The global Edge Computing Market is experiencing rapid advancement, driven by the growing need for real-time data processing closer to the data source. In 2023, the market was valued at USD 47 billion, and it is projected to reach nearly USD 206 billion by 2032, expanding at a strong CAGR of 18.3% throughout the forecast period. As organizations increasingly deploy connected devices and adopt latency-sensitive applications, edge computing has become a critical enabler of operational efficiency, data sovereignty, and reduced network dependency.

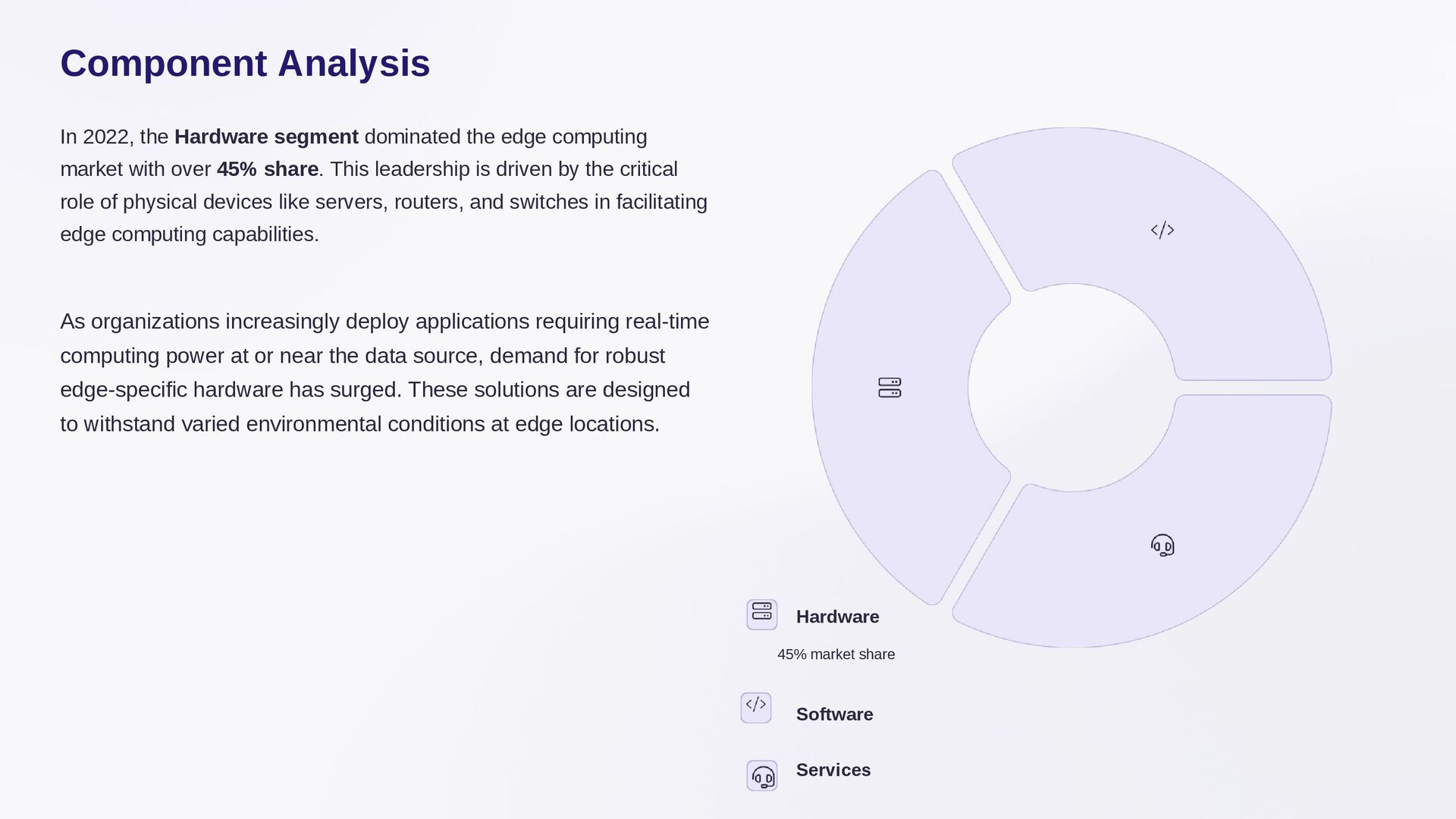

In 2022, the Hardware segment held a dominant position, capturing over 45% of the market share. The demand for specialized edge infrastructure - including edge servers, gateways, and routers - was essential for supporting data-heavy applications in low-latency environments.

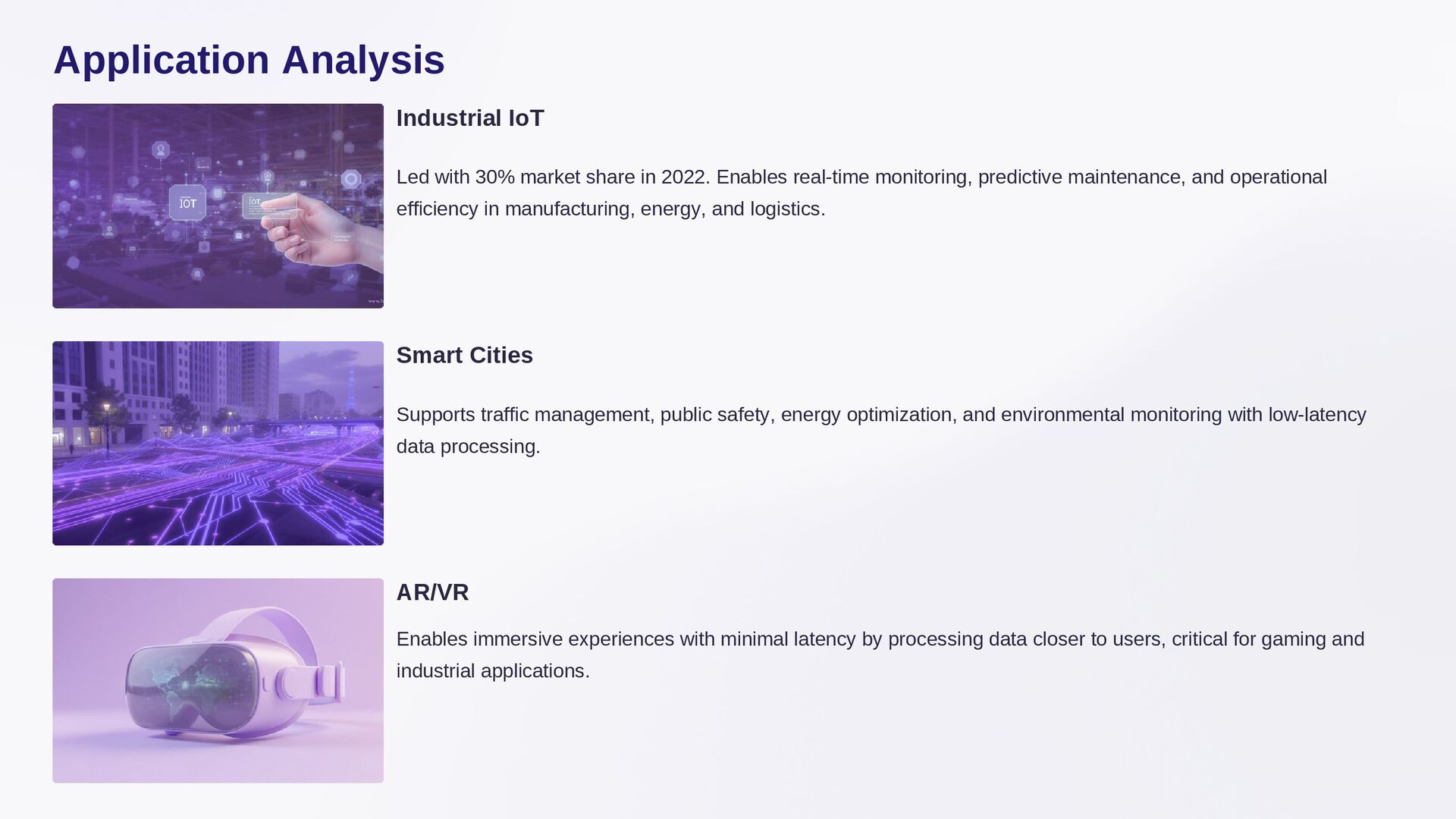

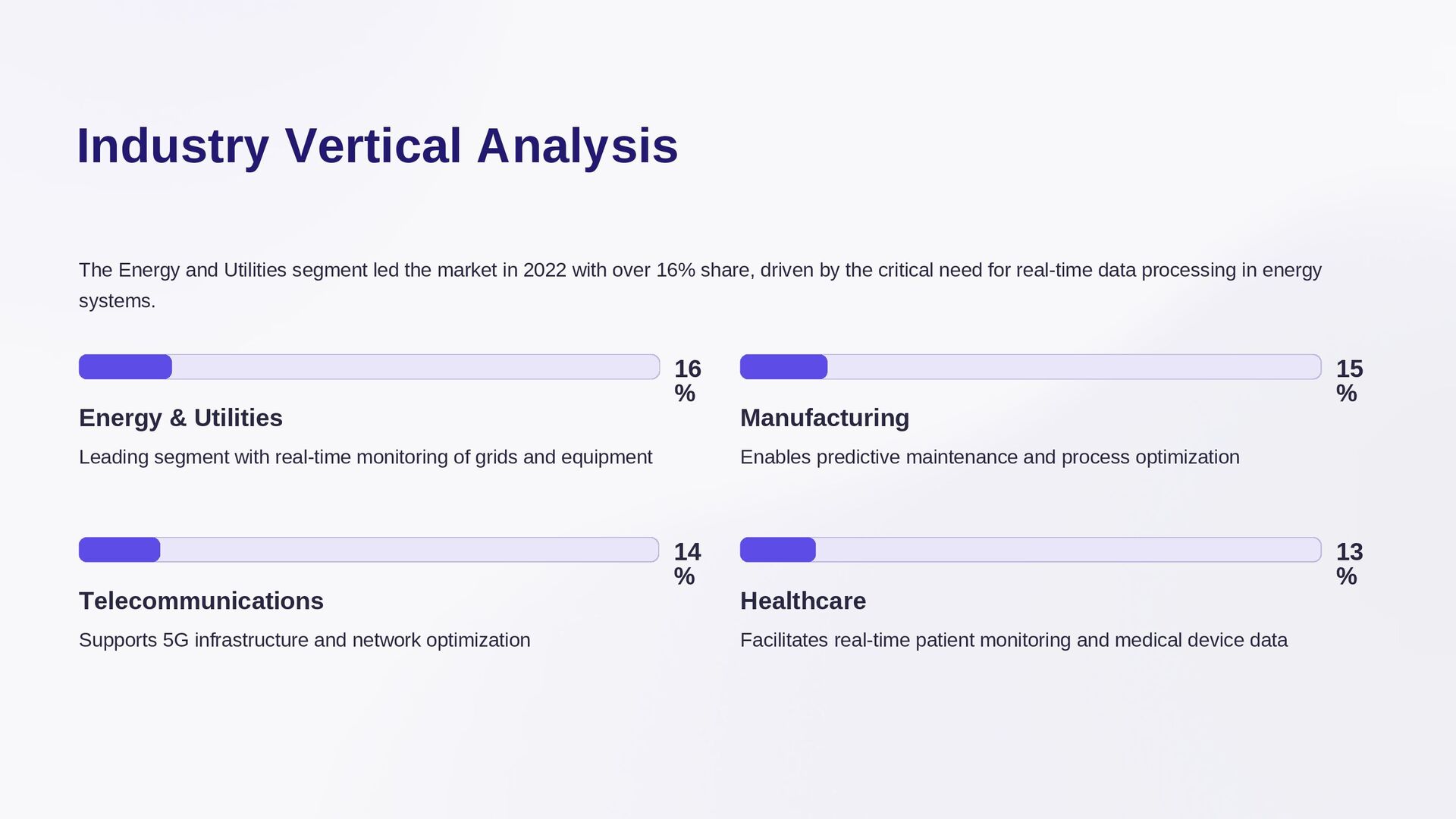

Among use cases, the Industrial Internet of Things (IIoT) emerged as the leading segment with over 30% share, driven by the need to process machine data locally for predictive maintenance, asset monitoring, and automation in manufacturing facilities. The Energy and Utilities sector also held a notable position, accounting for more than 16% of the market in 2022, as grid modernization and smart metering demanded decentralized data analytics.

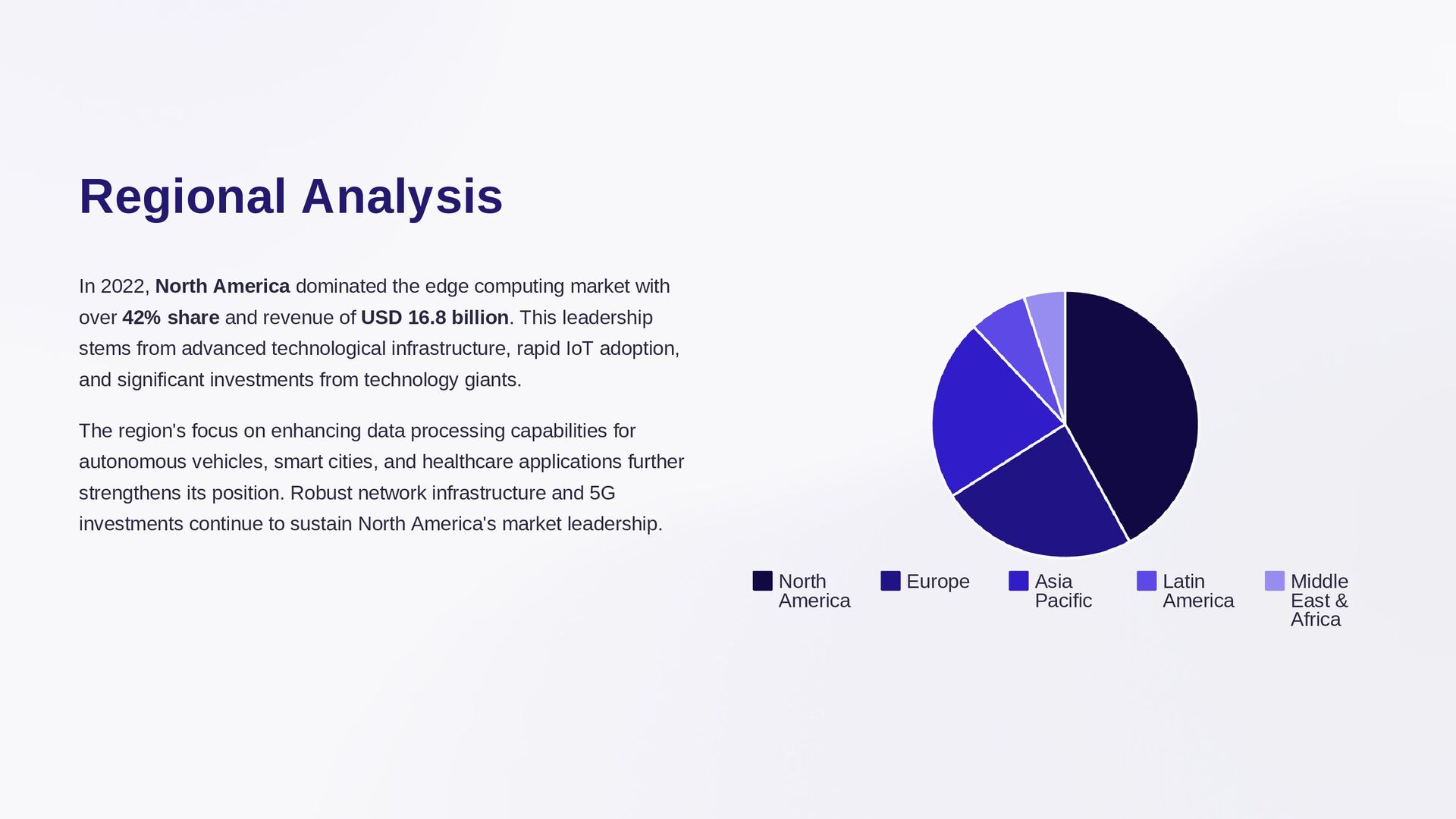

Regionally, North America led the global edge computing market in 2022, with a dominant 42% share and revenue of approximately USD 16.8 billion. This leadership was driven by early infrastructure investments, a robust base of cloud and AI providers, and growing industrial digitization efforts across the U.S. and Canada. With increasing deployments across autonomous vehicles, smart cities, and industrial automation, the region continues to be a critical hub for edge technology adoption and innovation.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}