Made with <3 by Ammar.

Huge thanks to Andrew Houghton for all of the work he put into this with me.

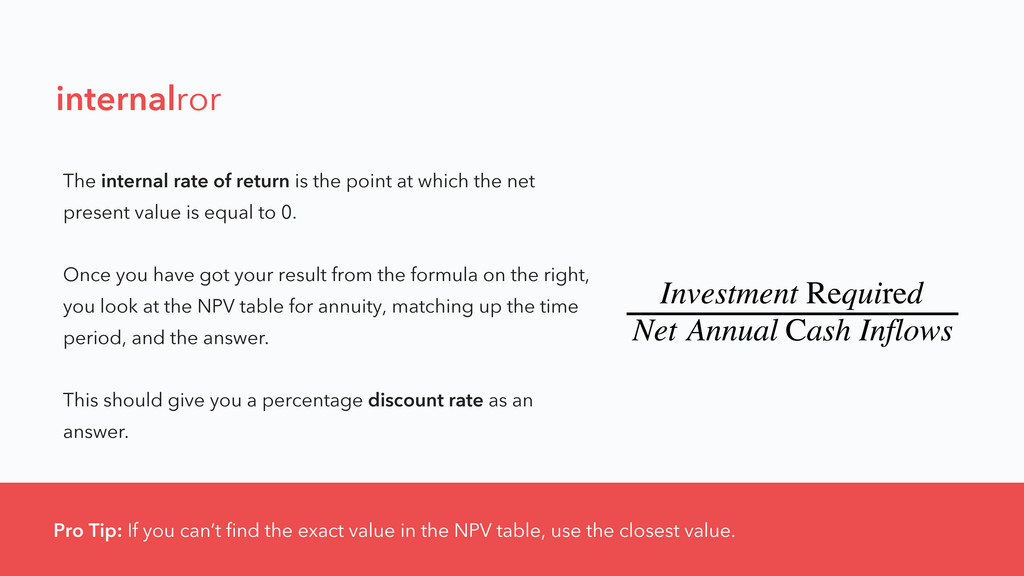

Also, make sure you download the NPV Tables if you're working through examples: http://d.pr/f/ITAC

If you spot any errors, shoot me a message and I'll fix it ASAP.

NB: This is no substitute for solid revision, I'm not responsible for failure / injury / death / the birth of demon babies caused by use of these slides, yada yada yada.

========================================

CONTAINS THE FOLLOWING TOPICS:

========================================

Cost-Volume-Profit Analysis.

Absorption Costing.

Yield Management.

Budgeting.

Investment Appraisal.

Decentralisation.

Strategic Management Accounting.

Strategic Cost Management.

Standard Costs.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}