal at maturity. •Collateral: First deed of trust on commercial, office, or industrial property(s) being constructed, other assets as needed. Equipment Loans •Term loans to purchase new or used equipment. •$25,000 to $3,000,000. •Up to 100% financing available. •Up to 10 years depending on the collateral type. •Principal and interest monthly, fully amortized. •Fixed and adjustable rates available. •Collateral: Existing or purchased business equipment, other assets as needed. New Business Development Loans •Term loan for the purpose of starting a new business. •$25,000 to $2,000,000. •Minimum of 30% cash down payment. •Up to 10 years depending on the collateral type. •Principal and interest monthly, fully amortized. •Fixed and adjustable rates available. •Collateral: All of the business assets along with some owners’ personal assets if needed. Working Capital or Debt Consolidation Loans •Term loan for working capital/debt consolidation. •$25,000 to $2,000,000. •Working capital — Up to 7 years. •Debt consolidation — Up to 10 years depending on the collateral type. •Principal and interest monthly, fully amortized. •Fixed and adjustable rates available. •Collateral: Real property, equipment, deposit accounts, and other business assets.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}