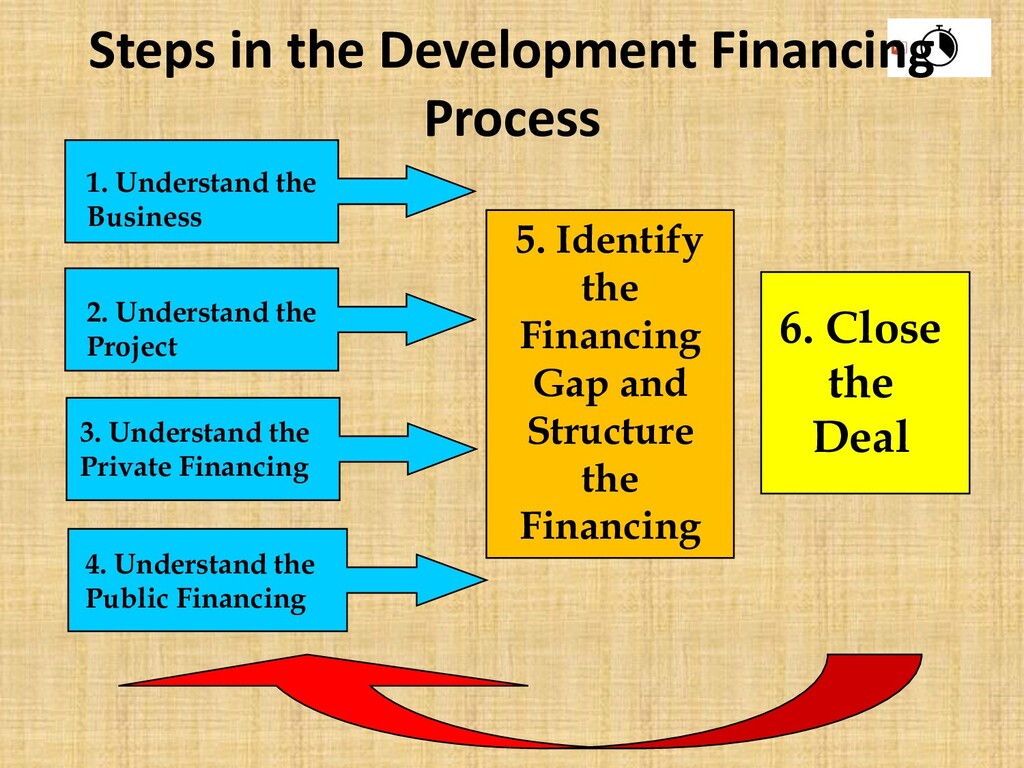

the Private Financing 4. Understand the Public Financing 6. Close the Deal 5. Identify the Financing Gap and Structure the Financing Steps in the Development Financing Process

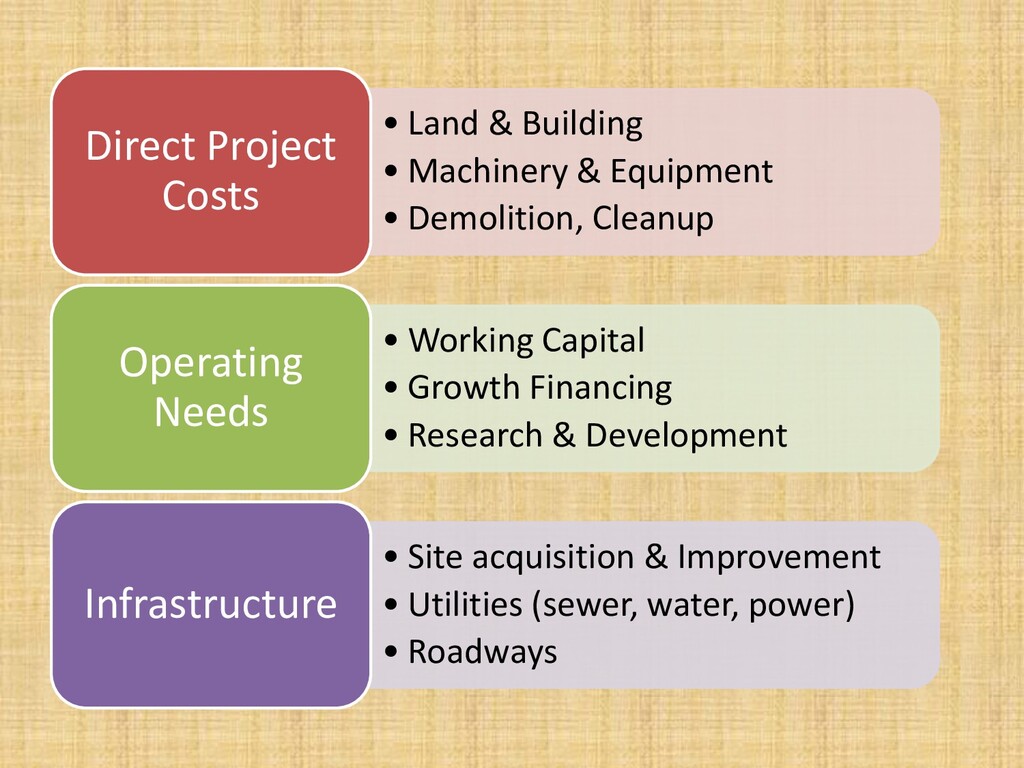

Cleanup Direct Project Costs • Working Capital • Growth Financing • Research & Development Operating Needs • Site acquisition & Improvement • Utilities (sewer, water, power) • Roadways Infrastructure

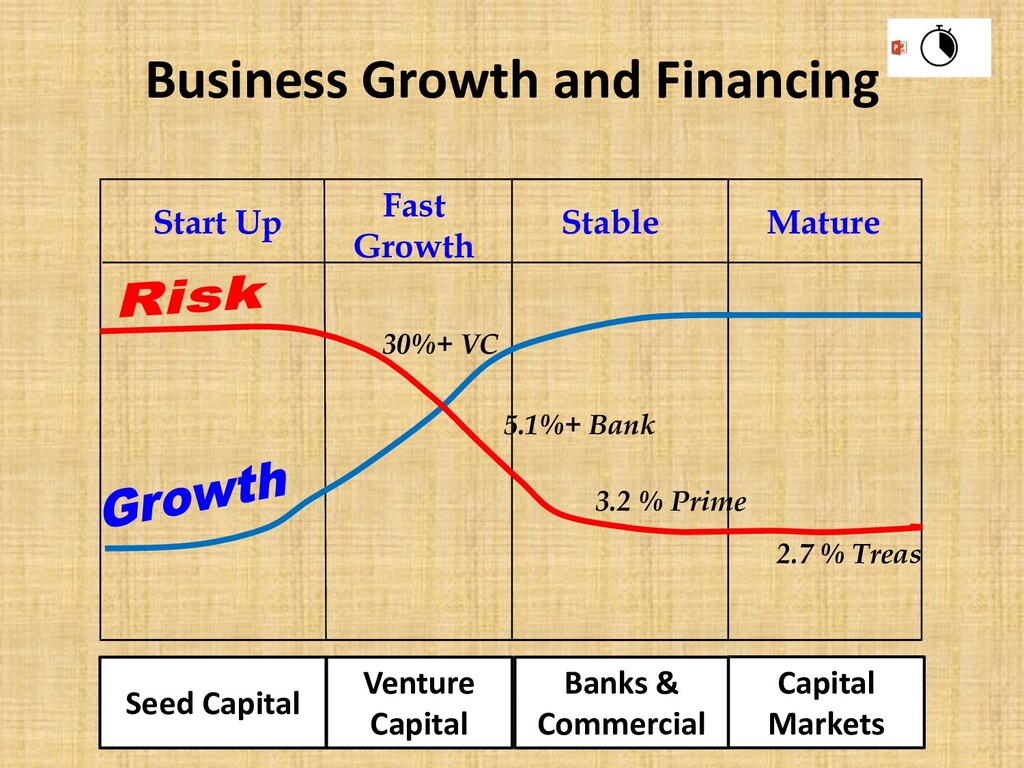

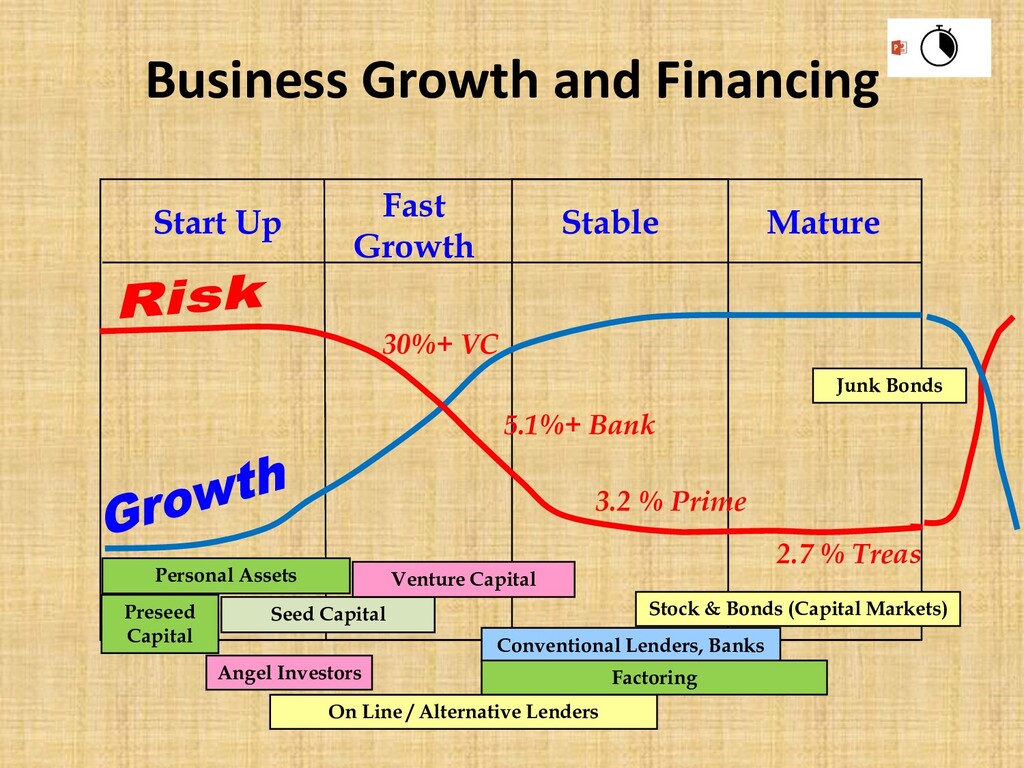

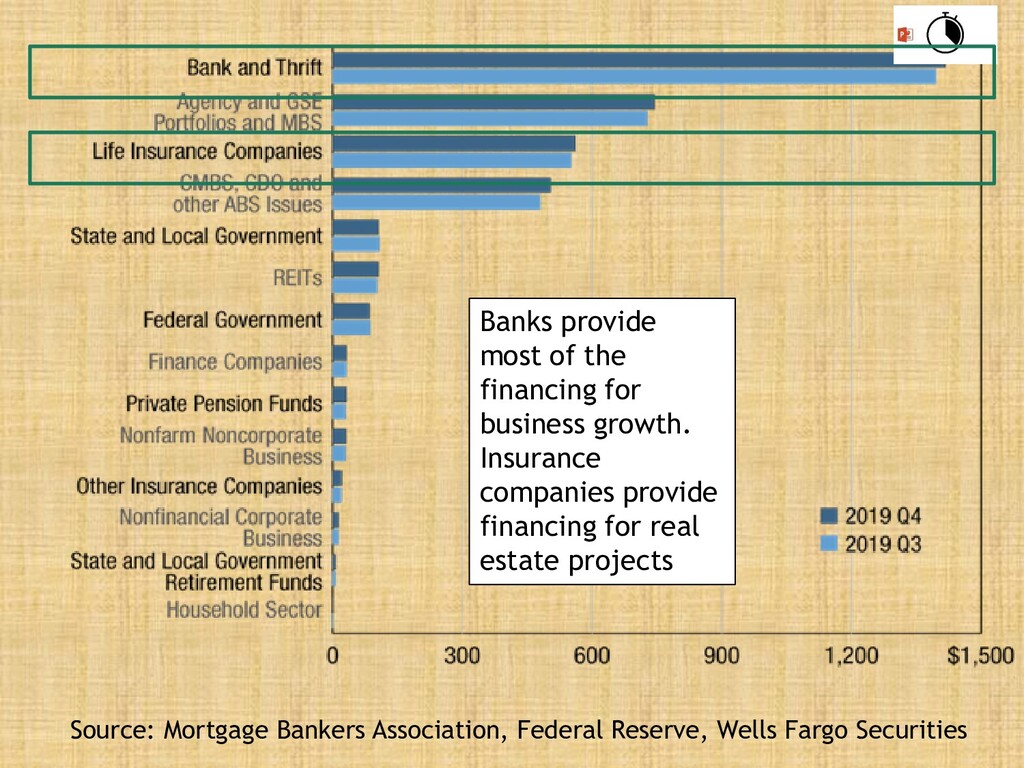

3.2 % Prime 2.7 % Treas Personal Assets Preseed Capital Seed Capital Venture Capital Angel Investors Conventional Lenders, Banks Stock & Bonds (Capital Markets) On Line / Alternative Lenders Factoring Junk Bonds Business Growth and Financing

managers – nothing more and nothing less -- with different goals for return on investment based upon their source of funding, profitability, and management goals. Private sector investors and lenders have no obligation to look at your project.

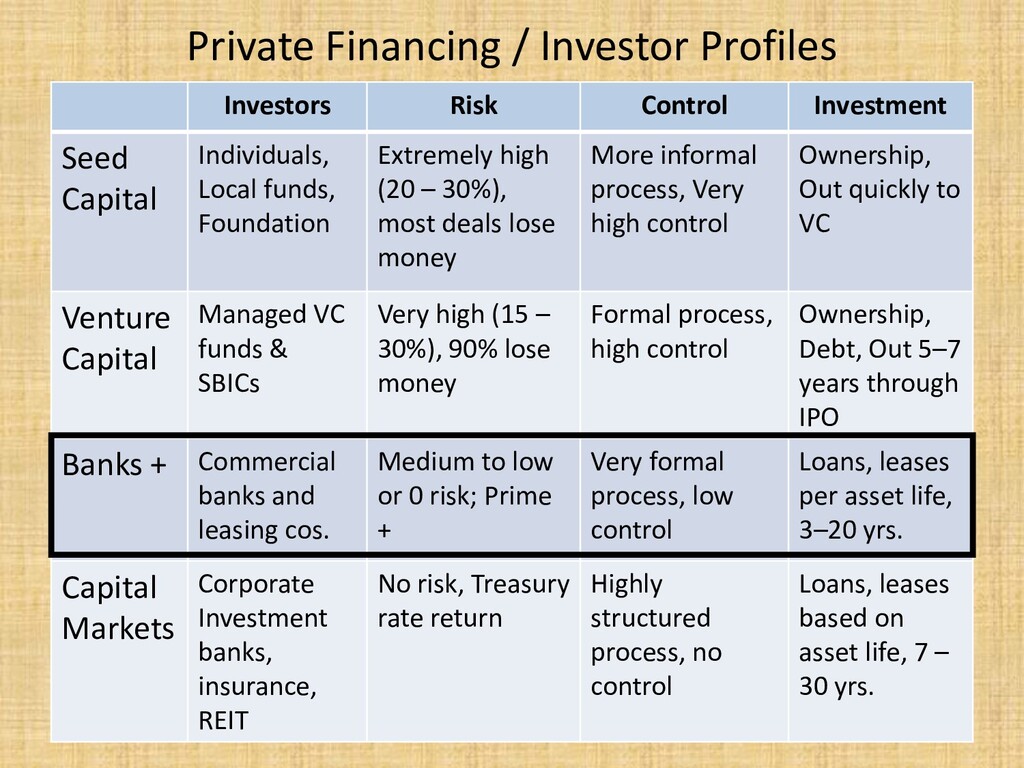

Capital Individuals, Local funds, Foundation Extremely high (20 – 30%), most deals lose money More informal process, Very high control Ownership, Out quickly to VC Venture Capital Managed VC funds & SBICs Very high (15 – 30%), 90% lose money Formal process, high control Ownership, Debt, Out 5–7 years through IPO Banks + Commercial banks and leasing cos. Medium to low or 0 risk; Prime + Very formal process, low control Loans, leases per asset life, 3–20 yrs. Capital Markets Corporate Investment banks, insurance, REIT No risk, Treasury rate return Highly structured process, no control Loans, leases based on asset life, 7 – 30 yrs.

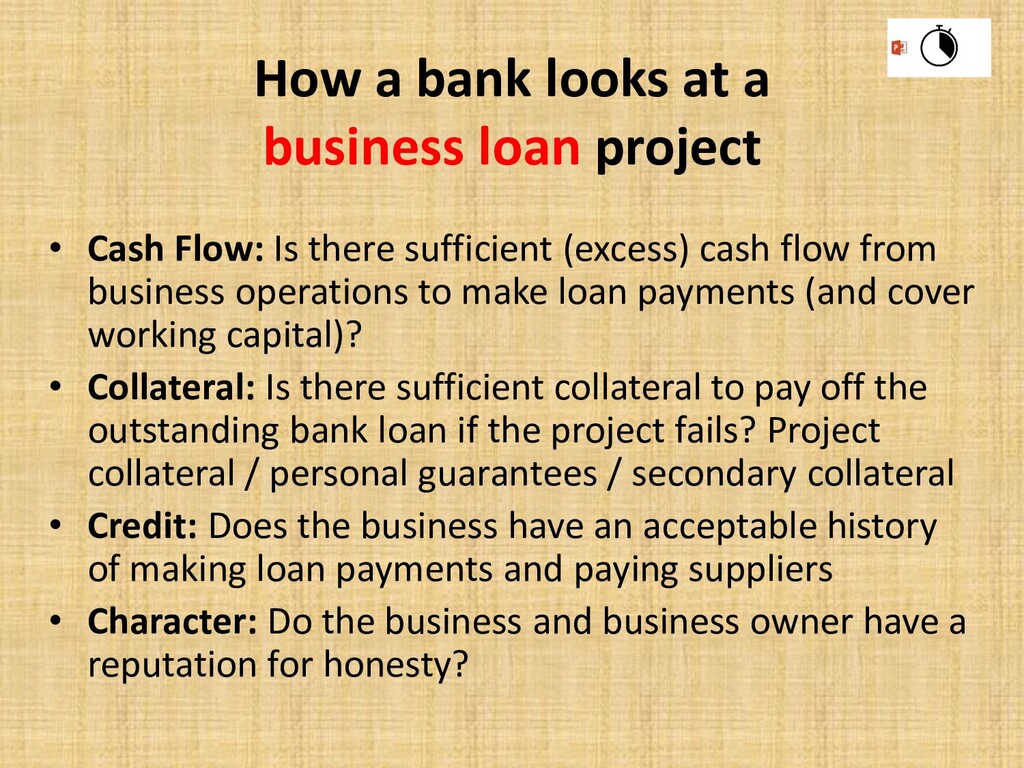

Cash Flow: Is there sufficient (excess) cash flow from business operations to make loan payments (and cover working capital)? • Collateral: Is there sufficient collateral to pay off the outstanding bank loan if the project fails? Project collateral / personal guarantees / secondary collateral • Credit: Does the business have an acceptable history of making loan payments and paying suppliers • Character: Do the business and business owner have a reputation for honesty?

supply chain and customer base. Some banks have preferred industries Amount of Loan: Lower loan amounts for riskier businesses; Concern about “single purpose” collateral or environmental contamination. Concerned about special purpose equipment; Value ≠ Cost Use of Funds: Real Estate acquisition, renovation or new construction; Equipment, Working Capital, Growth, Infrastructure, Site Development Interest Rate: Priced off prime rate; Prime + based on bank profits, risk; Higher interest rates for higher risk businesses or projects Fixed or Variable: Prefer variable rate financing; Fixed rate financing based upon additional guarantees, strength of business or assets Term of Loan: Term based on asset life; Real Estate: 10 years; Equipment: 7 years; Longer Amortization (ie: 10/20) Equity: Generally minimum equity towards project of 25%; Higher equity requirement based on collateral value, business risk, Lower equity if additional collateral pledged Collateral: First lien or mortgage position; Personal guarantees; “abundance of caution” collateral 16

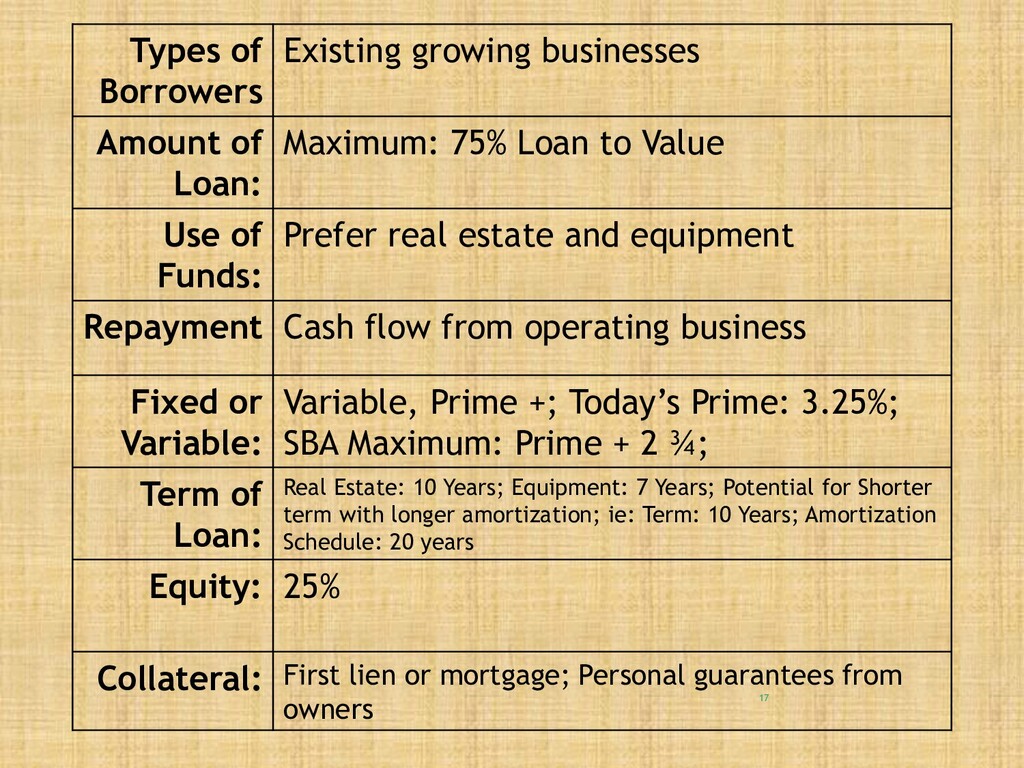

75% Loan to Value Use of Funds: Prefer real estate and equipment Repayment Cash flow from operating business Fixed or Variable: Variable, Prime +; Today’s Prime: 3.25%; SBA Maximum: Prime + 2 ¾; Term of Loan: Real Estate: 10 Years; Equipment: 7 Years; Potential for Shorter term with longer amortization; ie: Term: 10 Years; Amortization Schedule: 20 years Equity: 25% Collateral: First lien or mortgage; Personal guarantees from owners 17

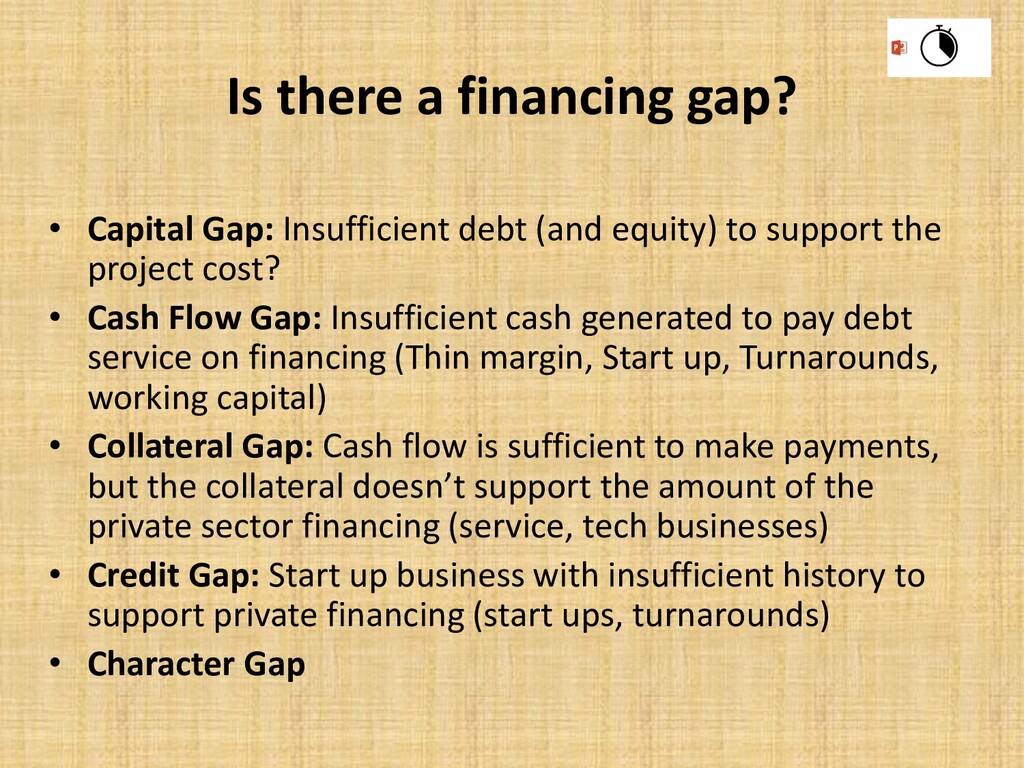

(and equity) to support the project cost? • Cash Flow Gap: Insufficient cash generated to pay debt service on financing (Thin margin, Start up, Turnarounds, working capital) • Collateral Gap: Cash flow is sufficient to make payments, but the collateral doesn’t support the amount of the private sector financing (service, tech businesses) • Credit Gap: Start up business with insufficient history to support private financing (start ups, turnarounds) • Character Gap

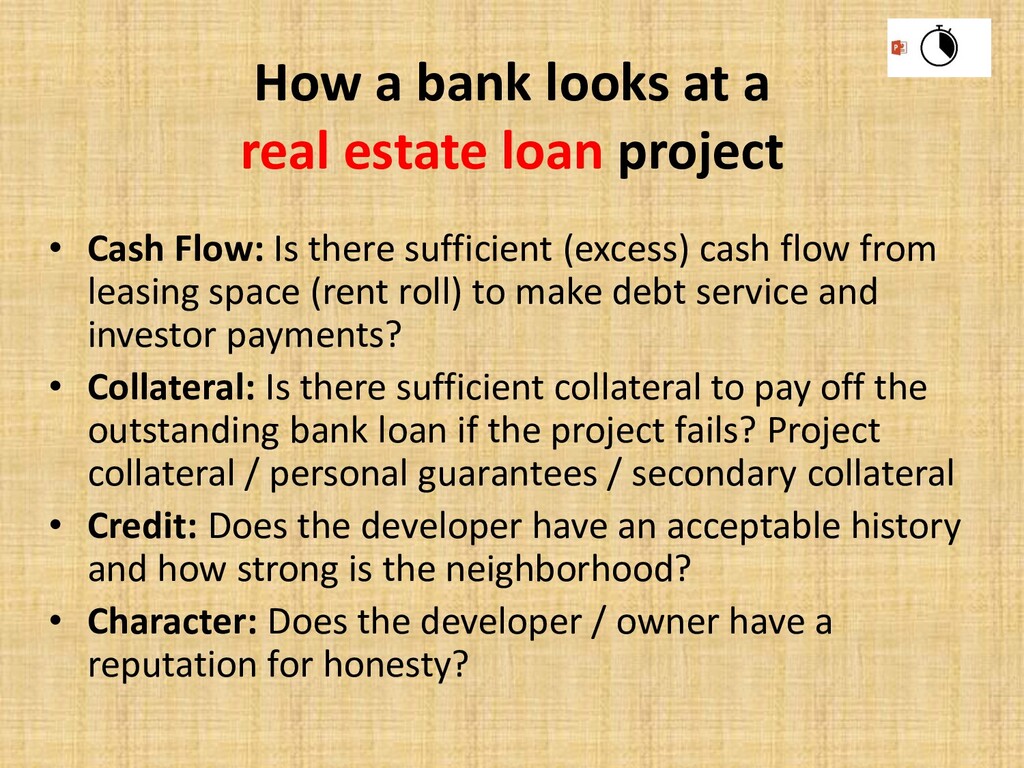

• Cash Flow: Is there sufficient (excess) cash flow from leasing space (rent roll) to make debt service and investor payments? • Collateral: Is there sufficient collateral to pay off the outstanding bank loan if the project fails? Project collateral / personal guarantees / secondary collateral • Credit: Does the developer have an acceptable history and how strong is the neighborhood? • Character: Does the developer / owner have a reputation for honesty?

Real estate projects tend to be for investments purposes. Business projects tend to provide assets for operating a business. • An investor’s Return on Investment is a critical part of real estate financing. • Repayment on real estate projects comes from leasing cash flow. Repayment for business loans comes from operating profits. • Collateral / Security: Real estate loans tend to be non- resource loans to a developer (no personal guarantee). Most business loans require a personal guarantee. • Real estate financing tends to start with construction financing which is “taken out” with permanent financing on stabilization. Business financing will use interim financing to acquire assets, followed by a term loan.

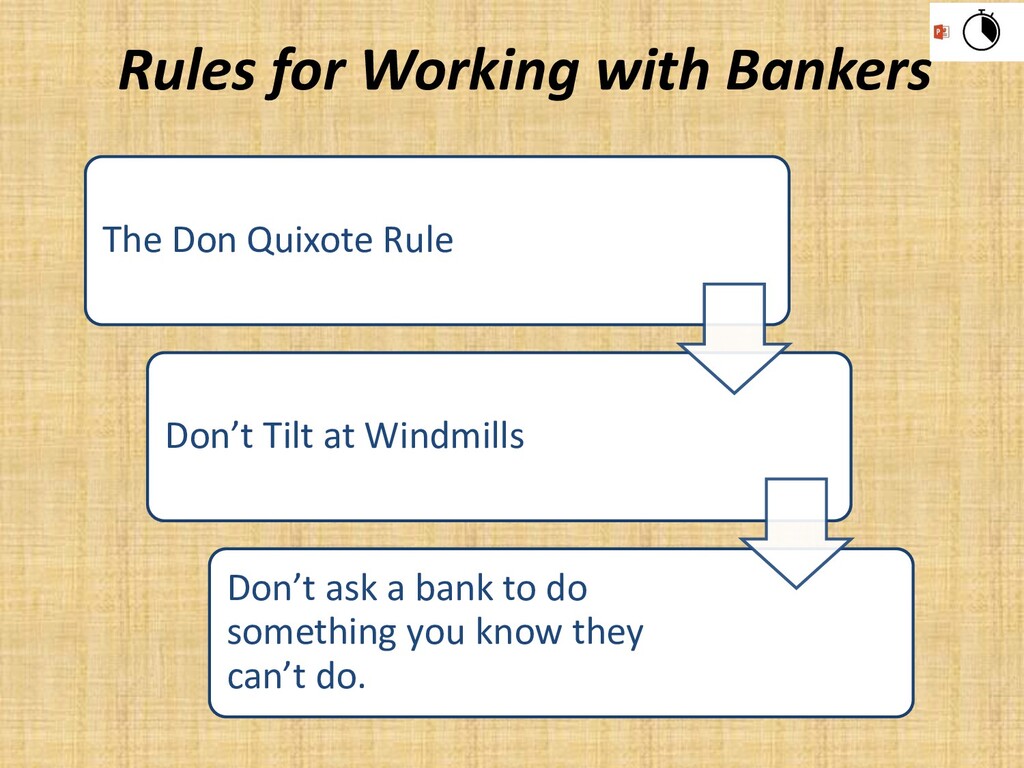

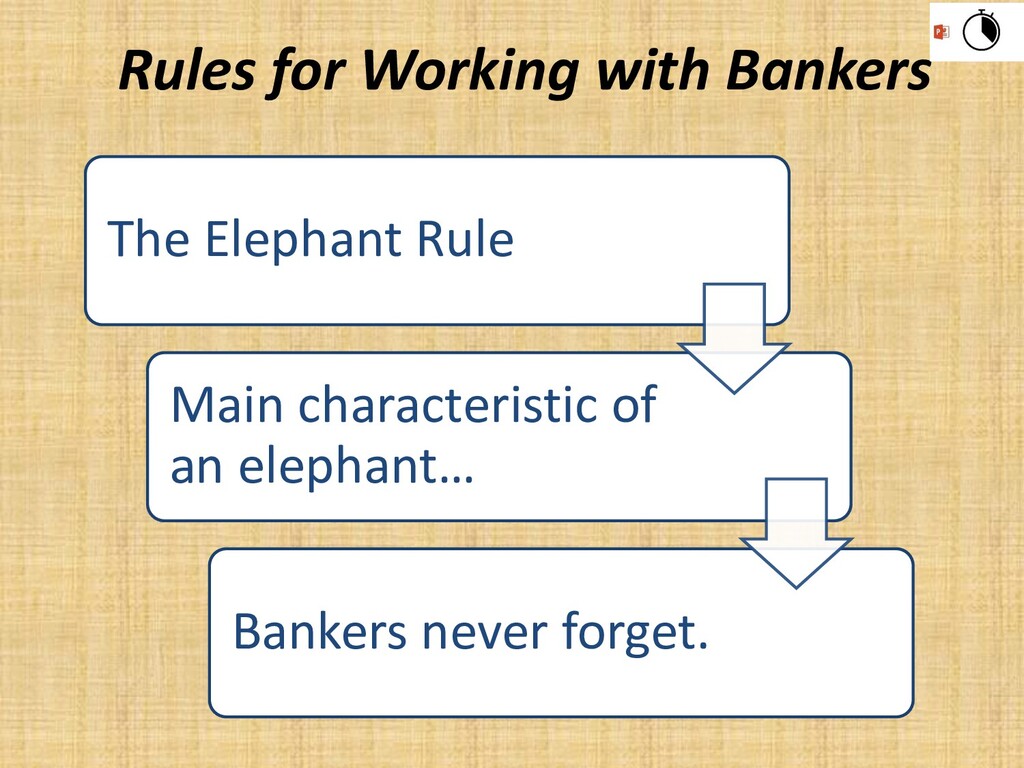

George Steinbrenner Rule The Berlitz Rule The Al Capone’s Safe Rule The Herb Cohen Rule The Robert Baden-Powell Rule The Henry S. Potter Rule The Don Quixote Rule The Elephant Rule

Job creation, job retention, place-based development, equity, other social goals • Reduce cash flow needs of business to preserve cash for working capital or growth capital • Fill capital gaps in the face of non-bankable projects • Encourage banks to lend in the face of financing gaps

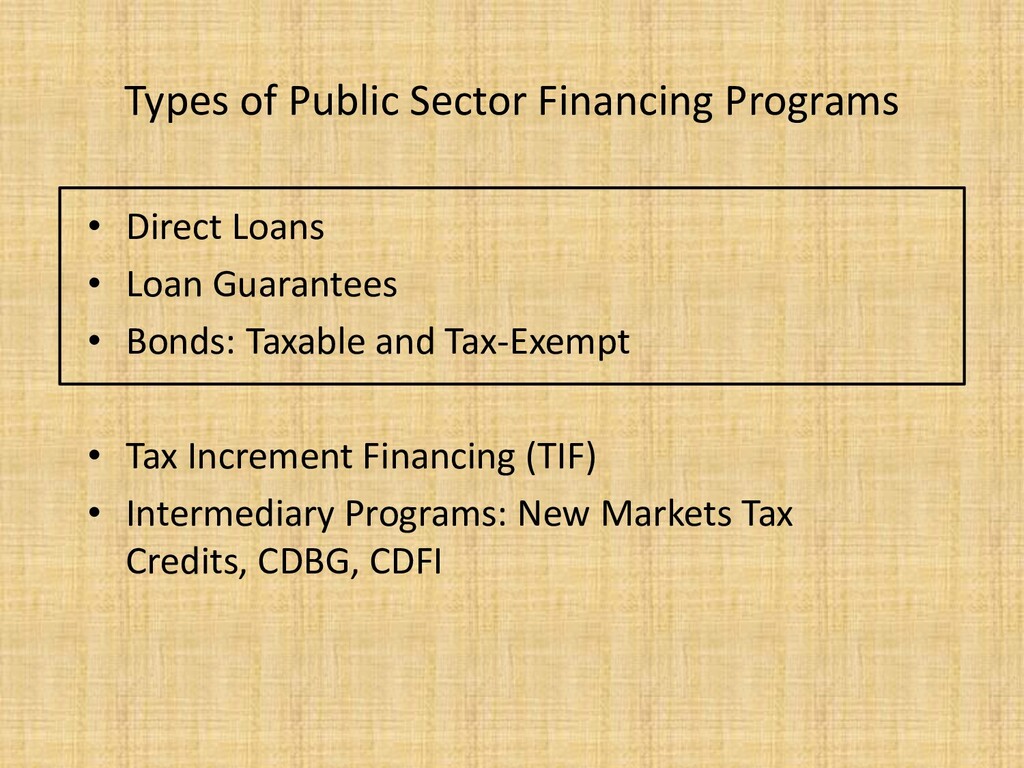

SBA 504 Direct Loan SBA 7A Loan Guarantee USDA B & I Collateral Enhancement / Capital Access This chart does not include COVID related stimulus financing Revolving Loan Funds

Loan Guarantees – Guarantee riskier credits or lower value collateral – Increase borrowing capacity – Does not necessarily get lower rate or longer term • Direct Loans – Lower down payment financing to preserve cash for working capital – Long Term Financing to stretch out payments – Fixed Rate Financing to provide predictable cash flow – Lower rate financing to reduce the cost of borrowing – Increased Borrowing Capacity – Fill Capital Gap between Debt, Equity & Project Cost • Bonds: – Bring lower rate and long-term financing through capital market bond financing (tax exempt or taxable)

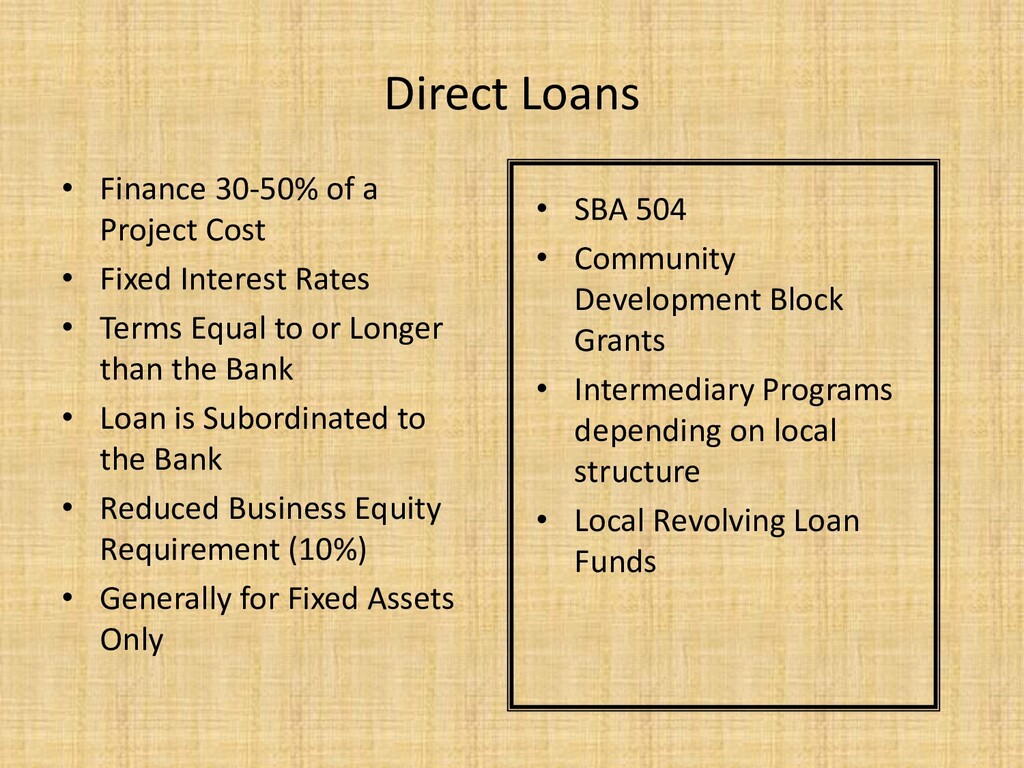

Fixed Interest Rates • Terms Equal to or Longer than the Bank • Loan is Subordinated to the Bank • Reduced Business Equity Requirement (10%) • Generally for Fixed Assets Only • SBA 504 • Community Development Block Grants • Intermediary Programs depending on local structure • Local Revolving Loan Funds

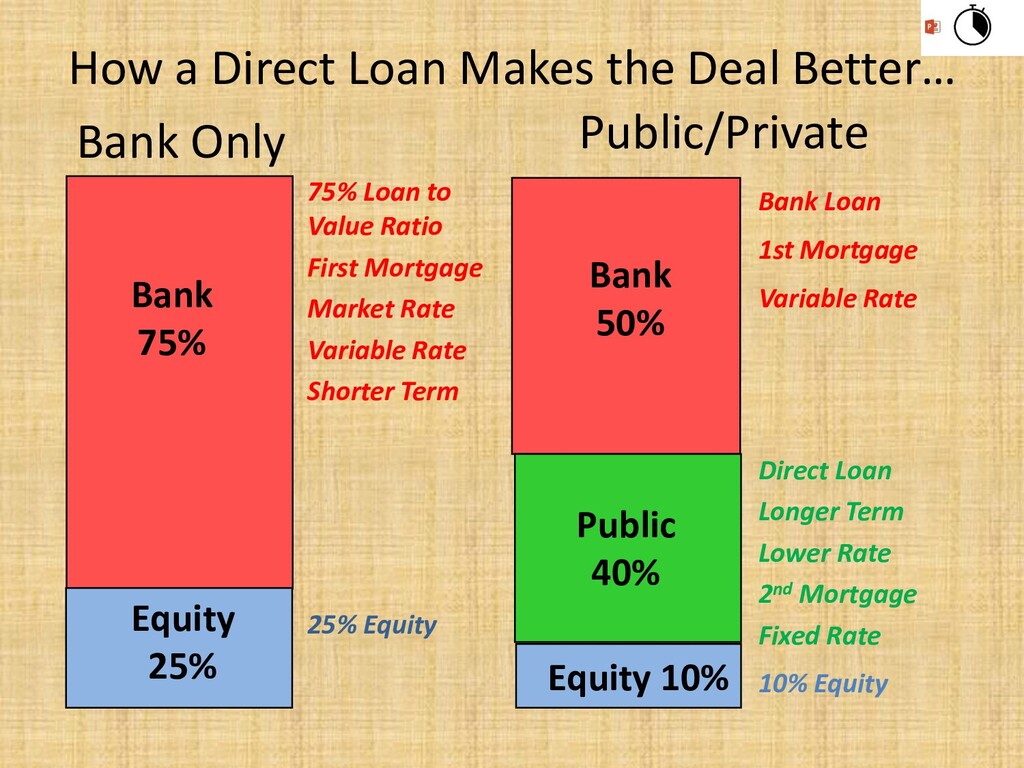

Equity 25% Bank 50% Equity 10% Public 40% Bank Only Public/Private 75% Loan to Value Ratio First Mortgage Market Rate Variable Rate Shorter Term 25% Equity Bank Loan 1st Mortgage Variable Rate Direct Loan Longer Term Lower Rate 2nd Mortgage Fixed Rate 10% Equity

and Term • Guaranty up to 85% of Bank Loan • Can Finance Working Capital • Alternative: Provide secured deposit • SBA 7(a) • SBA Community Advantage • Collateral Assistance Program • USDA Business and Industry Loan Program

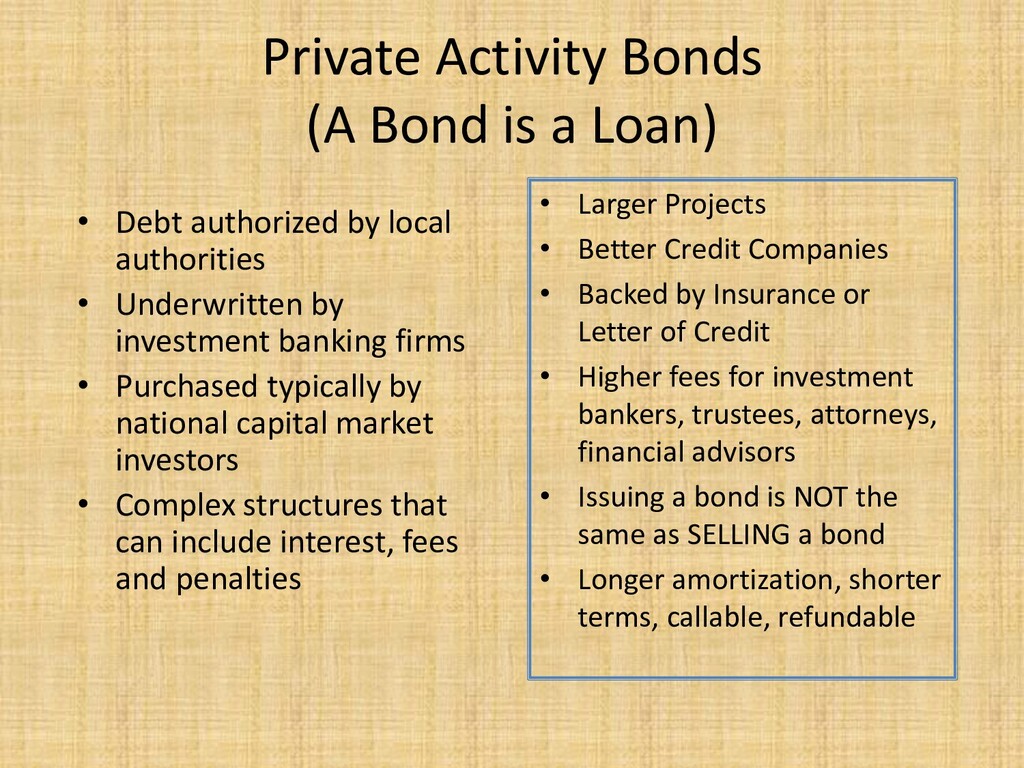

authorized by local authorities • Underwritten by investment banking firms • Purchased typically by national capital market investors • Complex structures that can include interest, fees and penalties • Larger Projects • Better Credit Companies • Backed by Insurance or Letter of Credit • Higher fees for investment bankers, trustees, attorneys, financial advisors • Issuing a bond is NOT the same as SELLING a bond • Longer amortization, shorter terms, callable, refundable

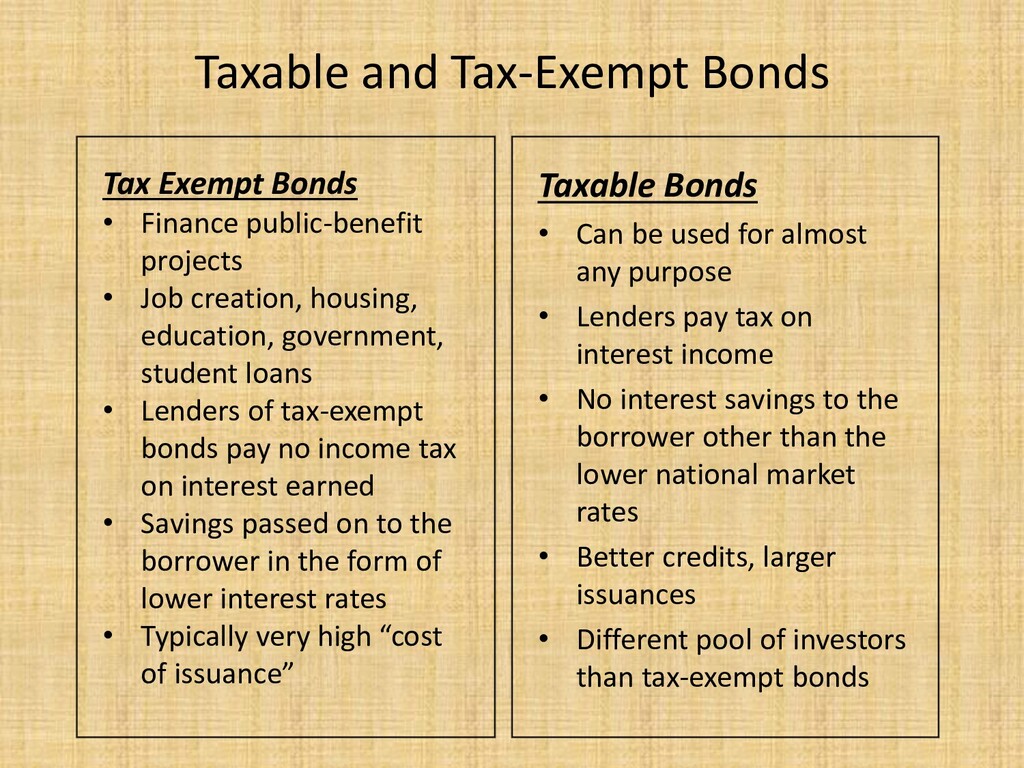

for almost any purpose • Lenders pay tax on interest income • No interest savings to the borrower other than the lower national market rates • Better credits, larger issuances • Different pool of investors than tax-exempt bonds Tax Exempt Bonds • Finance public-benefit projects • Job creation, housing, education, government, student loans • Lenders of tax-exempt bonds pay no income tax on interest earned • Savings passed on to the borrower in the form of lower interest rates • Typically very high “cost of issuance”

to local economic development for relending • Local group takes responsibility for policy, underwriting, marketing, processing and management of funds • Local group assumes responsibility for funds management and repayment of funds to the government, if a loan • EB 5 Financing • SBA 504 • SBA Microloan • CDBG • New Markets Tax Credits • Community Development Financial Institutions • USDA Intermediary Relending • SBA Intermediary Program

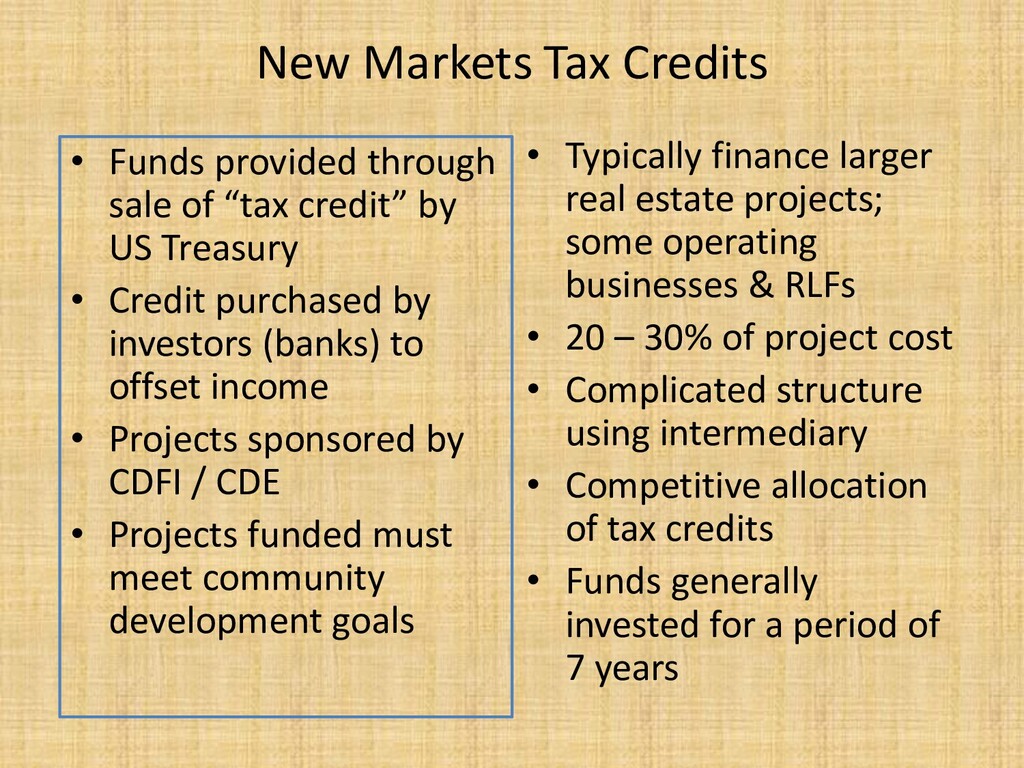

“tax credit” by US Treasury • Credit purchased by investors (banks) to offset income • Projects sponsored by CDFI / CDE • Projects funded must meet community development goals • Typically finance larger real estate projects; some operating businesses & RLFs • 20 – 30% of project cost • Complicated structure using intermediary • Competitive allocation of tax credits • Funds generally invested for a period of 7 years

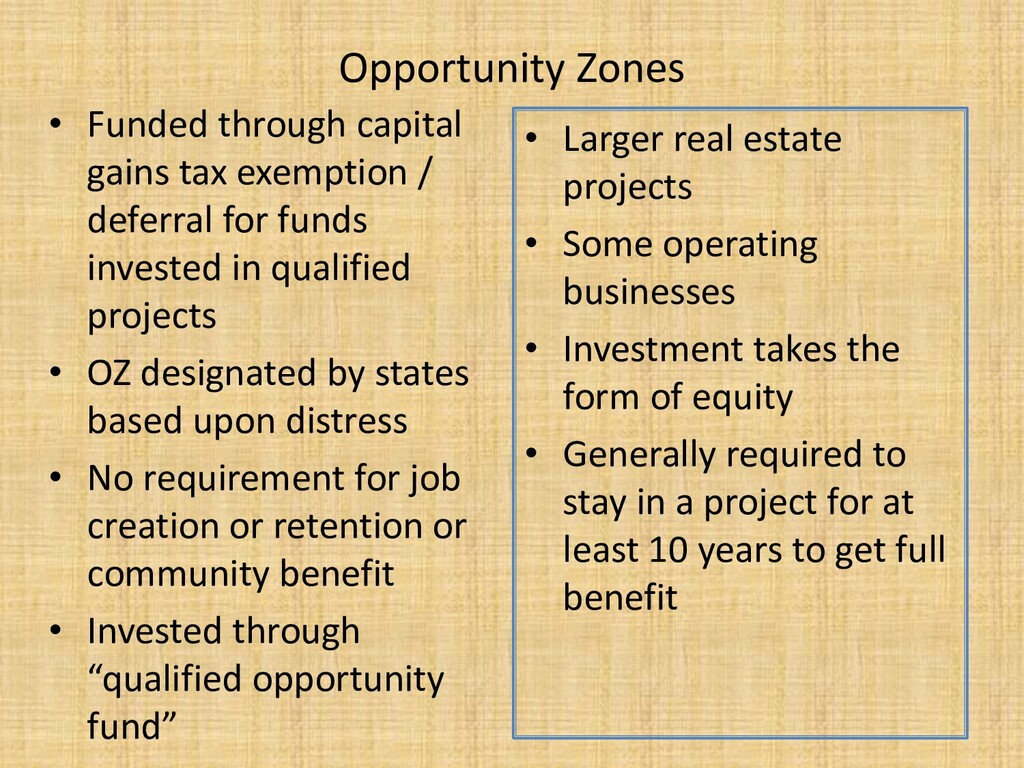

deferral for funds invested in qualified projects • OZ designated by states based upon distress • No requirement for job creation or retention or community benefit • Invested through “qualified opportunity fund” • Larger real estate projects • Some operating businesses • Investment takes the form of equity • Generally required to stay in a project for at least 10 years to get full benefit

development into a fund to pay for infrastructure • Up to 75% of Property taxes primarily, state gross receipts tax • Funds can be used directly to pay for costs or to pay debt service on bonds to finance infrastructure • Requires spending plan • Generally 25-year term • Biggest Challenge: Interim financing needed

SBA – Main Street – CDBG – Economic Development Administration • Local – Stimulus vs. Lending – Pay for expenses – Must reemploy – Expand CDBG RLFs – Expand EDA RLFs

financials and tax returns? ✓Do they expect “free money”? ✓Is their answer always “It’s someone else’s job” ✓Is their answer always “it’s someone else's problem?” ✓Are they willing to spend more money to help make the deal happen?

tell their story … once 2. Get to know the program people; Let the program people represent their program 3. Explain the strings up front 4. Don’t pile on programs 5. Be prepared to do the paperwork 6. It ALWAYS takes longer 7. Underwrite like a bank … but don’t act like a bank 8. …

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

![Mark Barbash Ohio Economic Development Institute (614) 774-7599 www.linkedin.com/in/markbarbash [email protected]](https://files.speakerdeck.com/presentations/9e81affcde8743788769e000df0808ca/slide_51.jpg){kind=link}