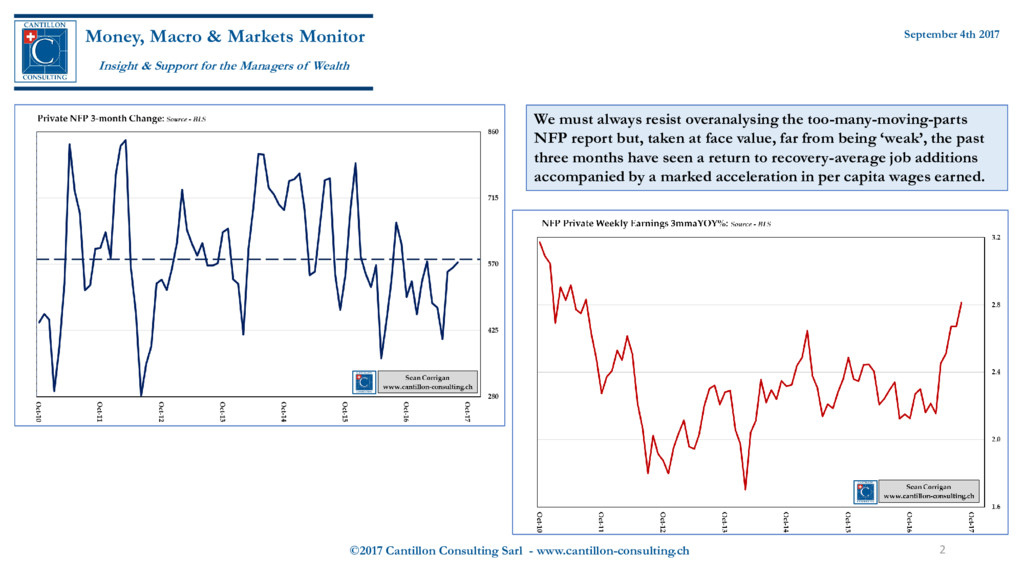

Many commentators saw Friday's payroll report as 'weak' but was that really the case? Yes, there are softer pockets of activity; yes, too, there are inconsistencies in the numbers. But there are also a number of pointers which suggest the ensuing fall in bond yields was not entirely justified.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}