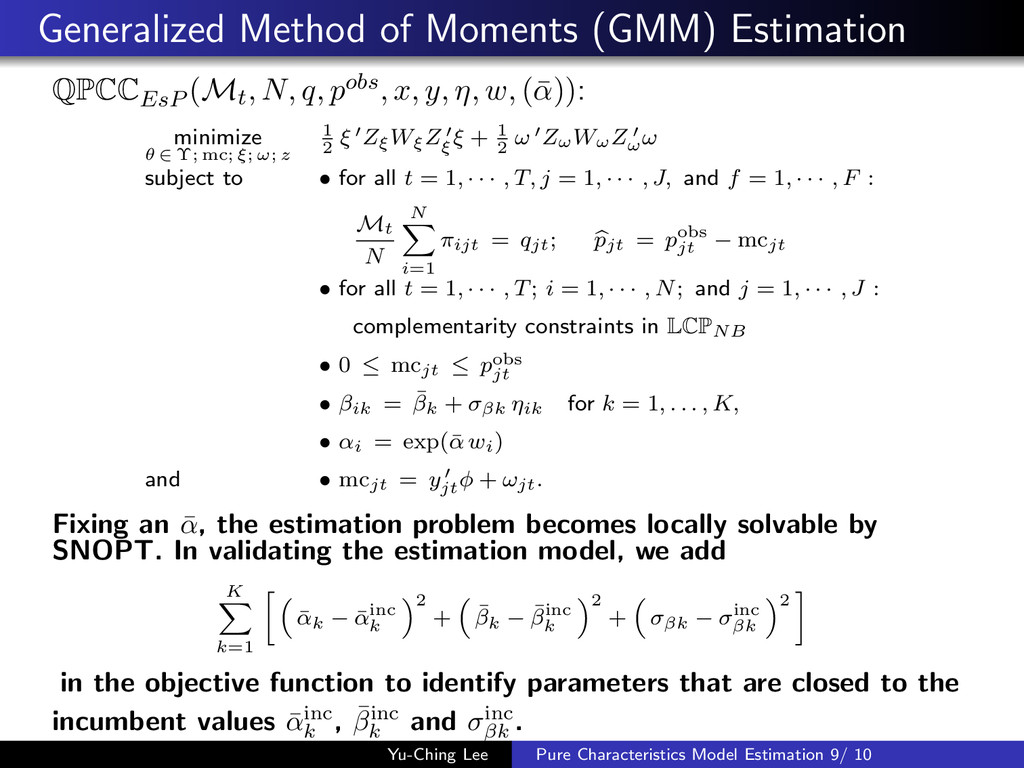

N, q, pobs, x, y, η, w, (¯ α)): minimize θ ∈ Υ; mc; ξ; ω; z 1 2 ξ ′ZξWξZ ′ ξ ξ + 1 2 ω ′ZωWωZ ′ ω ω subject to • for all t = 1, · · · , T, j = 1, · · · , J, and f = 1, · · · , F : Mt N N ∑ i=1 πijt = qjt; pjt = pobs jt − mcjt • for all t = 1, · · · , T; i = 1, · · · , N; and j = 1, · · · , J : complementarity constraints in LCPNB • 0 ≤ mcjt ≤ pobs jt • βik = ¯ βk + σβk ηik for k = 1, . . . , K, • αi = exp(¯ α wi) and • mcjt = y ′ jt ϕ + ωjt. Fixing an ¯ α, the estimation problem becomes locally solvable by SNOPT. In validating the estimation model, we add K ∑ k=1 [ ( ¯ αk − ¯ αinc k ) 2 + ( ¯ βk − ¯ βinc k ) 2 + ( σβk − σinc βk ) 2 ] in the objective function to identify parameters that are closed to the incumbent values ¯ αinc k , ¯ βinc k and σinc βk . Yu-Ching Lee Pure Characteristics Model Estimation 9/ 10

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}