invest is to see a return (profit) on the investment. n Financial Security: Many people decide to learn more about investing because they want to feel secure financially. n Lifestyle: Earning money through investing can help people afford a desired lifestyle so they can afford those things they bwant`. n Investing can also be a way for people to get their money working for them (instead of having to work for every dollar) to free up time to live the lifestyle they desire.

rely on Social Security (a social welfare program that provides people over the age of 62 monthly payments) and Medicare (a social welfare program that provides older people medical insurance coverage) to retire. n Unfortunately, for people under the age of 35 today, the SSI and Medicare system will likely be bankrupt by the time you reach retirement age so you will likely receive no or very limited benefits. n This means you need to plan for your own retirement early.

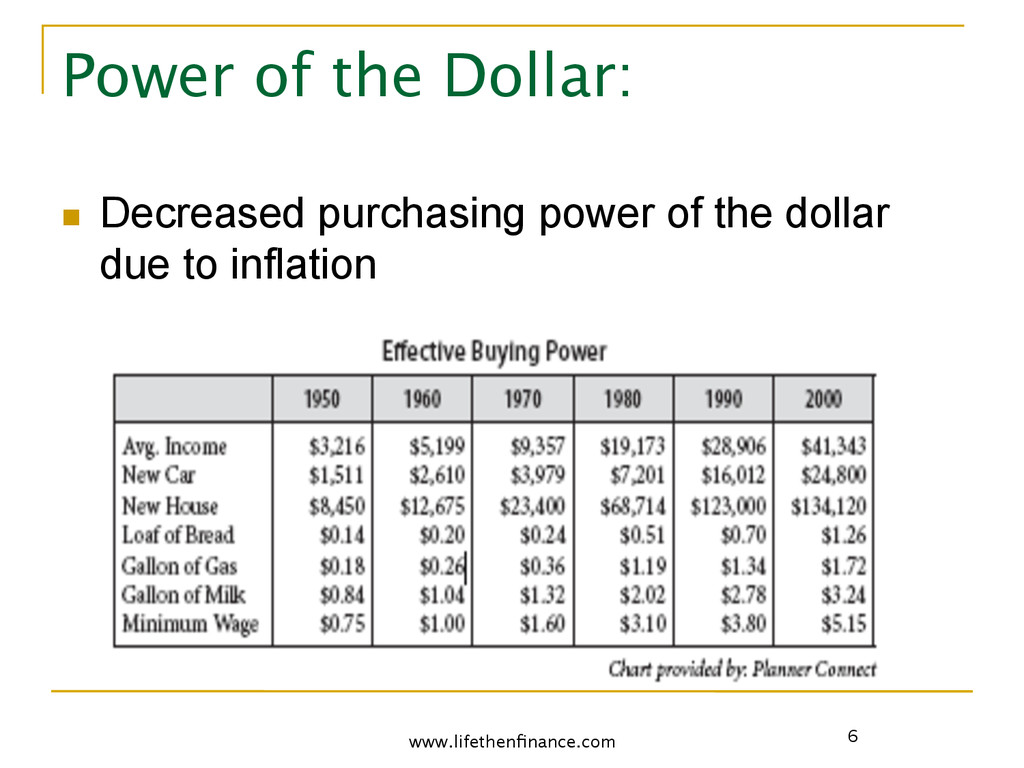

is defined as bto many dollars chasing to few goods`. n When this happens prices go up. n Inflation – many people use a rough 3% figure to calculate the average inflation per year . . . This varies widely.

72 says to divide the interest rate you are receiving on an investment into 72 and the answer is how many years it will take for that money to double. n The earlier you save for retirement the more chances your money has to double.

or credit union that earns interest. n Returns: n Low, typically well below inflation. Currently most savings rates are under 1%. n Benefits: n Able to access money fast and safety of principle. n Risk: n Very low risk–insured by the FDIC banks or by the NCAU for credit unions. n Liquidity: n Can access money instantly; however with larger amounts there may be some delay. n Cost to access money: $0 n Risks: n Having returns lower than inflation rates.

and medium term debt instruments offered by banks and credit unions. n CD`s are similar to savings accounts except they typically have a higher interest yields and have set time lengths. q For example common CD terms are 3 month, 6 month, 1 year, 2 years and 5 years. n Returns: n Low but typically higher than savings accounts. n The more money you have to invest in CDs the larger return you can earn. n A current 1-year CD rate with $10,000 is around 1.4%

Safety of principle and higher return than typical savings accounts. n Risk: n Very low risk of loss of capital because they are insured by the FDIC banks or by the NCAU for credit unions. n However the longer term CD you choose the higher risk that it will earn a return less than inflation. n Liquidity: n CD`s vary on their liquidity. Cost to access money: $0 as long as you wait until maturity date. n If you sell before the CD bmaturity date` you will likely pay penalties. n Note: n Money Market accounts have similar qualities but are typically shorter in nature, often maturity dates of 1 year or less.

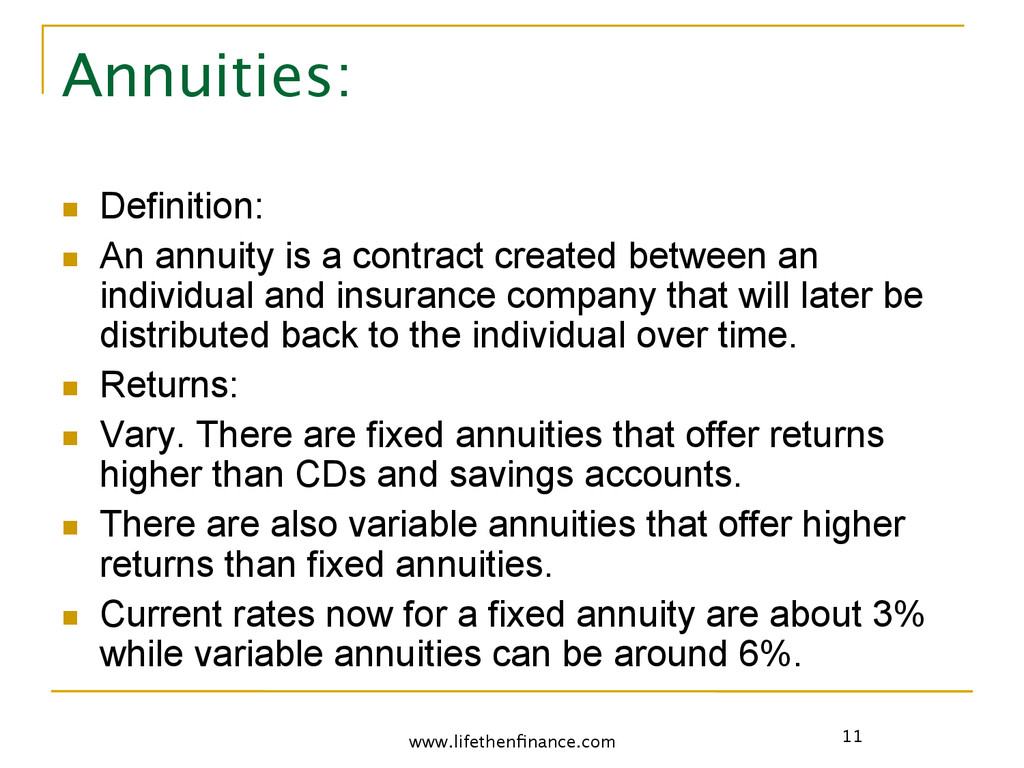

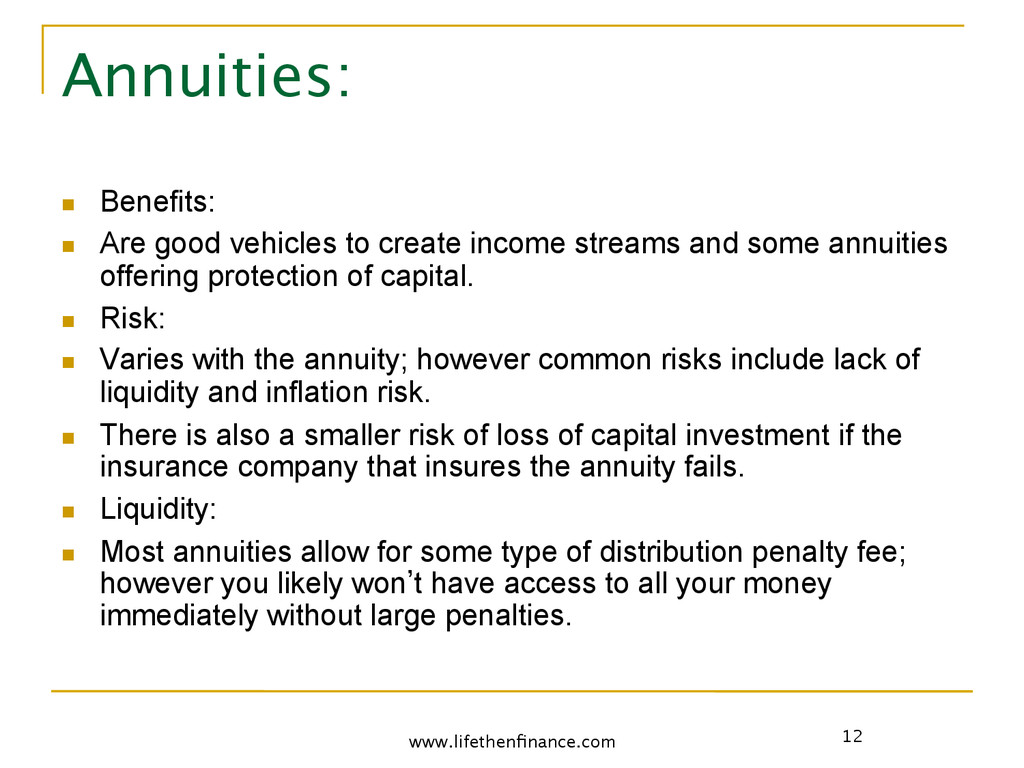

contract created between an individual and insurance company that will later be distributed back to the individual over time. n Returns: n Vary. There are fixed annuities that offer returns higher than CDs and savings accounts. n There are also variable annuities that offer higher returns than fixed annuities. n Current rates now for a fixed annuity are about 3% while variable annuities can be around 6%.

create income streams and some annuities offering protection of capital. n Risk: n Varies with the annuity; however common risks include lack of liquidity and inflation risk. n There is also a smaller risk of loss of capital investment if the insurance company that insures the annuity fails. n Liquidity: n Most annuities allow for some type of distribution penalty fee; however you likely won`t have access to all your money immediately without large penalties.

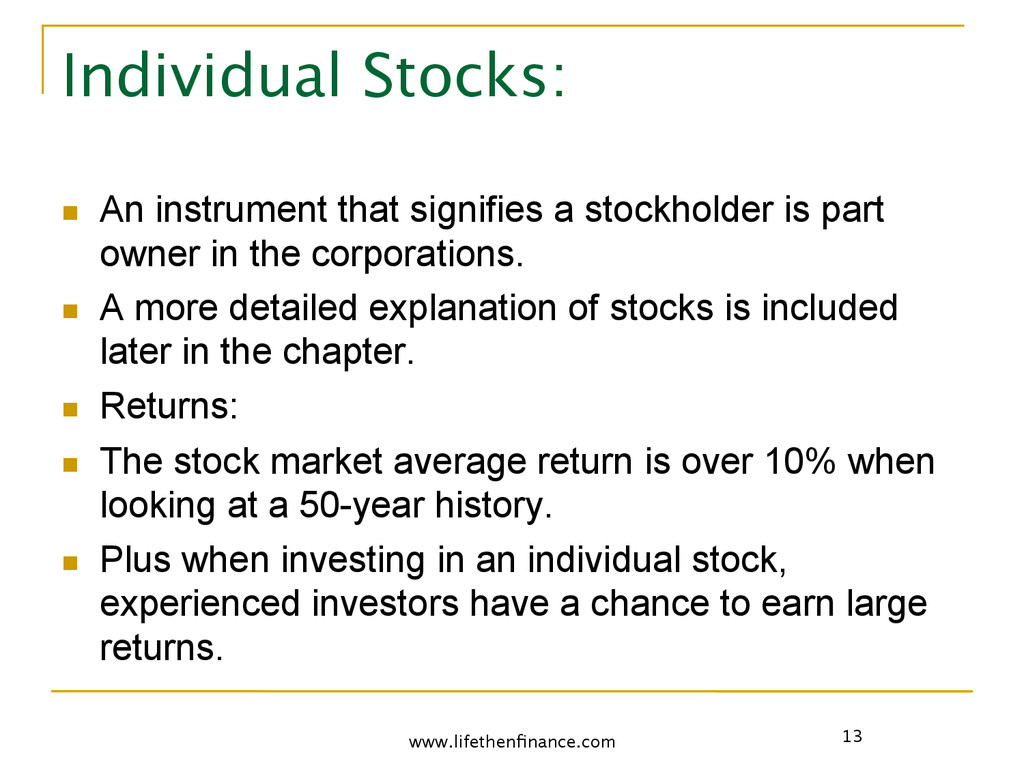

stockholder is part owner in the corporations. n A more detailed explanation of stocks is included later in the chapter. n Returns: n The stock market average return is over 10% when looking at a 50-year history. n Plus when investing in an individual stock, experienced investors have a chance to earn large returns.

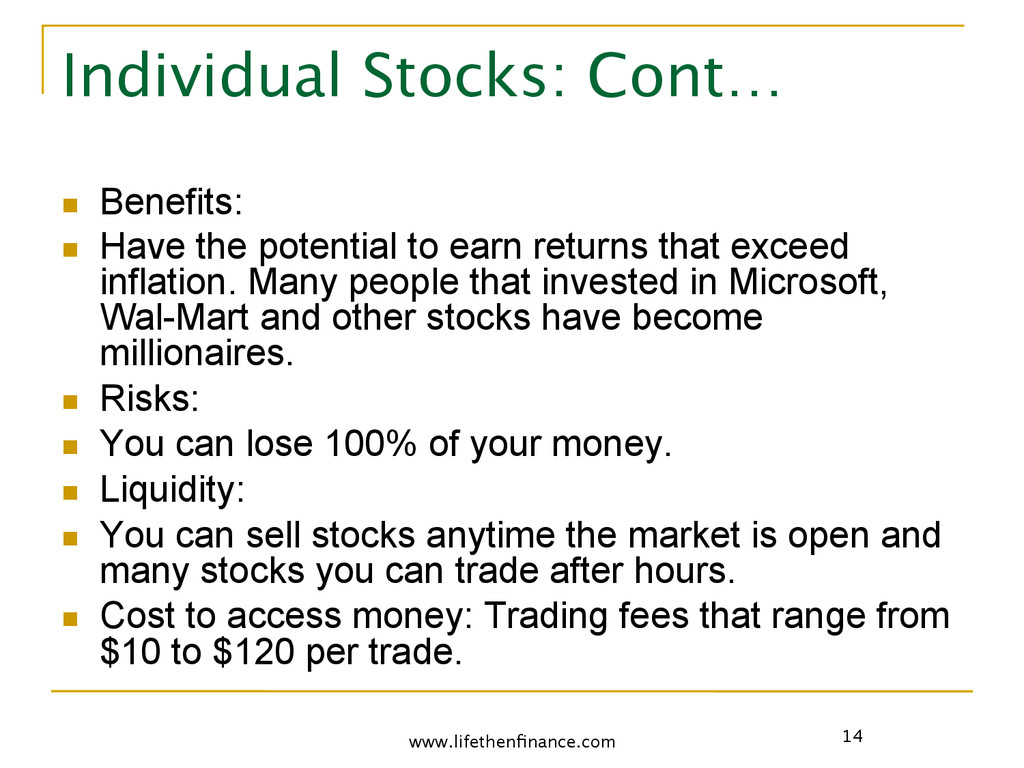

potential to earn returns that exceed inflation. Many people that invested in Microsoft, Wal-Mart and other stocks have become millionaires. n Risks: n You can lose 100% of your money. n Liquidity: n You can sell stocks anytime the market is open and many stocks you can trade after hours. n Cost to access money: Trading fees that range from $10 to $120 per trade.

company and raises money from shareholders then invest that money into assets that aligns with the stated investment objective. n Returns: n Vary greatly upon type of mutual fund investment. n Benefits: n You have a wide selection of mutual funds to choose from to meet a variety of investment goals. n The returns that one can expect are tied to the amount of risk one is willing to take.

depending on the type of mutual fund you invest in however you can lose a substantial portion of your capital investment. n Liquidity: n Most mutual funds are liquid and like shares can be sold the same or next day at NAV (Net Asset Value). n There are different types of mutual fund classes that you can choose, some will penalize you for an early withdrawal.

debt. The investor receives a contract from the organization borrowing money that they will repay borrowed money with interest at fixed intervals. n Returns: n There are a wide variety of bonds available. Bonds have a price and yield however; for this example the yield (interest) will be explored. US Treasury bonds are considered the safest and currently earn a return under 1%. n Other form of municipal bonds (bonds issued by cities, counties, etc) varies depending on safety of investment but typically range from 2% to 5%. n Corporate bonds again vary depending on risk of investment and currently range from 4% to 20% for very high-risk bonds (also know as bjunk bonds`).

than stocks and are often used by investors to stabilize value of their portfolios. n Income is received at regular intervals and there may be tax advantages with some bonds. n Risk: n Varies depending on bond. If you choose a high-risk bond and the company that issued the debt goes bankrupt you could lose your entire investment – Default risk. n Interest rate risk bond prices have an inverse relationship to interest rates. When one rises, the other falls so if you sell before it matures you could lose money. n There is also inflation risk. n Liquidity: n Not as liquid as stock investments and if a bond is downgraded or in default there could be trouble getting out of the investment.

from buying your own home, to a rental property, to commercial buildings. n Benefits: n There are several benefits associated with real estate: appreciation (property goes up in value), cash flow (rental and income producing properties), potential tax benefits and leverage. n Risks: n Depreciation, housing prices fall. Most people purchase real estate with a loan – if at anytime you lose a job or have other financial hardships you may not be able to pay the loan back.

you may have to short sell the home (sell it for less than the house is worth) or have your home foreclosed (the lender takes back the home) and in both cases you would lose the money you invested in the home, plus it would negatively impact your credit rating. n Benefits: n Rental property you can benefit from appreciation (prices going up), cash flow (income from the rents you collect) and potential tax benefits. n The benefits of owning a home you live in include appreciation and potential tax benefits. n Liquidity: n In good real estate markets you can sell within a few months. n In bad real estate markets it may take years to sell at a deep discount. Cost of sale about 8% of the home sales price.

elimination of pension and SSI benefits it is now critical that you become an educated investor. n Investing is buying assets that you think will go up in value. n Assets are things like real estate, stocks, gold, or a business to name a few. n Assets do not always increase in value so anytime you invest your risk losing some or all of your money. n It`s important to become an educated investor and get your money working for you.

ponzi scheme is an investment fraud when people invest and their return on the investment is paid from the money of new investors. n Example: The Bernie Madoff Scandle

option, and futures markets are just a few. n The stock market is one piece of the overall U.S. financial market. n When comparing it to all the other markets, the stock market offers the best returns for a young adult investor. It`s a great place to get started and get involved in investing

market is a market for the trading of company stock and other financial securities. n A stock is genuine partial ownership in a company. n The stock of companies in the United States is listed on several different exchanges; for example, the New York Stock Exchange (NYSE) and the NASDAQ

are bought and sold by bidding. When the bid price (price buyer is willing to buy at) and ask price (price seller is willing to sell at) match, a sale takes place. n This means that prices can fluctuate day-to- day, and the worth of the stock you own can change, depending on demand for the company`s stock.

market moves based on prices at which people are offering to purchase a stock. n A stockbroker is the middleman. He sells or buys stock on your behalf. n The reason is that stock transactions must be made between two members of the exchange—you can`t just walk into a stock exchange and start trading stocks. n So, you`re going to be using a broker to invest in stocks.

stockbrokers may also offer financial advice to their clients on which stocks to buy. (Bare in mind, they`re on commission—everyone`s after your hard- earned money!) n Therefore, a basic stock market transaction works like this: n You Broker Electronic Exchange Broker You

and Demand: n This is a fundamental rule of economics, and what you need to know is that the stock market runs according to this rule. n Supply is the quantity of stock shares available for sale. n Demand is the number of stock investors are willing to purchase at a given price. n If supply is greater than demand, in the case of stocks, then the price will naturally fall. n If supply is less than demand, the price will go up. n This basically explains why stocks prices go up and down, but the reason for greater interest (or lack of interest) in a stock is more related to the company`s performance, or gossip about the company`s future, and technical factors.

Risk and Return: n Just like supply and demand, risk and return have a correlative relationship, or at least they should if you`re getting a good deal. n If you`re investing in something with low risk, then you probably won`t be expecting high returns. n The opposite is true of high-risk ventures, where you would expect higher returns in exchange for risking your money (which you could lose!). n For instance, if you invest your money in a brand new company that does not have a proven track record–that is a high risk investment. n That company could easily go out of business, and you would lose everything. On the other hand, it could be successful, and you would make a lot of money. n Once you have established a solid savings account and have a lot of knowledge on how to choose individual stocks, it`s OK to allocate a small portion of your portfolio to riskier investments, but not before!

n Owning a stock makes you a co-owner of the company. n With ownership, you gain a voice in the company`s business. n You can vote at meetings and take a real interest in the inner workings of the company you invest in. n There is an important difference, though: llimited liability.z if something bad happens in your company, they can`t haul you off to prison for it (just think Martha Stewart being carted off to jail in handcuffs!). n The people in your company who break the law are the only ones who go to jail for it, not you. n The most that can happen to you is your stock becomes worthless.

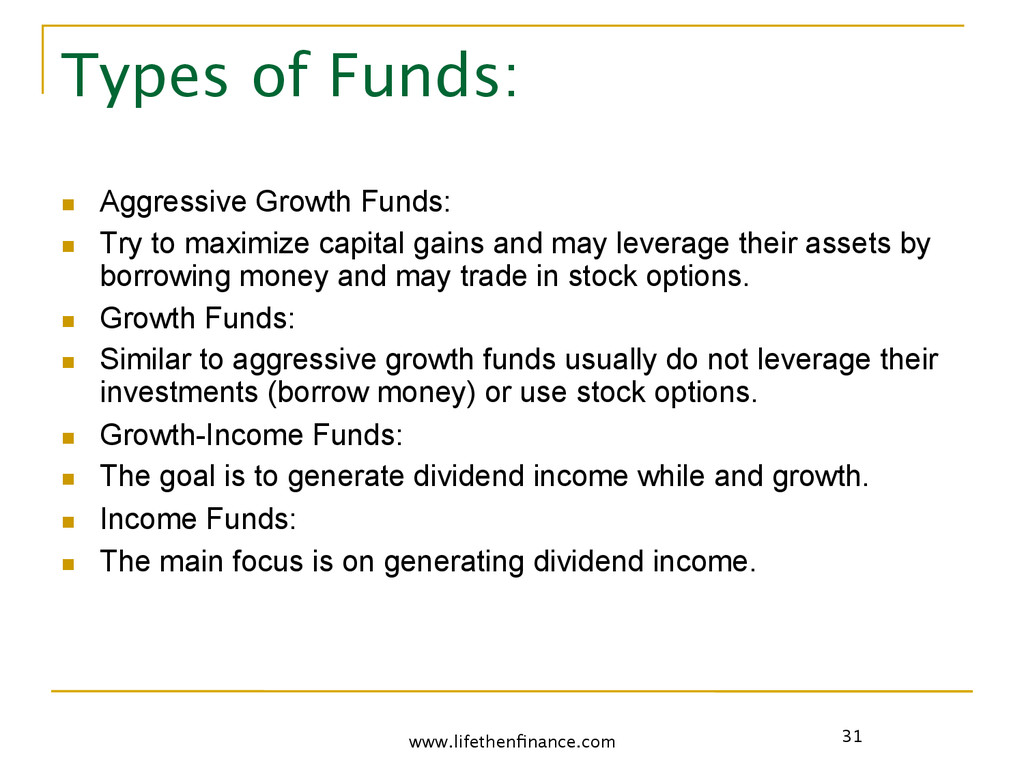

Try to maximize capital gains and may leverage their assets by borrowing money and may trade in stock options. n Growth Funds: n Similar to aggressive growth funds usually do not leverage their investments (borrow money) or use stock options. n Growth-Income Funds: n The goal is to generate dividend income while and growth. n Income Funds: n The main focus is on generating dividend income.

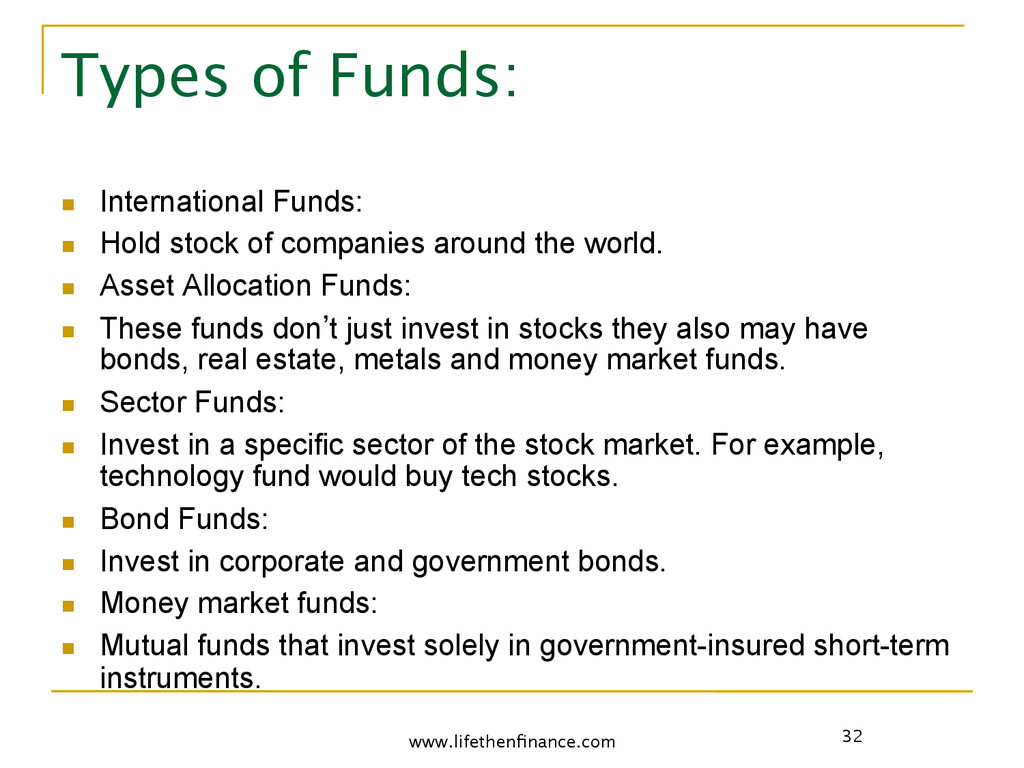

stock of companies around the world. n Asset Allocation Funds: n These funds don`t just invest in stocks they also may have bonds, real estate, metals and money market funds. n Sector Funds: n Invest in a specific sector of the stock market. For example, technology fund would buy tech stocks. n Bond Funds: n Invest in corporate and government bonds. n Money market funds: n Mutual funds that invest solely in government-insured short-term instruments.

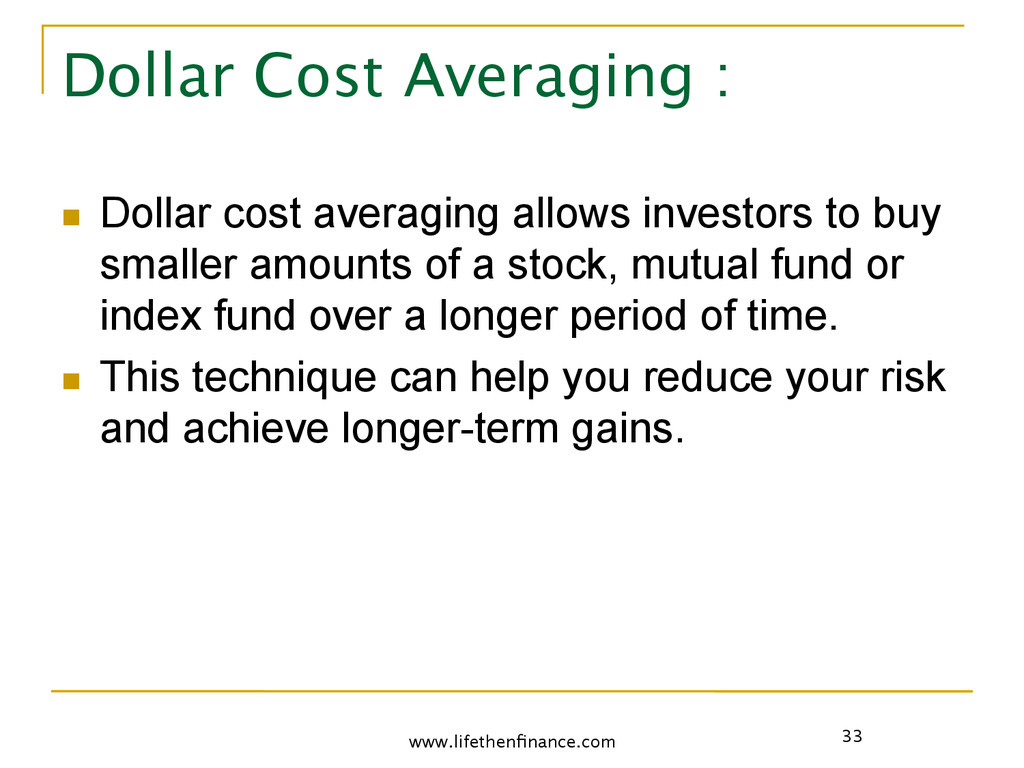

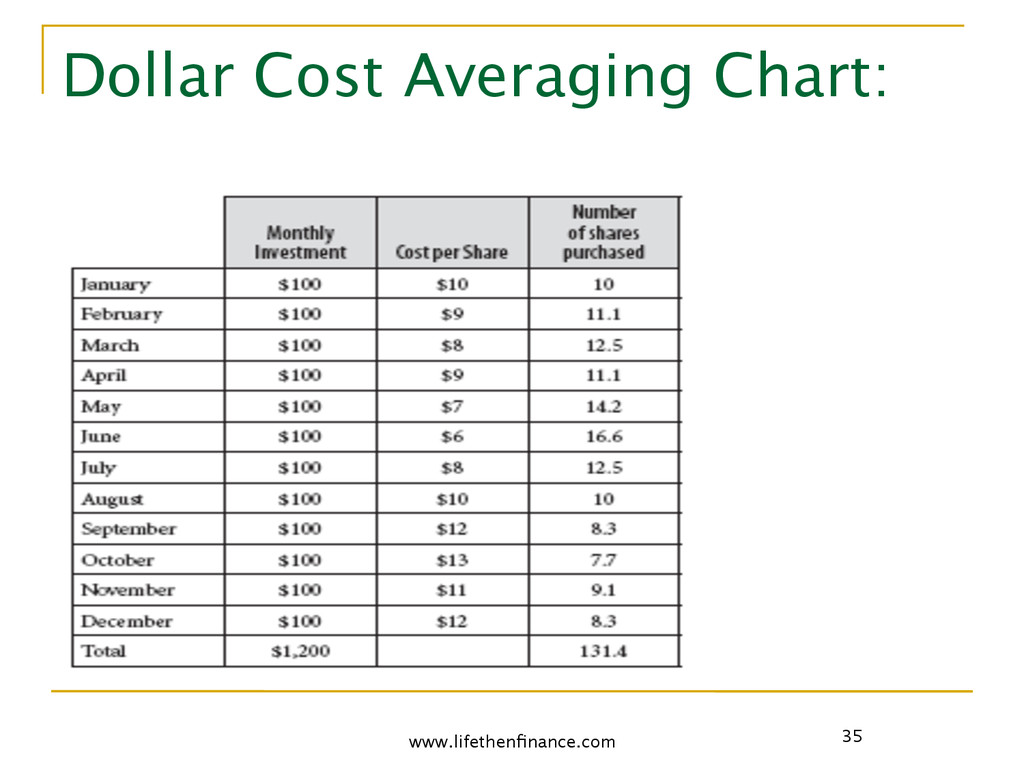

allows investors to buy smaller amounts of a stock, mutual fund or index fund over a longer period of time. n This technique can help you reduce your risk and achieve longer-term gains.

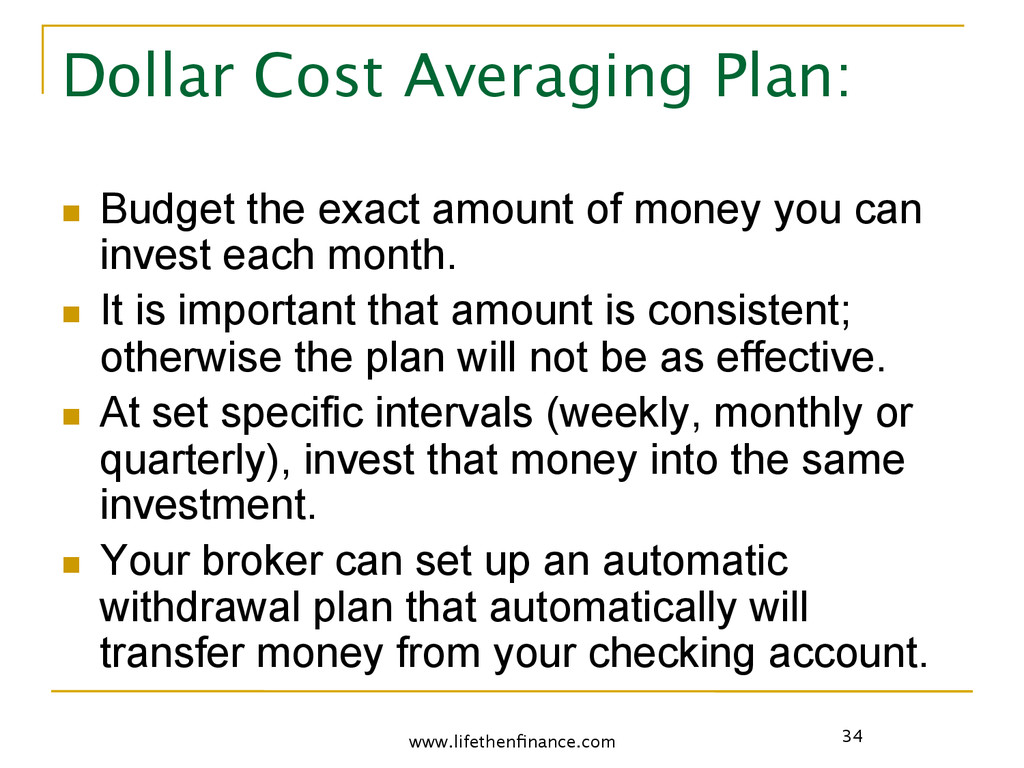

amount of money you can invest each month. n It is important that amount is consistent; otherwise the plan will not be as effective. n At set specific intervals (weekly, monthly or quarterly), invest that money into the same investment. n Your broker can set up an automatic withdrawal plan that automatically will transfer money from your checking account.

were to invest $100 per month you would own 131 shares after one year. n Your investment would of increased in value $376 n If you did not follow a dollar cost averaging plan and purchased n $1,200 worth of shares at once, in January, your return would be $240. You would own 120 total n Shares ($10 cost per share divided by $1,200 investment = 120 total shares)

Account, designed for a person to set aside money each year towards retirement. n There are two types of IRA`s traditional and Roth. n Both types of IRA`s have early withdrawal policies. n Traditional IRA n An IRA that you set aside pre-tax income and must pay taxes on the income upon withdrawal of the money. n Roth IRA: n An IRA that you set aside after-tax income and you do not pay taxes upon withdrawal of the money.

IRA where a person pays taxes on when they withdraw and they are able to invest pretax dollars. n The main difference is that a 401k is employer sponsored and there are different contribution limits. n Some employers will match the amount of the contribution the employee invests.

payment. n Property Taxes n Each area has different tax rates, so these can vary from place to place. They are typically between 1% and 3% of the purchase price. n Insurance : This would protect the homeowner against such perils as fire, wind, and earthquake damage. n It`s important to have, and some lenders will not allow a mortgage on an uninsured property. n Contact an insurance agent for a rough quote on potential homes. In states like Florida, a resident pays a lot higher insurance premiums after the recent major hurricanes.

dues: n Related to condominium, town home or planned unit developments, this could be a monthly or annual fee. n Maintenance: n This expense will be directly affected by the age and condition of the property, so you might need to estimate these costs. n The real estate agent or a registered home inspector can help, or you could ask a friendly builder or knowledgeable family member to take a look. n Generally, newer, well-kept properties will require less maintenance.

the Buyer: n Loan closing costs: 2.5% of the loan amount n For the Seller: n Closing costs: around 7% to 8% of selling price; Sellers pay for a full service real estate agent commission, which is negotiable, but accounts for 5% to 6% in most areas n Careful and considerate planning of your budget will be key to your success in real estate.

have the enviable ability to control a property of greater value than the cash you invested. n Leverage is achieved through borrowing money, typically from a financial institution. n For instance, when you purchase a $100,000 property, most people get a loan for the majority of that amount. q They may have $20,000 to use as a down payment, and then borrow the remaining 80% from a mortgage company. q The $80,000 is the loan and is referred to as the principle balance. q This allows you to control a much larger asset, and pay down the 80% loan over time (mortgage payments).

n Paying down the principle balance over time will give you predictable, steadily increasing equity growth over time. n Each time you make a mortgage payment, you are paying down part of the balance you owe. n It`s like a savings account built into home ownership. n Tax benefits: n There are many tax benefits available to real estate owners. Check with your tax advisor to find out more.

This is a real estate term for the increase in value of land and buildings. n If you purchase a $200,000 house, for example, and it appreciates 10%, your house value is now $220,000. n And if it appreciates 10% again the next year, the value grows to $242,000. n Higher return on investment potential: n Due to the leverage you have with real estate investing and the fact your investment appreciates on the total value of the property, your ROI is much higher than other forms of investing. n If you purchased $10,000 worth of stocks and you get a 15% return, you earned $1,500 for the year. n This also greatly increases your risk. n Cash flow: n Rental property owners are able to generate cash flow via the monthly income from their tenants (discussed further in this chapter`s section on owning a rental property).

you need to sell a property it can take years depending on the market conditions. n When it is a strong market most communities average 2 – 6 months to sell. n When it is bad market conditions the property can be listed for years before it sells. n Change in loan market: n Lenders can change their rules at any point. This can affect future purchasers and your ability to sell the property.

n When market conditions change things can turn quickly. n When owning a property it is important to look at the long-term outlook of the national market and your local community. n Maintenance: n Repairs on a home can be quite costly. n Ensure you have enough money saved and the right insurance so you are prepared.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}