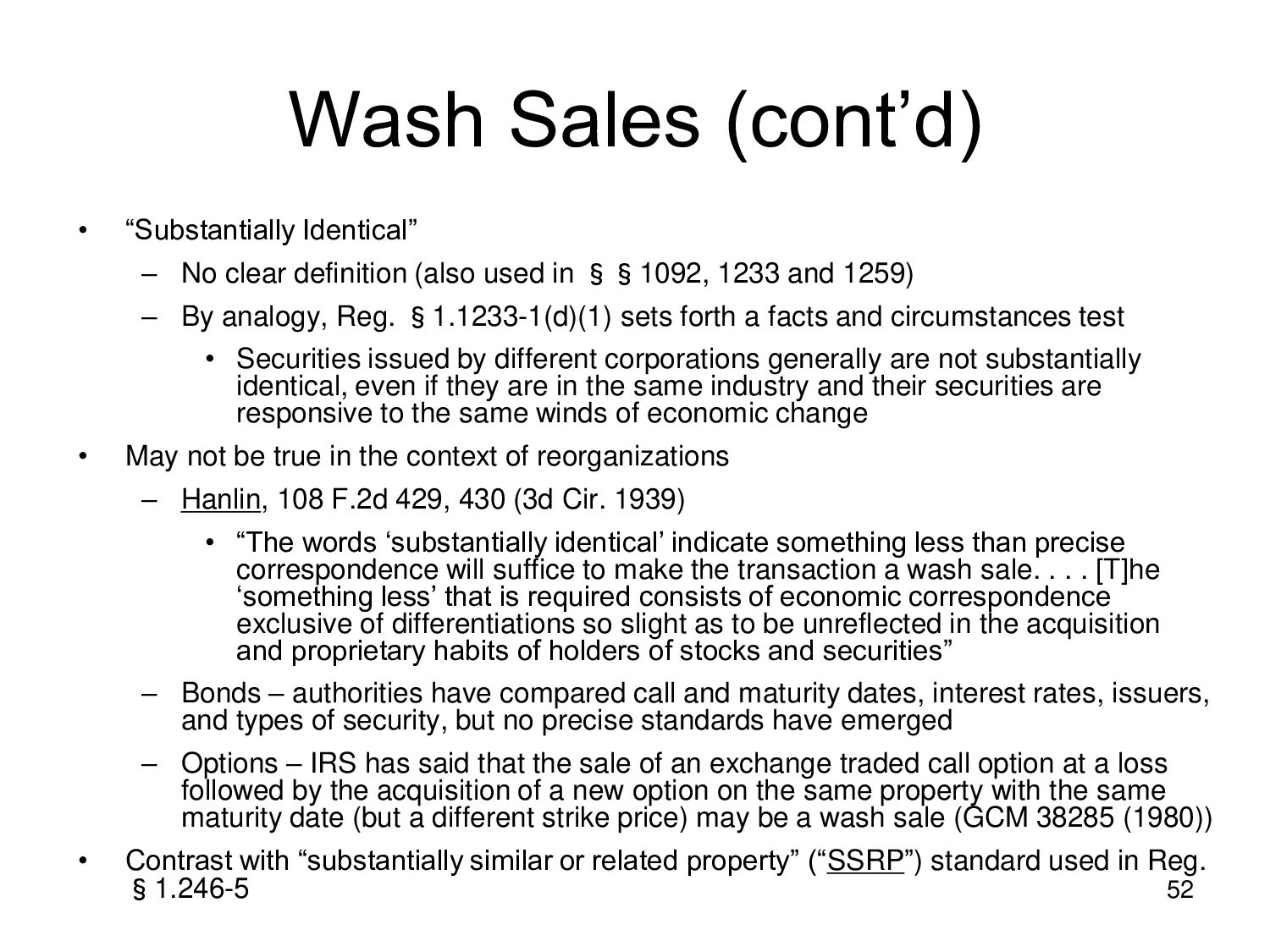

(also used in §§1092, 1233 and 1259) – By analogy, Reg. §1.1233-1(d)(1) sets forth a facts and circumstances test • Securities issued by different corporations generally are not substantially identical, even if they are in the same industry and their securities are responsive to the same winds of economic change • May not be true in the context of reorganizations – Hanlin, 108 F.2d 429, 430 (3d Cir. 1939) • “The words ‘substantially identical’ indicate something less than precise correspondence will suffice to make the transaction a wash sale. . . . [T]he ‘something less’ that is required consists of economic correspondence exclusive of differentiations so slight as to be unreflected in the acquisition and proprietary habits of holders of stocks and securities” – Bonds – authorities have compared call and maturity dates, interest rates, issuers, and types of security, but no precise standards have emerged – Options – IRS has said that the sale of an exchange traded call option at a loss followed by the acquisition of a new option on the same property with the same maturity date (but a different strike price) may be a wash sale (GCM 38285 (1980)) • Contrast with “substantially similar or related property” (“SSRP”) standard used in Reg. §1.246-5 52

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}