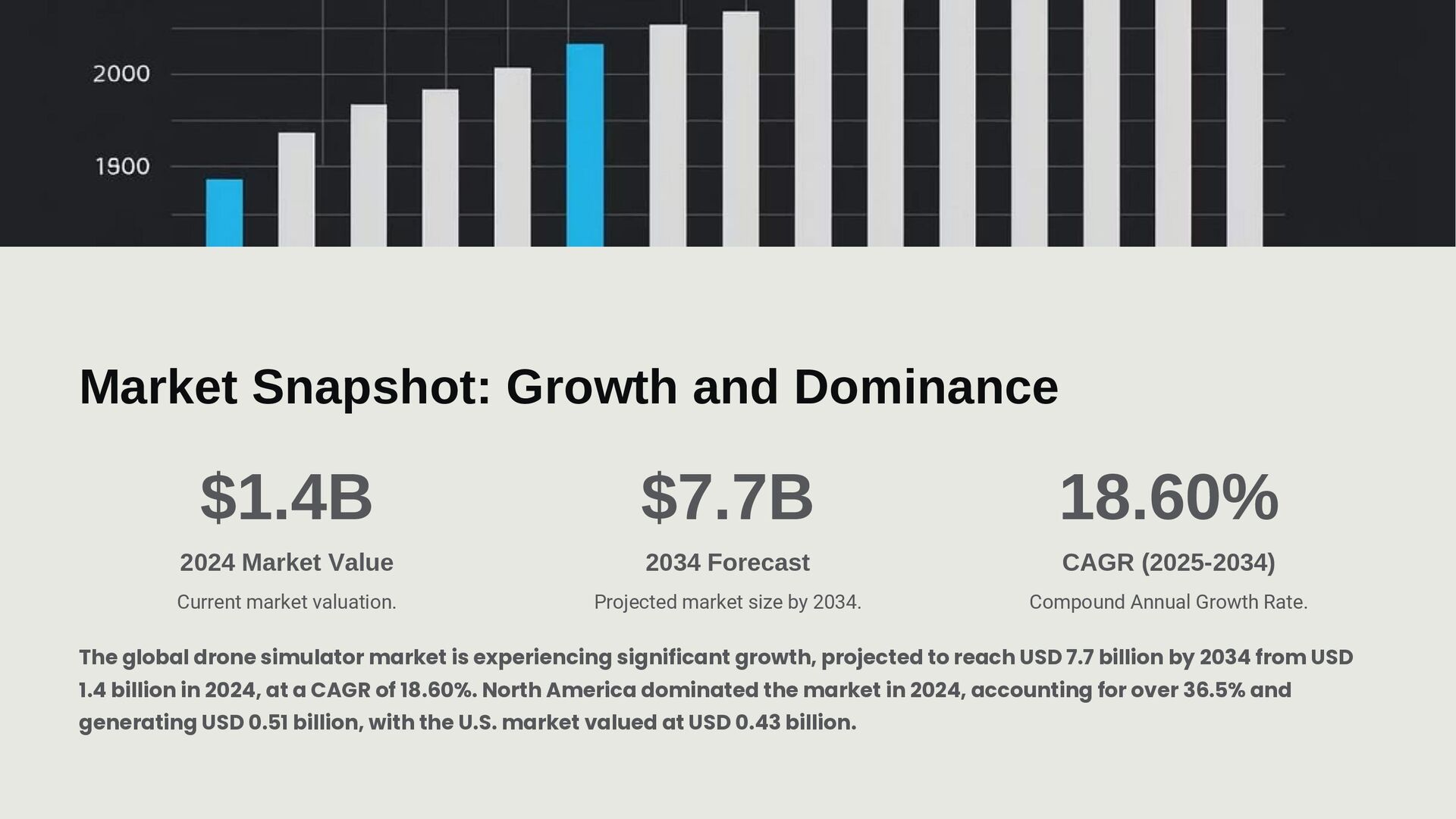

The Global Drone Simulator Market is expected to expand significantly, reaching USD 7.7 Billion by 2034, up from USD 1.4 Billion in 2024, with a robust CAGR of 18.60% during the forecast period from 2025 to 2034. This growth is driven by increasing demand for drone training solutions across both military and commercial applications, supported by rapid advancements in simulation technologies.

Read More - https://market.us/report/global-drone-simulator-market/

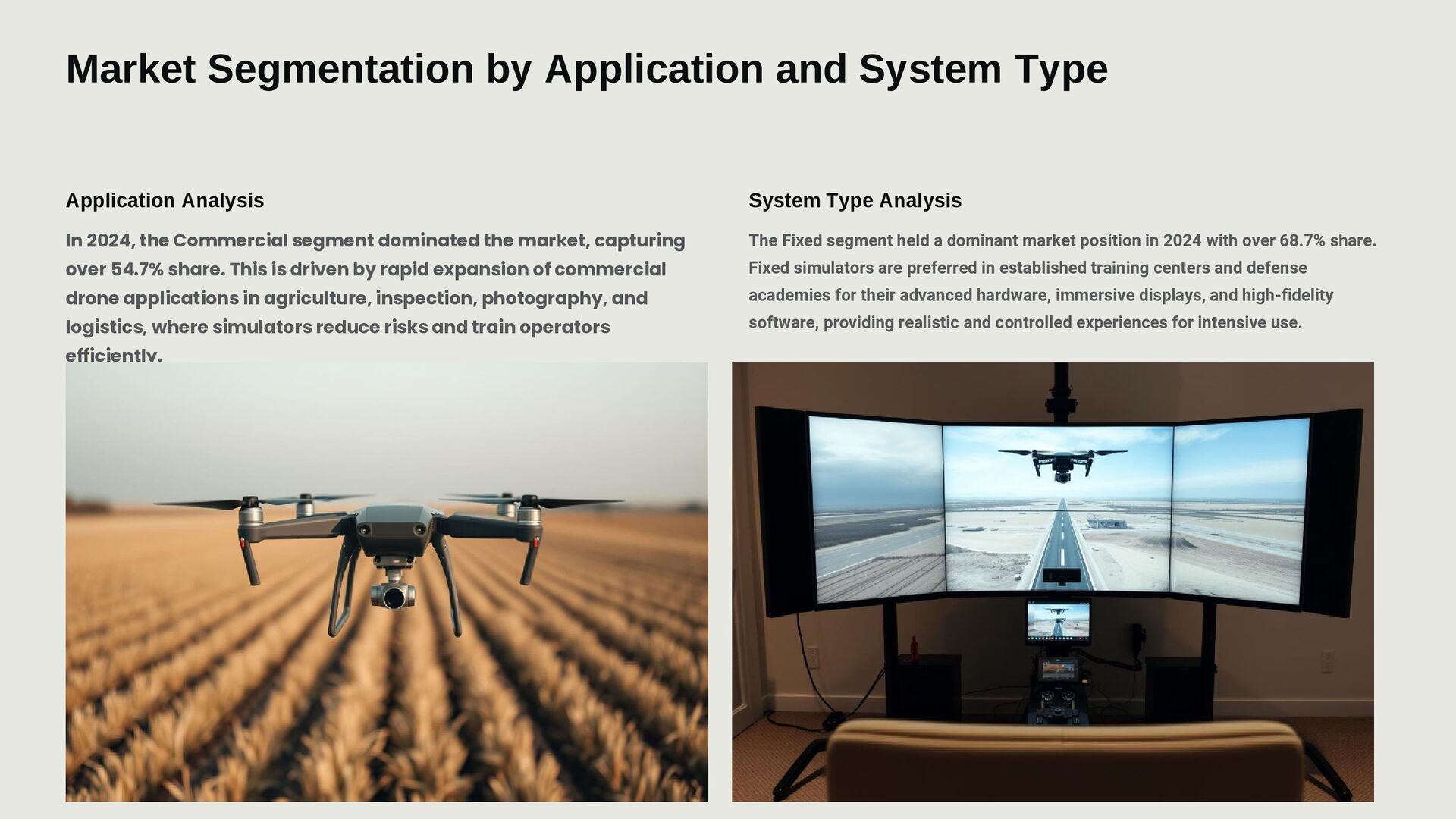

In 2024, the Commercial segment held the dominant position, accounting for more than 54.7% of the global market share. This leadership can be attributed to rising demand for drone pilots in industries such as logistics, agriculture, surveillance, and inspection services, where simulation offers a cost-effective and risk-free training environment.

By system type, the Fixed segment captured more than 68.7% market share in 2024. This reflects the growing preference for stationary simulator platforms that provide high-fidelity training environments and longer operational durability for both institutional and defense training facilities.

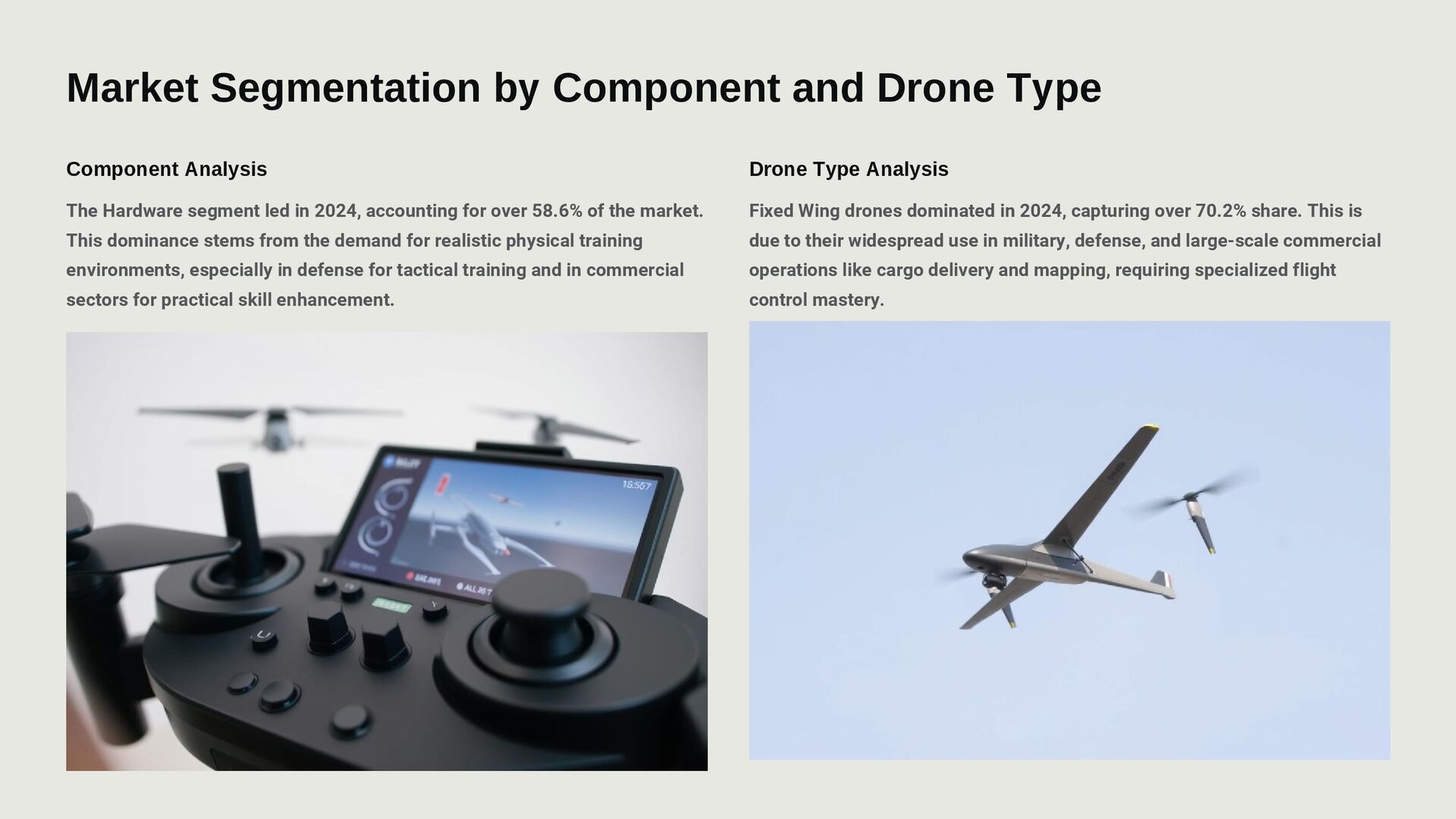

The Hardware segment emerged as the leading component category, contributing to more than 58.6% of the global revenue. Hardware-driven demand was mainly fueled by the increasing need for immersive control stations, haptic devices, and physical simulation components that replicate real-world drone operation.

In terms of drone type, the Fixed Wing segment dominated with more than 70.2% market share in 2024. Fixed-wing drones are widely used in long-distance, high-endurance applications, and simulation tools for these systems have seen heightened demand in defense and large-scale commercial operations.

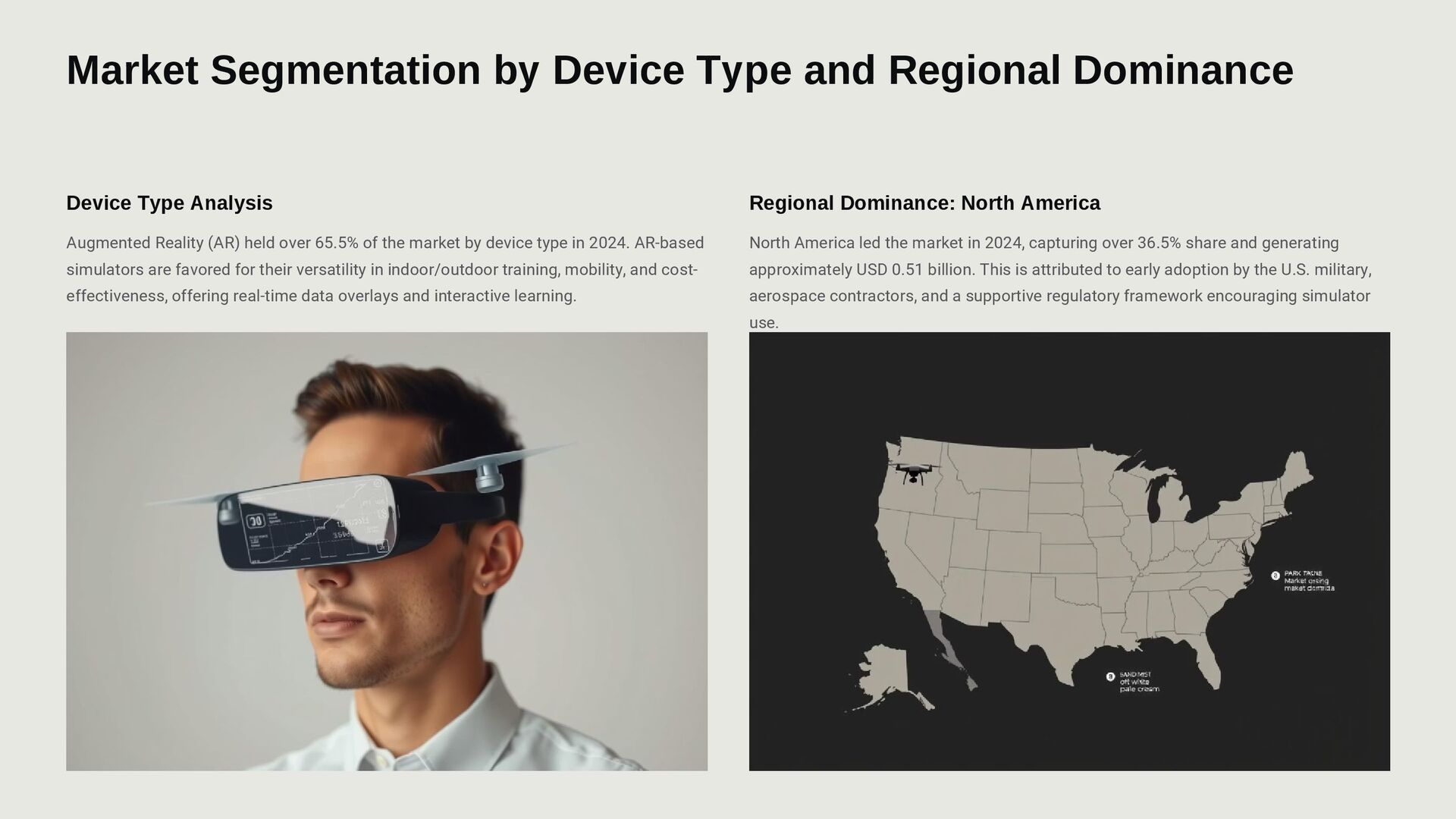

By device type, Augmented Reality (AR) simulators held the largest share at over 65.5% in 2024. AR-enabled platforms are being increasingly adopted for their ability to blend real-world scenarios with simulated training, improving realism and pilot responsiveness.

Regionally, North America led the global market, accounting for more than 36.5% share in 2024, generating approximately USD 0.51 billion in revenue. This dominance is supported by advanced defense infrastructure, rising commercial drone usage, and a strong focus on pilot training technologies.

Within the region, the U.S. market stood at USD 0.43 billion in 2024, reflecting its strategic emphasis on drone mission planning, military readiness, and commercial UAV operator training. The U.S. market is forecasted to expand at a CAGR of 16.7%, underscoring its continued investment in simulation-based drone technologies.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}