Market is projected to grow from USD 2.5 billion in 2024 to USD 24.8 billion by 2034, at a remarkable CAGR of 25.8%. This presentation explores market dynamics, key segments, regional insights, and growth opportunities in this rapidly expanding sector.

Growing at 25.8% CAGR from 2025-2034 37.2% North America Share Leading region with $0.9B revenue in 2024 22.4% US Market CAGR US market valued at $0.8B in 2024 Direct-to-Chip Liquid Cooling systems transfer heat away from high- performance processors by circulating fluid directly through cold plates attached to chips. This technology enables much faster and more efficient heat removal compared to traditional air cooling methods, supporting high- density computing needs.

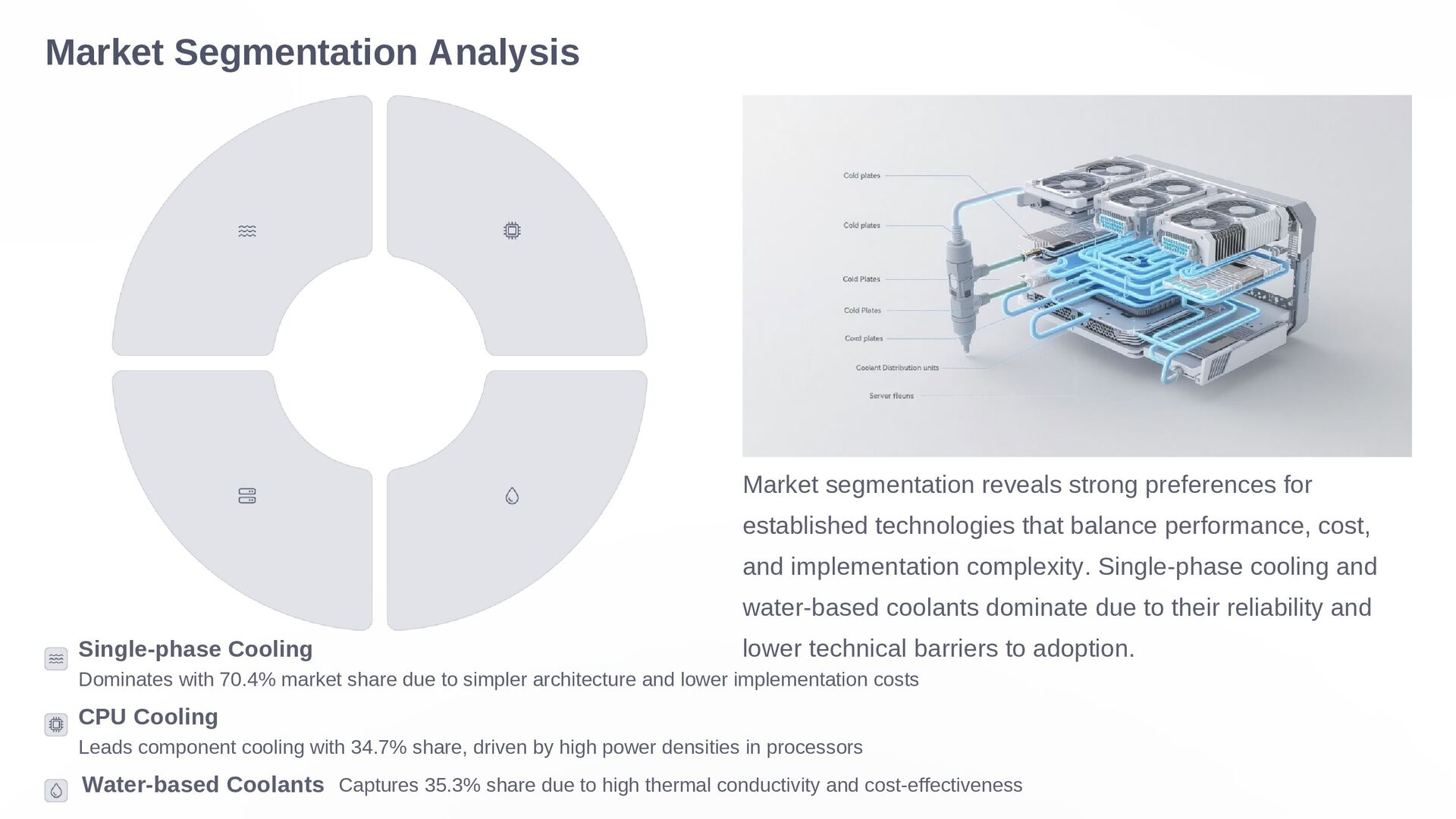

due to simpler architecture and lower implementation costs CPU Cooling Leads component cooling with 34.7% share, driven by high power densities in processors Water-based Coolants Captures 35.3% share due to high thermal conductivity and cost-effectiveness Market segmentation reveals strong preferences for established technologies that balance performance, cost, and implementation complexity. Single-phase cooling and water-based coolants dominate due to their reliability and lower technical barriers to adoption.

a dominant position in 2024, capturing over 37.2% market share with approximately $0.9 billion in revenue. The U.S. market alone reached $0.79 billion and is advancing at a strong CAGR of 22.4%. This leadership is attributed to: Rising demand for energy-efficient cooling in hyperscale facilities Rapid adoption of AI workloads and cloud infrastructure Governmental emphasis on sustainable IT infrastructure Strong R&D ecosystems and early technology adoption The U.S. direct-to-chip liquid cooling market is anticipated to reach approximately $6.0 billion by 2034, expanding at a CAGR of 22.4% during the forecast period from 2025 to 2034.

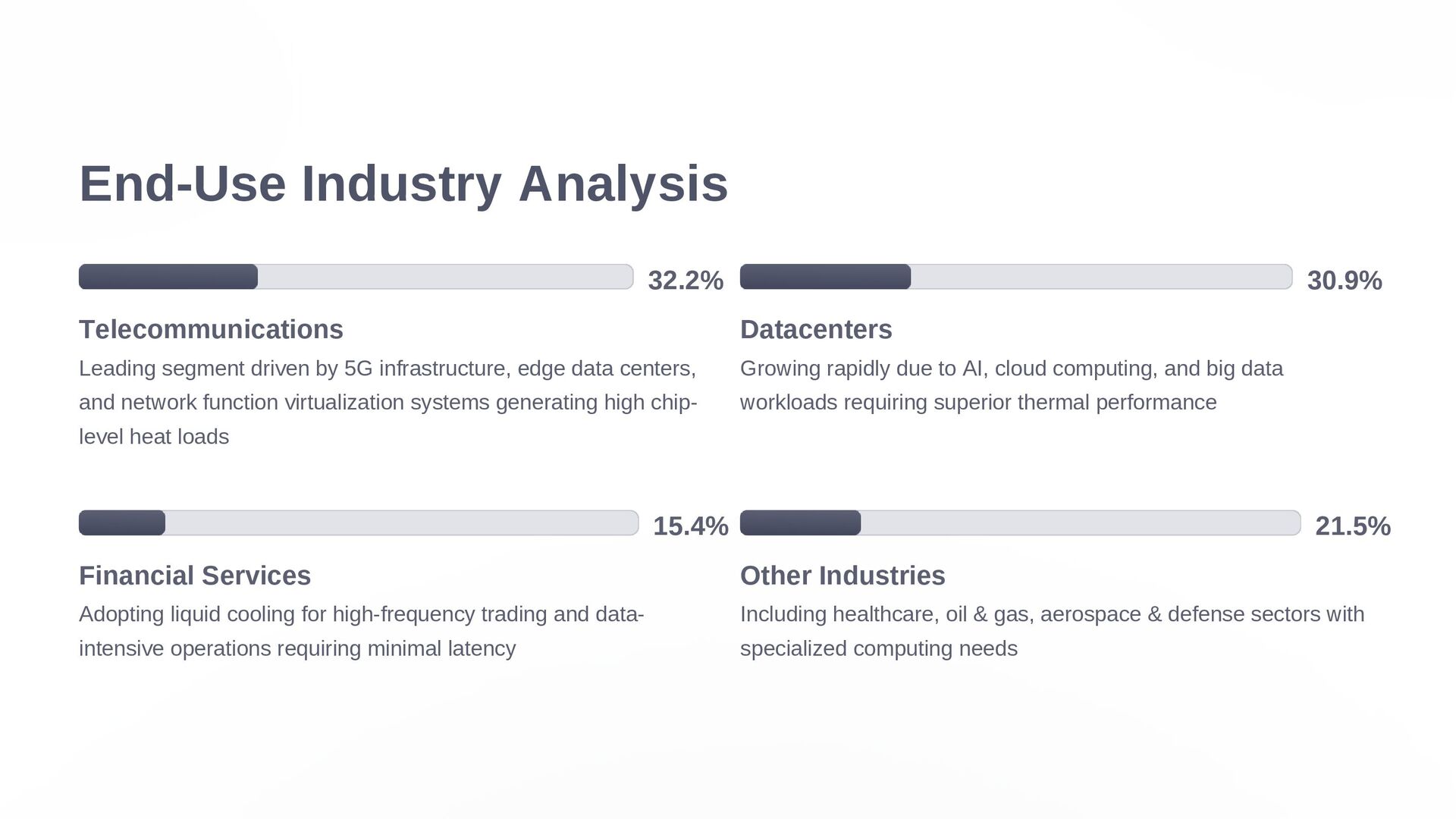

infrastructure, edge data centers, and network function virtualization systems generating high chip- level heat loads 30.9% Datacenters Growing rapidly due to AI, cloud computing, and big data workloads requiring superior thermal performance 15.4% Financial Services Adopting liquid cooling for high-frequency trading and data- intensive operations requiring minimal latency 21.5% Other Industries Including healthcare, oil & gas, aerospace & defense sectors with specialized computing needs

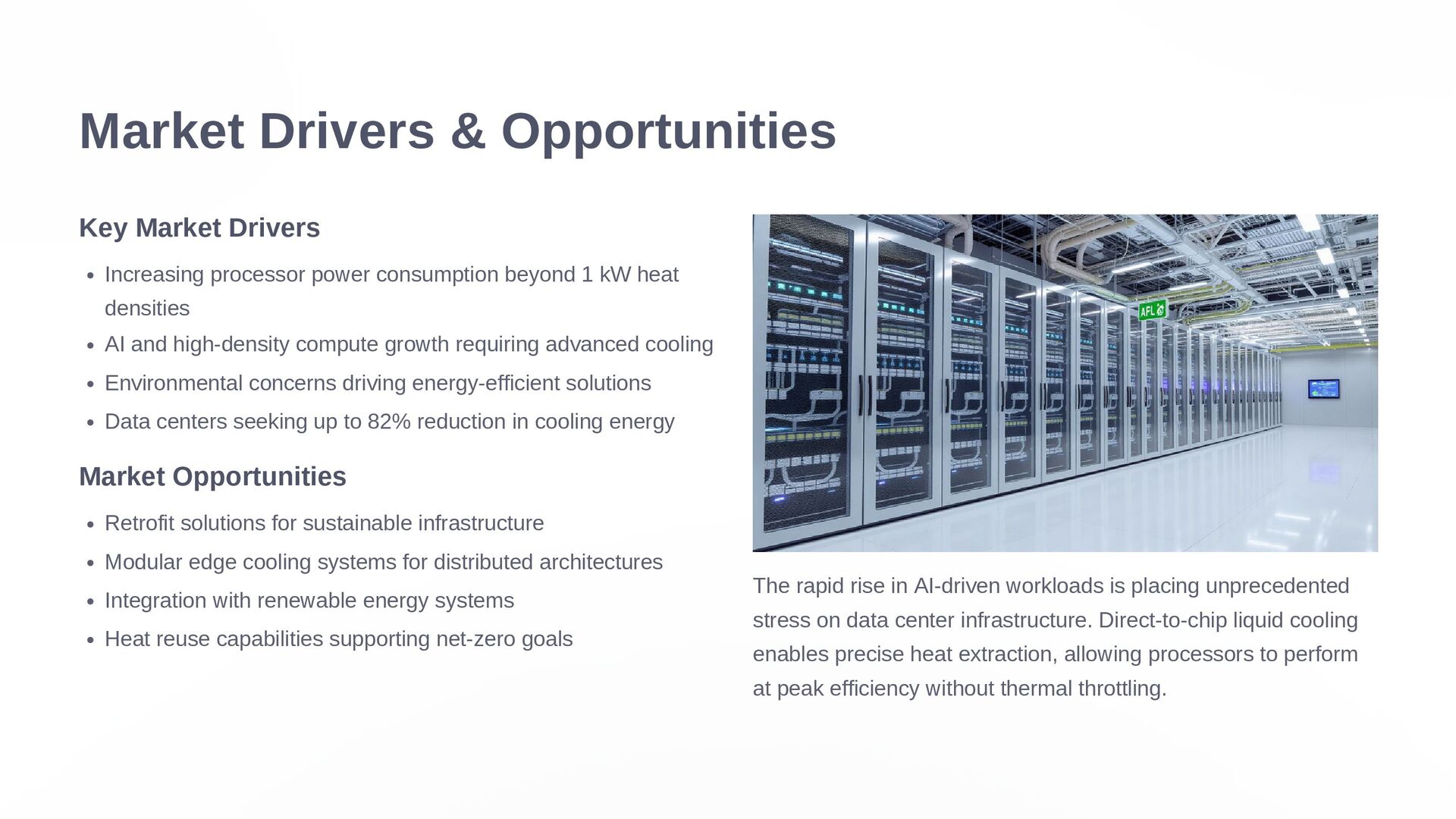

consumption beyond 1 kW heat densities AI and high-density compute growth requiring advanced cooling Environmental concerns driving energy-efficient solutions Data centers seeking up to 82% reduction in cooling energy Market Opportunities Retrofit solutions for sustainable infrastructure Modular edge cooling systems for distributed architectures Integration with renewable energy systems Heat reuse capabilities supporting net-zero goals The rapid rise in AI-driven workloads is placing unprecedented stress on data center infrastructure. Direct-to-chip liquid cooling enables precise heat extraction, allowing processors to perform at peak efficiency without thermal throttling.

advantages, adoption is hindered by high upfront capital requirements for customized cold plates, fluid circulation networks, monitoring sensors, and integration with existing infrastructure. Coolant Management Risks Water-based coolants may introduce risks of corrosion or microbial growth if not properly treated, while dielectric fluids involve higher handling costs and specific safety requirements. Compatibility Issues Integration challenges with certain chip architectures or server designs make custom engineering necessary, creating complexity across multi-vendor hardware ecosystems.

Pioneering force with deep experience in thermal management CoolIT Systems - Strong portfolio of liquid cooling technologies for hyperscale environments ZutaCore - Disrupting with two-phase liquid cooling architecture Vertiv Holdings Co - Expanded thermal management portfolio through acquisitions Iceotope Technologies - Innovative chassis-level liquid cooling approach Recent Developments April 2025: JetCool Technologies introduced SmartSense CDU, handling up to 300kW per rack March 2025: CoolIT launched new cold plate for D2C liquid cooling in data centers March 2025: Accelsius unveiled NeuCool™ two-phase direct-to-chip cooling solution February 2025: ZutaCore appointed executives to support rising global demand June 2024: Asetek formed strategic alliance with FABRIC8 LABS for AI-optimized cold plates

nearly 10x from $2.5B to $24.8B by 2034, driven by increasing computing demands and thermal management challenges Technological Evolution Advancements in two-phase cooling, engineered fluids, and modular systems will enhance efficiency and reduce implementation barriers Sustainability Focus Environmental regulations and corporate ESG goals will accelerate adoption as organizations seek to reduce energy consumption and carbon footprint

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}