summer of 2010. It was his first ‘real job’ and he’s never left. He currently works as the Vice President of Sales. Previously, Christian was the General Manager of Bookkeeping and Accounting Services, supervising a team of accountants that deliver services to our 1,000+ non-profit clients.

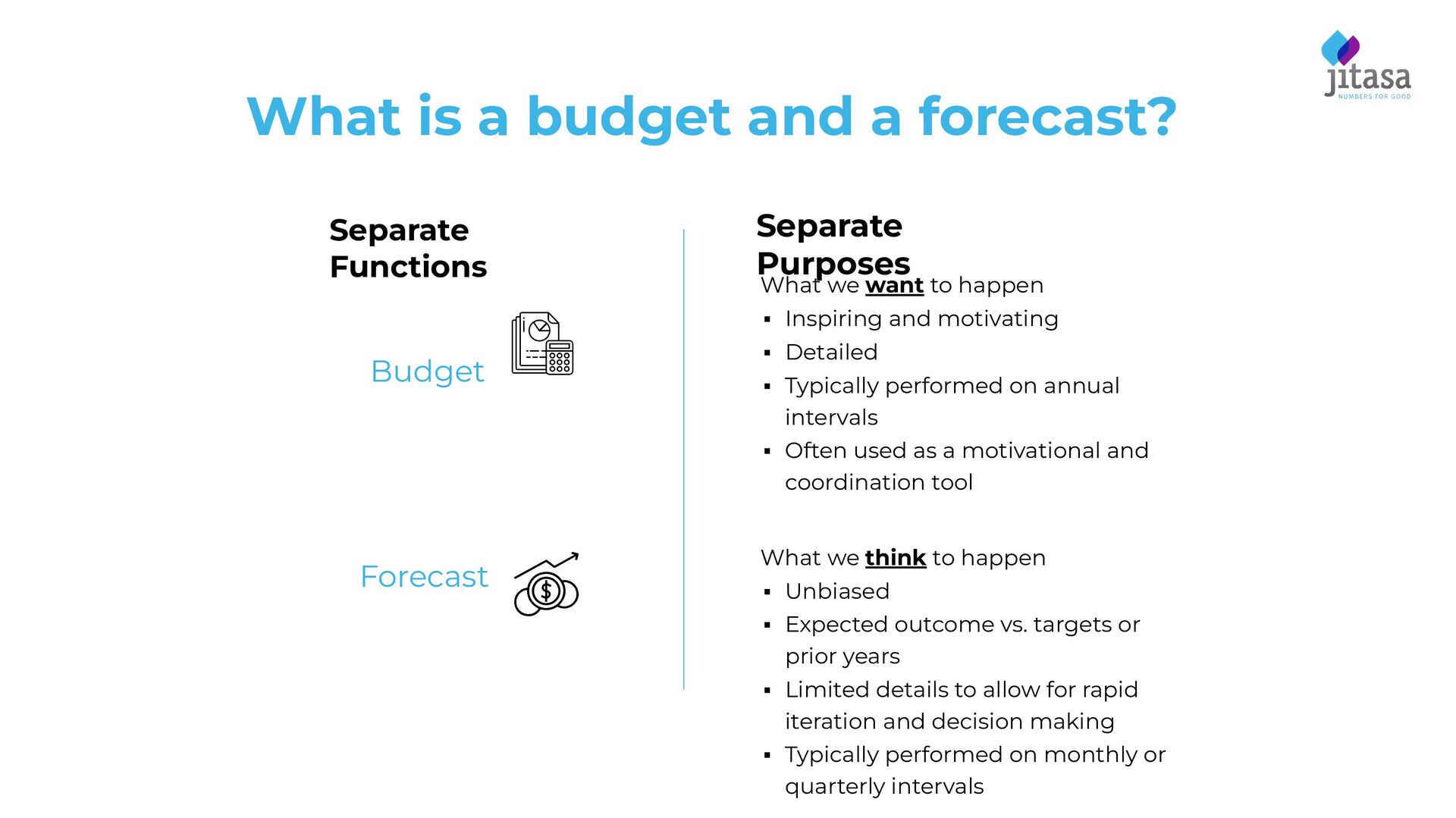

Forecast Separate Purposes What we want to happen ▪ Inspiring and motivating ▪ Detailed ▪ Typically performed on annual intervals ▪ Often used as a motivational and coordination tool What we think to happen ▪ Unbiased ▪ Expected outcome vs. targets or prior years ▪ Limited details to allow for rapid iteration and decision making ▪ Typically performed on monthly or quarterly intervals

the ocean • The path to the destination is mapped from the start • The path of the ship is continuously monitored • There can be many unforeseen obstacles (such as weather) • Corrective action is taken when the ship steers off course

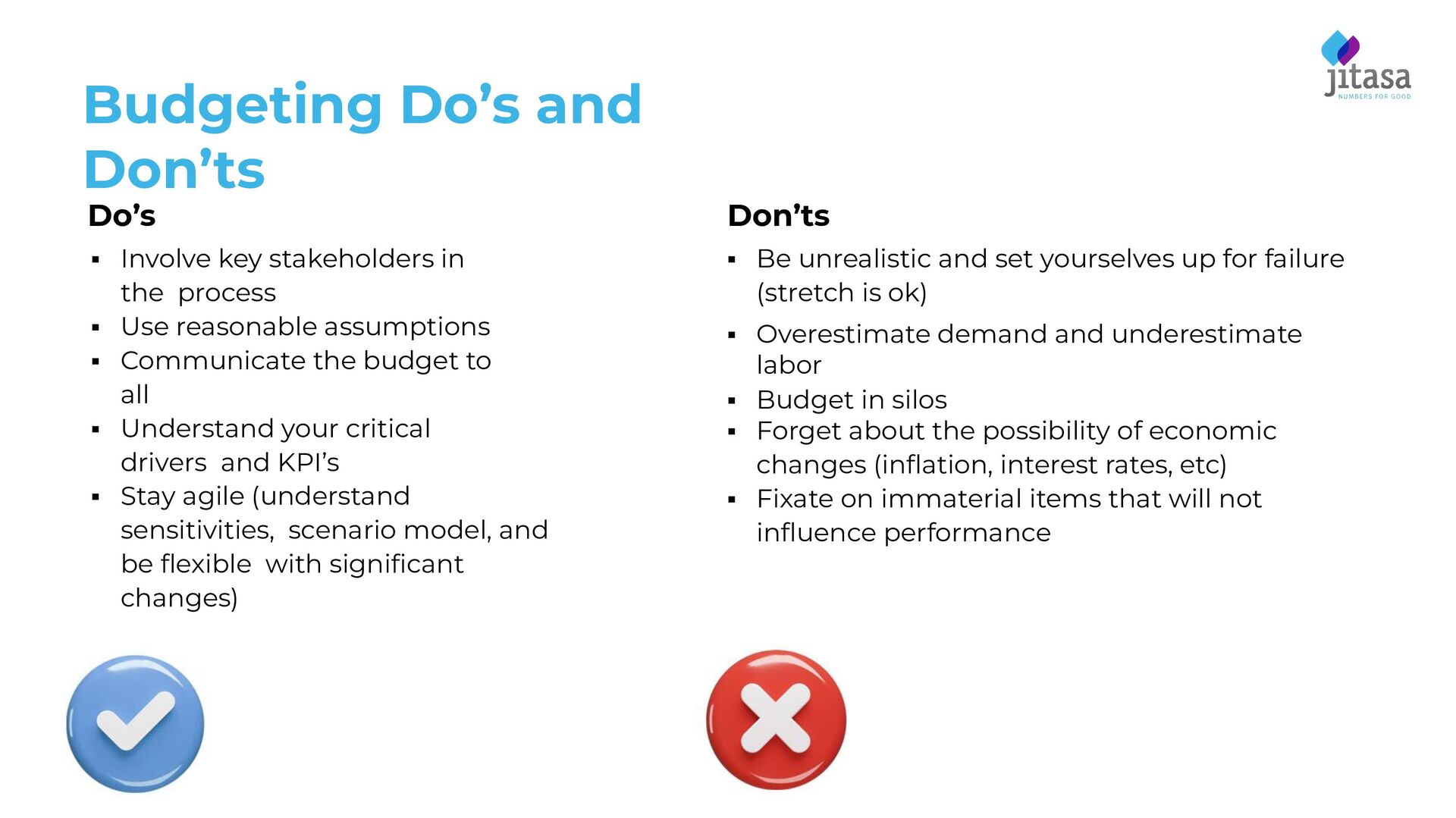

reasonable assumptions ▪ Communicate the budget to all ▪ Understand your critical drivers and KPI’s ▪ Stay agile (understand sensitivities, scenario model, and be flexible with significant changes) Don’ts ▪ Be unrealistic and set yourselves up for failure (stretch is ok) ▪ Overestimate demand and underestimate labor ▪ Budget in silos ▪ Forget about the possibility of economic changes (inflation, interest rates, etc) ▪ Fixate on immaterial items that will not influence performance Budgeting Do’s and Don’ts

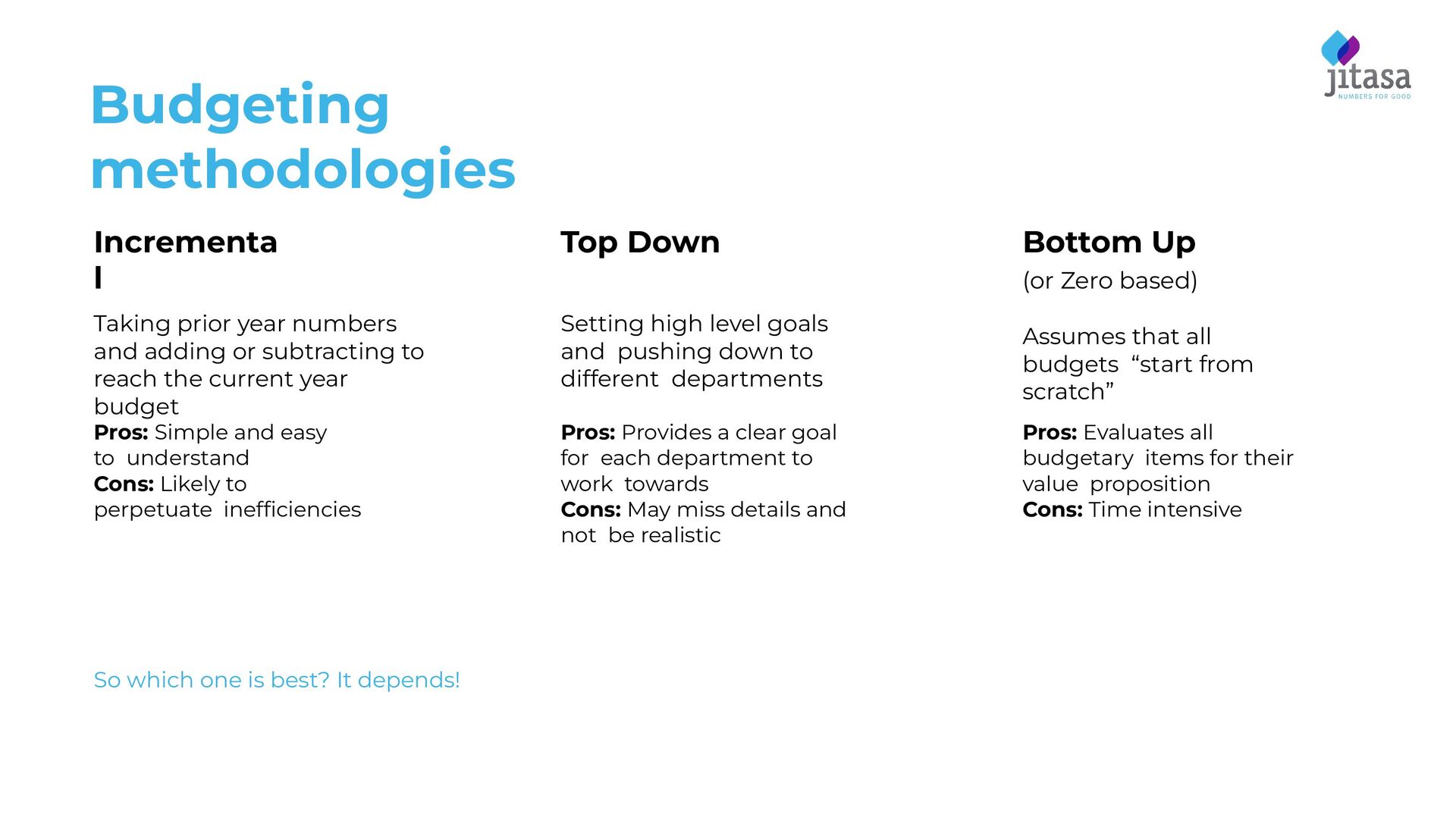

that all budgets “start from scratch” Budgeting methodologies So which one is best? It depends! Taking prior year numbers and adding or subtracting to reach the current year budget Pros: Simple and easy to understand Cons: Likely to perpetuate inefficiencies Setting high level goals and pushing down to different departments Pros: Provides a clear goal for each department to work towards Cons: May miss details and not be realistic Pros: Evaluates all budgetary items for their value proposition Cons: Time intensive

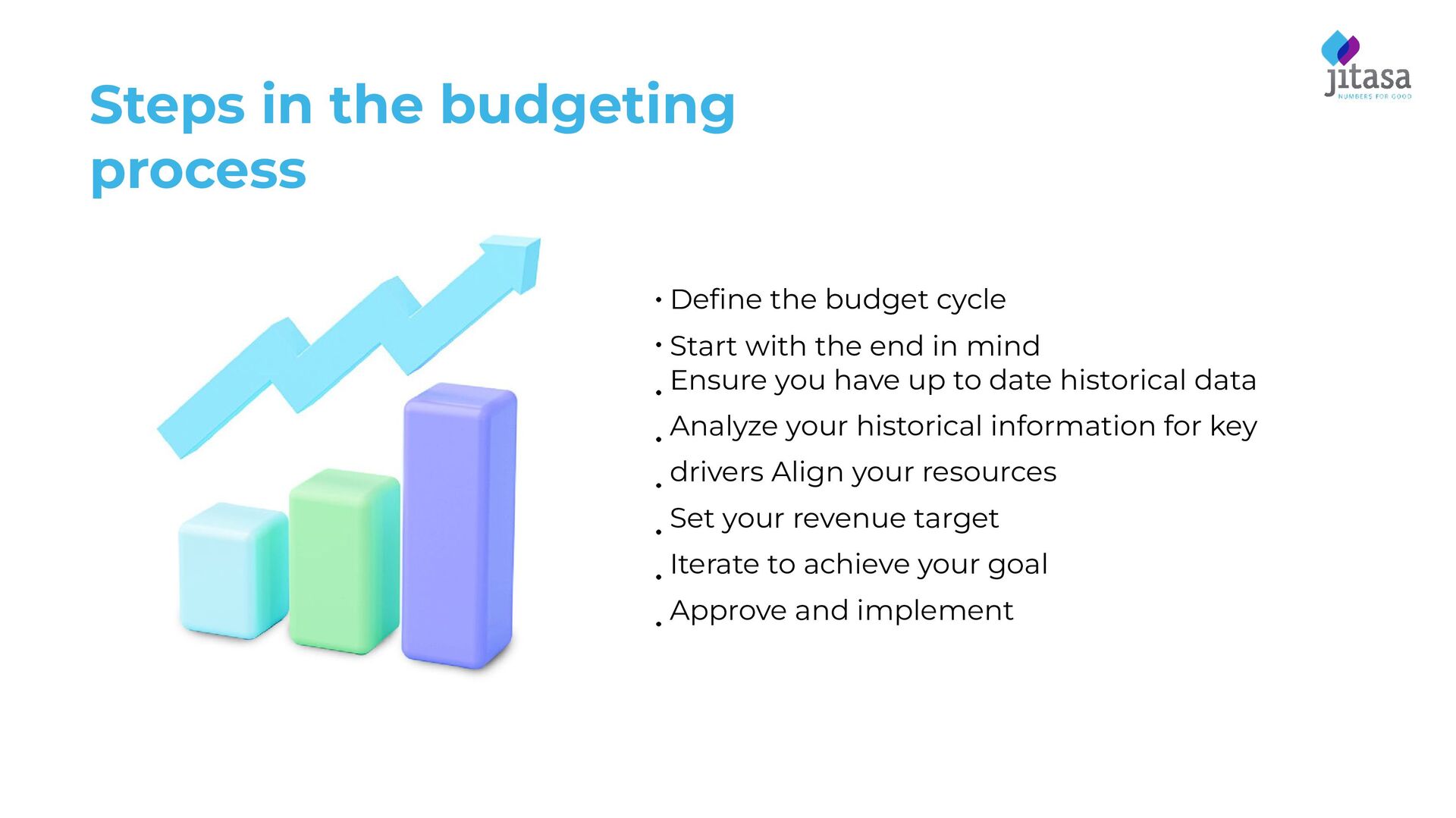

with the end in mind Ensure you have up to date historical data Analyze your historical information for key drivers Align your resources Set your revenue target Iterate to achieve your goal Approve and implement

key drivers and assumptions to be made in the budget What are we looking for? ▪ Understand common size ▪ Focus on materiality ▪ Relationships between financial items ▪ Revenue and expense impacts of new initiatives

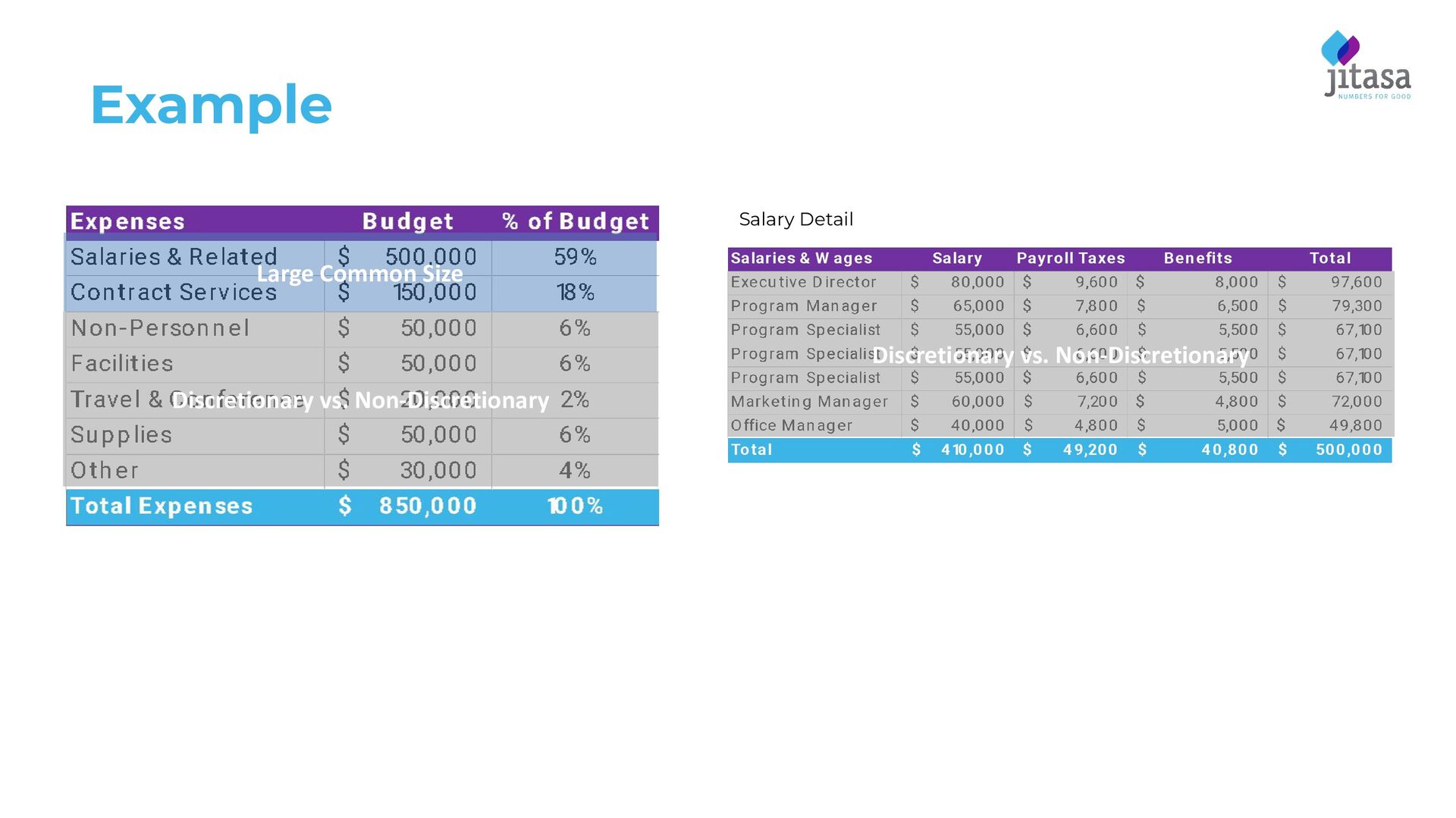

▪ Focus on common size and new initiatives ▪ Document assumptions ▪ Understand recurring vs. one time spend ▪ Identify Discretionary vs. non-discretionary spending ▪ “Nice to have” vs. “Must have”

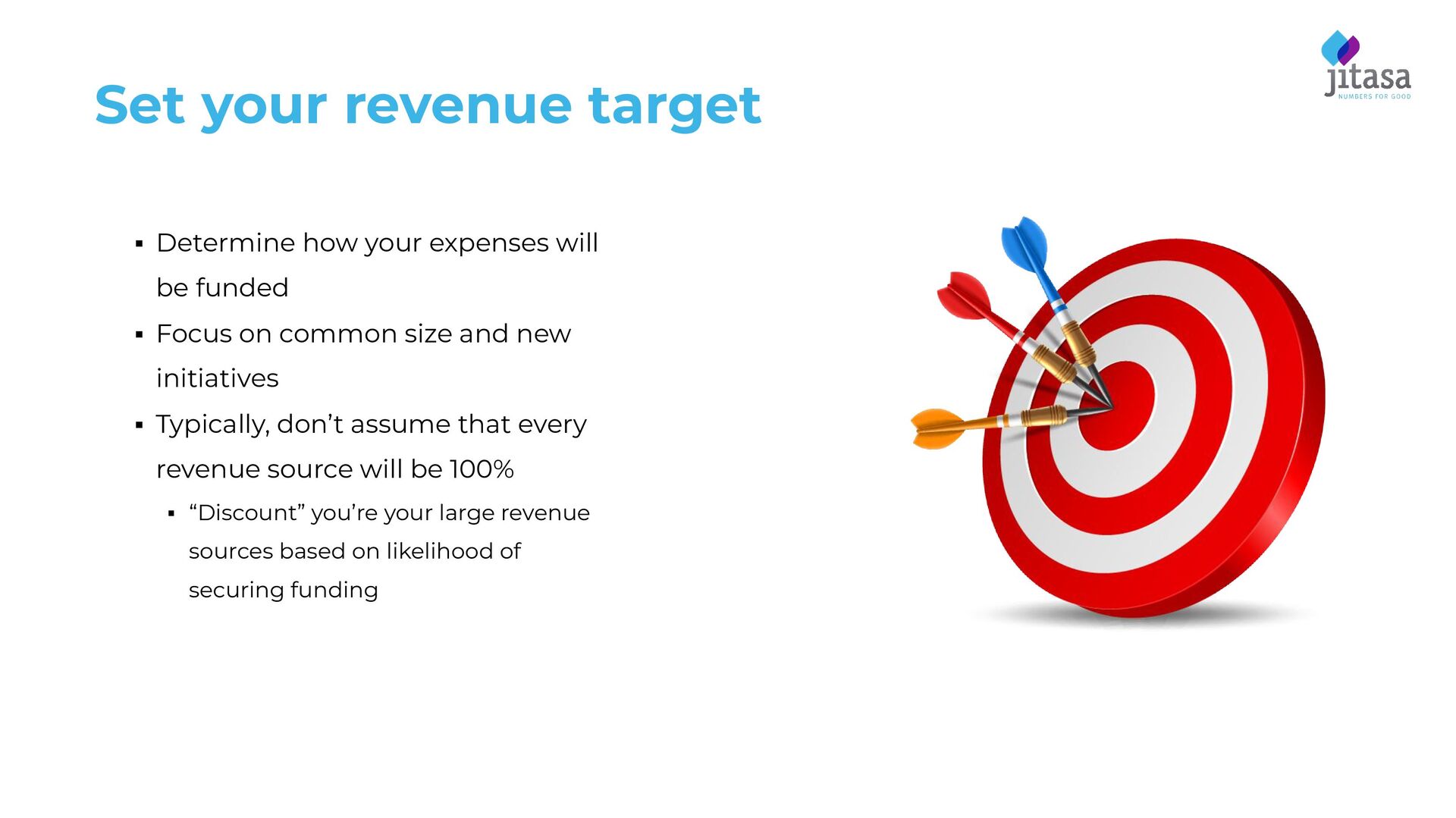

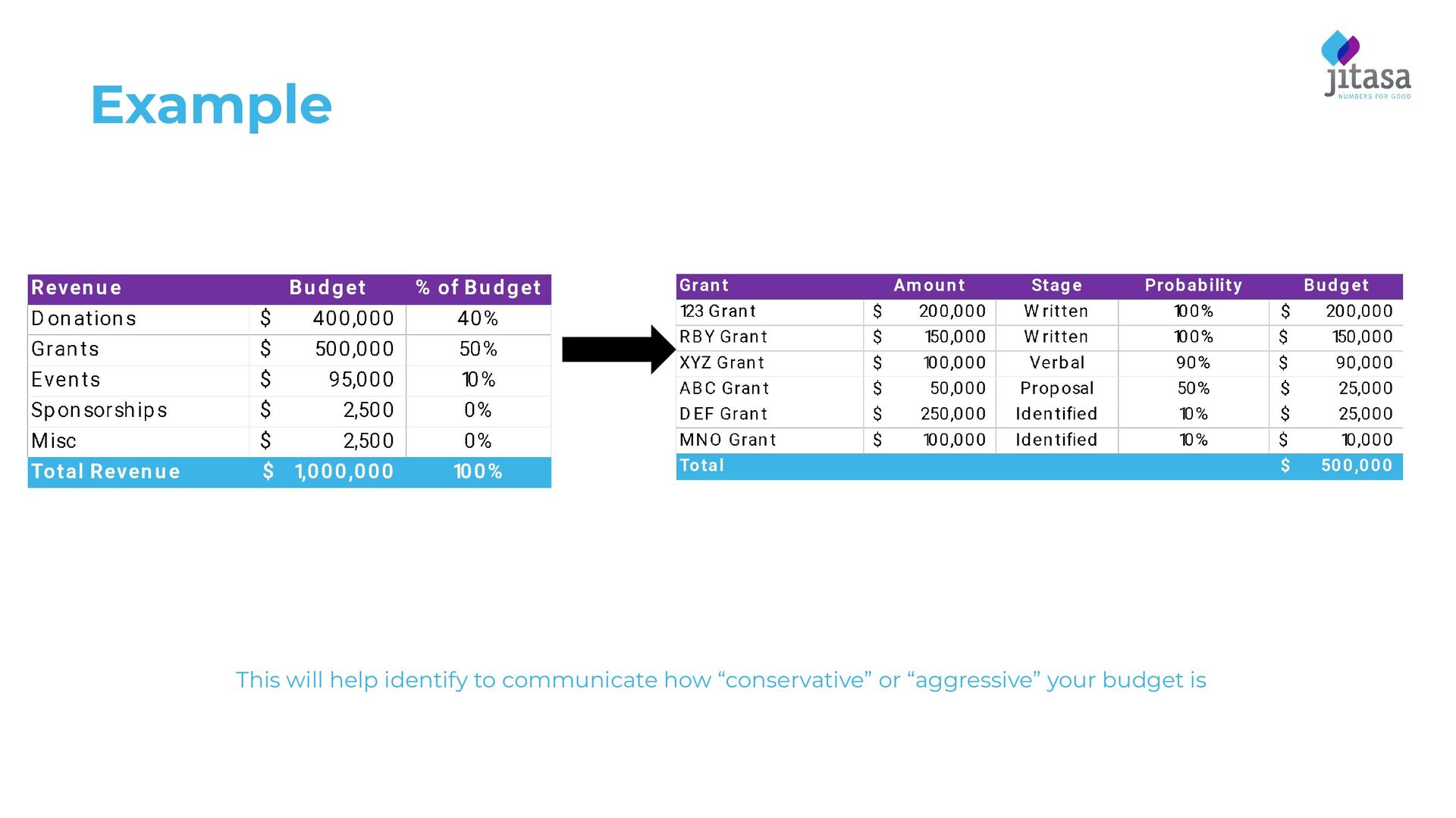

be funded ▪ Focus on common size and new initiatives ▪ Typically, don’t assume that every revenue source will be 100% ▪ “Discount” you’re your large revenue sources based on likelihood of securing funding

Identify risky and aggressive assumptions in the plan! ▪ At this stage, “reality” often sets in…it’s OK! ▪ Identify funding opportunities to close the gap ▪ Perhaps you have been “conservative” on your revenue estimates ▪ Identify areas of spending that may not be necessary ▪ Remember the identification of discretionary vs. non-discretionary items ▪ Use “if-then” sequencing

approval ▪ Once budget is approved: ▪ Enter into accounting system ▪ Re-communicate the approved budget to staff ▪ Do not change budget to make budget match the actuals

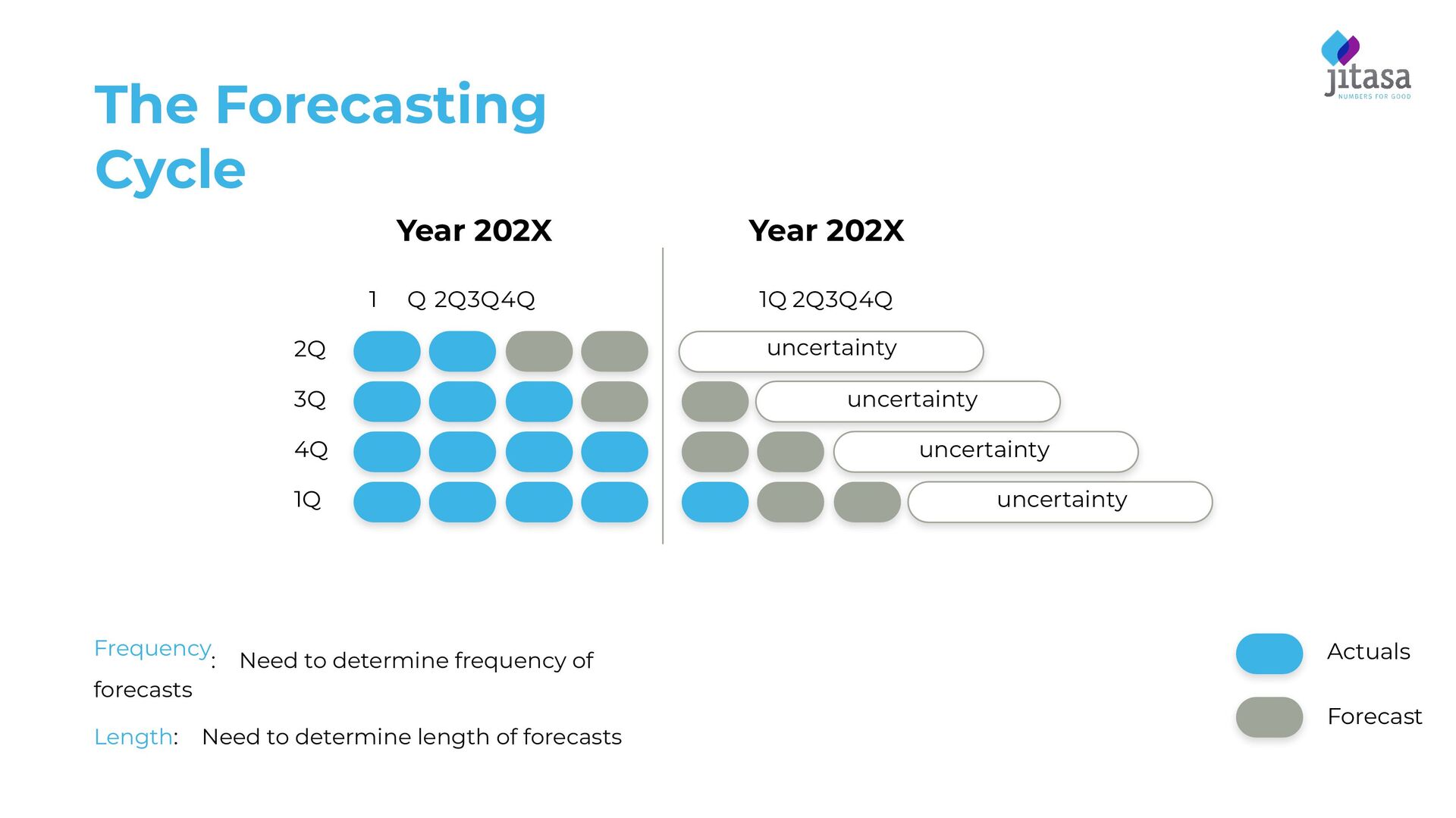

need to monitor our course and provide corrective action as needed ▪ Determine what we think will happen ▪ Analyze and compare to our budget ▪ Make corrective decisions as needed

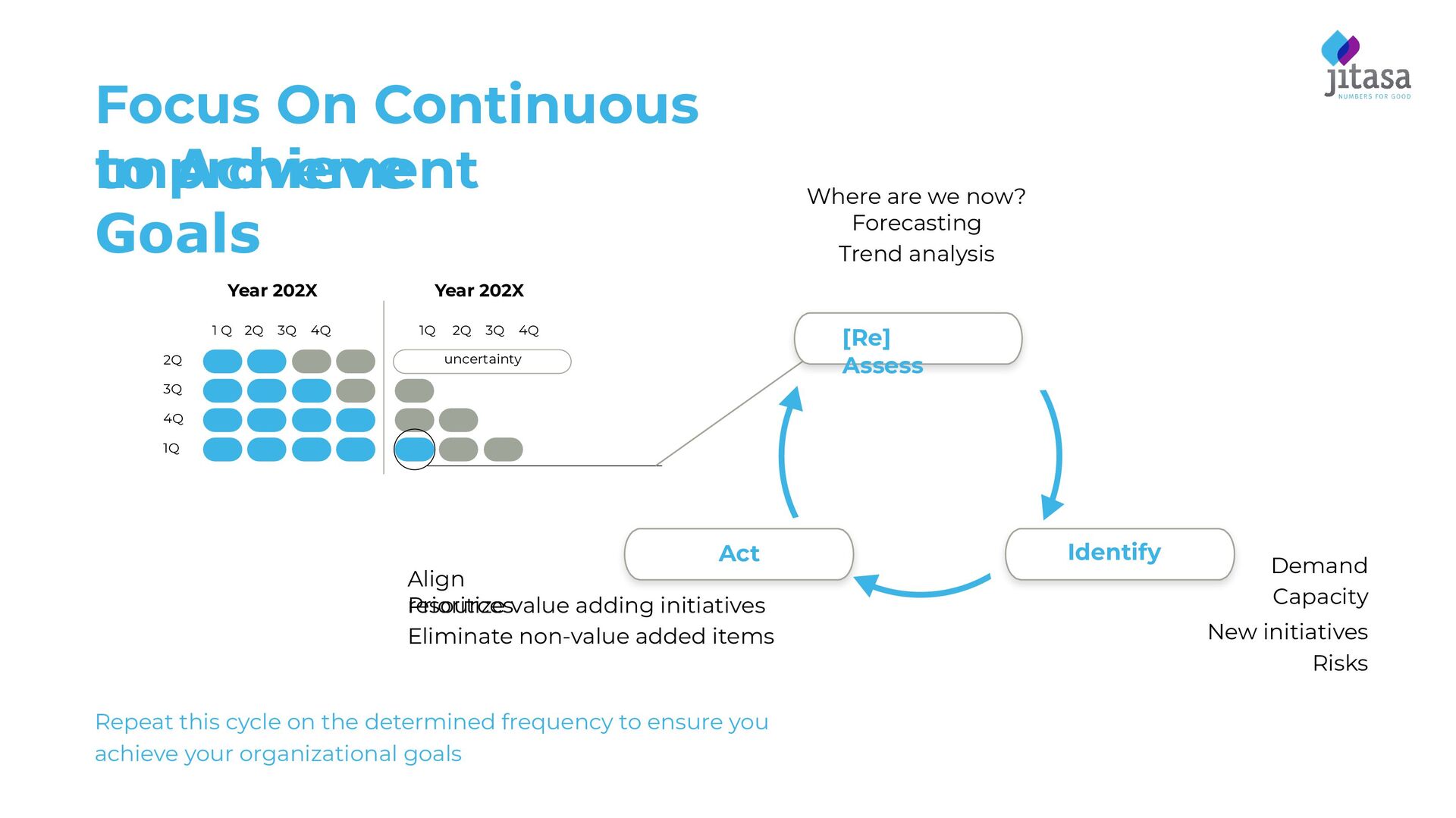

Q 2Q 3Q 4Q Year 202X 1Q 2Q 3Q 4Q uncertainty 2Q 3Q 4Q 1Q Where are we now? Forecasting Trend analysis Align resources Prioritize value adding initiatives Eliminate non-value added items Demand Capacity New initiatives Risks [Re] Assess Act Identify Repeat this cycle on the determined frequency to ensure you achieve your organizational goals

forecasts wisely Eliminate Focu s Pre-set allocation of resources encourages hoarding Is it in the budget? Be flexible as you allocate resources throughout the year Are there better uses of these funds?

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

![Q&A [email protected]](https://files.speakerdeck.com/presentations/1842590c4b4c4af6b279a5f5caa368bd/slide_27.jpg){kind=link}