Javier Revuelta, Senior Principal de AFRY, empresa de consultoría e ingeniería y Javier Colón, Presidente de ACENEL, Asociación de Comercializadores Independientes de Energía Eléctrica, te invitan a compartir su análisis sobre qué podemos esperar del mercado eléctrico en España en los siguientes años y qué proyecciones manejan, según la evolución de la cotización del gas natural, derechos de la emisión de CO2 y resto de drivers, así como qué podremos esperar de la política energética nacional y la comparación con el resto de países de nuestro entorno.

Porque el futuro no lo podemos conocer, pero sí que podemos imaginarnos distintas posibilidades.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

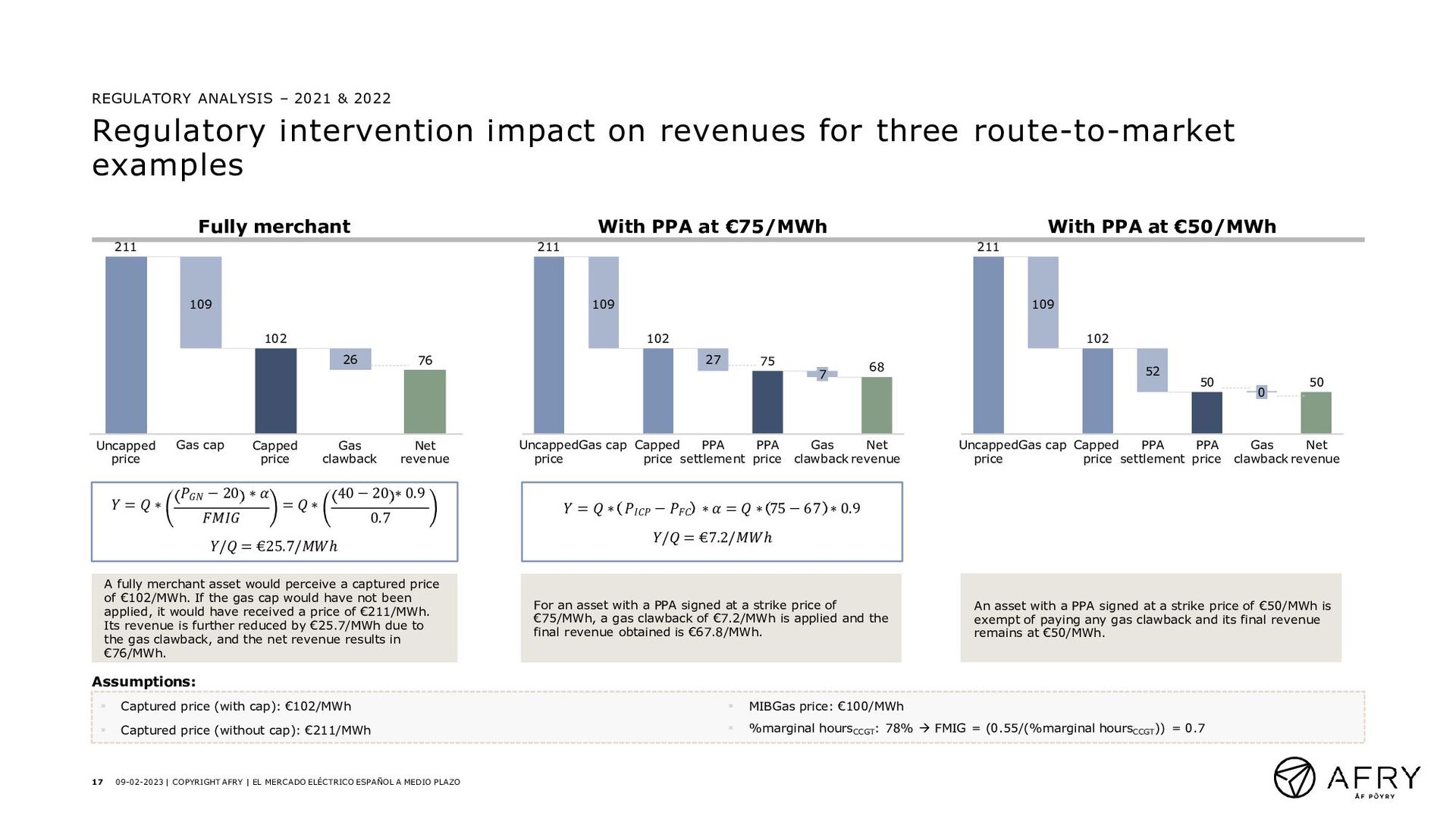

![𝑃𝐺𝑁 − 𝑃𝑅𝐺𝑁 𝑌 = 0.55 Being: − PGN [€/MWh]:](https://files.speakerdeck.com/presentations/8a0a499480324fd68c9d56aebbbe5a42/slide_14.jpg){kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}