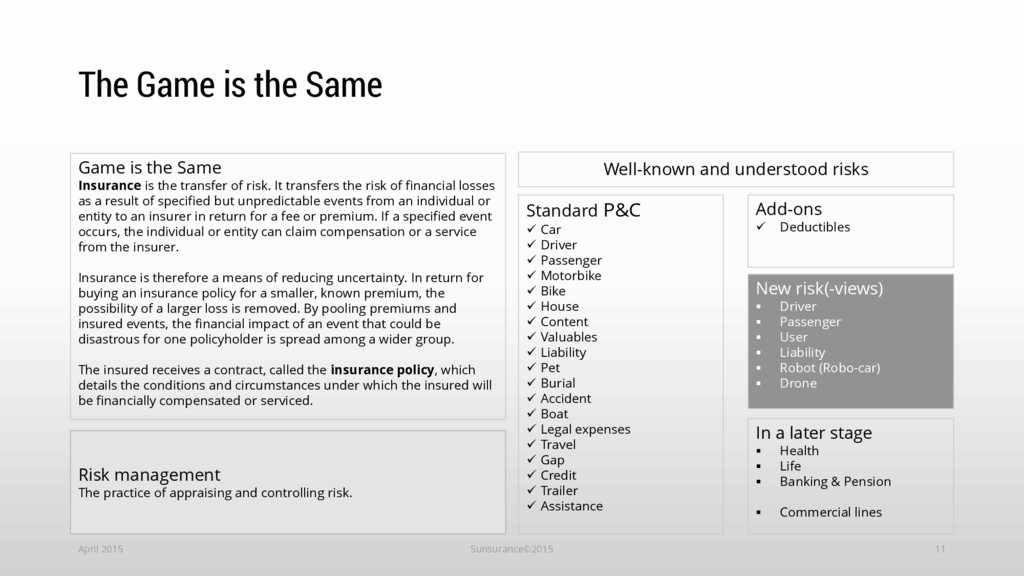

and understood risks Standard P&C Car Driver Passenger Motorbike Bike House Content Valuables Liability Pet Burial Accident Boat Legal expenses Travel Gap Credit Trailer Assistance Add-ons Deductibles New risk(-views) Driver Passenger User Liability Robot (Robo-car) Drone Game is the Same Insurance is the transfer of risk. It transfers the risk of financial losses as a result of specified but unpredictable events from an individual or entity to an insurer in return for a fee or premium. If a specified event occurs, the individual or entity can claim compensation or a service from the insurer. Insurance is therefore a means of reducing uncertainty. In return for buying an insurance policy for a smaller, known premium, the possibility of a larger loss is removed. By pooling premiums and insured events, the financial impact of an event that could be disastrous for one policyholder is spread among a wider group. The insured receives a contract, called the insurance policy, which details the conditions and circumstances under which the insured will be financially compensated or serviced. In a later stage Health Life Banking & Pension Commercial lines Risk management The practice of appraising and controlling risk.

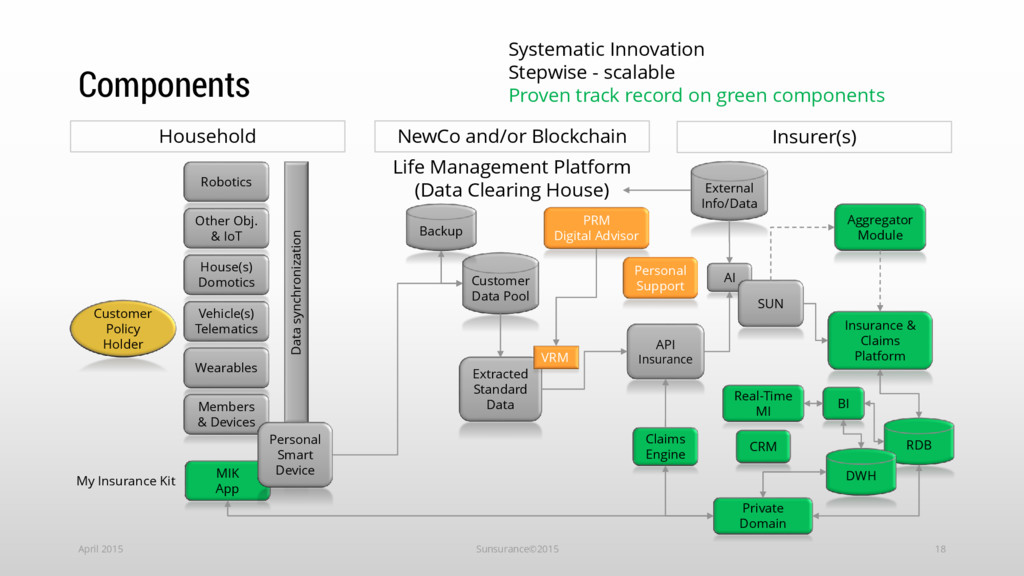

Holder Extracted Standard Data SUN Insurance & Claims Platform Private Domain Vehicle(s) Telematics Wearables MIK App House(s) Domotics Household Data synchronization RDB Customer Data Pool Backup Members & Devices Systematic Innovation Stepwise - scalable Proven track record on green components Aggregator Module Robotics Personal Smart Device DWH Real-Time MI BI Claims Engine NewCo and/or Blockchain Insurer(s) My Insurance Kit External Info/Data Other Obj. & IoT VRM Life Management Platform (Data Clearing House) PRM Digital Advisor Personal Support CRM

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}