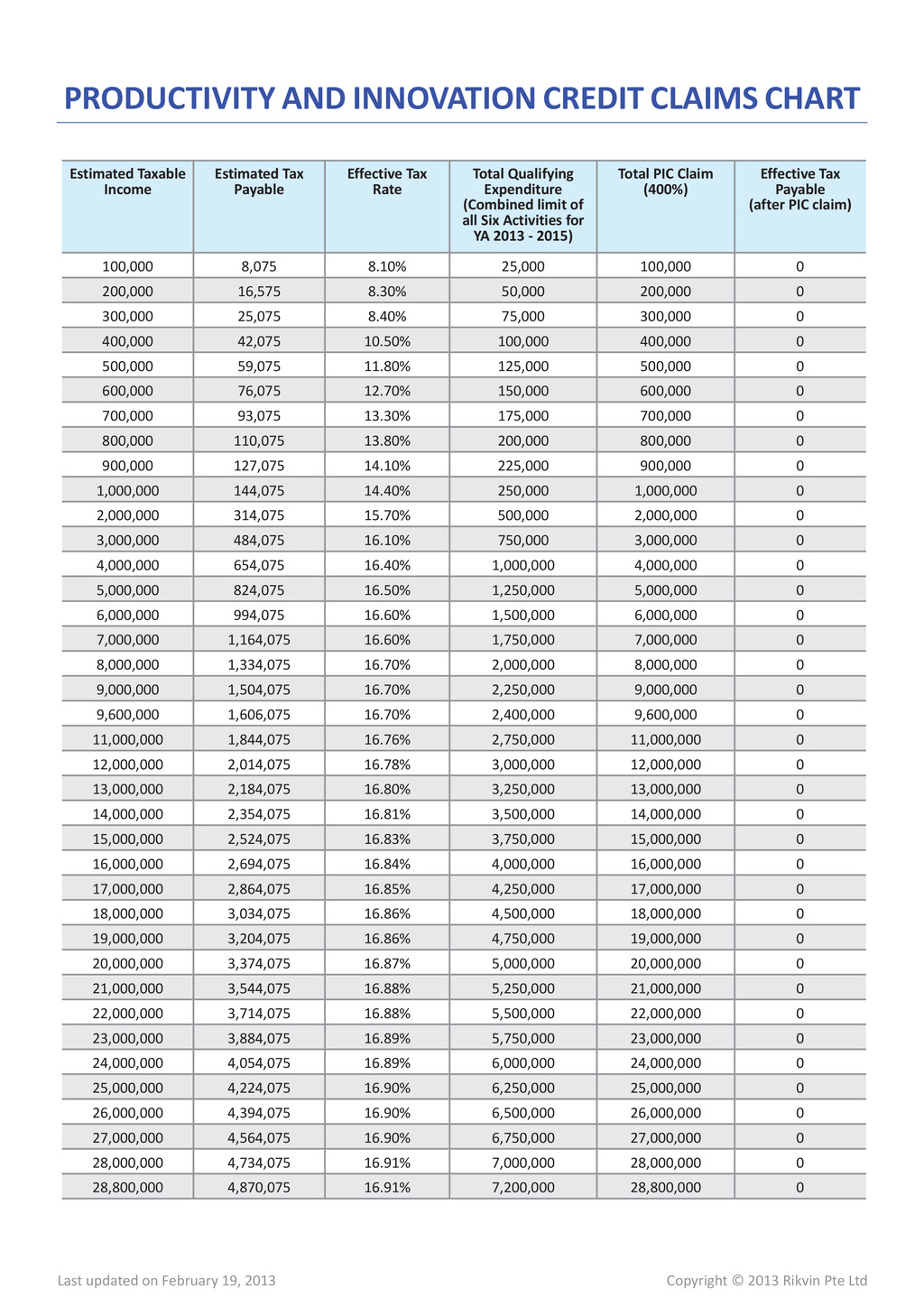

19, 2013 Estimated Taxable Income Estimated Tax Payable Effective Tax Rate Total Qualifying Expenditure (Combined limit of all Six Activities for YA 2013 - 2015) Total PIC Claim (400%) Effective Tax Payable (after PIC claim) 100,000 8,075 8.10% 25,000 100,000 0 200,000 16,575 8.30% 50,000 200,000 0 300,000 25,075 8.40% 75,000 300,000 0 400,000 42,075 10.50% 100,000 400,000 0 500,000 59,075 11.80% 125,000 500,000 0 600,000 76,075 12.70% 150,000 600,000 0 700,000 93,075 13.30% 175,000 700,000 0 800,000 110,075 13.80% 200,000 800,000 0 900,000 127,075 14.10% 225,000 900,000 0 1,000,000 144,075 14.40% 250,000 1,000,000 0 2,000,000 314,075 15.70% 500,000 2,000,000 0 3,000,000 484,075 16.10% 750,000 3,000,000 0 4,000,000 654,075 16.40% 1,000,000 4,000,000 0 5,000,000 824,075 16.50% 1,250,000 5,000,000 0 6,000,000 994,075 16.60% 1,500,000 6,000,000 0 7,000,000 1,164,075 16.60% 1,750,000 7,000,000 0 8,000,000 1,334,075 16.70% 2,000,000 8,000,000 0 9,000,000 1,504,075 16.70% 2,250,000 9,000,000 0 9,600,000 1,606,075 16.70% 2,400,000 9,600,000 0 11,000,000 1,844,075 16.76% 2,750,000 11,000,000 0 12,000,000 2,014,075 16.78% 3,000,000 12,000,000 0 13,000,000 2,184,075 16.80% 3,250,000 13,000,000 0 14,000,000 2,354,075 16.81% 3,500,000 14,000,000 0 15,000,000 2,524,075 16.83% 3,750,000 15,000,000 0 16,000,000 2,694,075 16.84% 4,000,000 16,000,000 0 17,000,000 2,864,075 16.85% 4,250,000 17,000,000 0 18,000,000 3,034,075 16.86% 4,500,000 18,000,000 0 19,000,000 3,204,075 16.86% 4,750,000 19,000,000 0 20,000,000 3,374,075 16.87% 5,000,000 20,000,000 0 21,000,000 3,544,075 16.88% 5,250,000 21,000,000 0 22,000,000 3,714,075 16.88% 5,500,000 22,000,000 0 23,000,000 3,884,075 16.89% 5,750,000 23,000,000 0 24,000,000 4,054,075 16.89% 6,000,000 24,000,000 0 25,000,000 4,224,075 16.90% 6,250,000 25,000,000 0 26,000,000 4,394,075 16.90% 6,500,000 26,000,000 0 27,000,000 4,564,075 16.90% 6,750,000 27,000,000 0 28,000,000 4,734,075 16.91% 7,000,000 28,000,000 0 28,800,000 4,870,075 16.91% 7,200,000 28,800,000 0 PRODUCTIVITY AND INNOVATION CREDIT CLAIMS CHART

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}