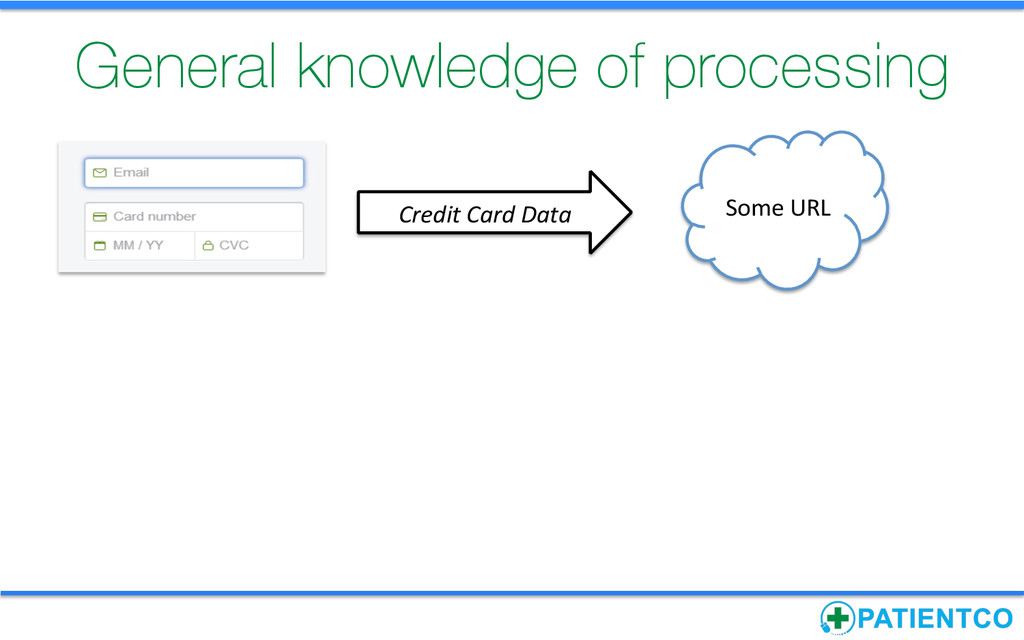

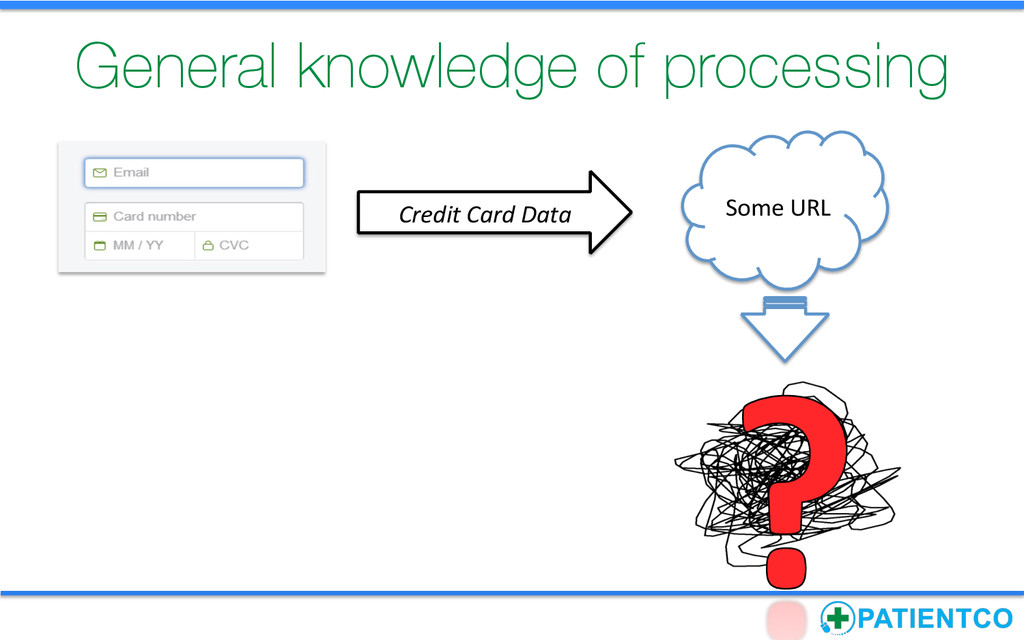

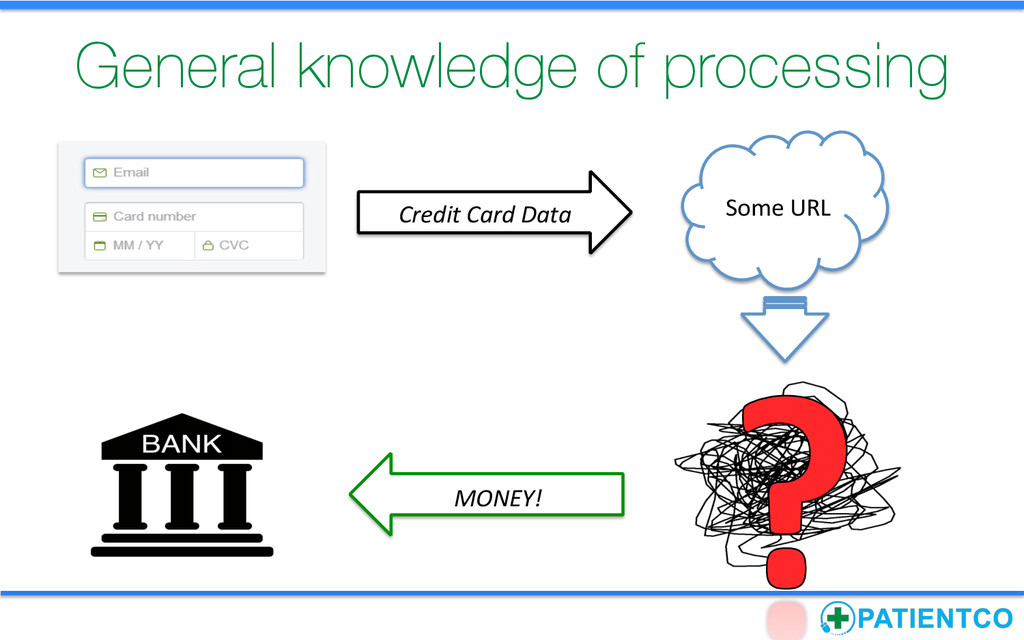

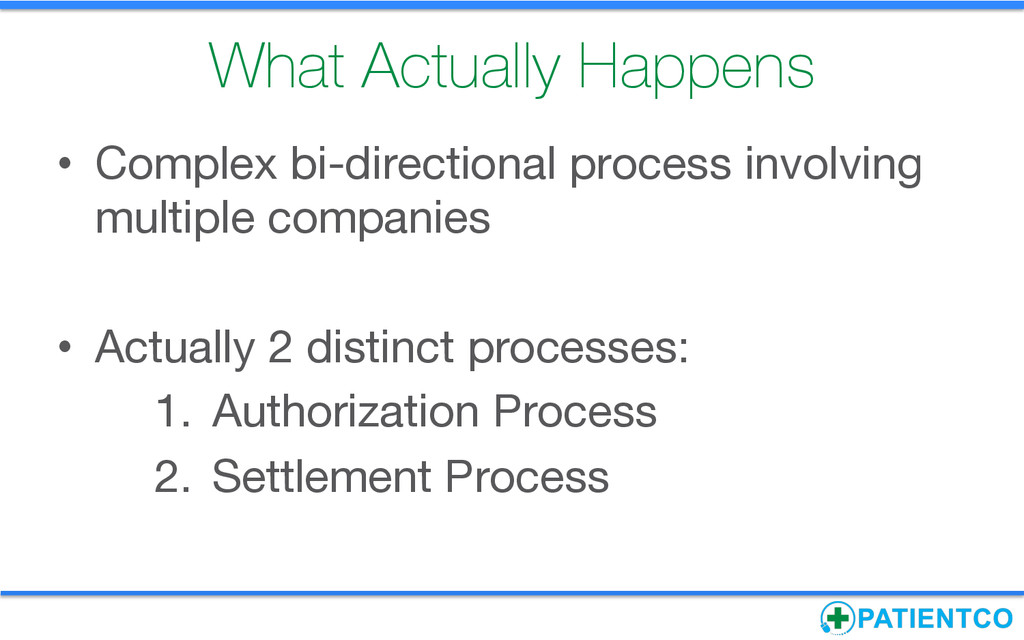

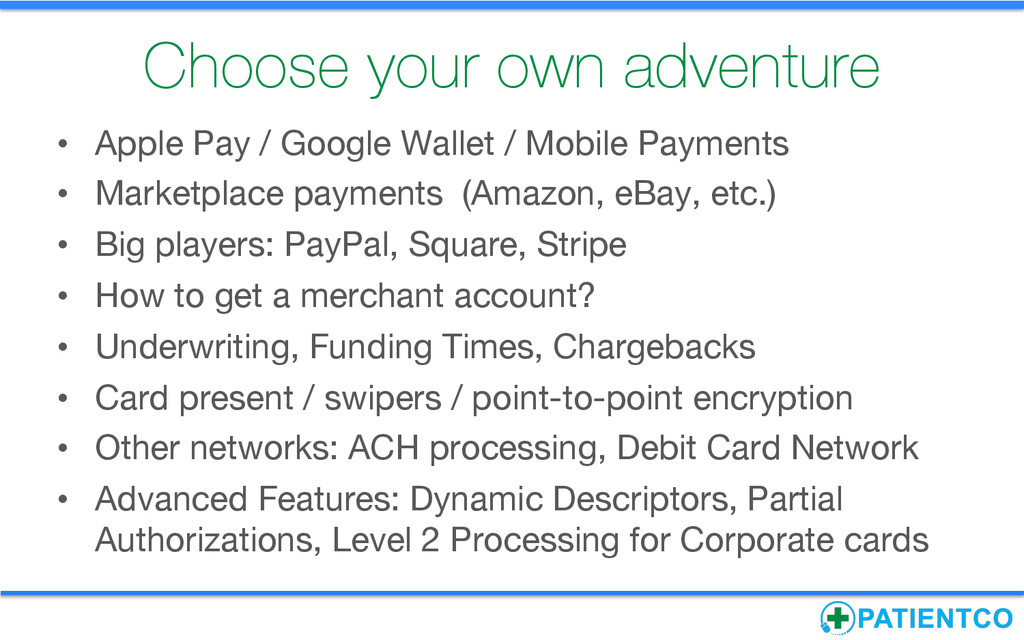

Working on your first payment processing project? Mystified by MIDs, interchange rates, AVS results, PCI, or payment gateways? Curious about Apple Pay or the United States' transition to EMV (chip-and-signature) credit cards? Learn the nuts and bolts of payment processing on the web and walk away with a plethora of resources to use on your next eCommerce or payment processing project. I'll discuss what actually happens behind the scenes as a card is processed and outline best practices – both technical and operational – for achieving a secure, compliant, and robust processing environment.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

![Questions? [email protected] http://www.PatientcoLife.com/ https://joind.in/13743](https://files.speakerdeck.com/presentations/66ecfde14d56473da622d5b46136a89c/slide_49.jpg){kind=link}