car insurance online, with double digit percentage year on year hikes not uncommon. Transparency does not exist as current soluBons offer different panels of providers and different prices for the same providers. No easy way exists to search across all of these current soluBons to consistently achieve the best value for the consumer. Walled gardens restricBng the movement of data, lack of APIs and copyright implicaBons of screenscraping content.

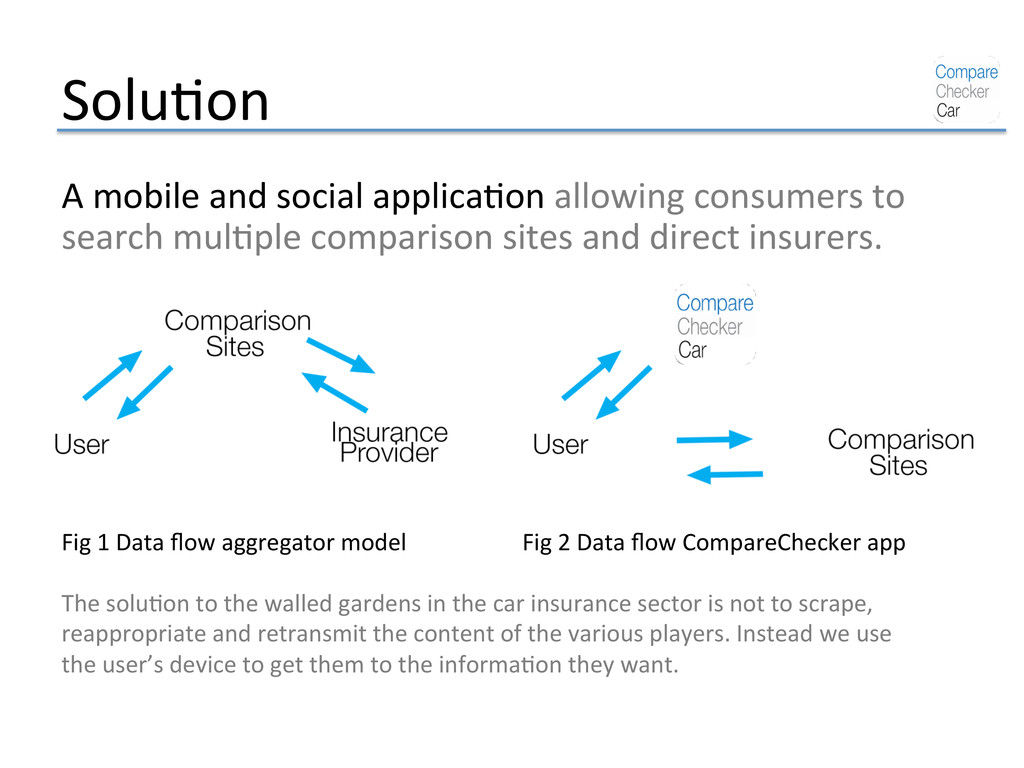

search mulBple comparison sites and direct insurers. Fig 1 Data flow aggregator model Fig 2 Data flow CompareChecker app The soluBon to the walled gardens in the car insurance sector is not to scrape, reappropriate and retransmit the content of the various players. Instead we use the user’s device to get them to the informaBon they want.

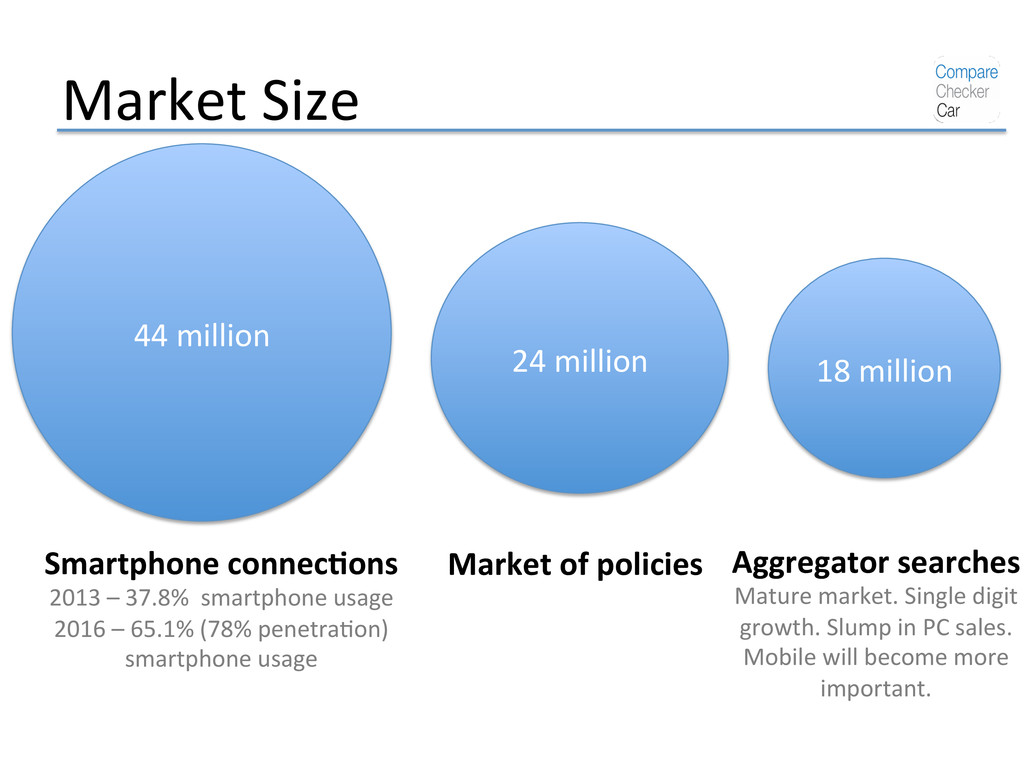

of policies Aggregator searches Mature market. Single digit growth. Slump in PC sales. Mobile will become more important. 44 million Smartphone connec=ons 2013 – 37.8% smartphone usage 2016 – 65.1% (78% penetraBon) smartphone usage

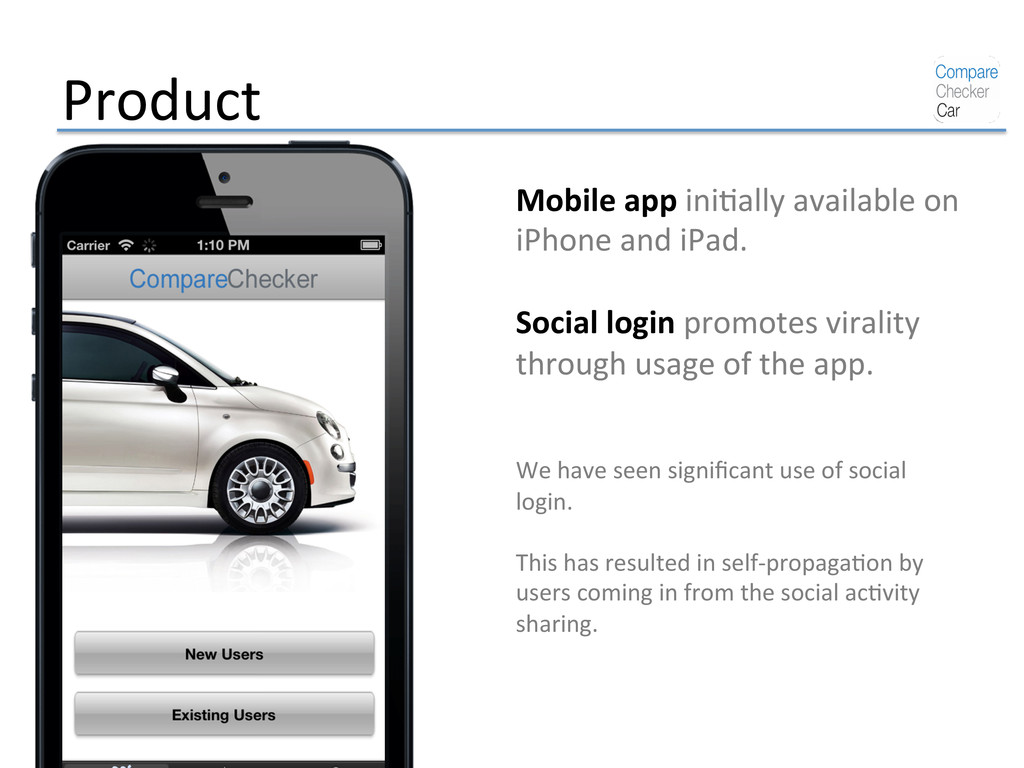

iPad. Social login promotes virality through usage of the app. We have seen significant use of social login. This has resulted in self-‐propagaBon by users coming in from the social acBvity sharing.

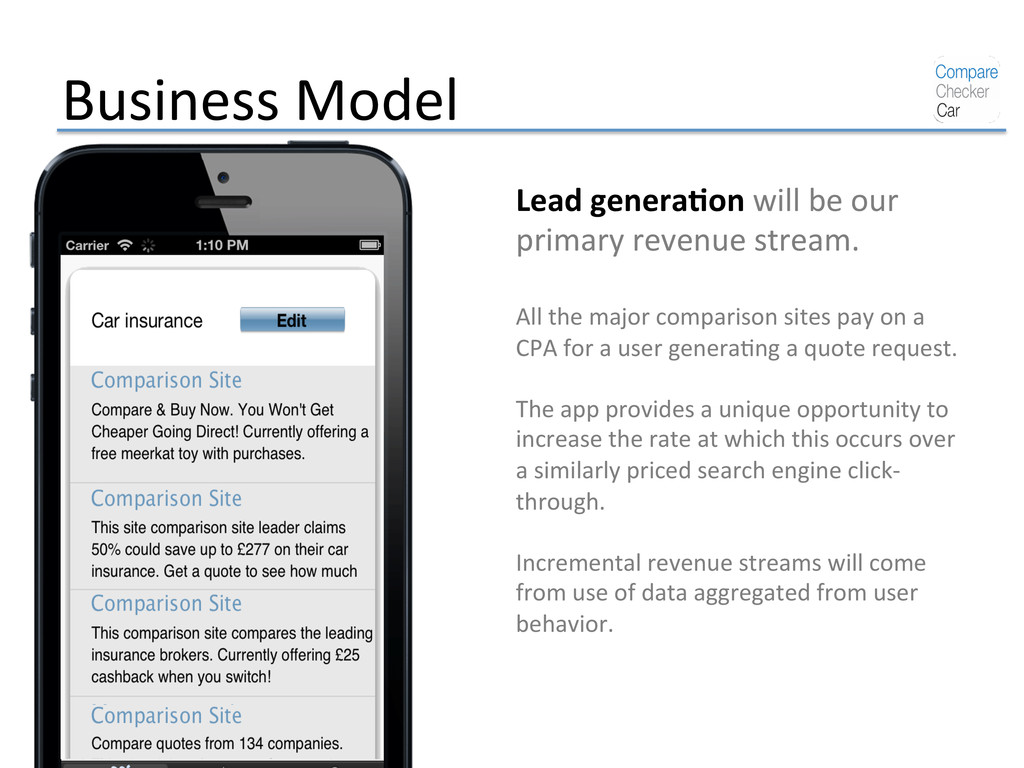

revenue stream. All the major comparison sites pay on a CPA for a user generaBng a quote request. The app provides a unique opportunity to increase the rate at which this occurs over a similarly priced search engine click-‐ through. Incremental revenue streams will come from use of data aggregated from user behavior.

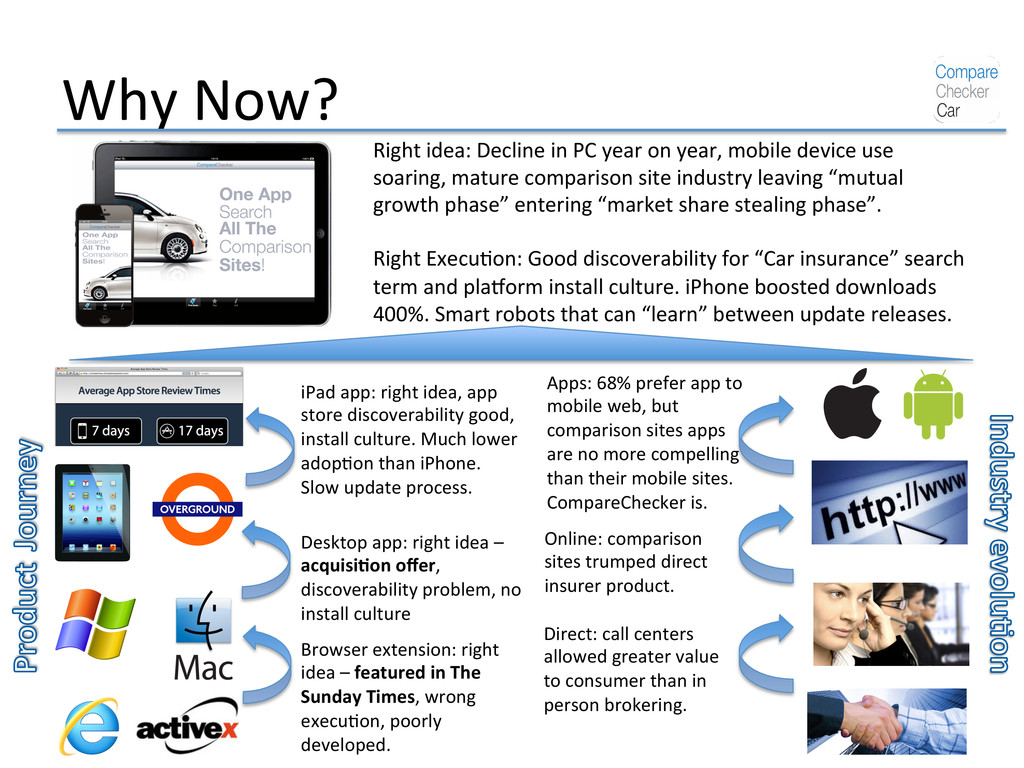

in The Sunday Times, wrong execuBon, poorly developed. Desktop app: right idea – acquisi=on offer, discoverability problem, no install culture iPad app: right idea, app store discoverability good, install culture. Much lower adopBon than iPhone. Slow update process. Apps: 68% prefer app to mobile web, but comparison sites apps are no more compelling than their mobile sites. CompareChecker is. Online: comparison sites trumped direct insurer product. Direct: call centers allowed greater value to consumer than in person brokering. Right idea: Decline in PC year on year, mobile device use soaring, mature comparison site industry leaving “mutual growth phase” entering “market share stealing phase”. Right ExecuBon: Good discoverability for “Car insurance” search term and plagorm install culture. iPhone boosted downloads 400%. Smart robots that can “learn” between update releases.

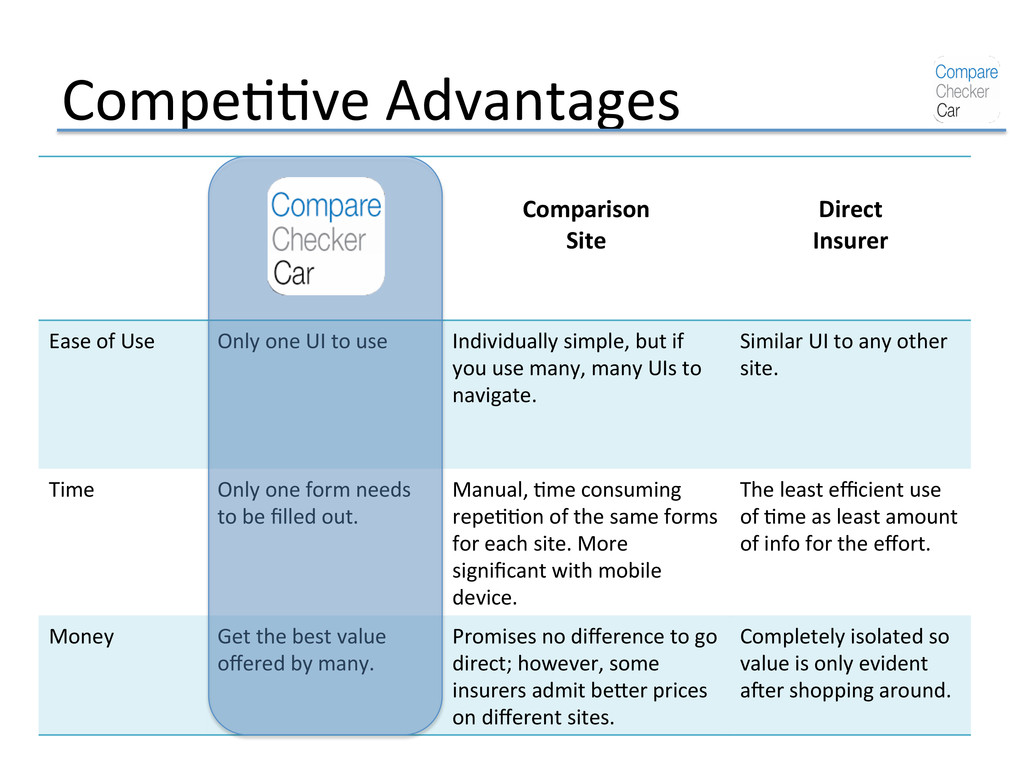

Site Direct Insurer Ease of Use Only one UI to use Individually simple, but if you use many, many UIs to navigate. Similar UI to any other site. Time Only one form needs to be filled out. Manual, Bme consuming repeBBon of the same forms for each site. More significant with mobile device. The least efficient use of Bme as least amount of info for the effort. Money Get the best value offered by many. Promises no difference to go direct; however, some insurers admit be\er prices on different sites. Completely isolated so value is only evident aker shopping around.

acquisiBon cost less than conservaBve projected average revenue per install. Social sharing – Social login users automaBcally share acBvity. This brings in more users. Increase word-‐of-‐mouth Publish arBcles regularly – journalists have been advising consumers on our use case for years. App Store SEO – Compelling product has resulted in strong posiBon for relevant search terms in the Apple App store in the beta.

BA Finance, AccounBng and Management – University of Nolngham Business School Strong technical skills and understanding of the technologies underpinning CompareChecker. Built version of CompareChecker currently available.

their ‘Facebook’. Insurance Companies e.g. big players without any ownership in the comparison sector Banks e.g.firms that have shown interest in the comparison sector but were too late to market first Bme around. Tech firms

![CompareChecker Ade Molajo [email protected] CompareChecker](https://files.speakerdeck.com/presentations/2a21e3e09c3c0130246f226fb1014015/slide_0.jpg){kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

![Contact Ade Molajo [email protected]](https://files.speakerdeck.com/presentations/2a21e3e09c3c0130246f226fb1014015/slide_14.jpg){kind=link}