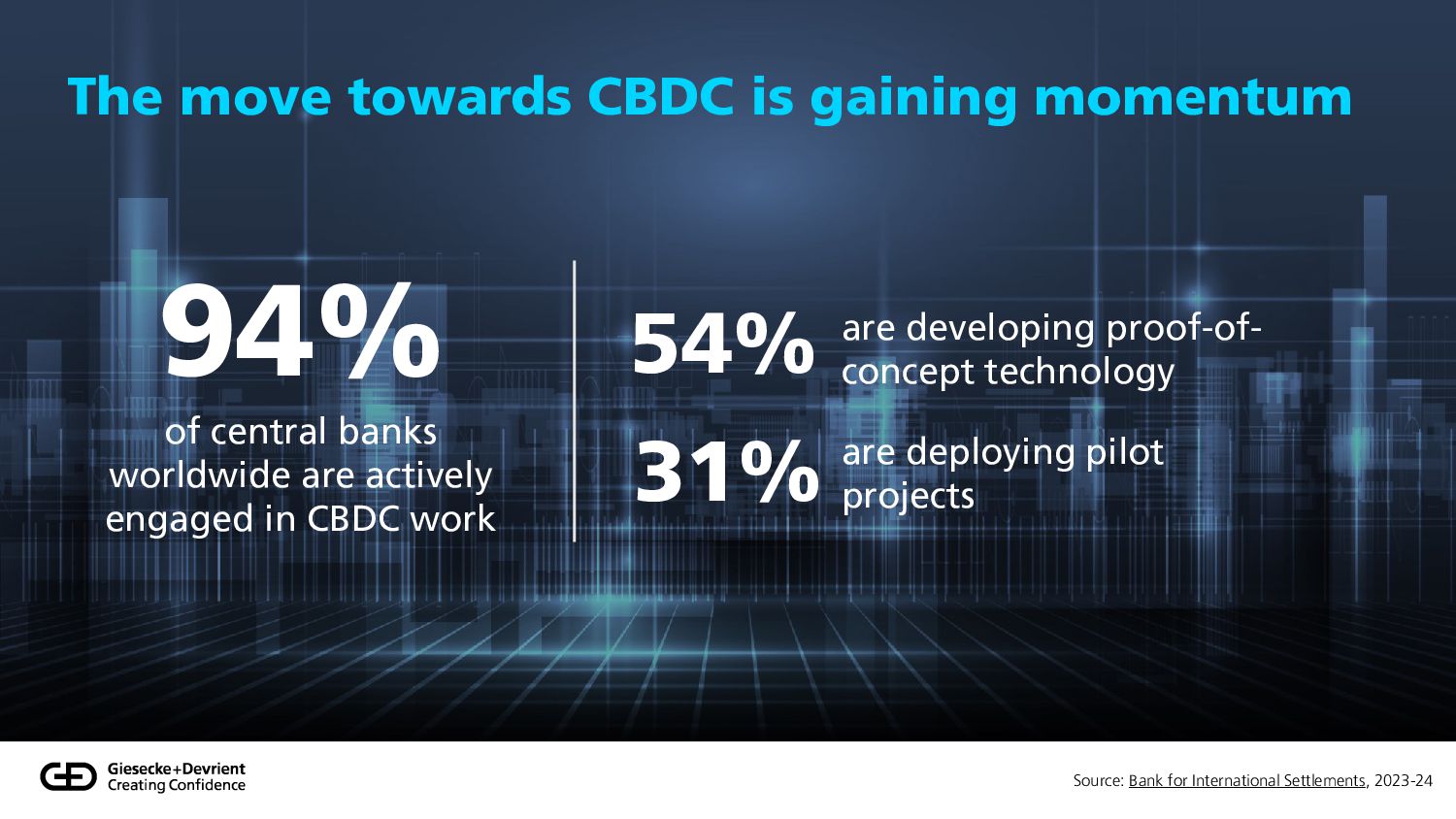

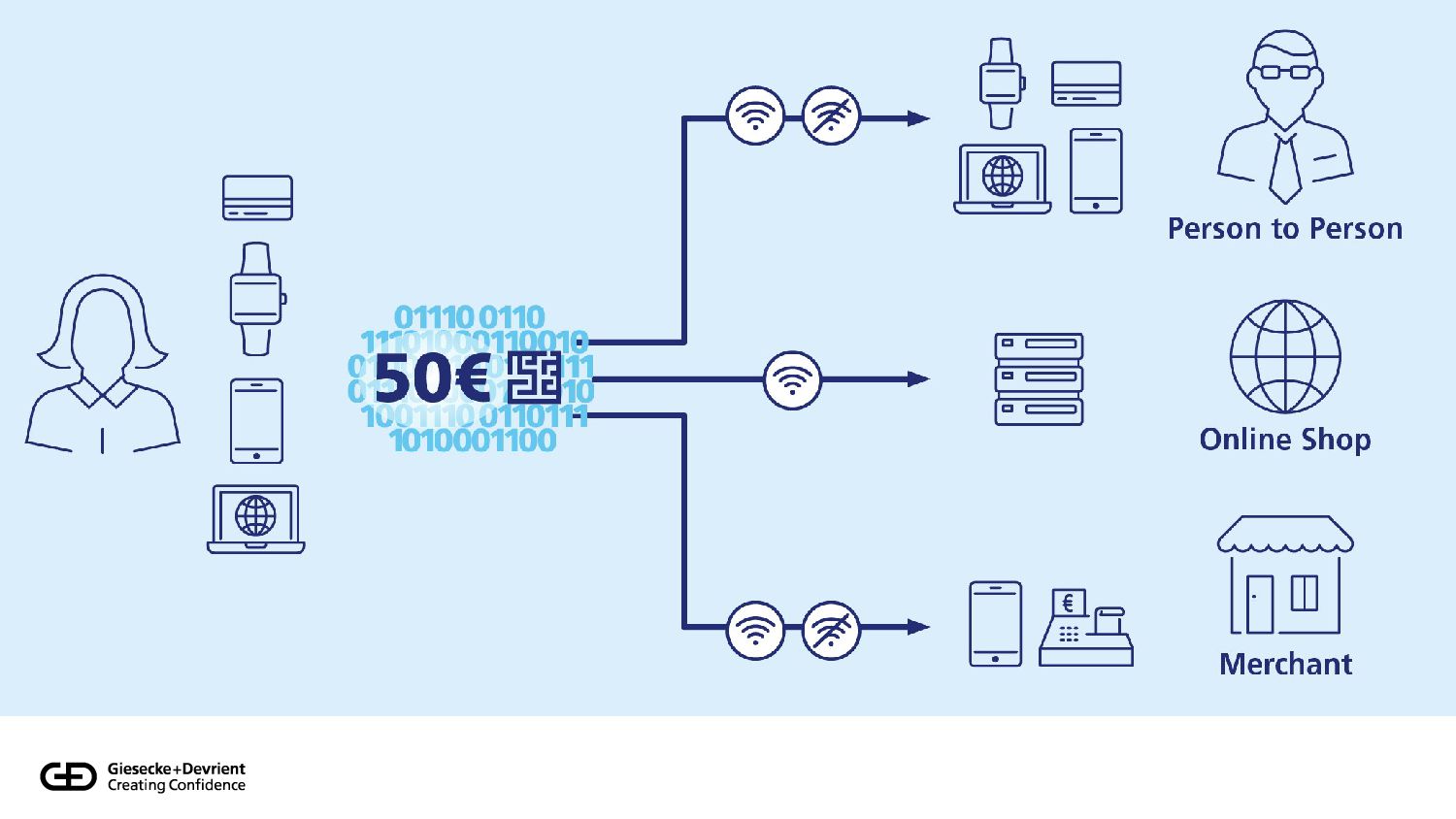

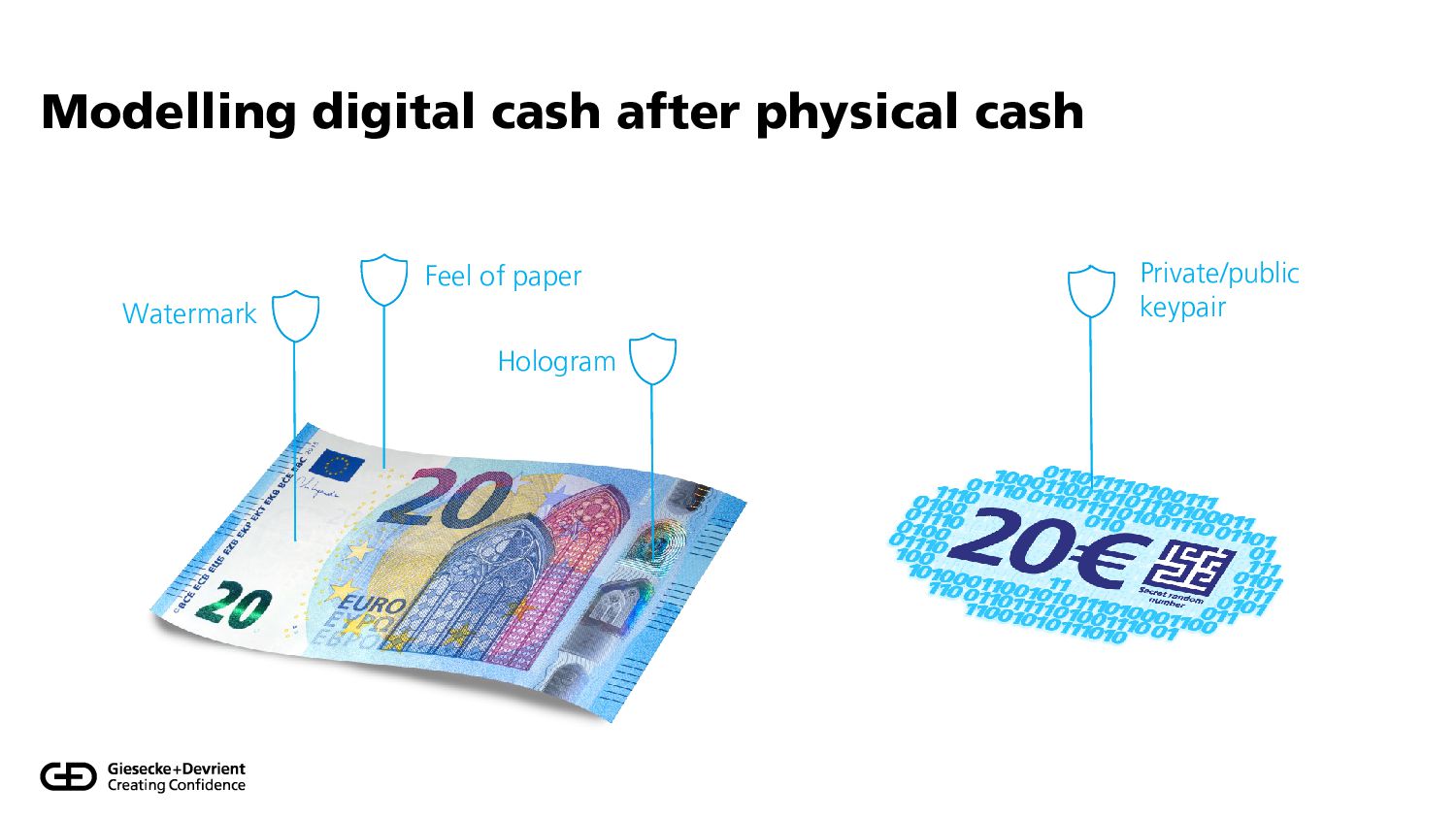

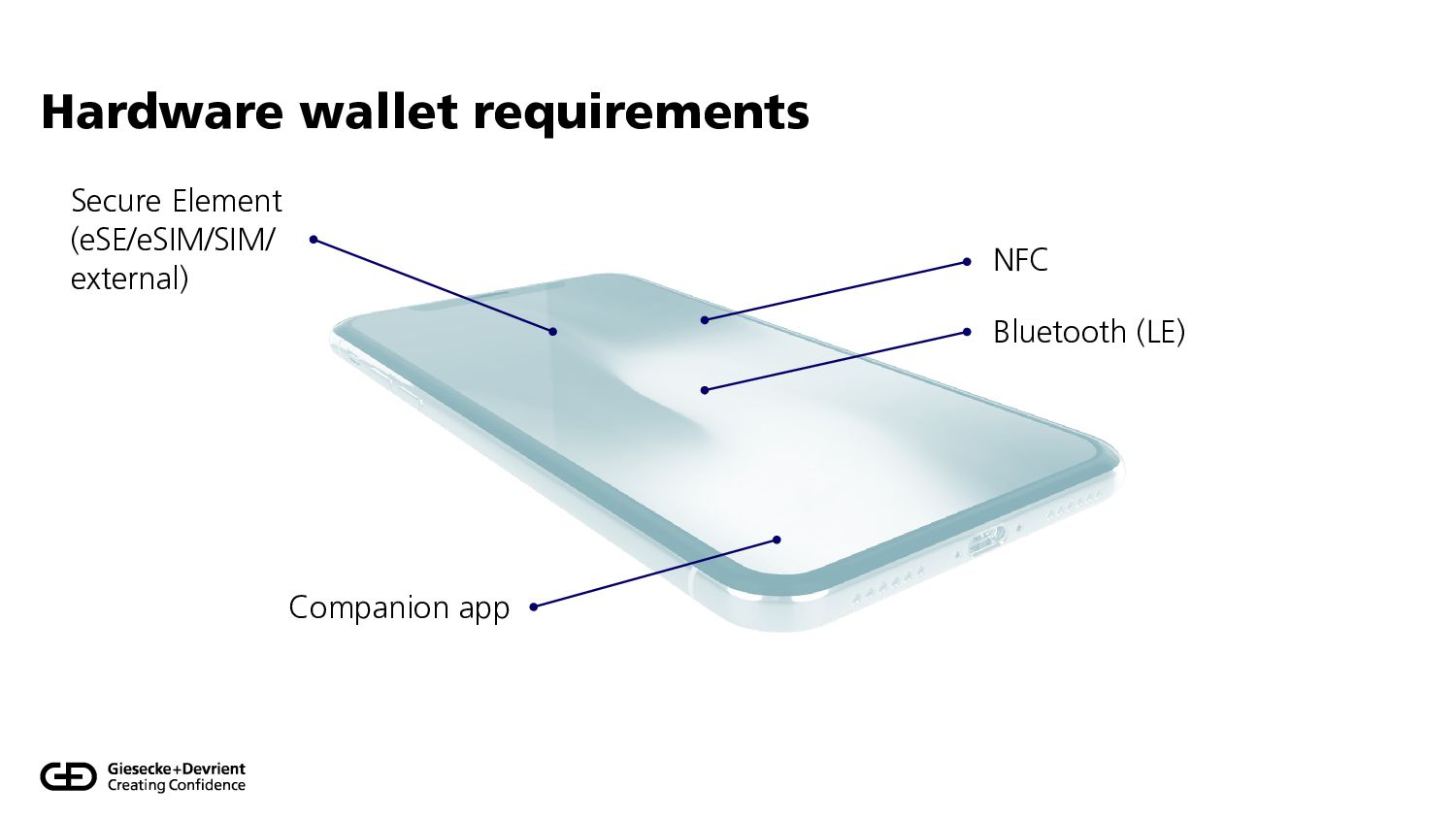

When we think of “electronic payments”, there are a lot of different interpretations: bank cards, credit cards, mobile money, QR codes, and more. Lately, many central banks – including the European Central Bank – have started investigating or piloting digital currencies (CBDC) to introduce yet another way to pay electronically. The wish list for CBDC is long: it should support online & offline payments, work as usual at the point of sale, be accessible to users without bank accounts, … At the centre of these design discussions are wallets, powered by secure hardware.

In this talk, I give an overview over the current CBDC ecosystem, explain some novel techniques that could help to implement wallets at scale, and give a perspective regarding standardisation.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

![Questions? Answers! Lars Hupel https://lars.hupel.info [email protected]](https://files.speakerdeck.com/presentations/ce96cabe0b094332a2674d0052bc48e3/slide_35.jpg){kind=link}