for 13 years. Executove Director of Golden Seeds, Managing Director at Dreamit Ventures, Founder of 1000 Angels and Reign Ventures. MBA from Columbia Business School and a BS from UCLA. Co-Founder & Managing Partner at 1000 Angels FOR DISCUSSION PURPOSES ONLY

Investor: An individual who makes a direct investment of personal funds into a venture; typically an early-stage businesses. Because the capital is being invested at a risky time in a business venture, the angel must be capable of taking a loss of the entire investment, and, as such, most angel investors are high-net worth individuals. These individuals are nearly always “accredited investors” as defined under the Securities Act of 1933. Note: 1000Angels requires that members be accredited to make investments

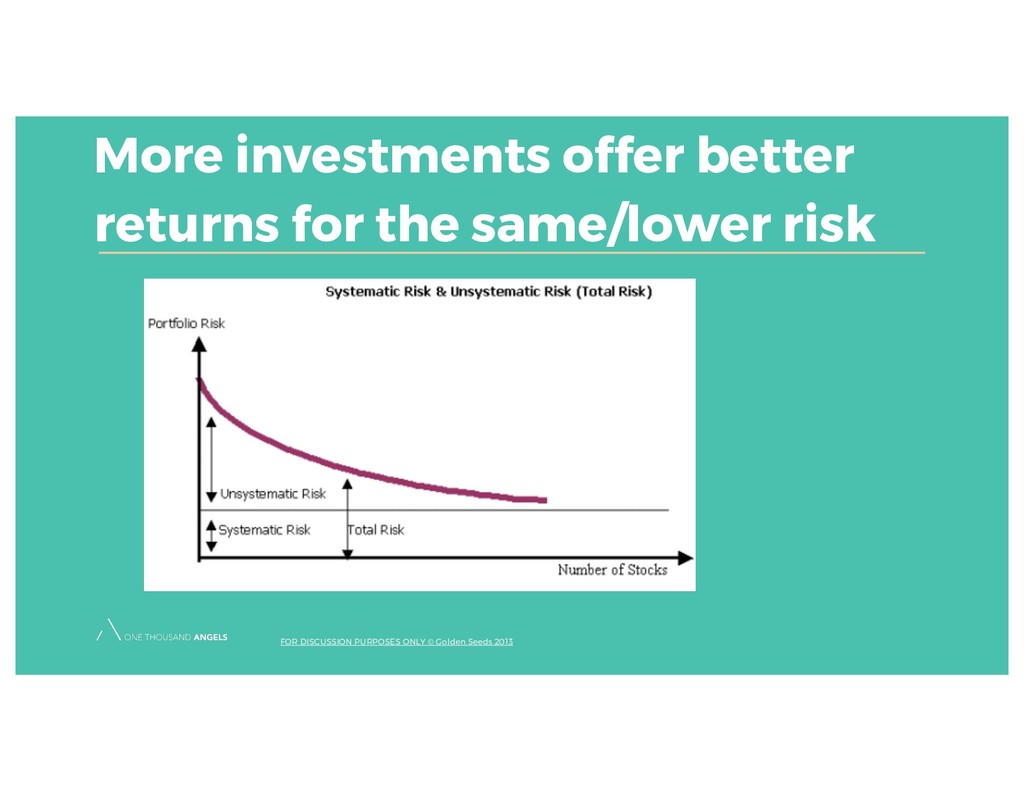

With a minimum portfolio of 10-20 investments, statistics are on your side: 30-40% - total loss 30-40% - break even 20-30% - positive return FOR DISCUSSION PURPOSES ONLY Source: Returns to Angels in Groups published November 2007 by Robert Wiltbank, PhD & Warren Boeker PhD

product and business model • Product in Market or Close to Market • Active Clients or Users • Barriers to Entry • Credible exit strategy FOR DISCUSSION PURPOSES ONLY

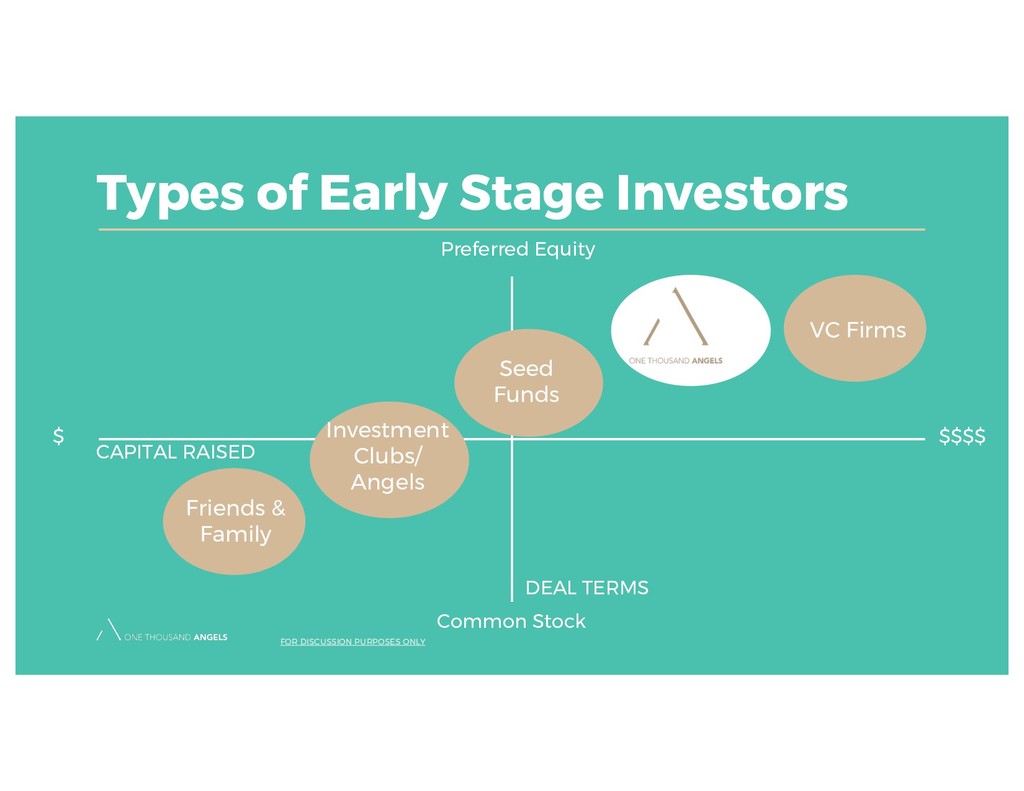

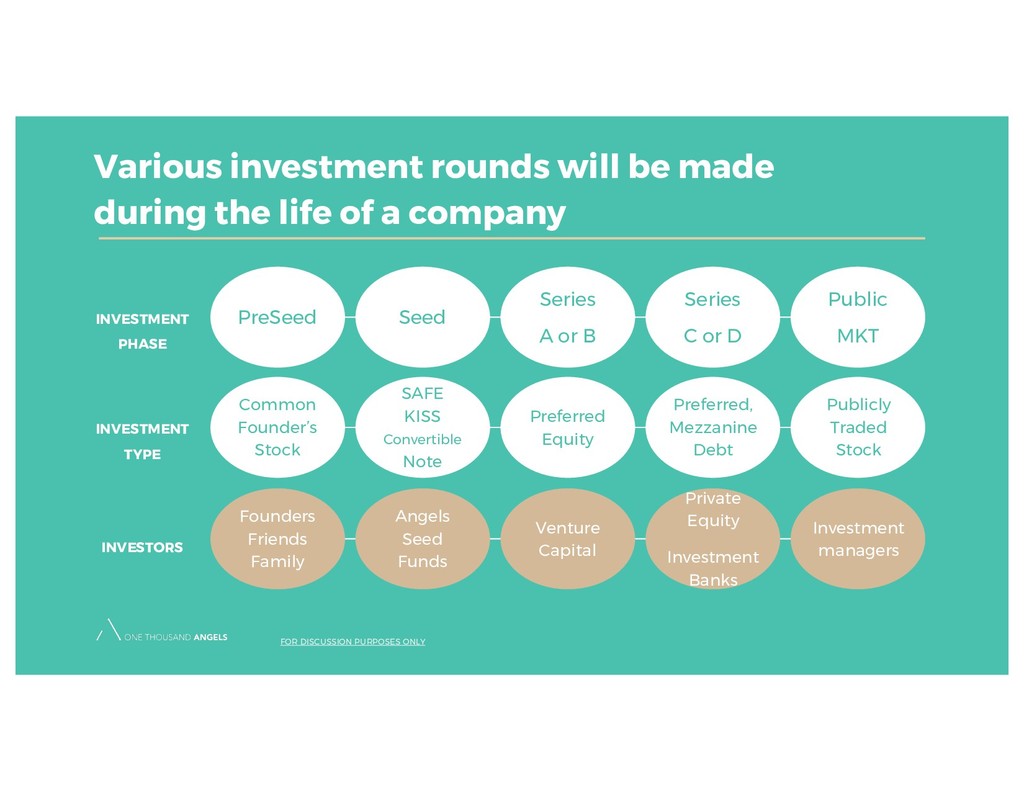

a company FOR DISCUSSION PURPOSES ONLY PreSeed INVESTMENT PHASE Seed Series A or B Series C or D Public MKT Common Founder’s Stock INVESTMENT TYPE SAFE KISS Convertible Note Preferred Equity Preferred, Mezzanine Debt Publicly Traded Stock Founders Friends Family INVESTORS Angels Seed Funds Venture Capital Private Equity Investment Banks Investment managers

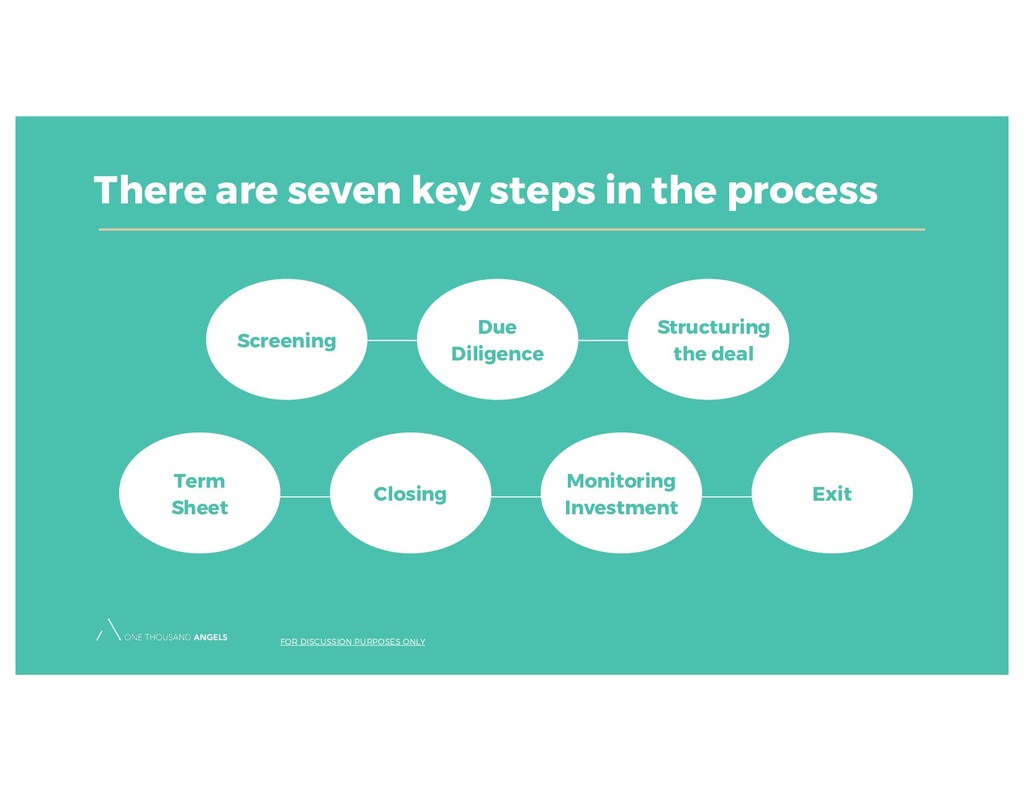

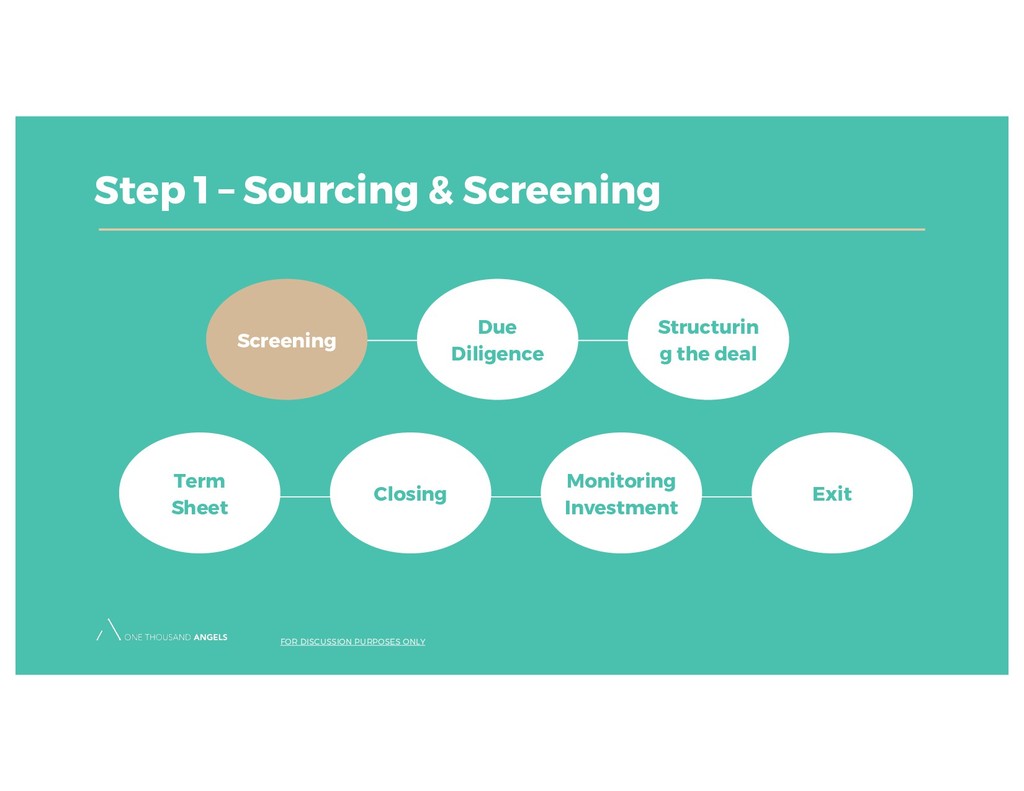

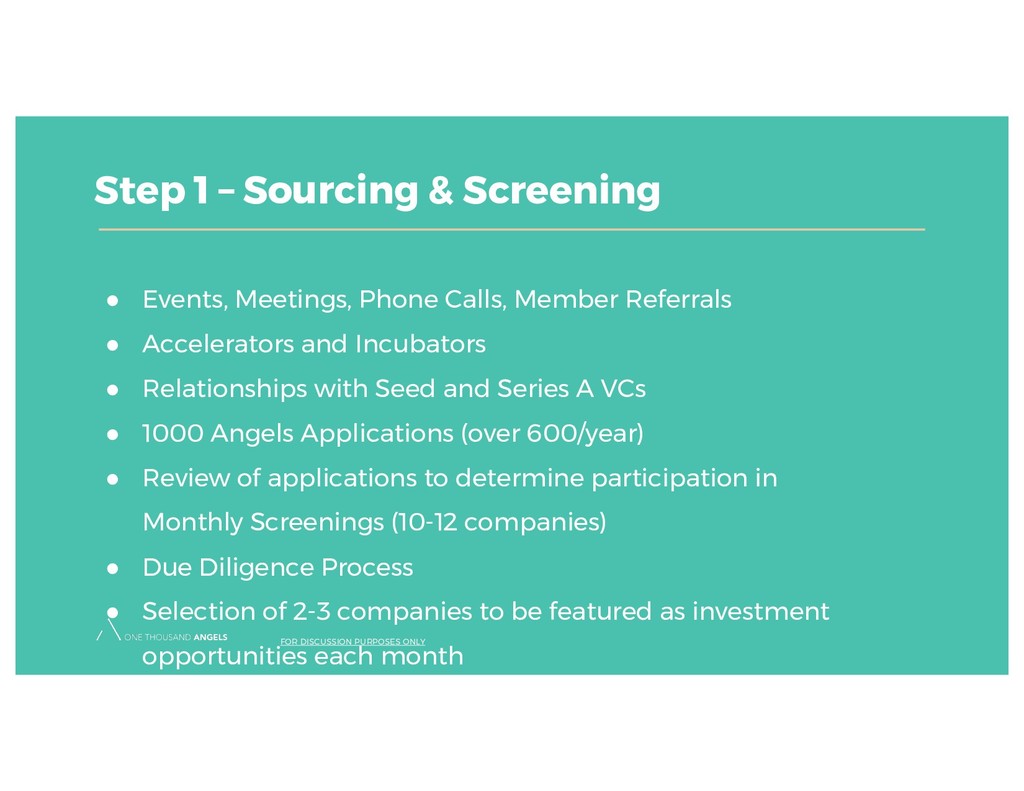

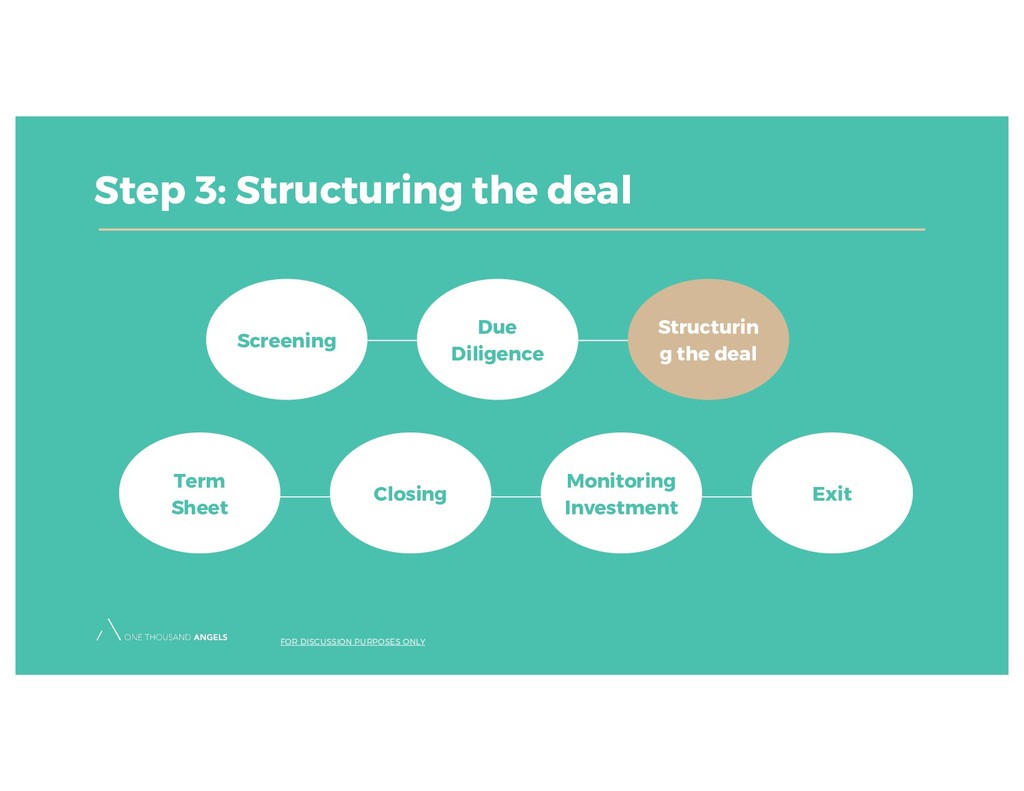

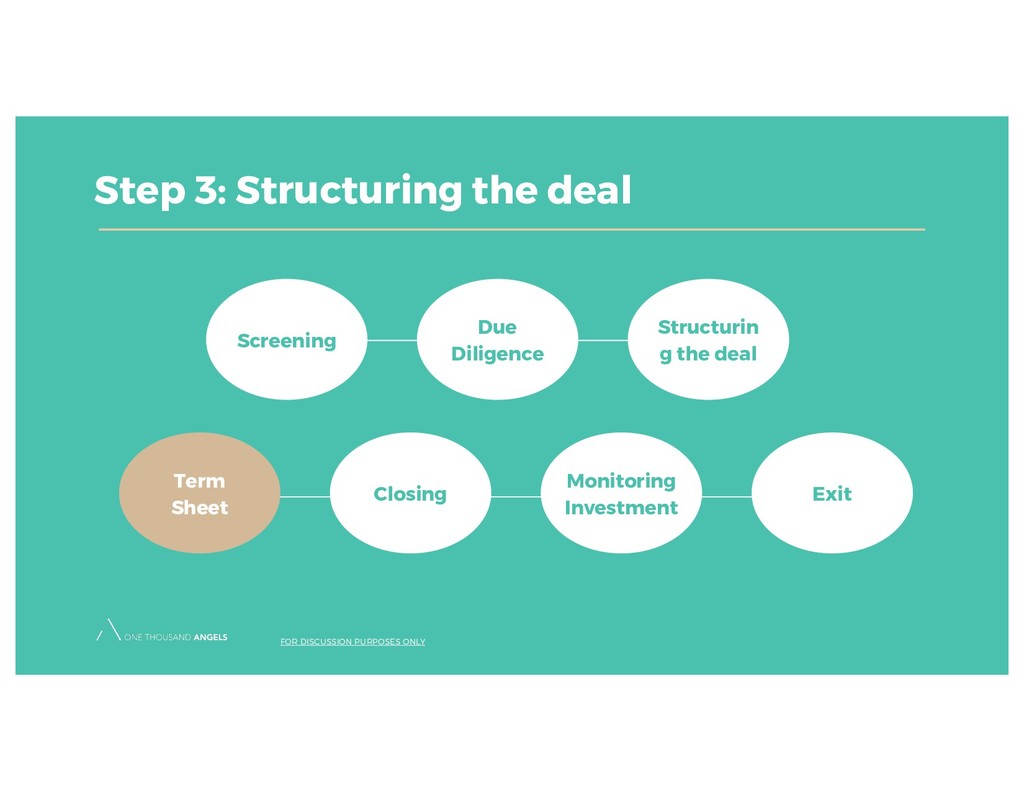

Calls, Member Referrals • Accelerators and Incubators • Relationships with Seed and Series A VCs • 1000 Angels Applications (over 600/year) • Review of applications to determine participation in Monthly Screenings (10-12 companies) • Due Diligence Process • Selection of 2-3 companies to be featured as investment opportunities each month FOR DISCUSSION PURPOSES ONLY

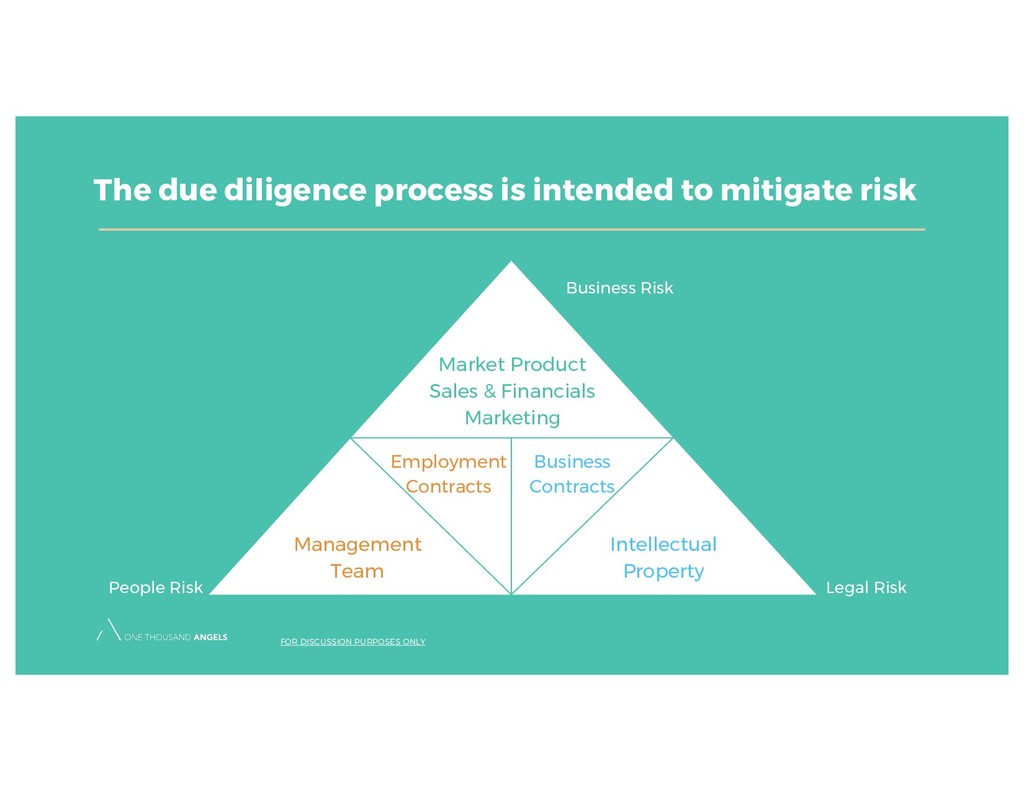

Risk FOR DISCUSSION PURPOSES ONLY Market Product Sales & Financials Marketing Management Team People Risk Legal Risk Employment Contracts Business Contracts Intellectual Property

to waste the company’s time • Don’t want to waste our time • Focus on the biggest areas of concern first • Communicate regularly with the team • Streamlined communications FOR DISCUSSION PURPOSES ONLY

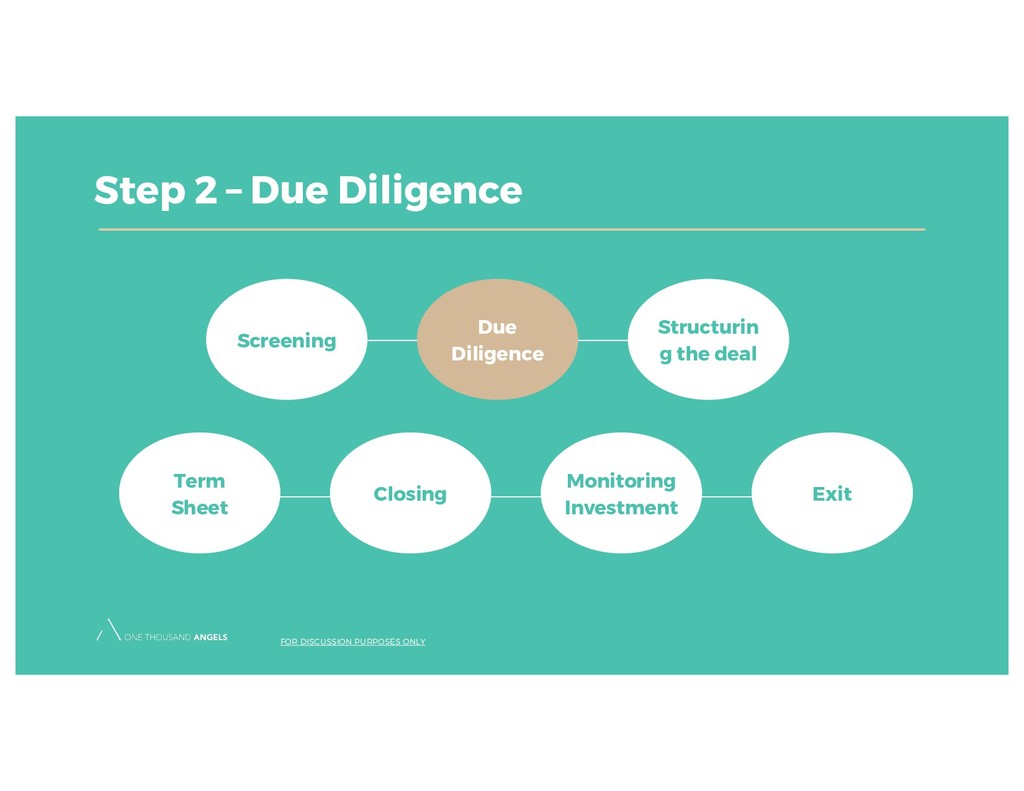

make money? Is it scalable? • Market Opportunity – has the company made good assumptions? Is it really a billion dollar opportunity? • Customers – does the company have a reasonable customer acquisition plan? Is CAC<CTLV? What is the sales cycle? • Financials – Does the financial model make sense? Are the assumptions and outcomes reasonable? Is the plan scalable? • Competition – What do we think about the company’s value proposition versus competitors? • Management Team – Reference checks and background Complete independent research FOR DISCUSSION PURPOSES ONLY

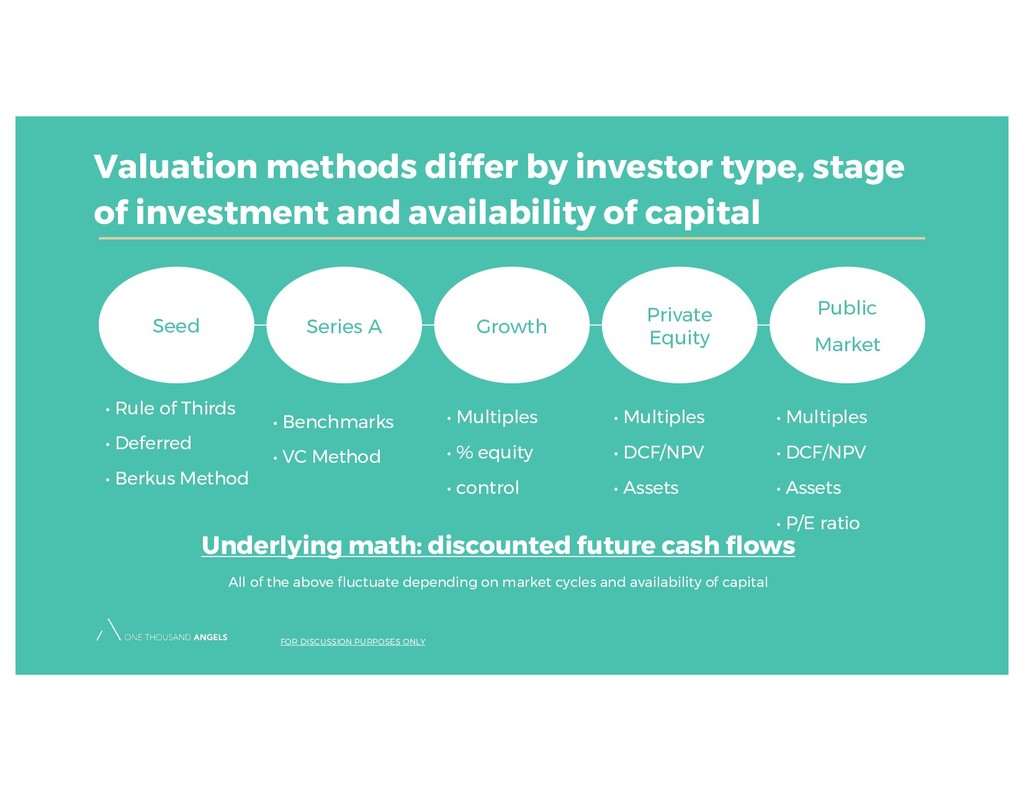

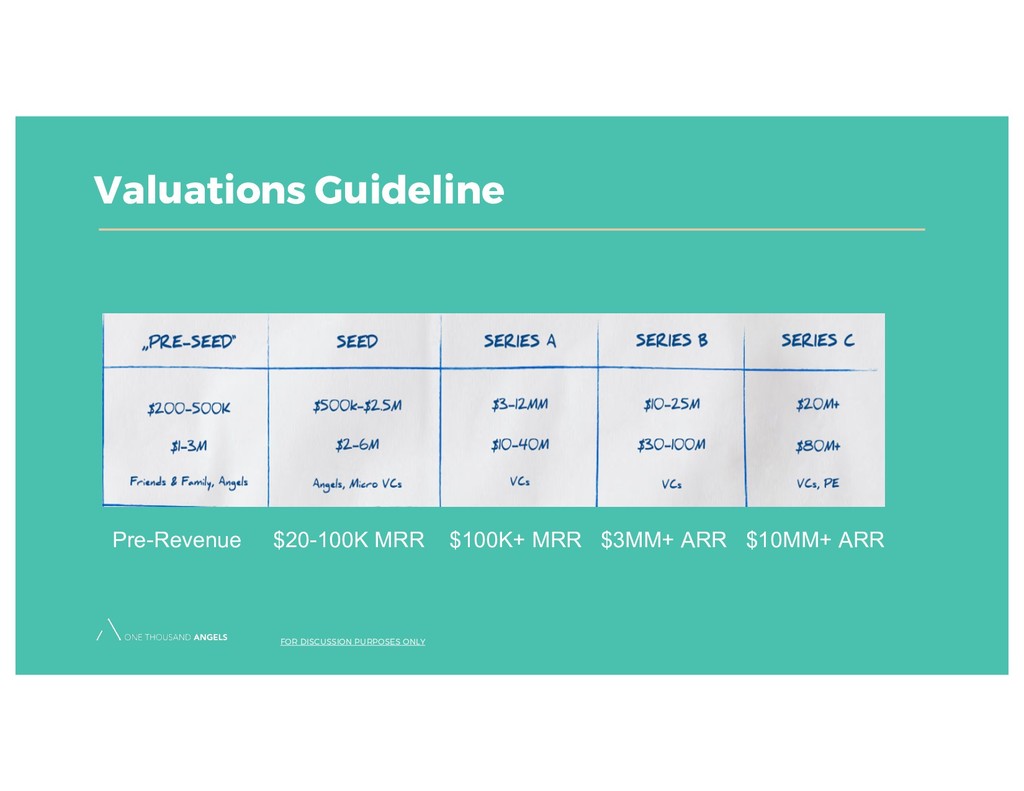

availability of capital FOR DISCUSSION PURPOSES ONLY Seed Series A Growth Private Equity Public Market • Rule of Thirds • Deferred • Berkus Method • Benchmarks • VC Method • Multiples • % equity • control • Multiples • DCF/NPV • Assets • Multiples • DCF/NPV • Assets • P/E ratio Underlying math: discounted future cash flows All of the above fluctuate depending on market cycles and availability of capital

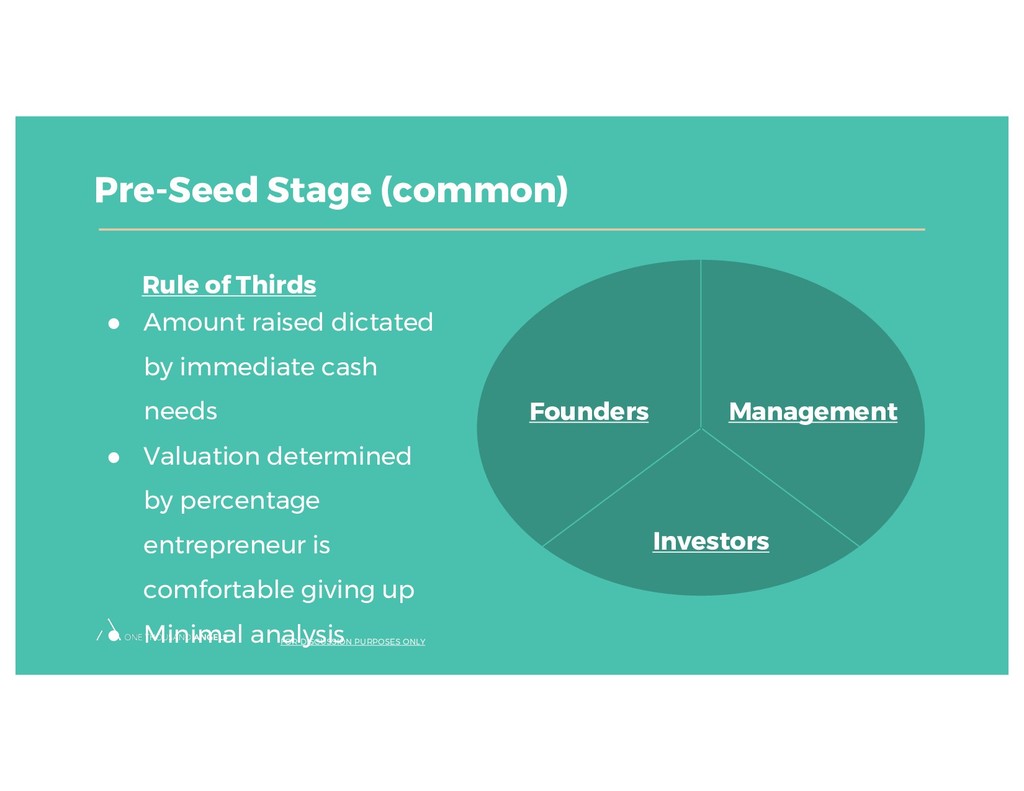

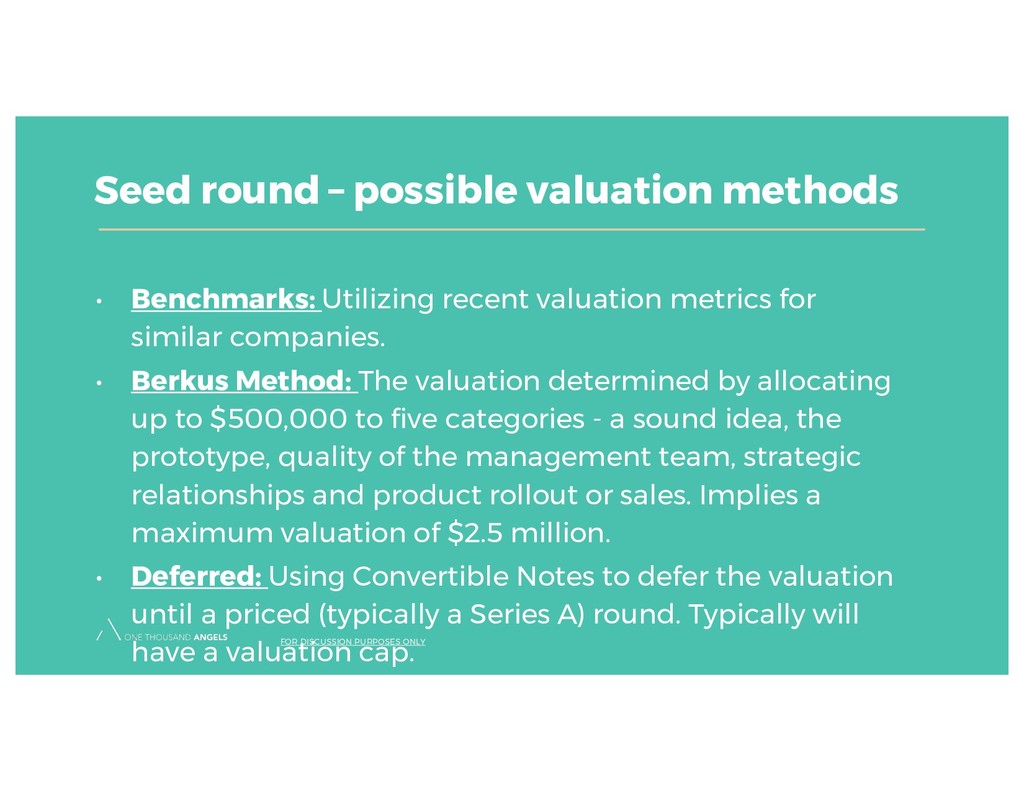

Berkus Method: The valuation determined by allocating up to $500,000 to five categories - a sound idea, the prototype, quality of the management team, strategic relationships and product rollout or sales. Implies a maximum valuation of $2.5 million. • Deferred: Using Convertible Notes to defer the valuation until a priced (typically a Series A) round. Typically will have a valuation cap. Seed round – possible valuation methods FOR DISCUSSION PURPOSES ONLY

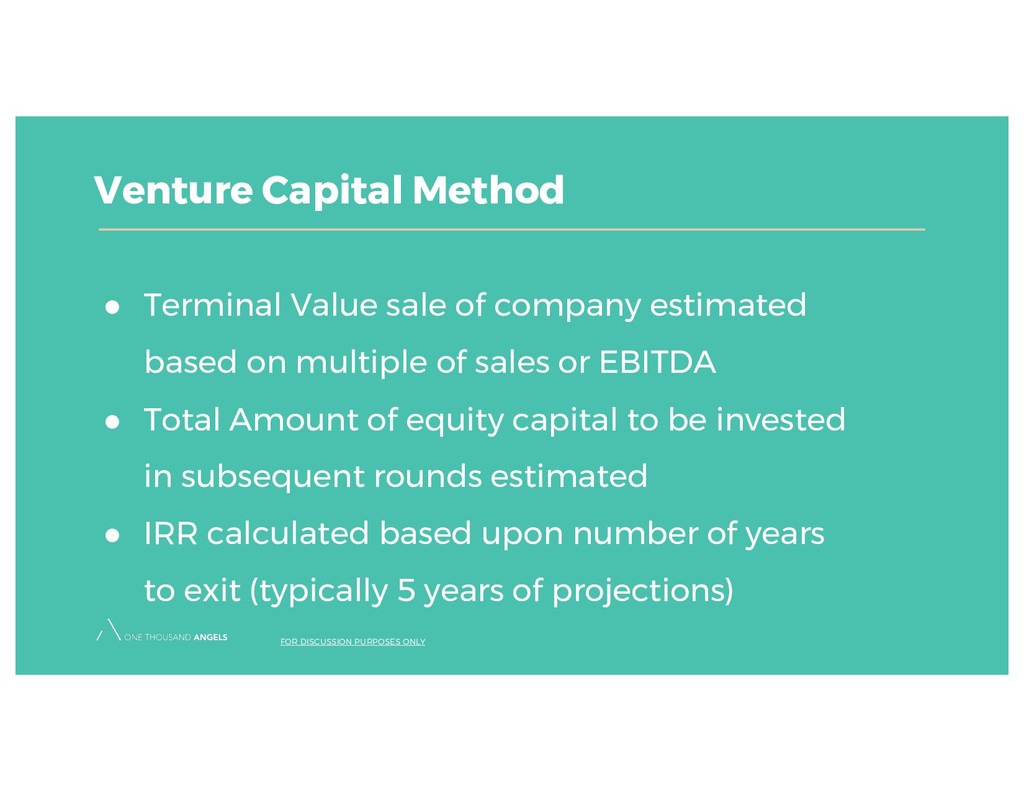

of sales or EBITDA • Total Amount of equity capital to be invested in subsequent rounds estimated • IRR calculated based upon number of years to exit (typically 5 years of projections) Venture Capital Method FOR DISCUSSION PURPOSES ONLY

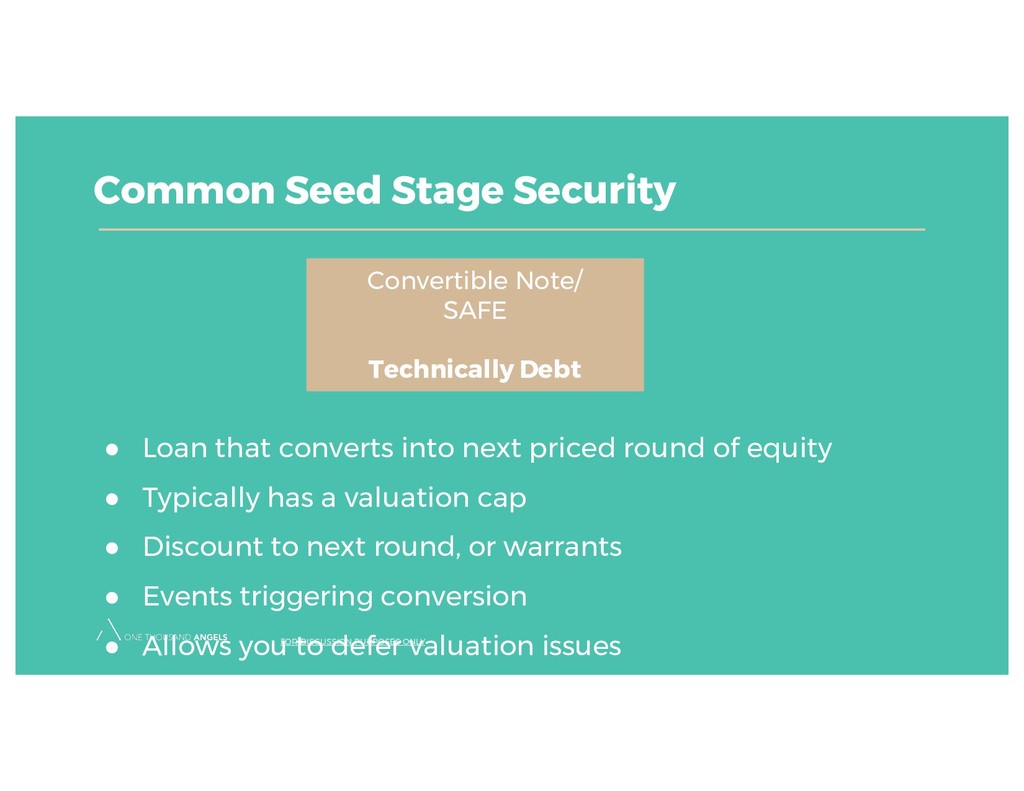

priced round of equity • Typically has a valuation cap • Discount to next round, or warrants • Events triggering conversion • Allows you to defer valuation issues FOR DISCUSSION PURPOSES ONLY Convertible Note/ SAFE Technically Debt

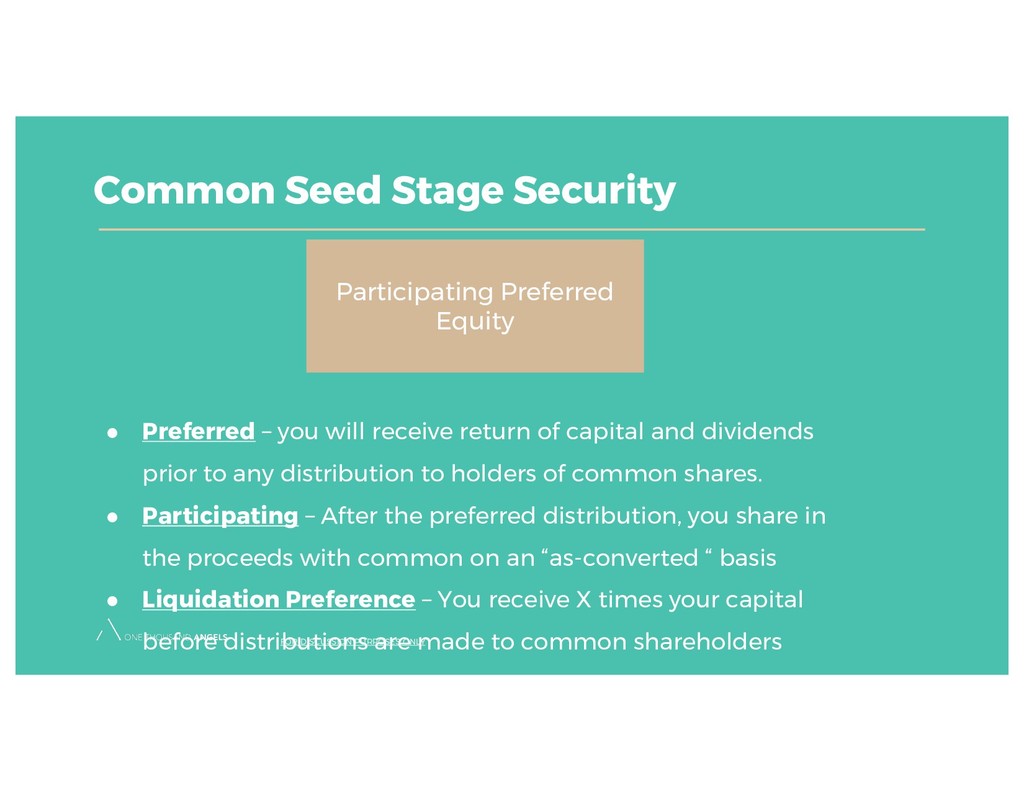

return of capital and dividends prior to any distribution to holders of common shares. • Participating – After the preferred distribution, you share in the proceeds with common on an “as-converted “ basis • Liquidation Preference – You receive X times your capital before distributions are made to common shareholders FOR DISCUSSION PURPOSES ONLY Participating Preferred Equity

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}