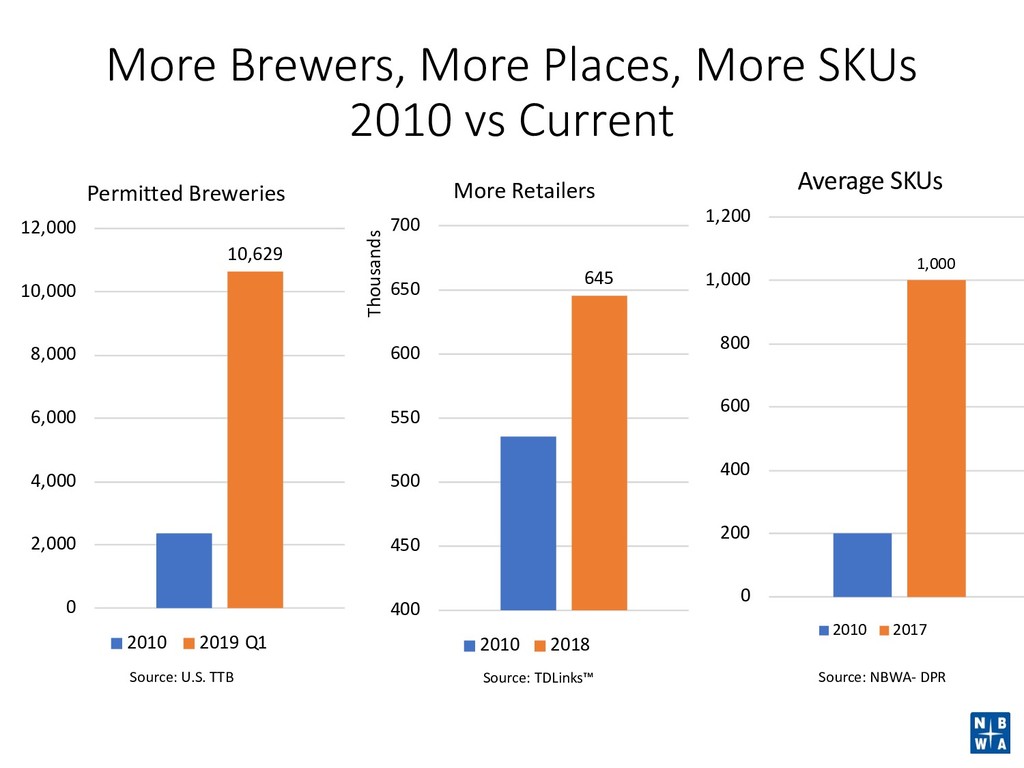

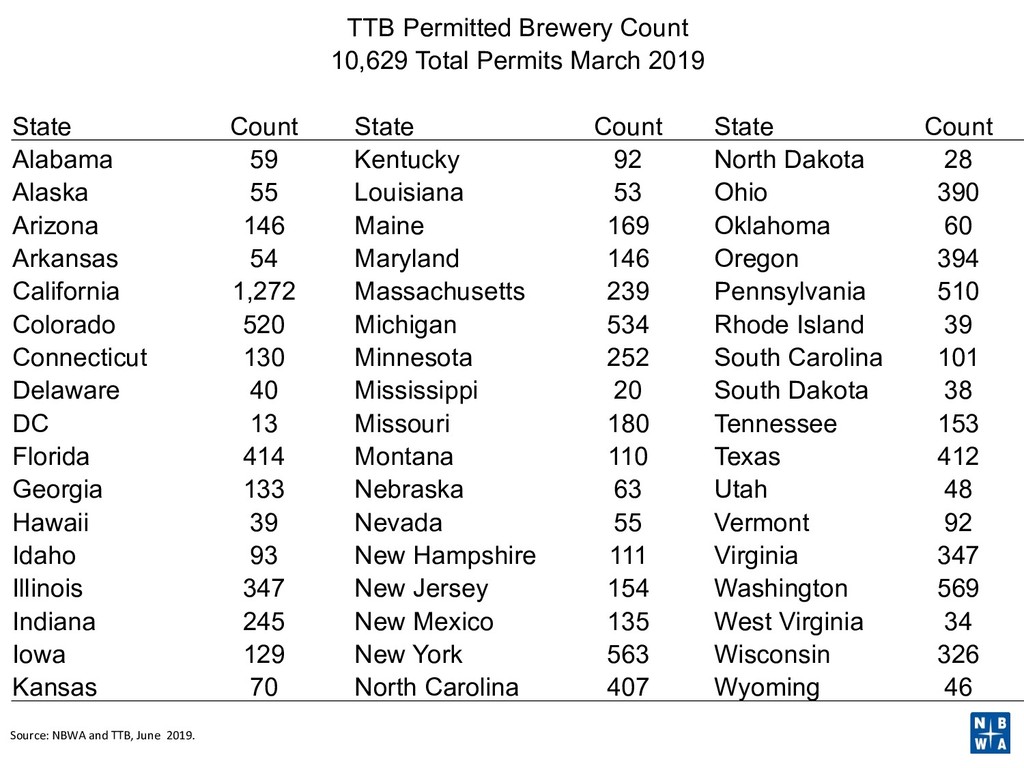

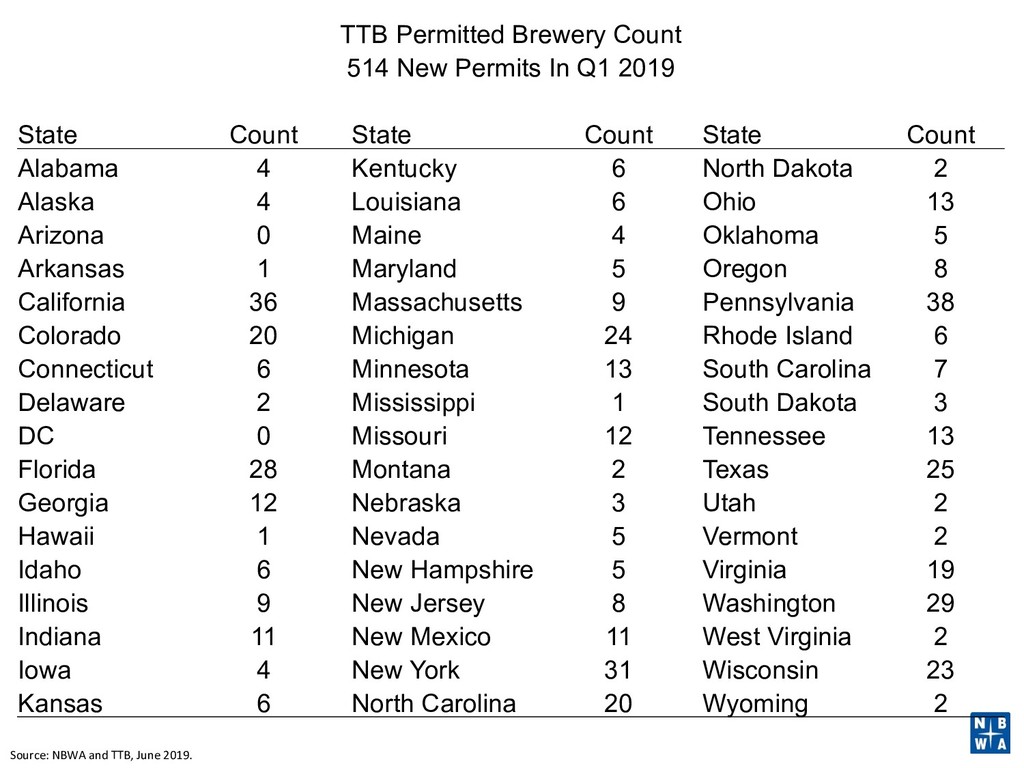

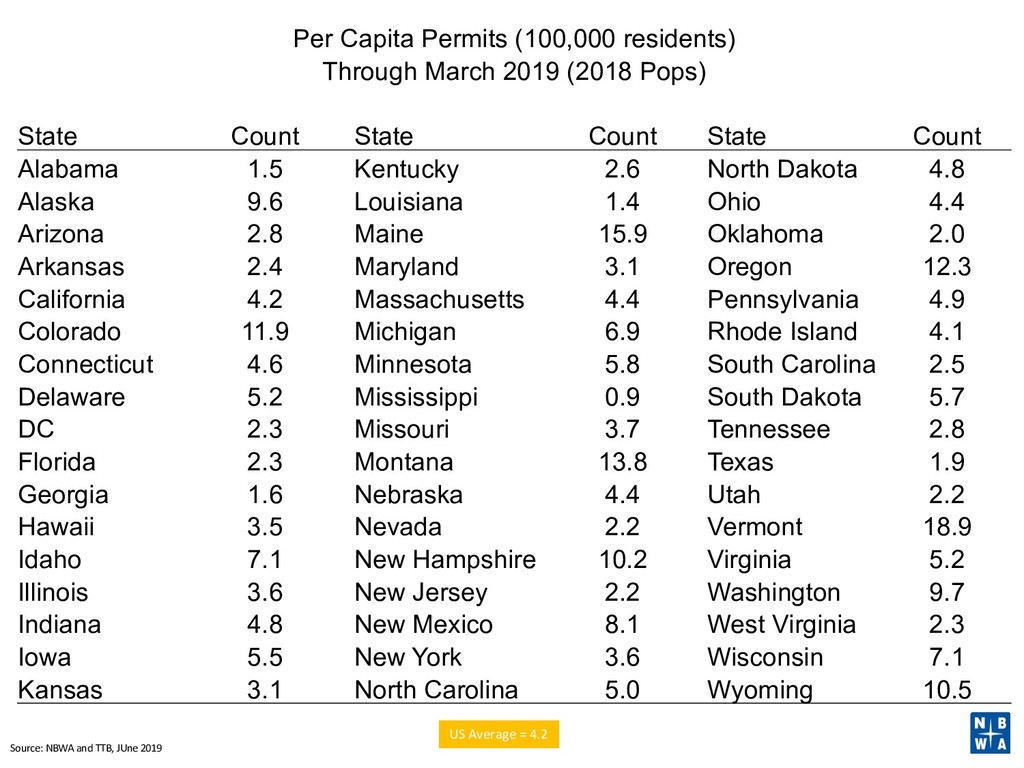

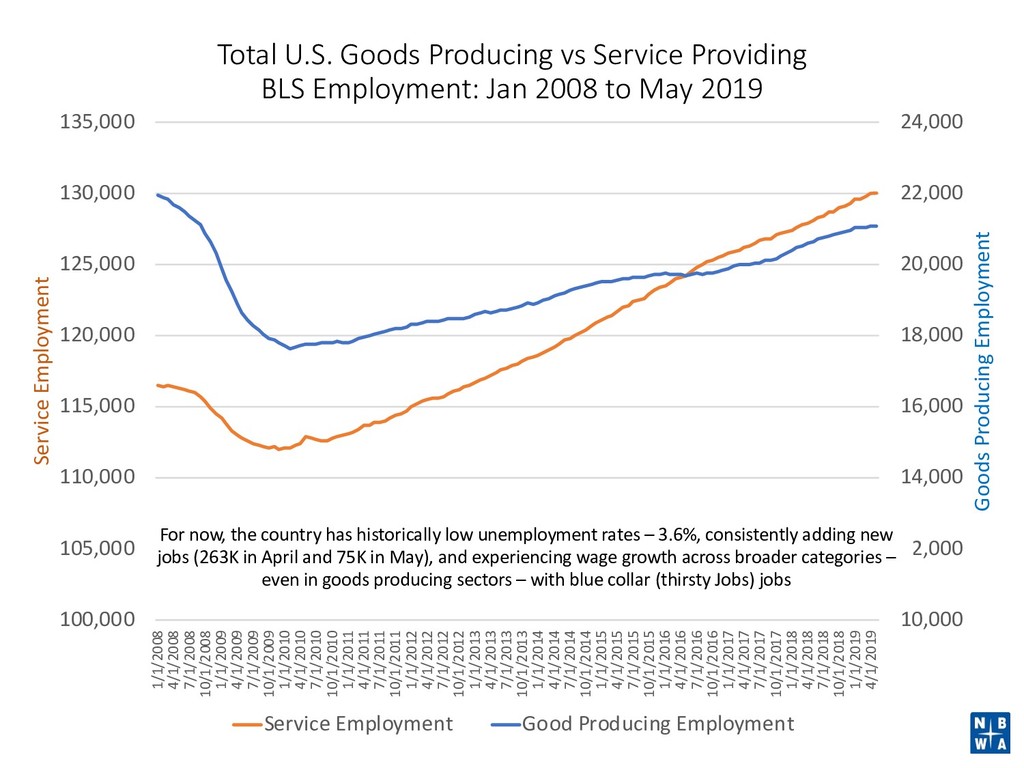

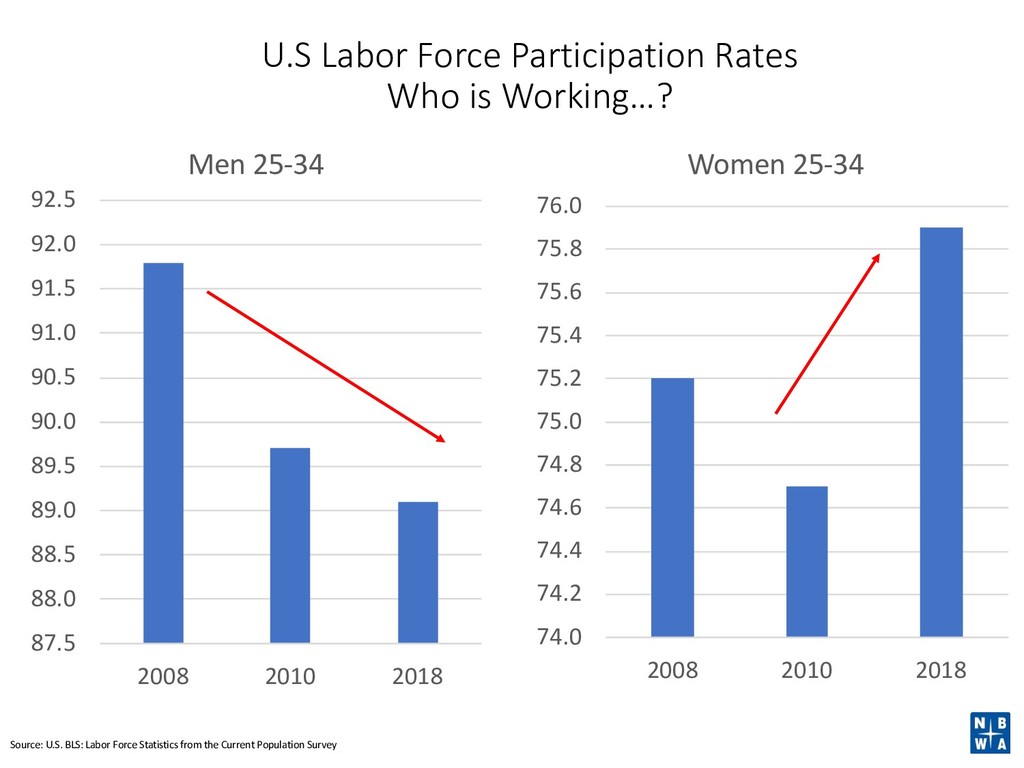

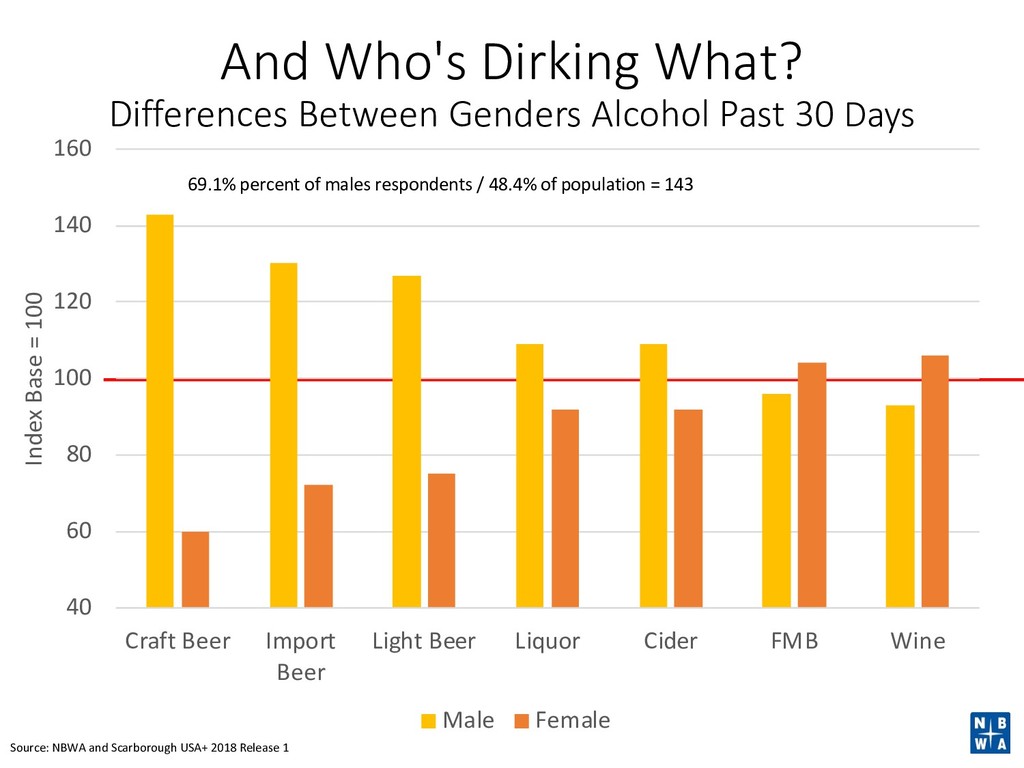

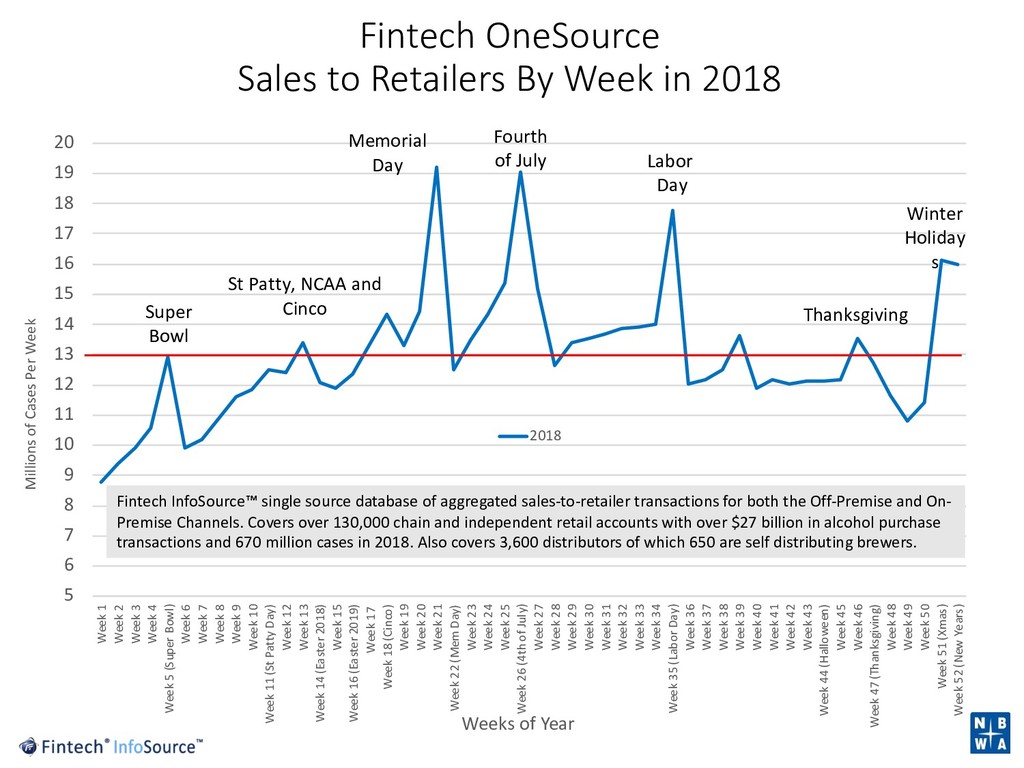

The U.S. Beer Market: Past, Present and Future: The beer industry has changed dramatically. Brewers, distributors and retailers continue to react to consumers’ demand for innovation in beer while looking quality and affordability. Existing breweries are merging, setting up taprooms and, in some cases, selling to larger players. Distributors are diversifying ways to get beer to a rapidly changing retail market. National Beer Wholesalers Association Chief Economist Lester Jones will examine where the industry has been and where it is headed. He will also help attendees understand the data that shape stories on the growing alcohol beverage marketplace. He will present compelling data and insights to help beer writers better understand the policy, economic and demographic factors shaping the industry in 2019 and beyond.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}