work with Ram Rajagopal2 Kameshwar Poolla1 Pravin Varaiya1 1University of California, Berkeley 2Stanford University November 1, 2016 Wenyuan Tang Virtual Bidding 1 / 41

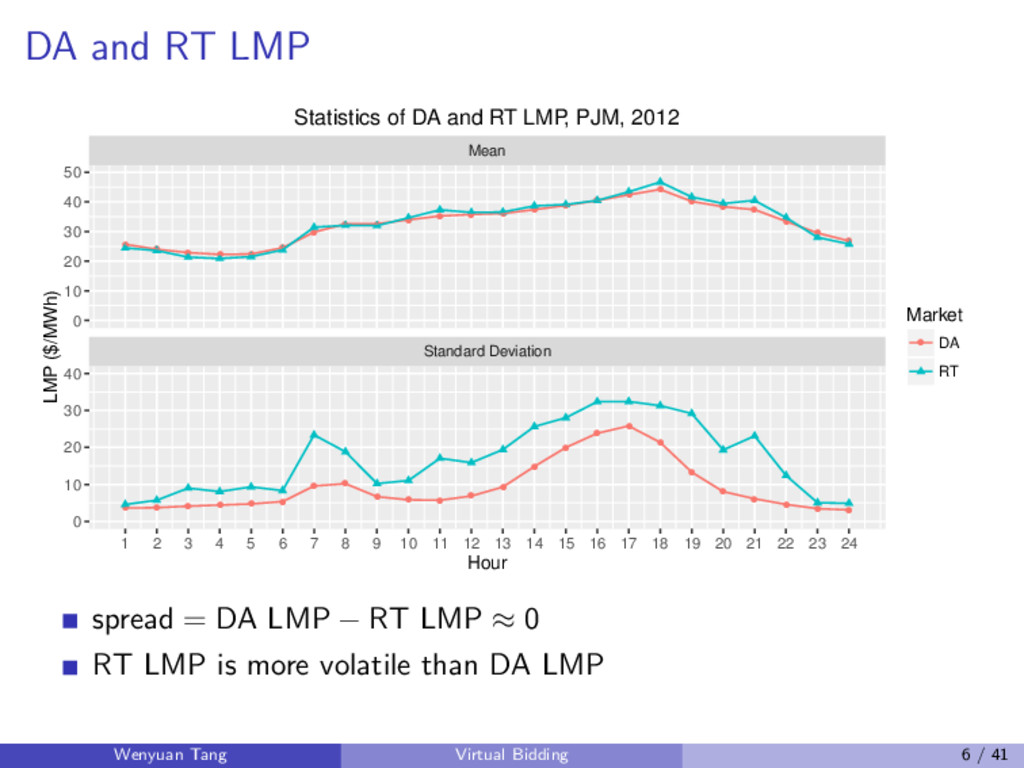

value (price) of power at different locations, and the LMP at a load-zone or a hub is the weighted average of the nodal LMPs The day-ahead (DA) market lets market participants commit to buy or sell power one day before the operating day, and establishes 24 hourly DA LMPs The real-time (RT) market balances the differences between DA commitments and the actual demand and supply during the course of the operating day, and establishes the 5-minute RT LMPs Systematic nonzero spreads are routinely observed, which indicates some market inefficiency hourly spread = hourly DA LMP − hourly average RT LMP Wenyuan Tang Virtual Bidding 2 / 41

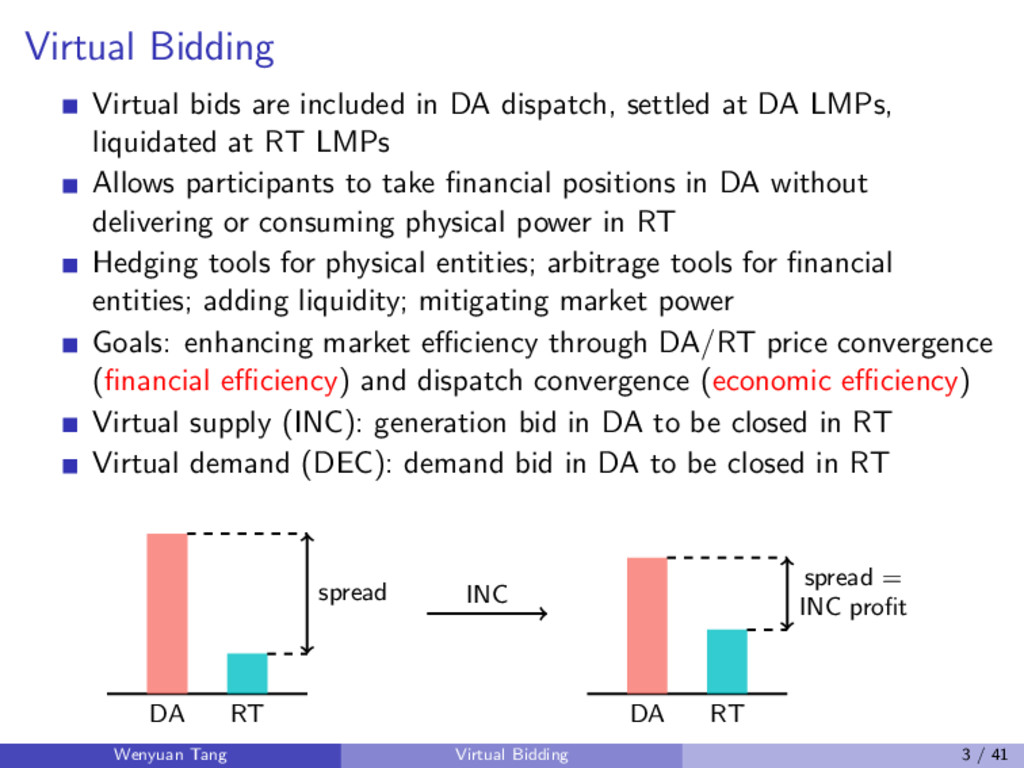

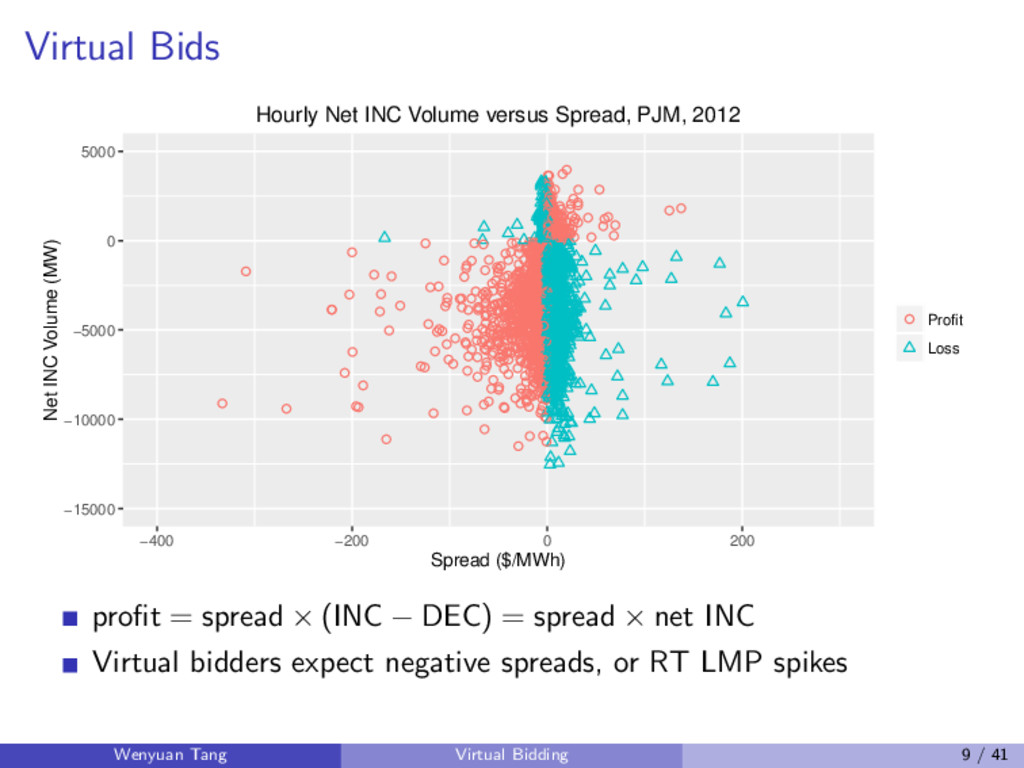

at DA LMPs, liquidated at RT LMPs Allows participants to take financial positions in DA without delivering or consuming physical power in RT Hedging tools for physical entities; arbitrage tools for financial entities; adding liquidity; mitigating market power Goals: enhancing market efficiency through DA/RT price convergence (financial efficiency) and dispatch convergence (economic efficiency) Virtual supply (INC): generation bid in DA to be closed in RT Virtual demand (DEC): demand bid in DA to be closed in RT DA RT spread INC DA RT spread = INC profit Wenyuan Tang Virtual Bidding 3 / 41

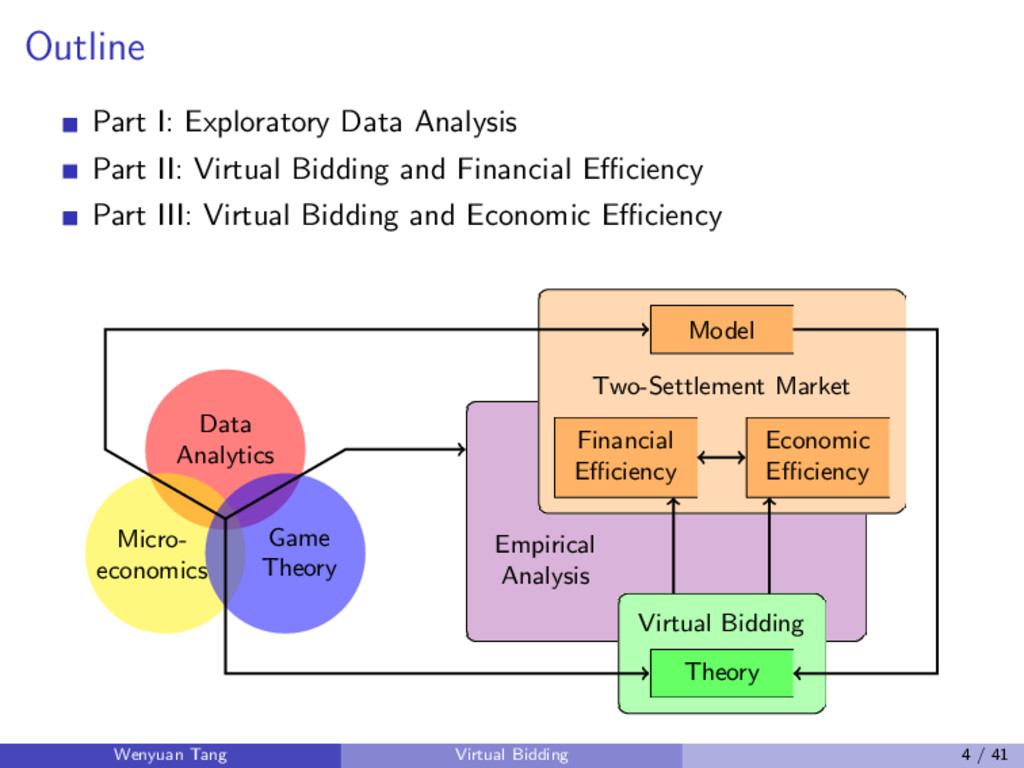

and Financial Efficiency Part III: Virtual Bidding and Economic Efficiency Data Analytics Micro- economics Game Theory Empirical Analysis Virtual Bidding Theory Two-Settlement Market Model Financial Efficiency Economic Efficiency Wenyuan Tang Virtual Bidding 4 / 41

($/MWh) Hour 4 18 Hourly Spread Time Series, PJM, 2014 The polar vortex triggered two extreme weather events in Jan 2014 Recent data do not support classical models, e.g., [Bessembinder & Lemmon 2002], which states that spread is negatively related to Var(RT LMP), and positively related to Skew(RT LMP) Wenyuan Tang Virtual Bidding 8 / 41

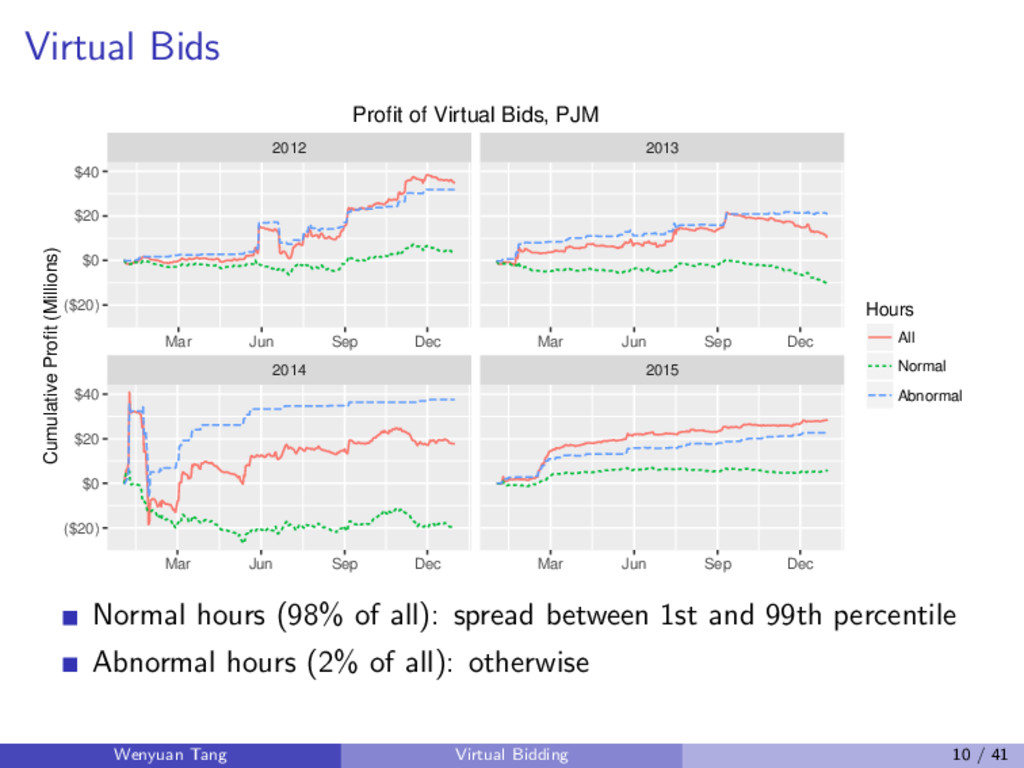

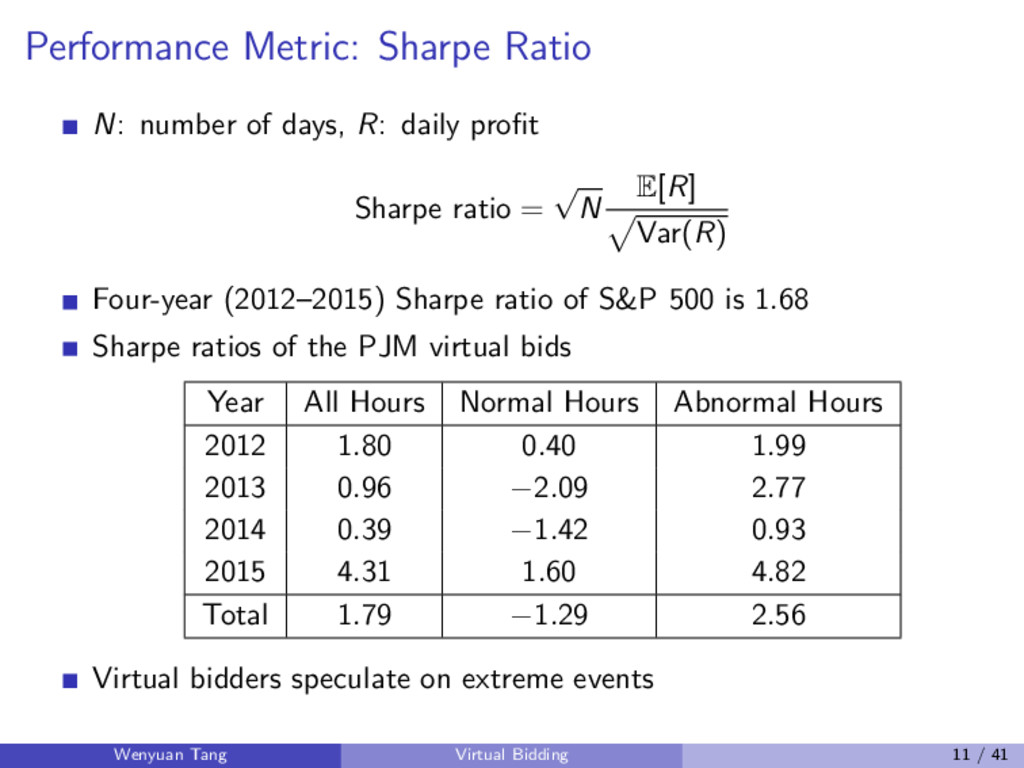

($20) $0 $20 $40 Mar Jun Sep Dec Mar Jun Sep Dec Mar Jun Sep Dec Mar Jun Sep Dec Cumulative Profit (Millions) Hours All Normal Abnormal Profit of Virtual Bids, PJM Normal hours (98% of all): spread between 1st and 99th percentile Abnormal hours (2% of all): otherwise Wenyuan Tang Virtual Bidding 10 / 41

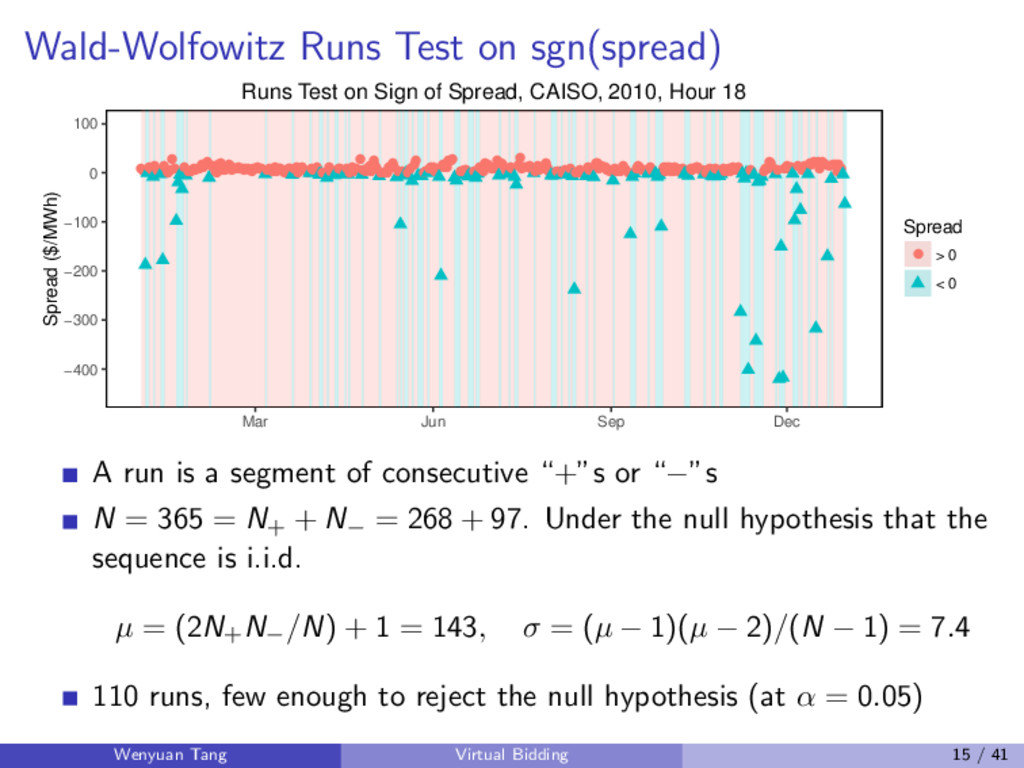

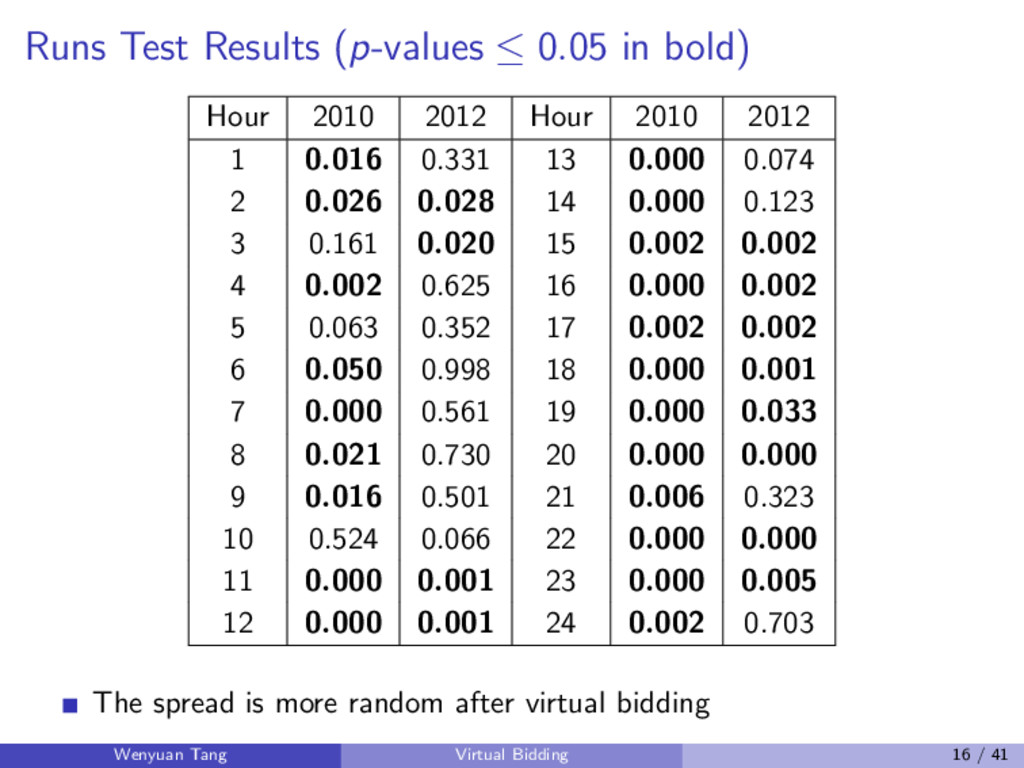

whether profitable bidding strategies exist before and after the implementation of virtual bidding [Li, Svoboda & Oren 2015], [Jha & Wolak 2015] We propose a measure that tests the randomness of the sequence of the spread: more random spread leaves less room for arbitrage opportunities We examine the autocorrelation of the sequence of the spread and propose a benchmark bidding strategy that is only based on the up-to-date price information We employ machine learning methods to design more sophisticated bidding strategies that utilize other data such as load Note that our definition of financial efficiency does not depend on transaction costs, which are therefore not considered Wenyuan Tang Virtual Bidding 14 / 41

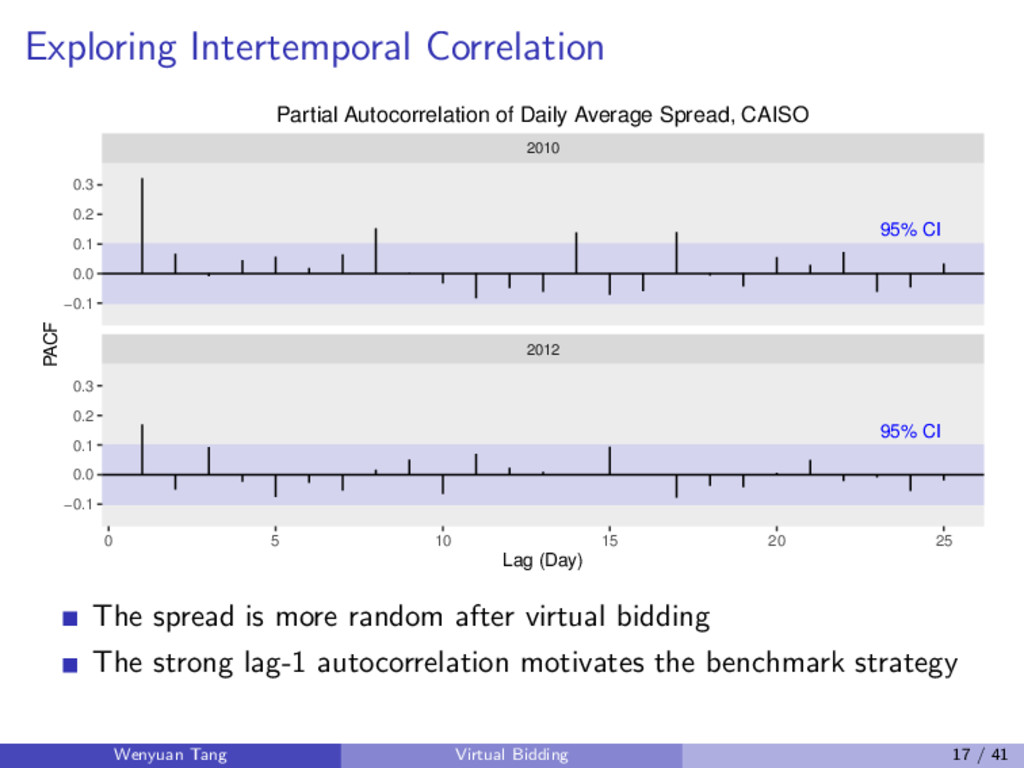

0.0 0.1 0.2 0.3 −0.1 0.0 0.1 0.2 0.3 0 5 10 15 20 25 Lag (Day) PACF Partial Autocorrelation of Daily Average Spread, CAISO The spread is more random after virtual bidding The strong lag-1 autocorrelation motivates the benchmark strategy Wenyuan Tang Virtual Bidding 17 / 41

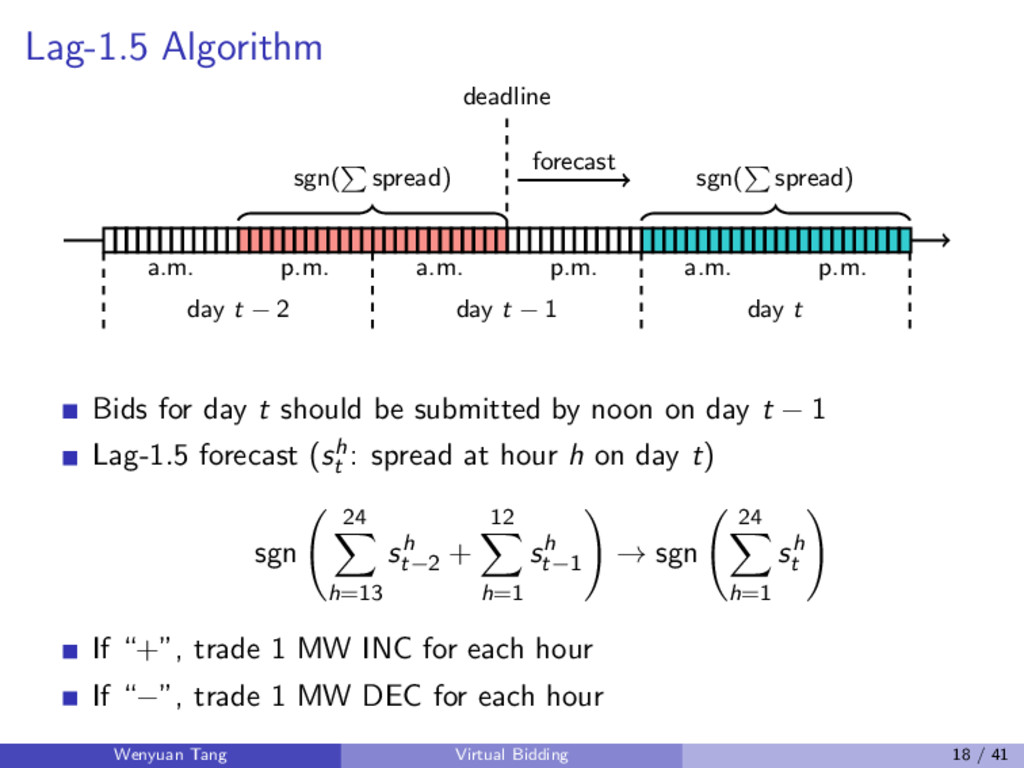

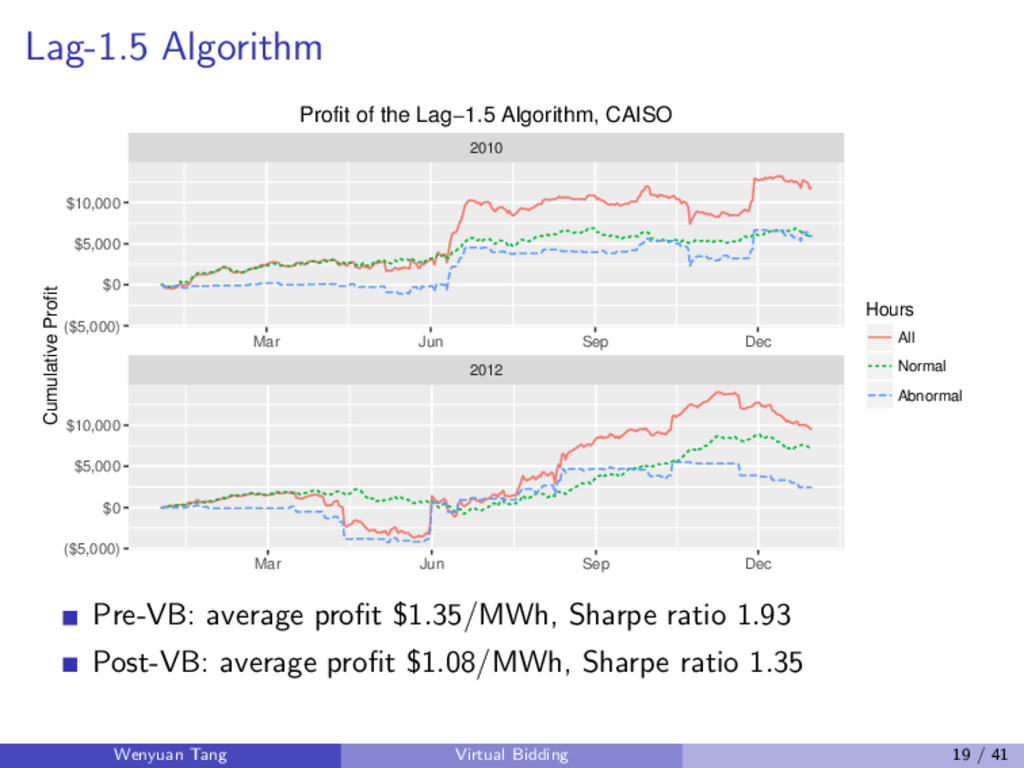

a.m. p.m. a.m. p.m. day t − 2 day t − 1 day t Bids for day t should be submitted by noon on day t − 1 Lag-1.5 forecast (sh t : spread at hour h on day t) sgn 24 h=13 sh t−2 + 12 h=1 sh t−1 → sgn 24 h=1 sh t If “+”, trade 1 MW INC for each hour If “−”, trade 1 MW DEC for each hour Wenyuan Tang Virtual Bidding 18 / 41

$5,000 $10,000 Mar Jun Sep Dec Mar Jun Sep Dec Cumulative Profit Hours All Normal Abnormal Profit of the Lag−1.5 Algorithm, CAISO Pre-VB: average profit $1.35/MWh, Sharpe ratio 1.93 Post-VB: average profit $1.08/MWh, Sharpe ratio 1.35 Wenyuan Tang Virtual Bidding 19 / 41

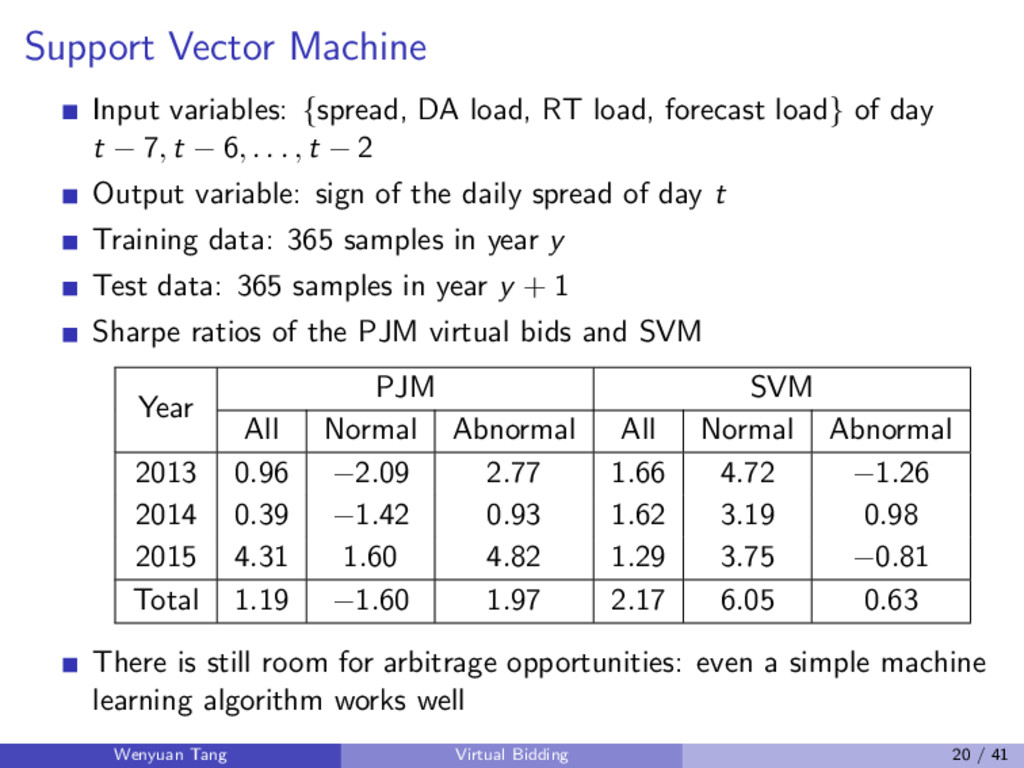

forecast load} of day t − 7, t − 6, . . . , t − 2 Output variable: sign of the daily spread of day t Training data: 365 samples in year y Test data: 365 samples in year y + 1 Sharpe ratios of the PJM virtual bids and SVM Year PJM SVM All Normal Abnormal All Normal Abnormal 2013 0.96 −2.09 2.77 1.66 4.72 −1.26 2014 0.39 −1.42 0.93 1.62 3.19 0.98 2015 4.31 1.60 4.82 1.29 3.75 −0.81 Total 1.19 −1.60 1.97 2.17 6.05 0.63 There is still room for arbitrage opportunities: even a simple machine learning algorithm works well Wenyuan Tang Virtual Bidding 20 / 41

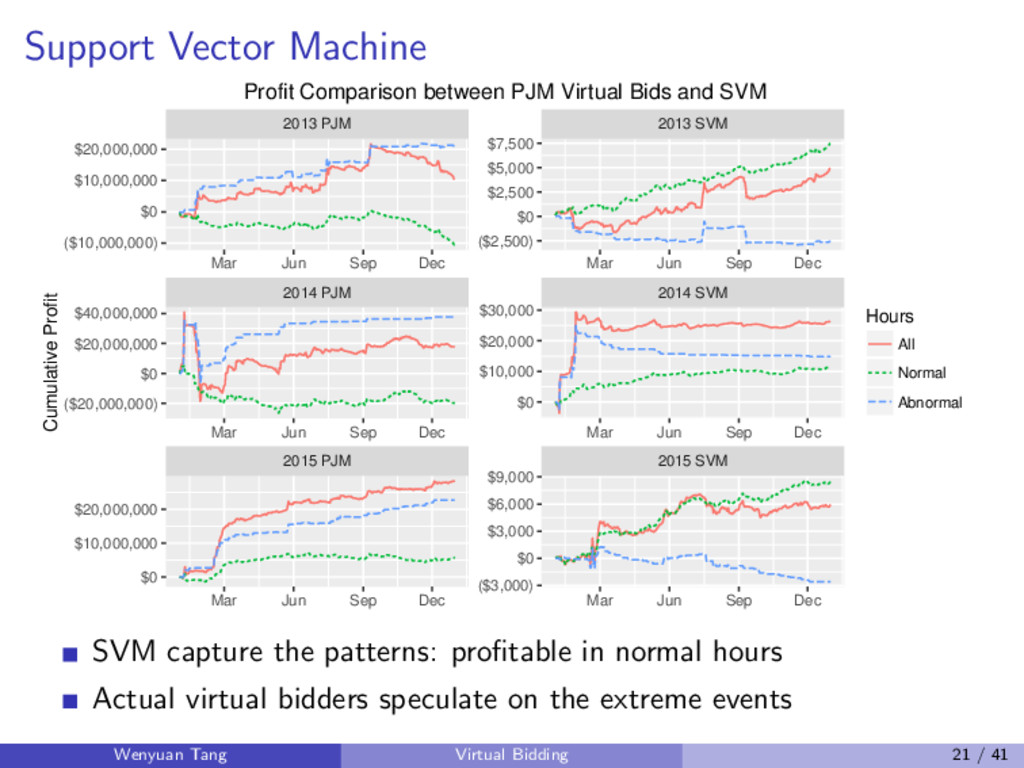

SVM 2014 SVM 2015 SVM ($10,000,000) $0 $10,000,000 $20,000,000 ($20,000,000) $0 $20,000,000 $40,000,000 $0 $10,000,000 $20,000,000 ($2,500) $0 $2,500 $5,000 $7,500 $0 $10,000 $20,000 $30,000 ($3,000) $0 $3,000 $6,000 $9,000 Mar Jun Sep Dec Mar Jun Sep Dec Mar Jun Sep Dec Mar Jun Sep Dec Mar Jun Sep Dec Mar Jun Sep Dec Cumulative Profit Hours All Normal Abnormal Profit Comparison between PJM Virtual Bids and SVM SVM capture the patterns: profitable in normal hours Actual virtual bidders speculate on the extreme events Wenyuan Tang Virtual Bidding 21 / 41

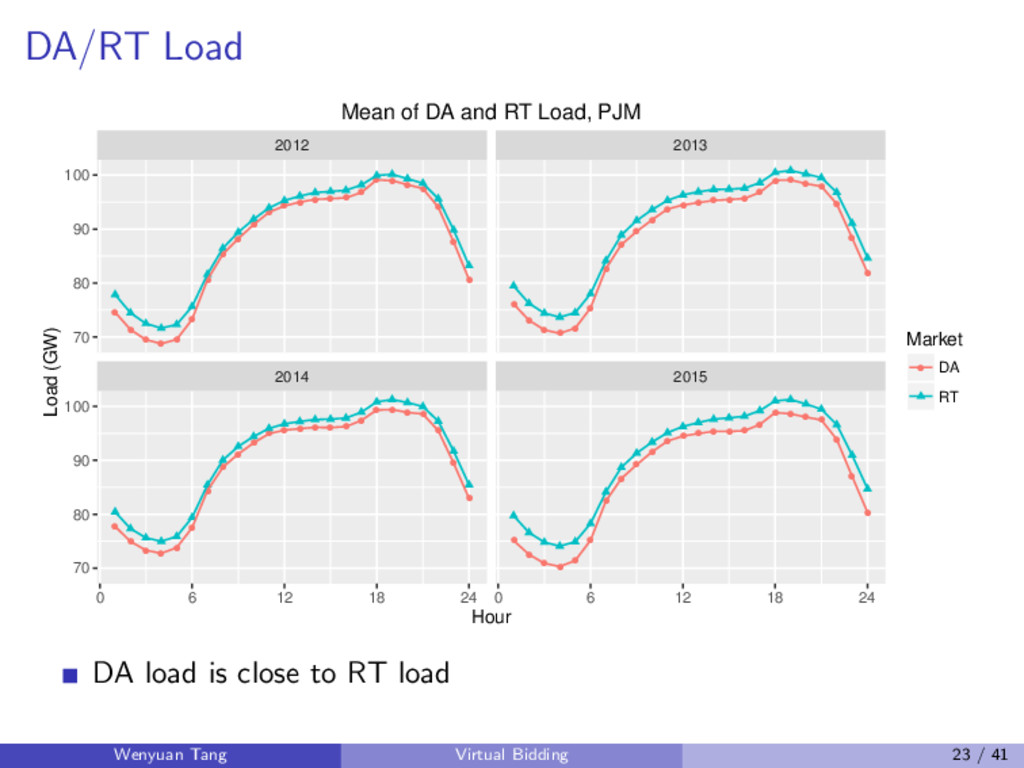

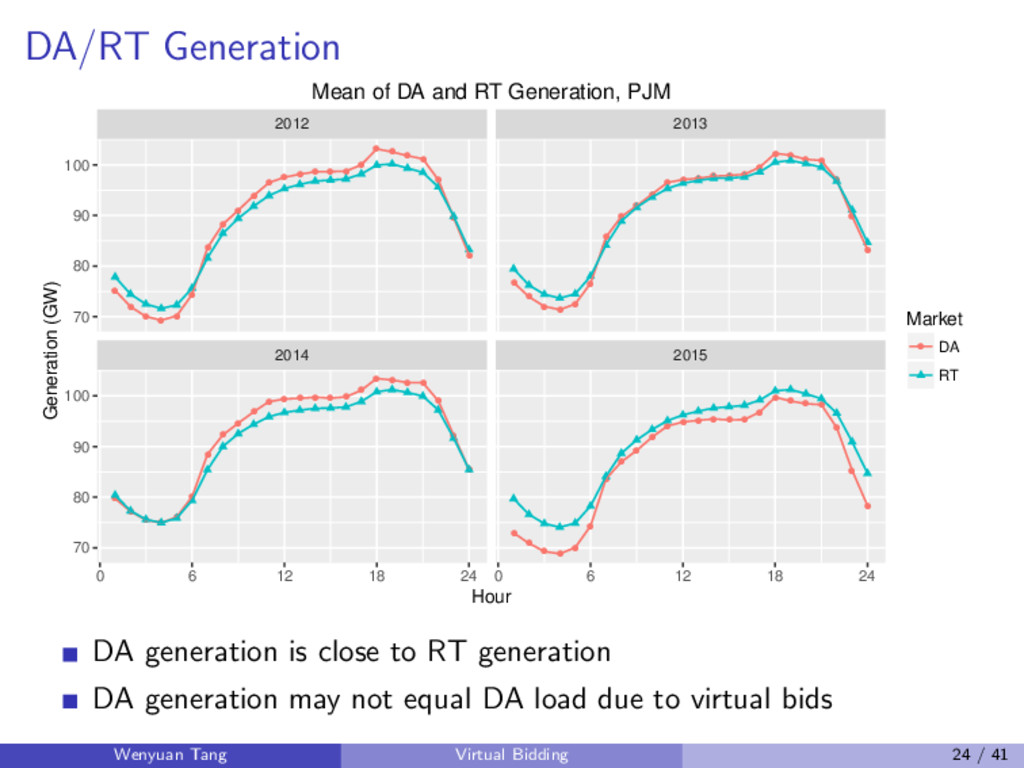

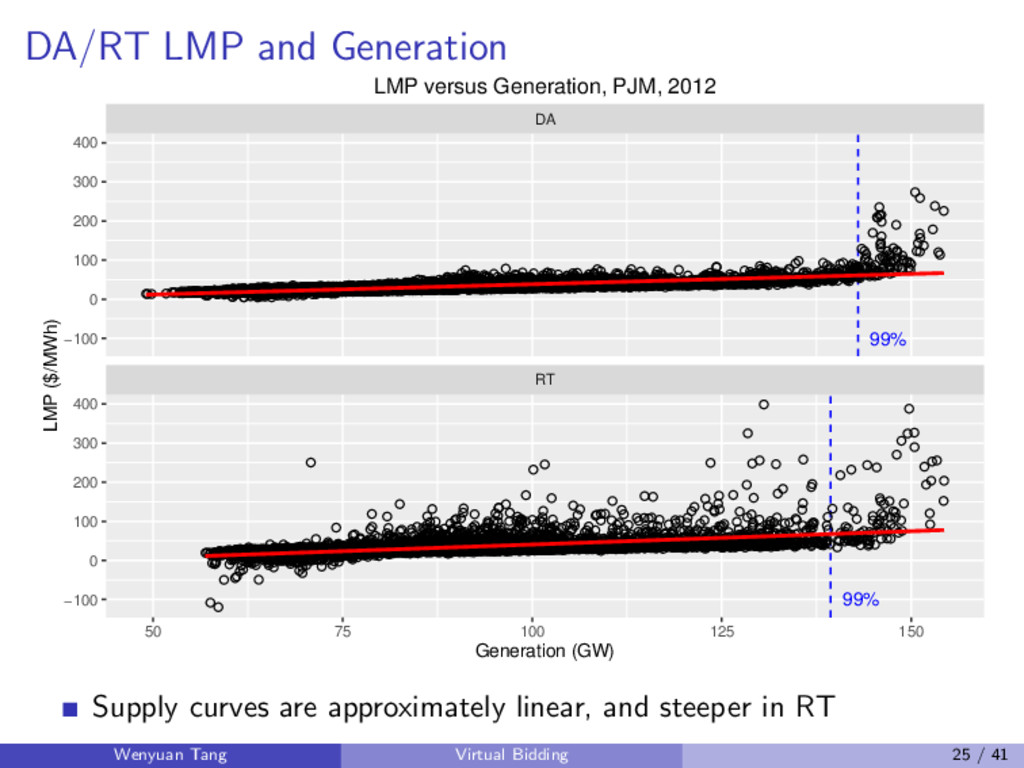

efficiency as generation cost minimization Why is load forecast important? Why is DA load close to RT load? Why is RT supply curve steeper than DA? How is economic efficiency related to price convergence? How is economic efficiency related to dispatch convergence? How to explain the phenomena: negative RT LMP; DA load close to RT load, but DA LMP far apart from RT LMP; etc. How does virtual bidding affect DA/RT dispatch? How to estimate the generation cost with and without virtual bids? Wenyuan Tang Virtual Bidding 22 / 41

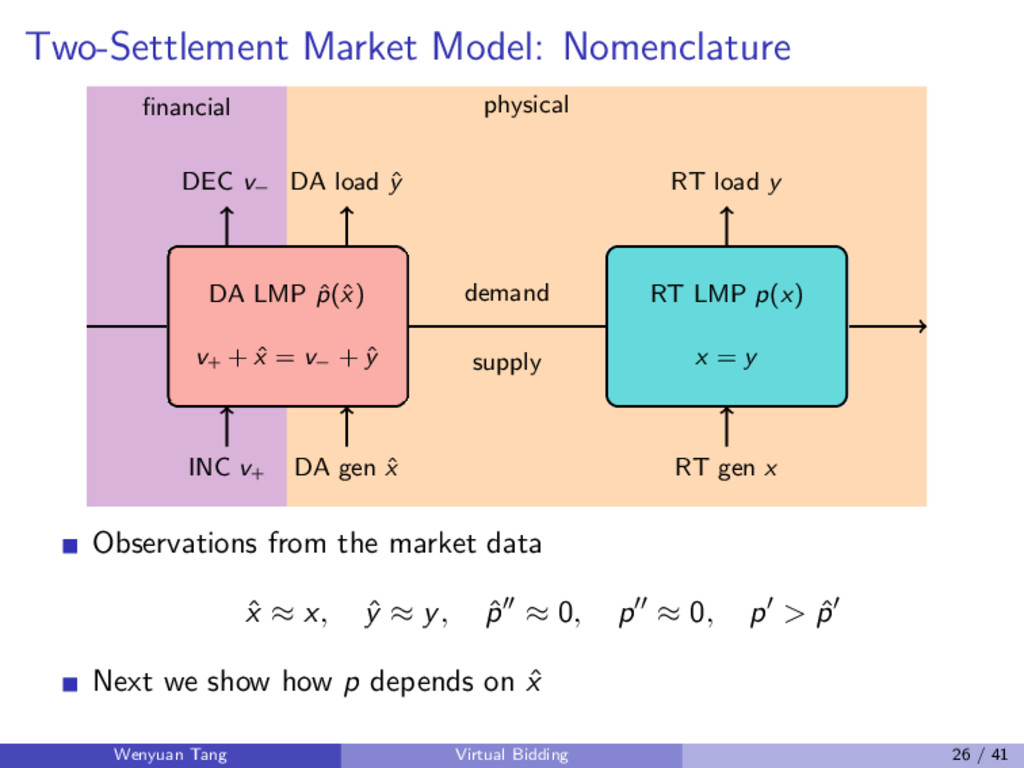

ˆ p(ˆ x) v+ + ˆ x = v− + ˆ y INC v+ DA gen ˆ x DEC v− DA load ˆ y RT LMP p(x) x = y RT gen x RT load y Observations from the market data ˆ x ≈ x, ˆ y ≈ y, ˆ p ≈ 0, p ≈ 0, p > ˆ p Next we show how p depends on ˆ x Wenyuan Tang Virtual Bidding 26 / 41

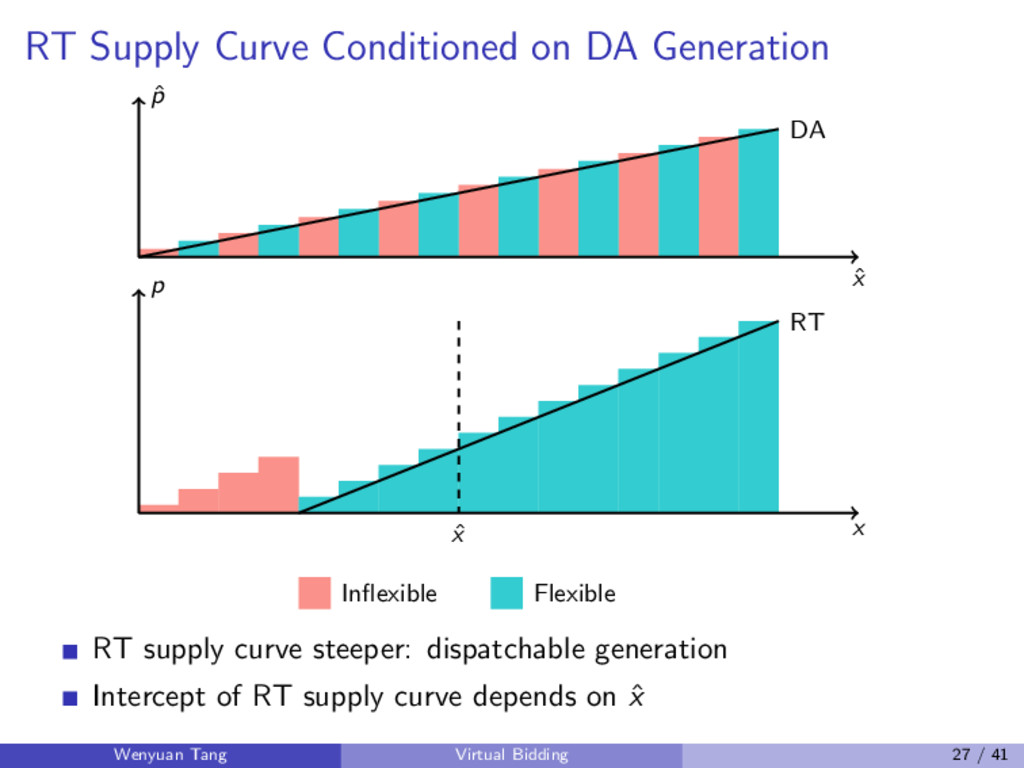

p DA x p RT ˆ x Inflexible Flexible RT supply curve steeper: dispatchable generation Intercept of RT supply curve depends on ˆ x Wenyuan Tang Virtual Bidding 27 / 41

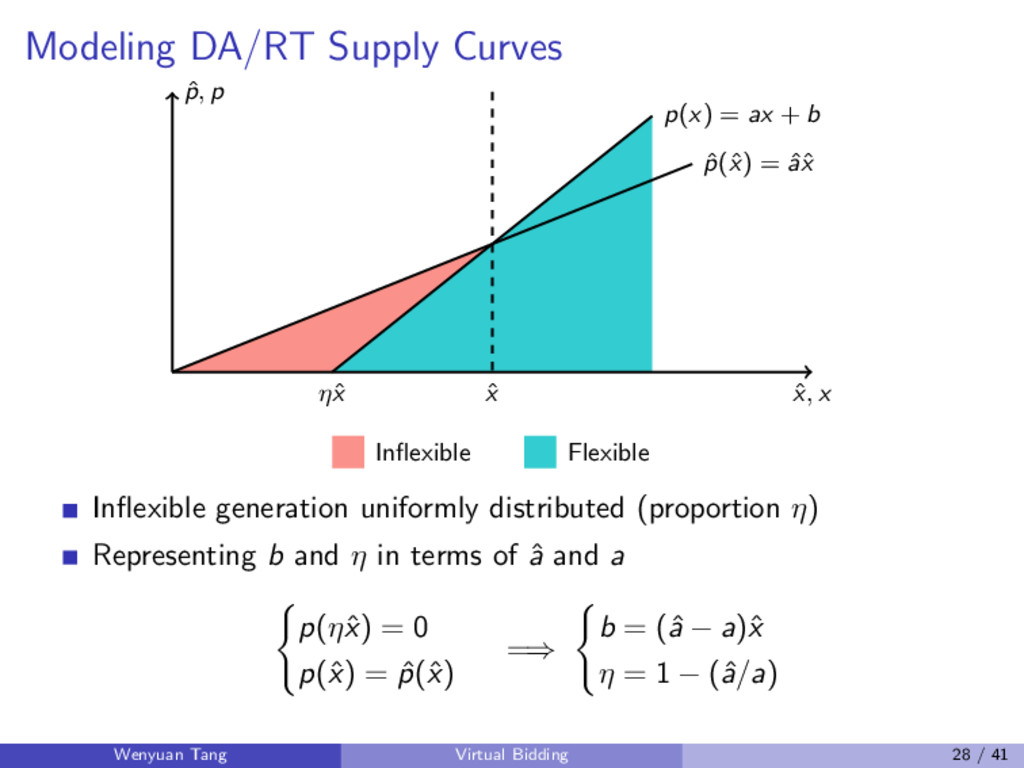

ˆ p(ˆ x) = ˆ aˆ x ηˆ x p(x) = ax + b ˆ x Inflexible Flexible Inflexible generation uniformly distributed (proportion η) Representing b and η in terms of ˆ a and a p(ηˆ x) = 0 p(ˆ x) = ˆ p(ˆ x) =⇒ b = (ˆ a − a)ˆ x η = 1 − (ˆ a/a) Wenyuan Tang Virtual Bidding 28 / 41

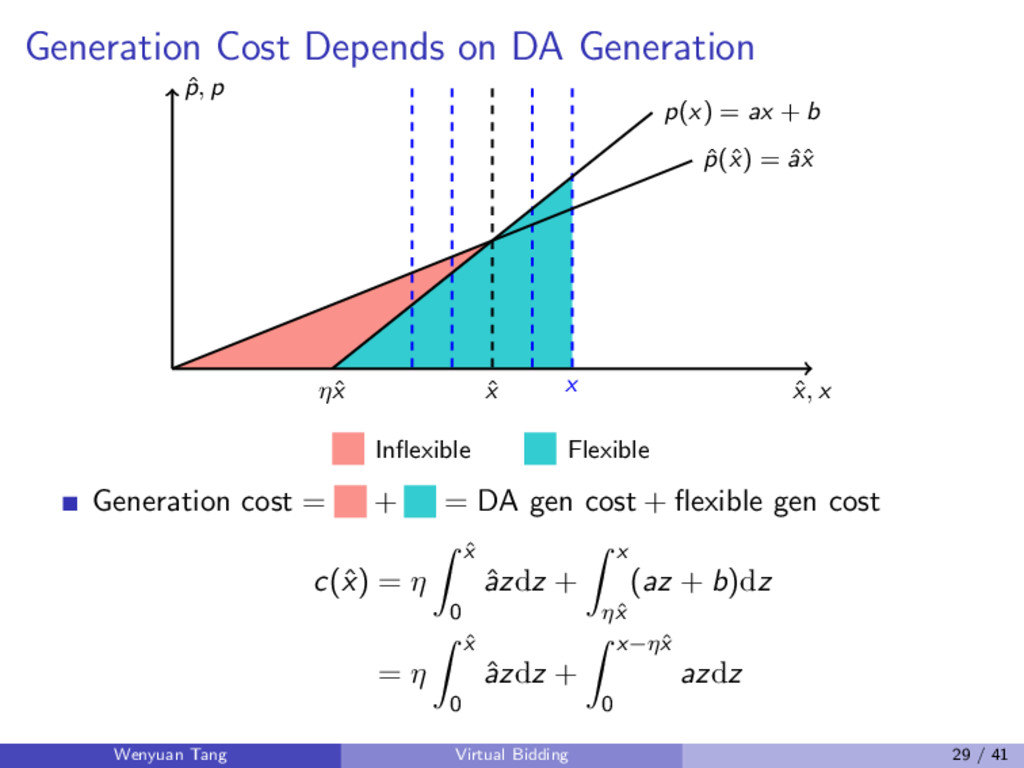

ˆ p, p ˆ p(ˆ x) = ˆ aˆ x ηˆ x p(x) = ax + b ˆ x Inflexible Flexible Generation cost = + = DA gen cost + flexible gen cost c(ˆ x) = η ˆ x 0 ˆ azdz + x ηˆ x (az + b)dz = η ˆ x 0 ˆ azdz + x−ηˆ x 0 azdz Wenyuan Tang Virtual Bidding 29 / 41

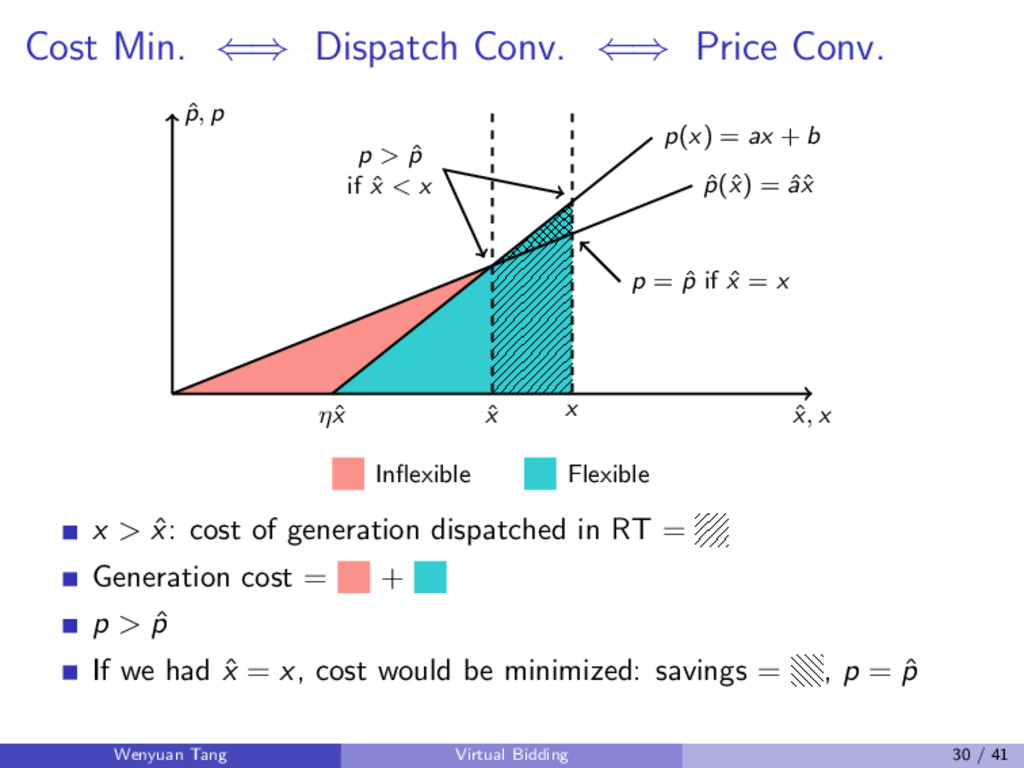

> ˆ p if ˆ x < x p = ˆ p if ˆ x = x ˆ x, x ˆ p, p ˆ p(ˆ x) = ˆ aˆ x ηˆ x p(x) = ax + b ˆ x Inflexible Flexible x > ˆ x: cost of generation dispatched in RT = Generation cost = + p > ˆ p If we had ˆ x = x, cost would be minimized: savings = , p = ˆ p Wenyuan Tang Virtual Bidding 30 / 41

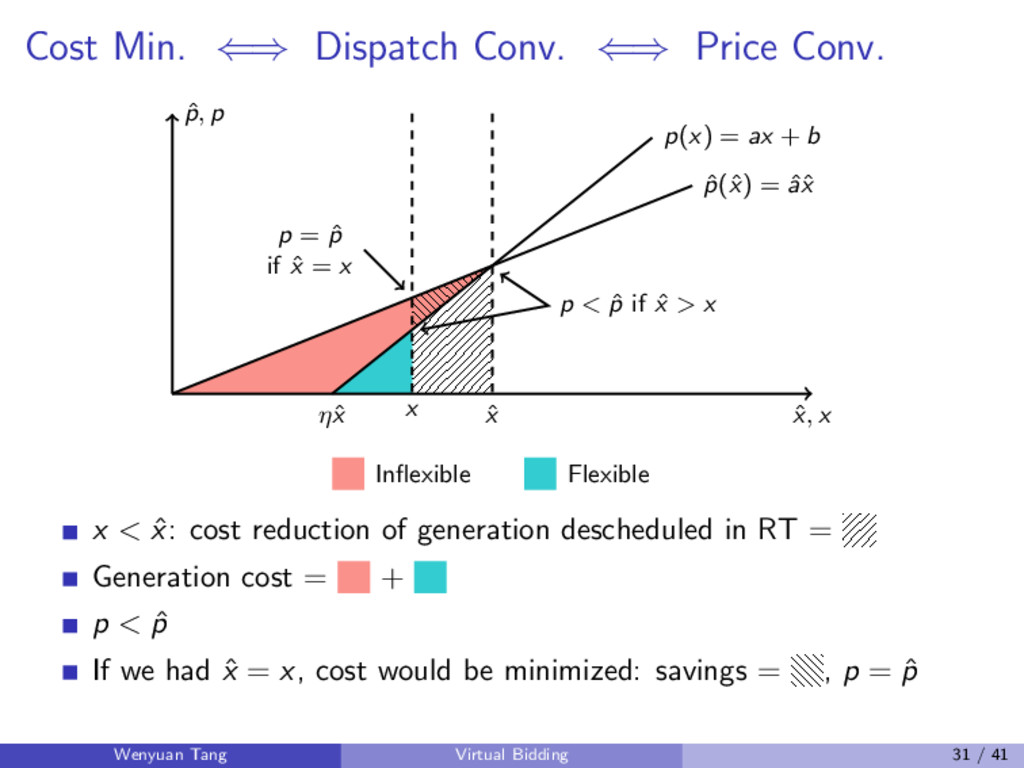

< ˆ p if ˆ x > x p = ˆ p if ˆ x = x ˆ x, x ˆ p, p ˆ p(ˆ x) = ˆ aˆ x ηˆ x p(x) = ax + b ˆ x Inflexible Flexible x < ˆ x: cost reduction of generation descheduled in RT = Generation cost = + p < ˆ p If we had ˆ x = x, cost would be minimized: savings = , p = ˆ p Wenyuan Tang Virtual Bidding 31 / 41

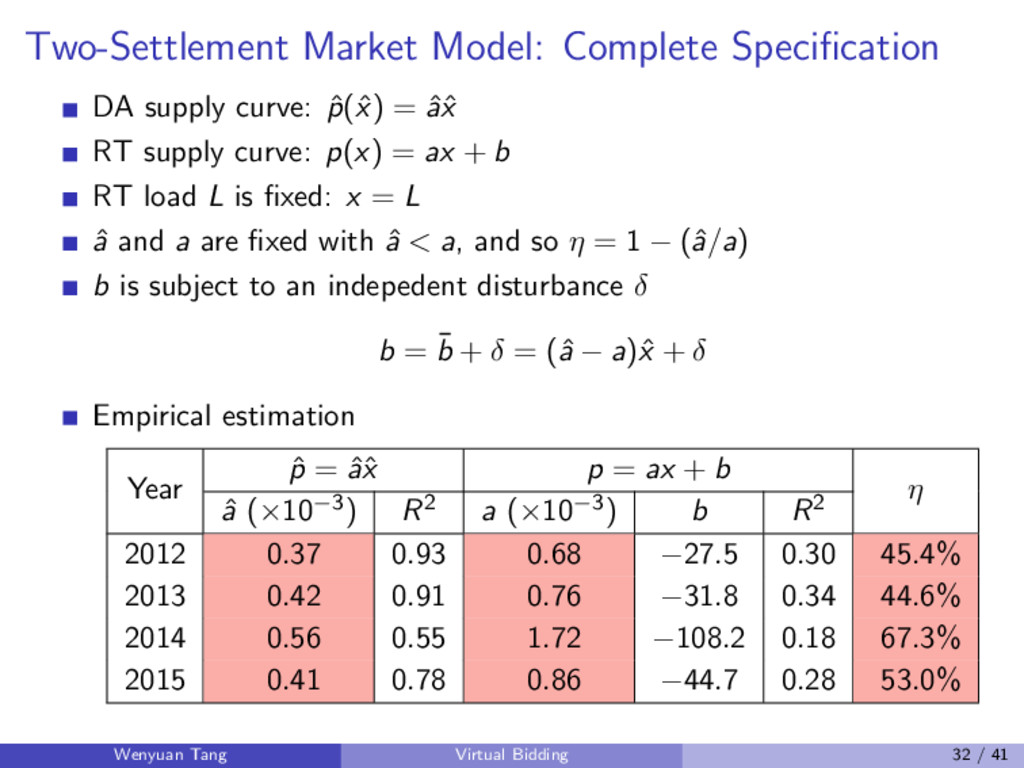

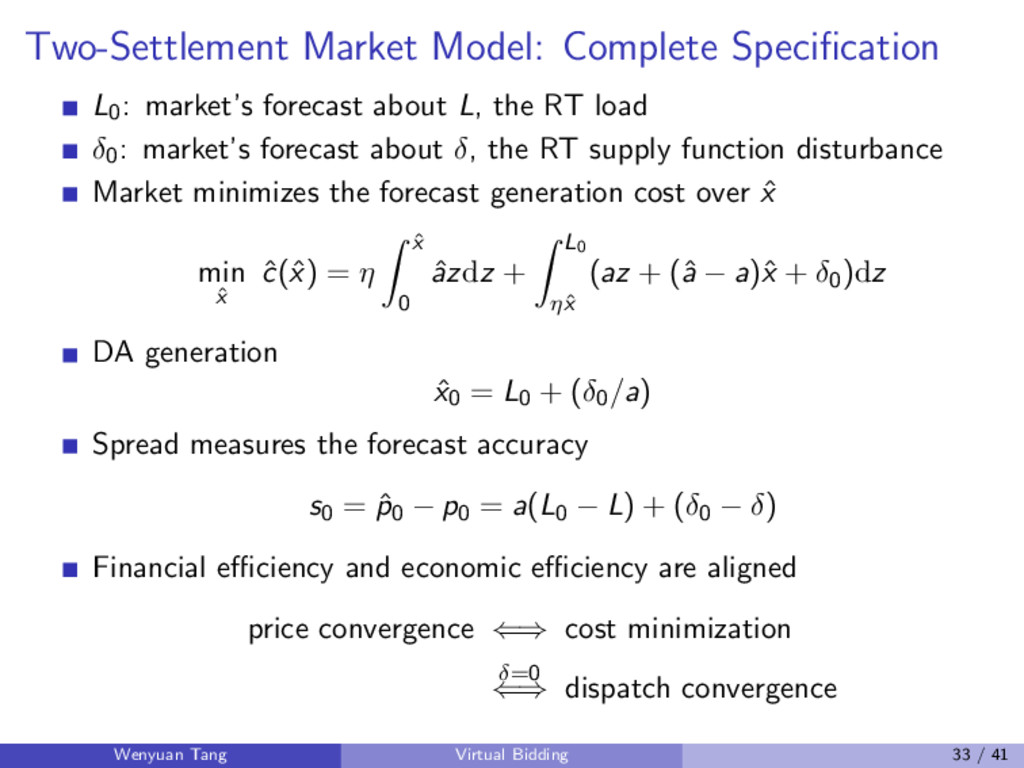

x) = ˆ aˆ x RT supply curve: p(x) = ax + b RT load L is fixed: x = L ˆ a and a are fixed with ˆ a < a, and so η = 1 − (ˆ a/a) b is subject to an indepedent disturbance δ b = ¯ b + δ = (ˆ a − a)ˆ x + δ Empirical estimation Year ˆ p = ˆ aˆ x p = ax + b η ˆ a (×10−3) R2 a (×10−3) b R2 2012 0.37 0.93 0.68 −27.5 0.30 45.4% 2013 0.42 0.91 0.76 −31.8 0.34 44.6% 2014 0.56 0.55 1.72 −108.2 0.18 67.3% 2015 0.41 0.78 0.86 −44.7 0.28 53.0% Wenyuan Tang Virtual Bidding 32 / 41

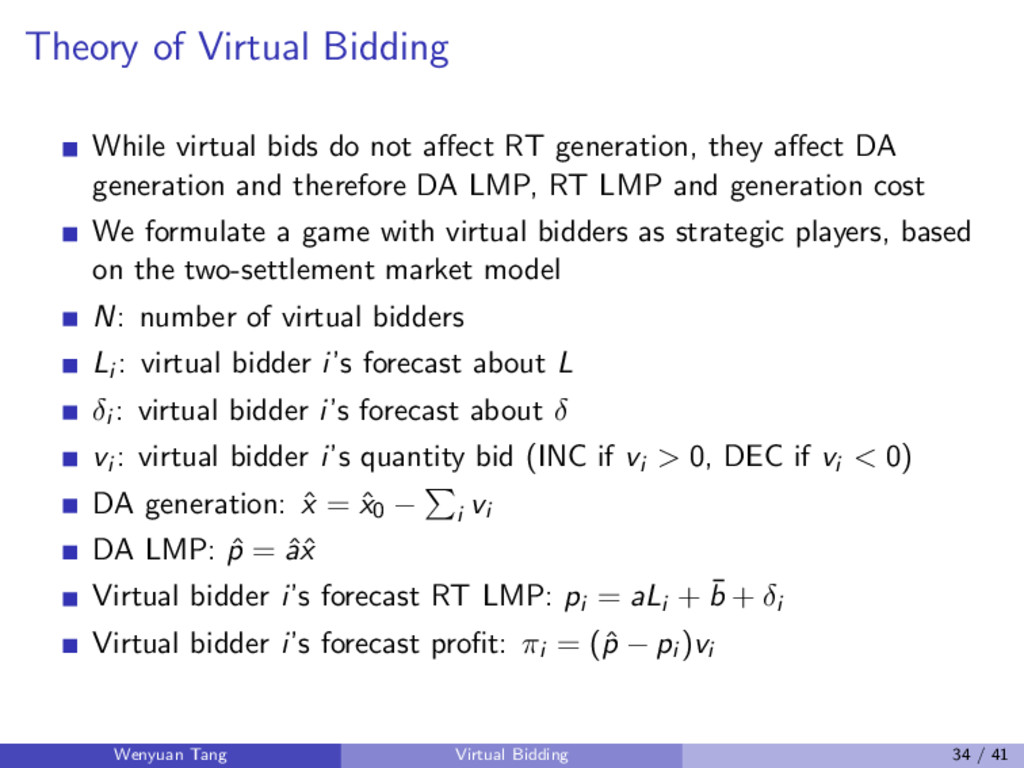

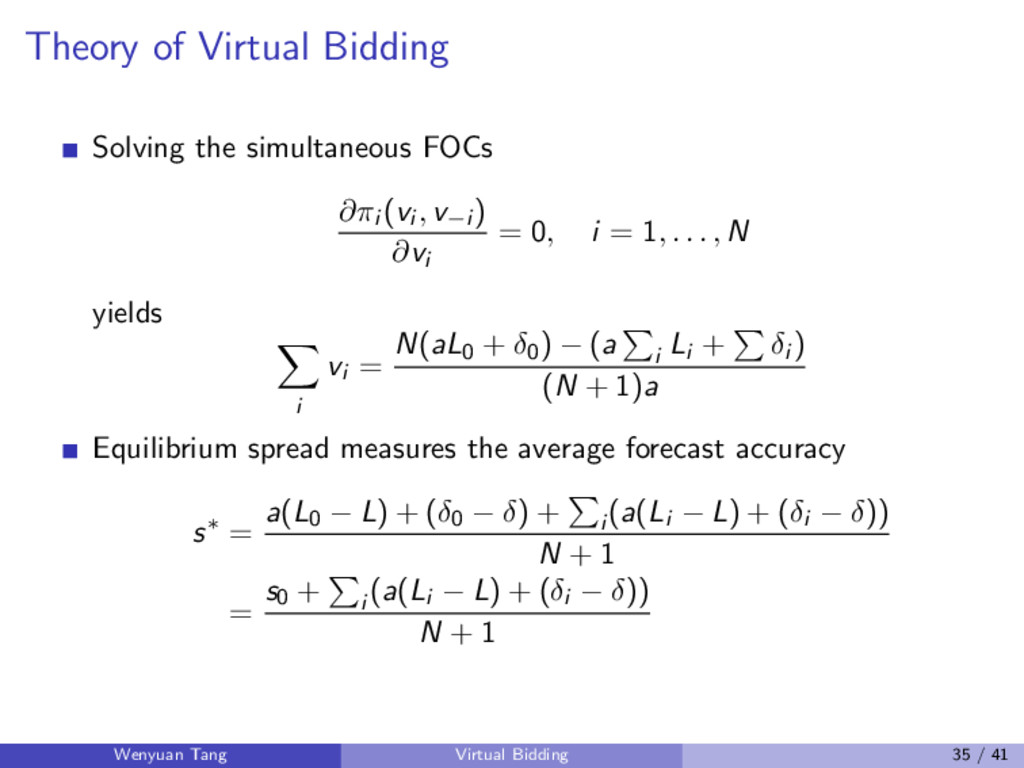

RT generation, they affect DA generation and therefore DA LMP, RT LMP and generation cost We formulate a game with virtual bidders as strategic players, based on the two-settlement market model N: number of virtual bidders Li : virtual bidder i’s forecast about L δi : virtual bidder i’s forecast about δ vi : virtual bidder i’s quantity bid (INC if vi > 0, DEC if vi < 0) DA generation: ˆ x = ˆ x0 − i vi DA LMP: ˆ p = ˆ aˆ x Virtual bidder i’s forecast RT LMP: pi = aLi + ¯ b + δi Virtual bidder i’s forecast profit: πi = (ˆ p − pi )vi Wenyuan Tang Virtual Bidding 34 / 41

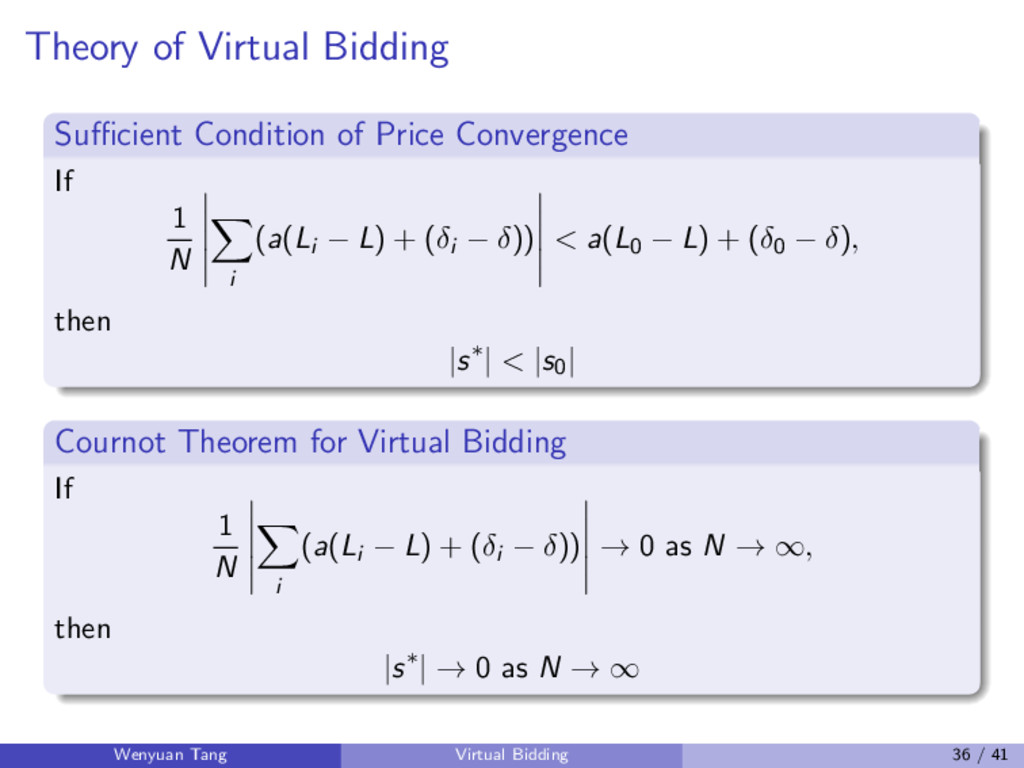

1 N i (a(Li − L) + (δi − δ)) < a(L0 − L) + (δ0 − δ), then |s∗| < |s0| Cournot Theorem for Virtual Bidding If 1 N i (a(Li − L) + (δi − δ)) → 0 as N → ∞, then |s∗| → 0 as N → ∞ Wenyuan Tang Virtual Bidding 36 / 41

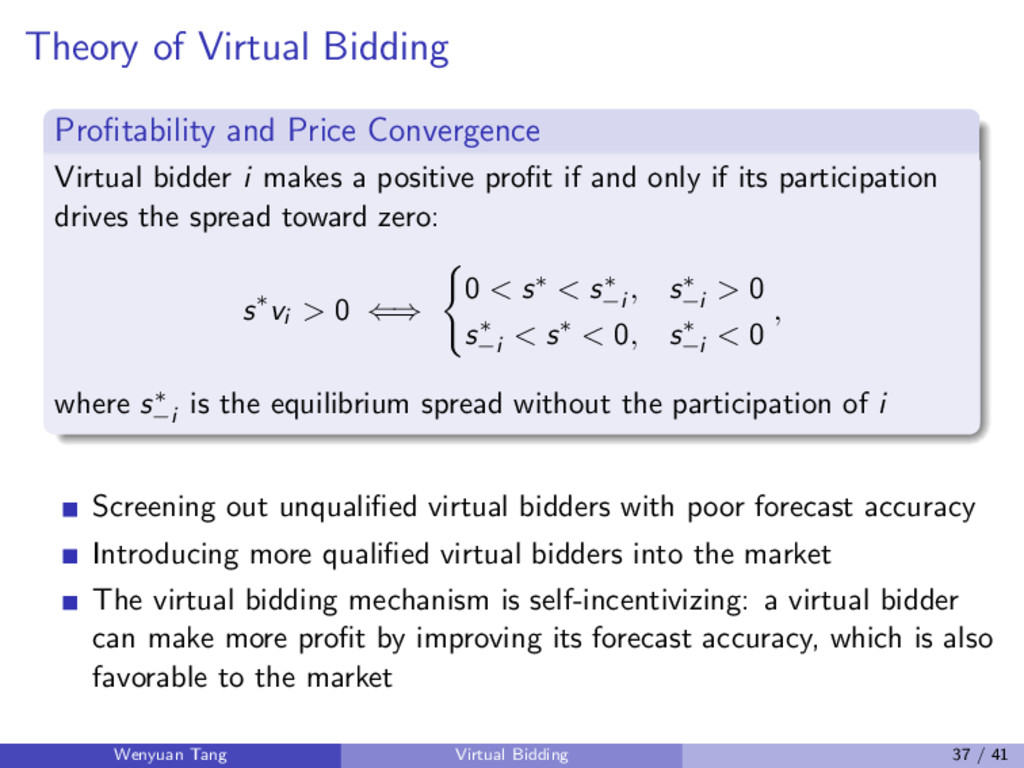

i makes a positive profit if and only if its participation drives the spread toward zero: s∗vi > 0 ⇐⇒ 0 < s∗ < s∗ −i , s∗ −i > 0 s∗ −i < s∗ < 0, s∗ −i < 0 , where s∗ −i is the equilibrium spread without the participation of i Screening out unqualified virtual bidders with poor forecast accuracy Introducing more qualified virtual bidders into the market The virtual bidding mechanism is self-incentivizing: a virtual bidder can make more profit by improving its forecast accuracy, which is also favorable to the market Wenyuan Tang Virtual Bidding 37 / 41

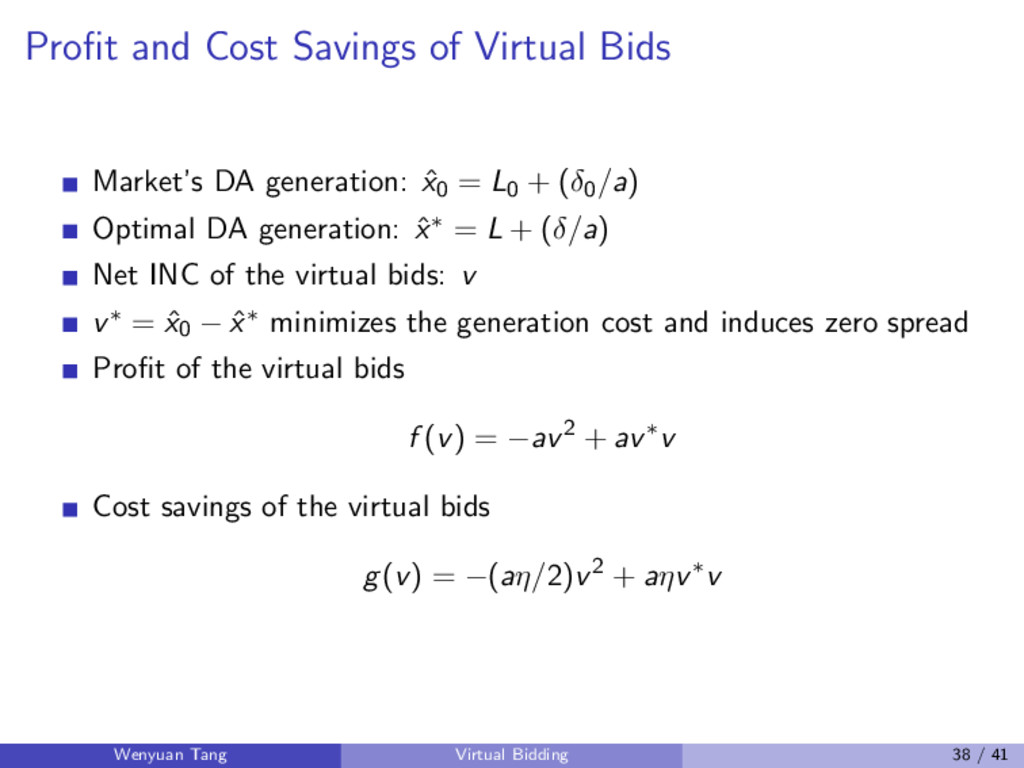

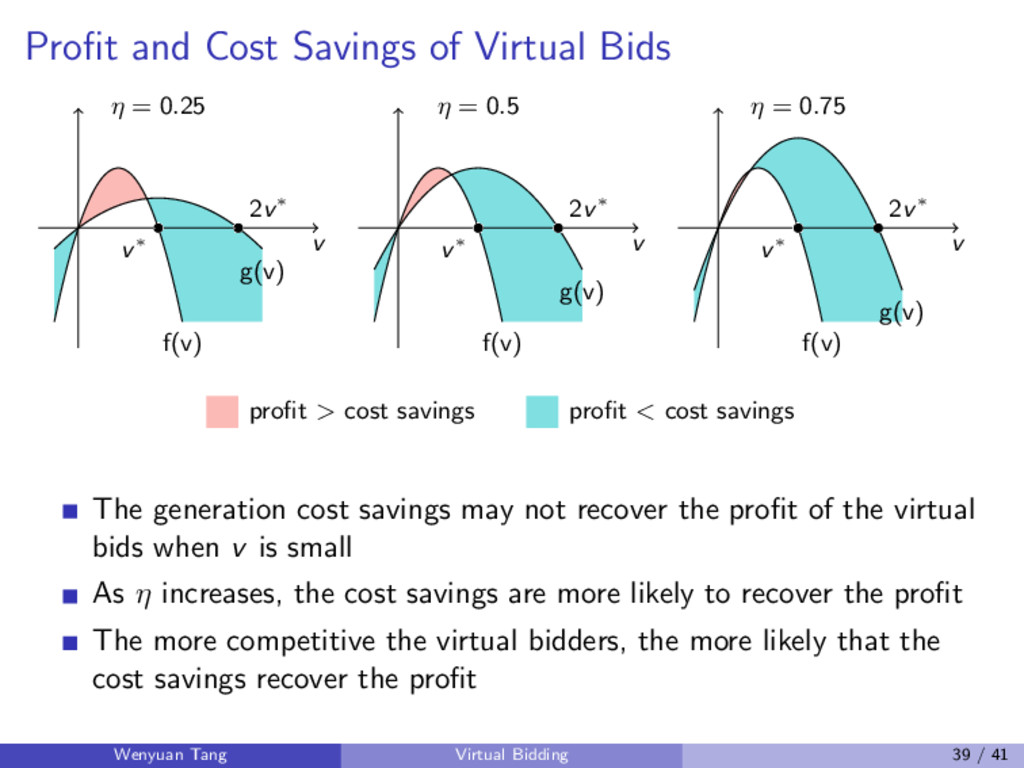

ˆ x0 = L0 + (δ0/a) Optimal DA generation: ˆ x∗ = L + (δ/a) Net INC of the virtual bids: v v∗ = ˆ x0 − ˆ x∗ minimizes the generation cost and induces zero spread Profit of the virtual bids f (v) = −av2 + av∗v Cost savings of the virtual bids g(v) = −(aη/2)v2 + aηv∗v Wenyuan Tang Virtual Bidding 38 / 41

v∗ 2v∗ η = 0.25 v f(v) g(v) v∗ 2v∗ η = 0.5 v f(v) g(v) v∗ 2v∗ η = 0.75 profit > cost savings profit < cost savings The generation cost savings may not recover the profit of the virtual bids when v is small As η increases, the cost savings are more likely to recover the profit The more competitive the virtual bidders, the more likely that the cost savings recover the profit Wenyuan Tang Virtual Bidding 39 / 41

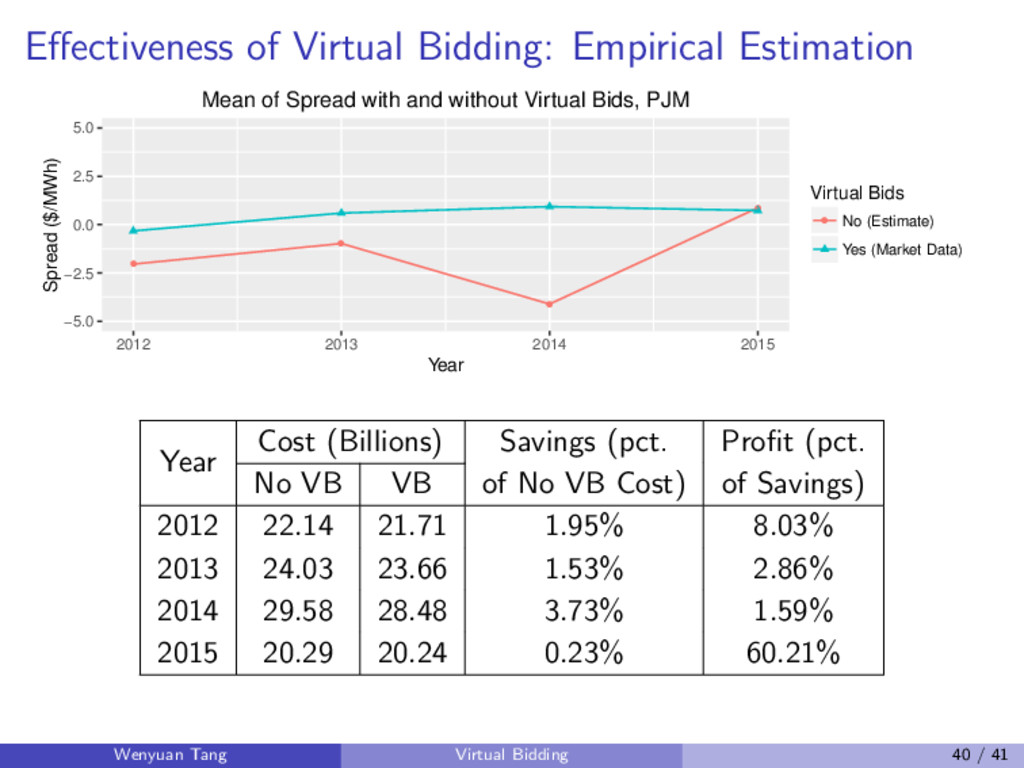

→ market model → theory and implications → methodology of estimation → empirical evidence by market data We propose a two-settlement market model which explains various phenomena in the market, and provides a methodology of estimating the generation cost The proposed model aligns financial efficiency and economic efficiency, which serves as the basis of the theory of virtual bidding Virtual bidding has improved the market efficiency: (i) comparative analysis before and after virtual bidding in CAISO; (ii) estimation of cost savings and price convergence by virtual bids in PJM There still exist substantial profitable opportunities: (i) market virtual bidders make profits; (ii) simple machine learning algorithms can be profitable on top of the market virtual bids Wenyuan Tang Virtual Bidding 41 / 41

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}