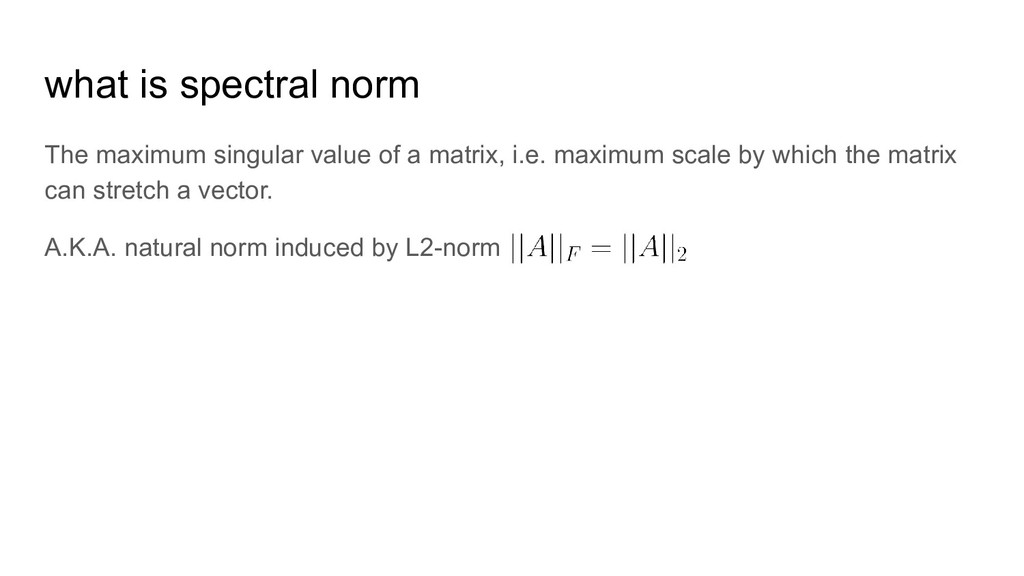

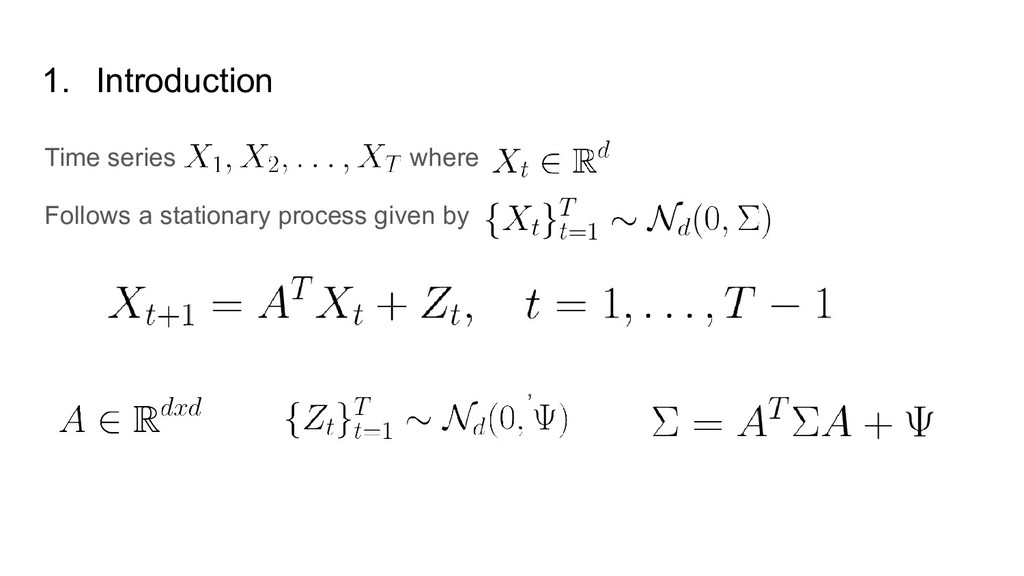

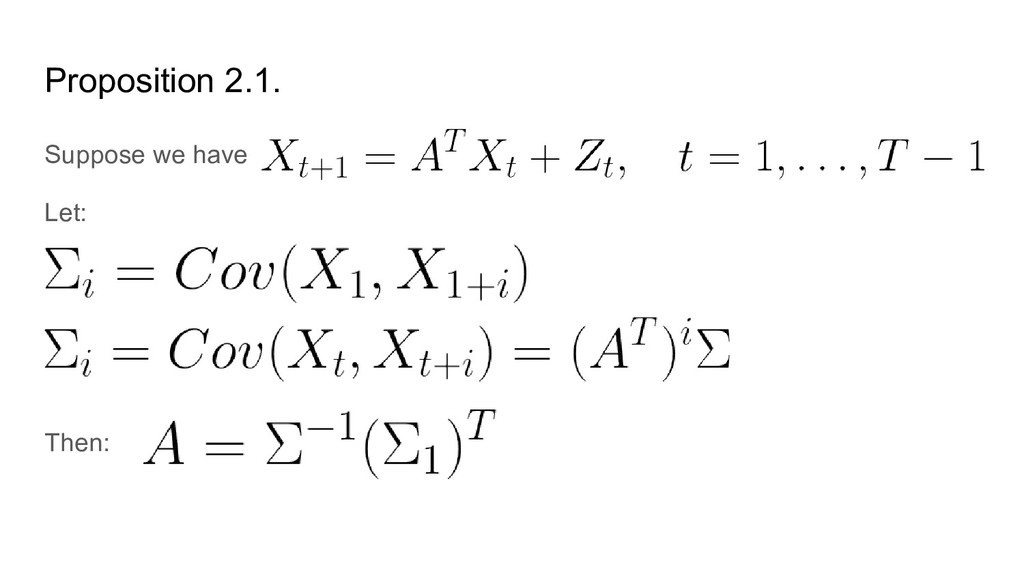

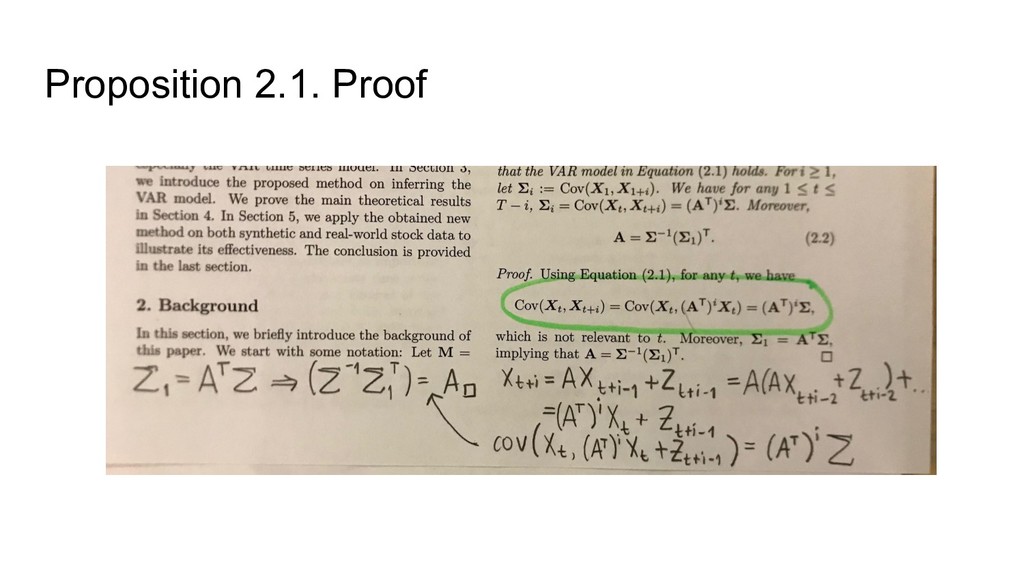

initial state vector produces the state vector at a later time. This is not the same as a stochastic matrix, which represents the transition probabilities in a Markov chain. The transition matrix is TIME INVARIANT.

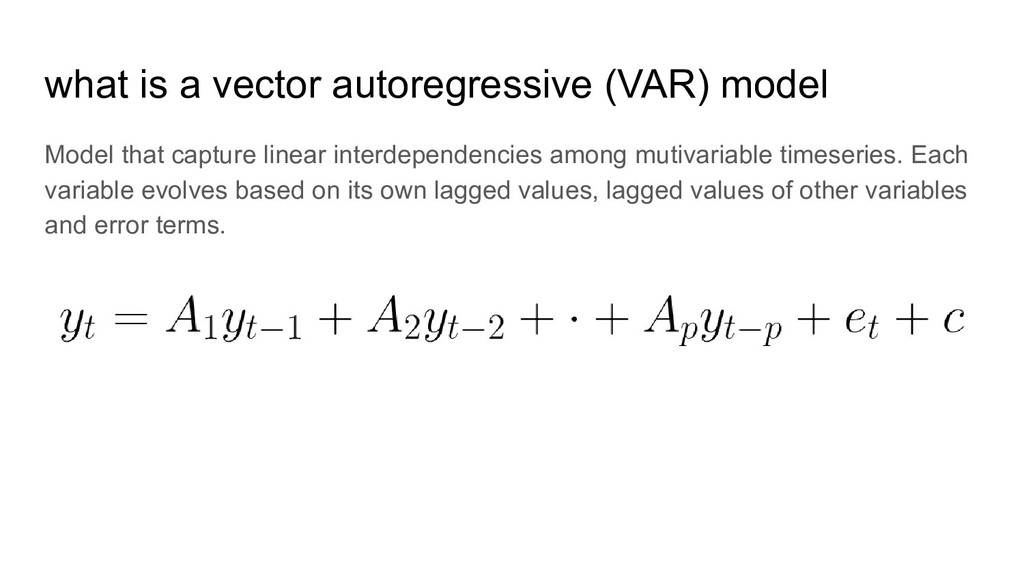

linear interdependencies among mutivariable timeseries. Each variable evolves based on its own lagged values, lagged values of other variables and error terms.

joint probability distribution does not change when shifted in time, i.e. mean and variance don't change over time. As you might imagine, many stochastic processes are non-stationary, but as we do in CSE world: non-linear becomes linear non-stationary becomes stationary Most common cause of stationarity violation: trend

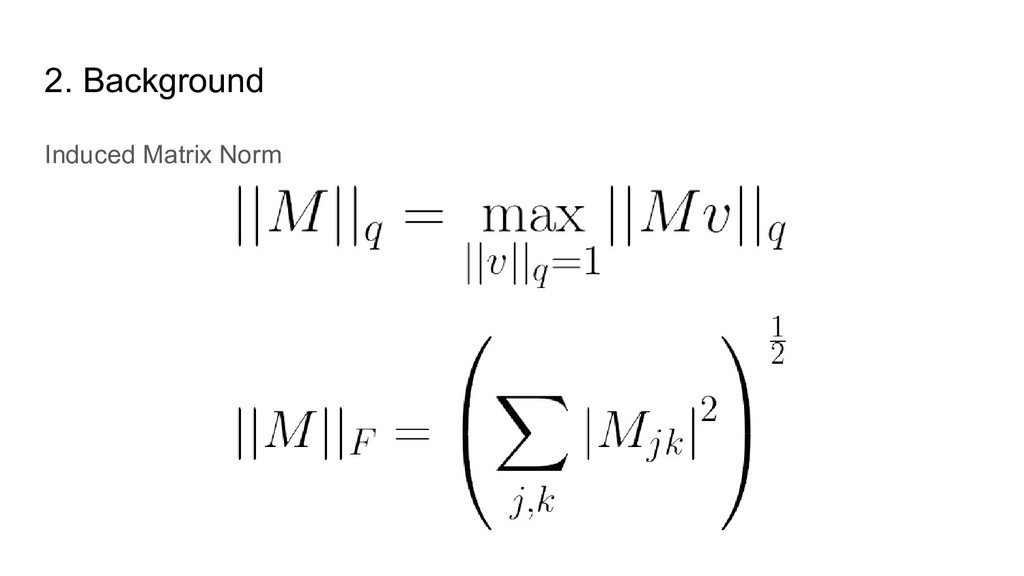

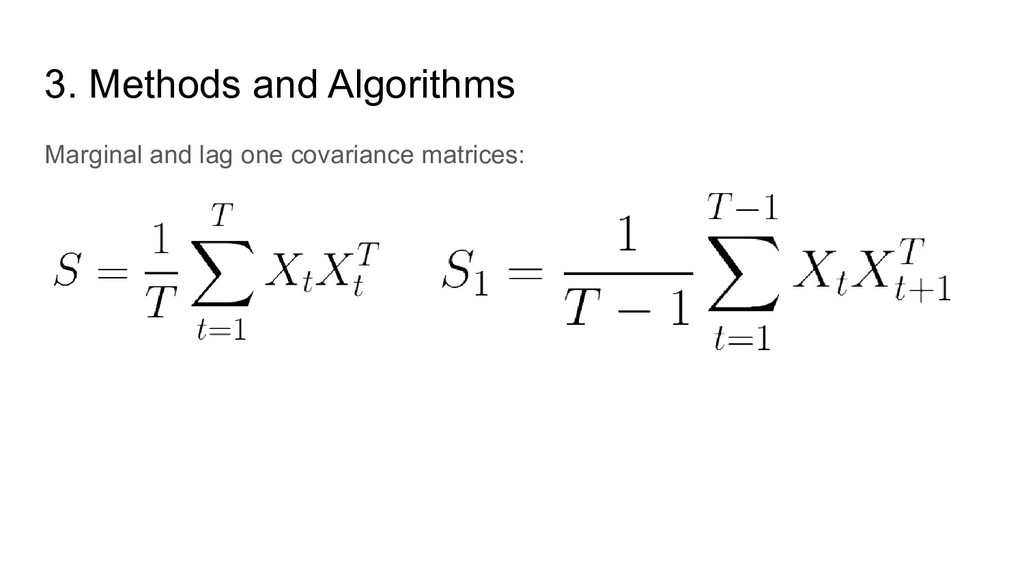

conditional. Direct representation of the covariance of the timeseries, without the effects of other variables. Relies on the marginal distribution of the variables. Lagged: Covariance of time series with time-lagged time series

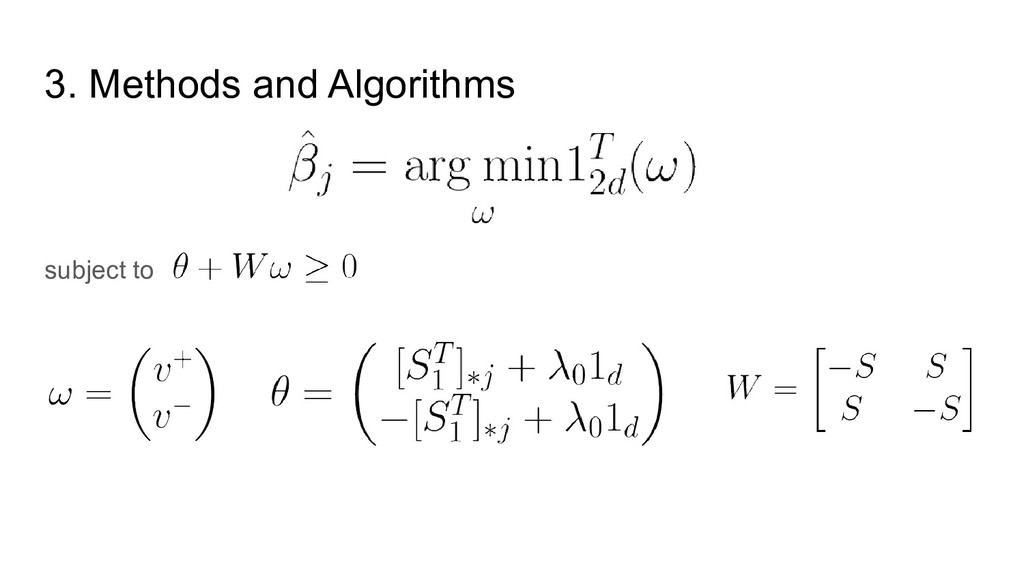

the equations that govern your system. If you know the dynamics of your system you should be able to calculate your matrix in a closed form. If you have non-linearities in your system you try to linearize and calculate the matrix. But if you HAVE NO IDEA of the dynamics of your system, you need a good estimator.

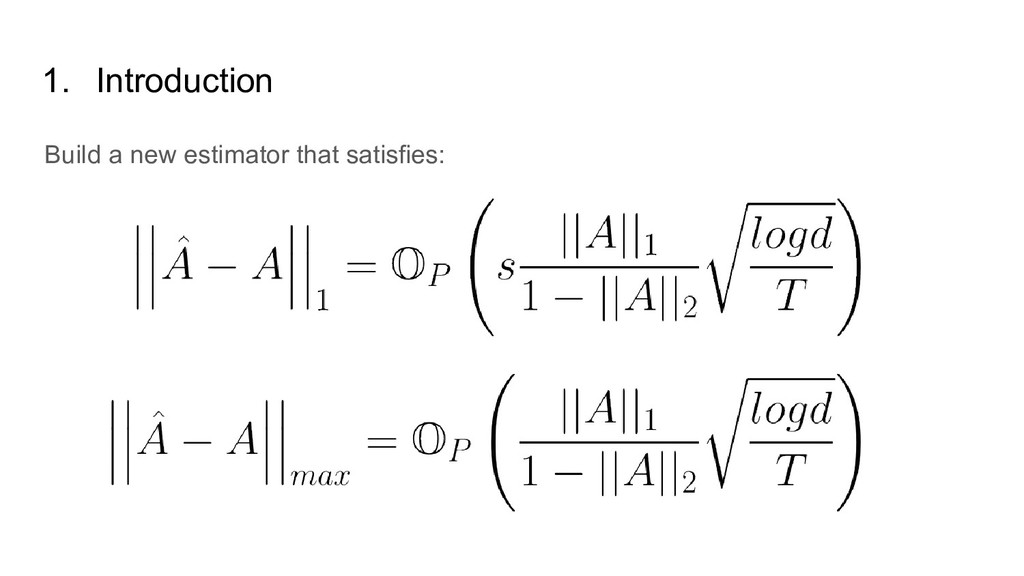

proposed method calculating the transition matrix of a VAR model is smaller than the one obtained using LSE and ridge/lasso penalty 2) Than this error is bounded

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}