the energy transition 2018 International Forum on Energy Eduation, Tainan – Taiwan, 7th December , 2018. Prof. Dr. André P.C. Faaij Distinguished Professor Energy System Analysis – University of Groningen Director of Science, ECN part of TNO

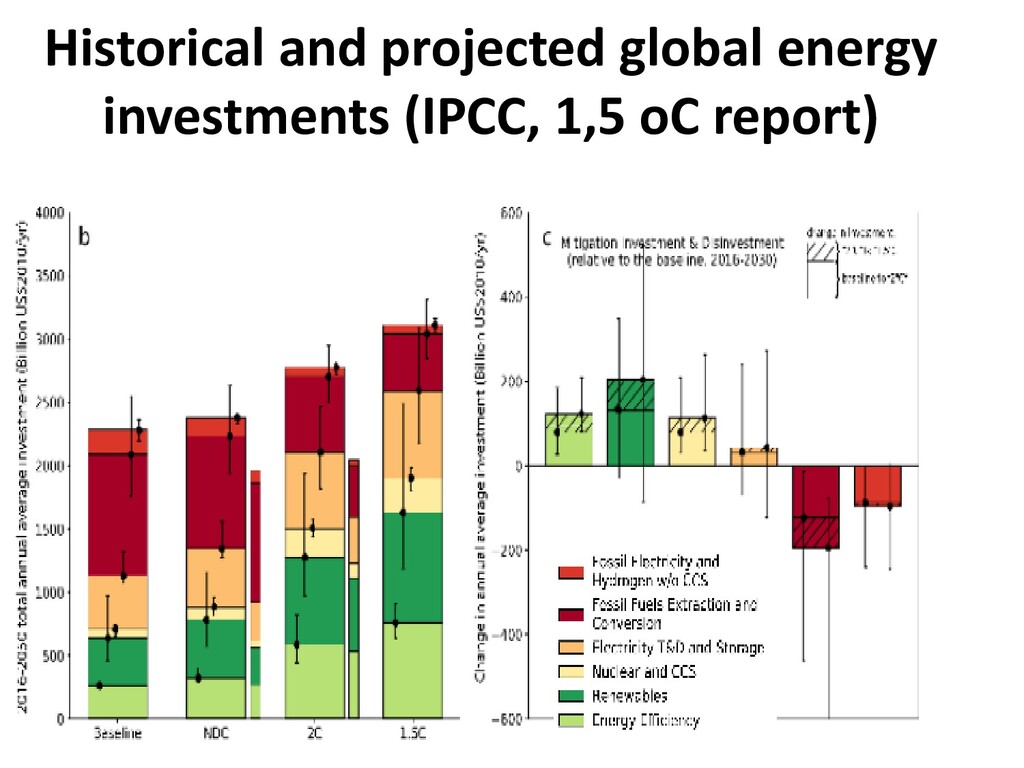

• Costs of CO2: estimates for a Below-1.5˚C pathway range from: • 135–5500 USD2010 tCO2-eq in 2030 • 245–13000 USD2010 tCO2-eq in 2050 • 420–17500 USD2010 tCO2-eq in 2070 • 690–27000 USD2010 tCO2-eq in 2100 • Models that encompass a higher degree of technology granularity and more flexibility in mitigation technology portfolio, often produce relatively lower mitigation costs. • Ranges explained by: methodologies, projected energy service demands, mitigation targets, fuel prices and technology availability. The characteristics of the technology portfolio, particularly in terms of investment costs and deployment rates play a key role. 6

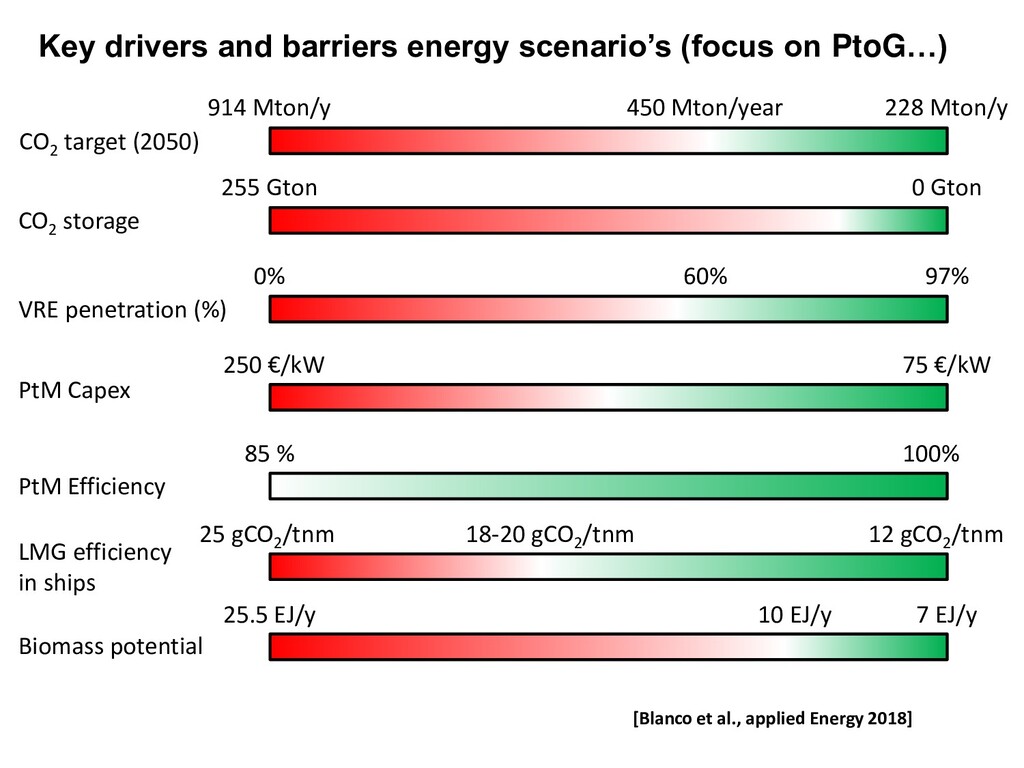

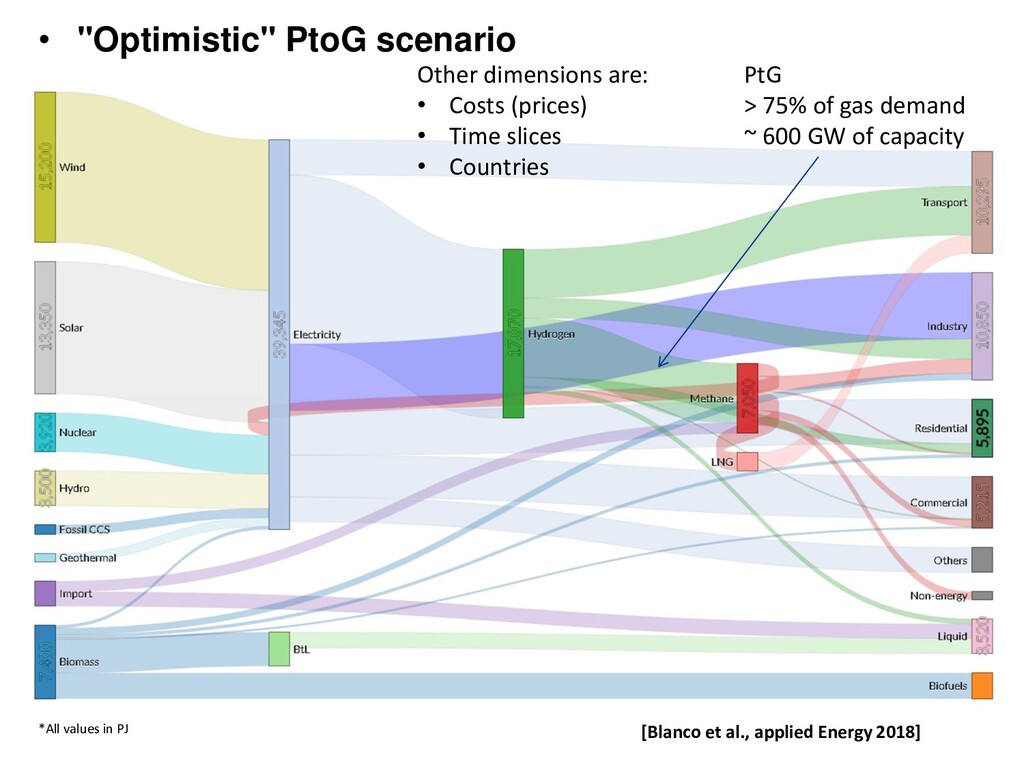

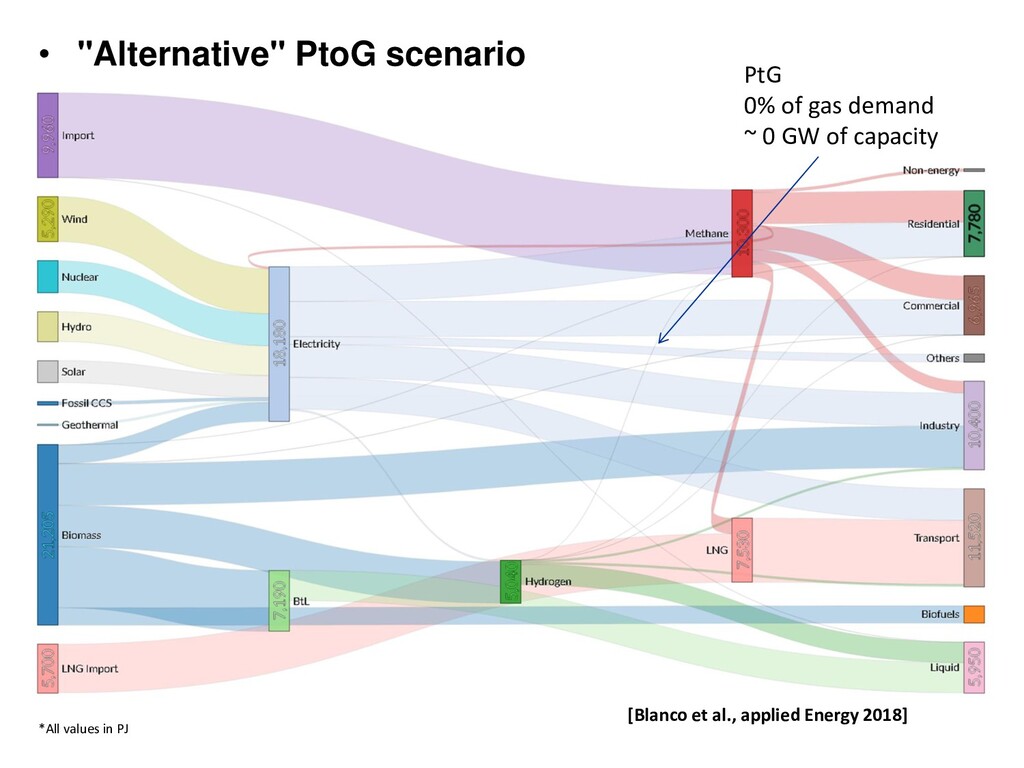

transport increases by 27% (2015 – 2050) in private transport, 20% for buses and almost 40% for heavy-duty, aviation 80-100% increase. • private transport reduces its energy demand by almost 60% (7900 to 3400 PJ) in large part due to electric vehicles, which have 60% share of the market, while the rest is due to the use of more efficient cars. • Industrial output increases ~20%, combined with 5 to 17% reduction of energy demand by 2050. This signals the widespread use of more efficient options. • Demand for space heating in the residential sector decreases by 30-40% (insulation). The 40% reduction in demand of the residential sector is also achieved through a shift in energy carrier to electricity, which has almost 75% share across the main scenarios, nearly eliminating gas use (reduction of 90- 95% vs. 2015) [Blanco et al., applied Energy 2018]

210 Mt CO2 o Electricity potential doubles this consumption o Dutch EEZ CO2 capacity in depleted gas and oil fields equals 13 years Technical potential North Sea Dutch EEZ Offshore wind 2,765 TWh/yr 240 TWh/yr Wave 77 TWh/yr 5 TWh/yr Algae 400 (37,000) PJ/yr 90 (2,800)/yr CO2 storage capacity 20 (125) Gt CO2 1.3 (2.3) Gt CO2 O&G extraction 137 EJ 0 1,000 2,000 3,000 Electricity (TWh/yr) Electricity N-Sea Wind Wave Capacity Generated 2016 0 5 10 15 20 CO2 (Gt) CO2 storage in O&G fields in N-Sea UK Norway NL Germany Denmark Belgium Emitted 2016 Sinks 13 X 2 X 15 NORTH SEA ENERGY POTENTIALS…

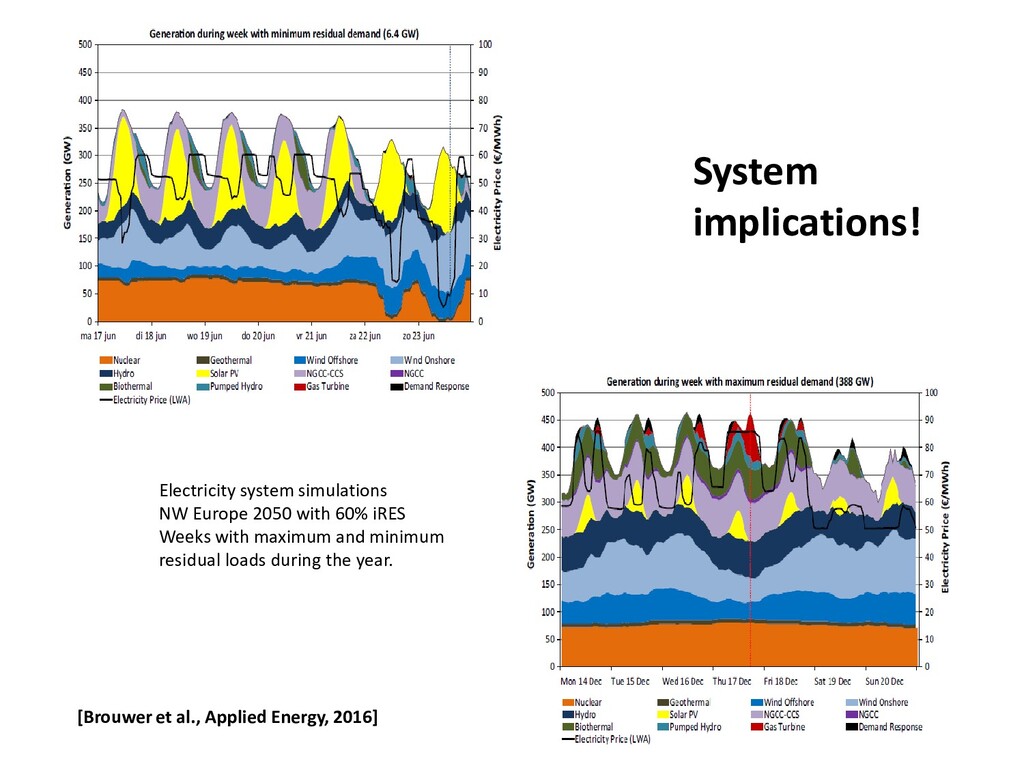

(electricity only!) Breakdown of installed capacities and power generation in the core scenarios in the year 2050. The dashed line depicts the peak load in 2050. [Brouwer et al., Applied Energy, 2016]

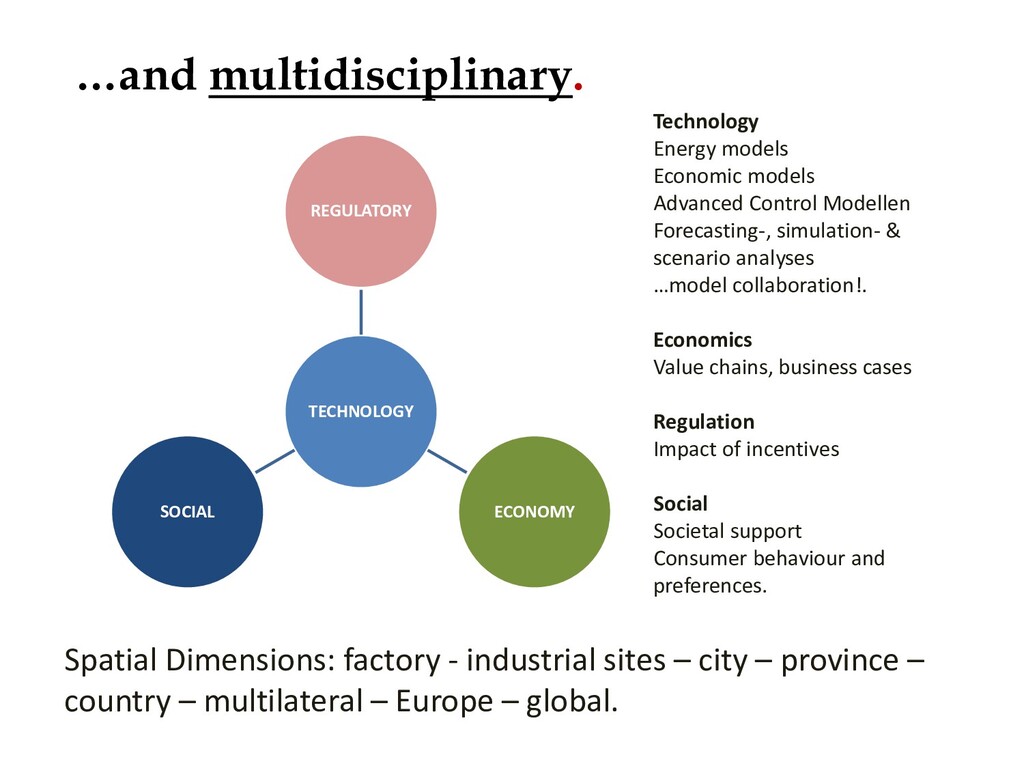

Control Modellen Forecasting-, simulation- & scenario analyses …model collaboration!. Economics Value chains, business cases Regulation Impact of incentives Social Societal support Consumer behaviour and preferences. …and multidisciplinary. Spatial Dimensions: factory - industrial sites – city – province – country – multilateral – Europe – global.

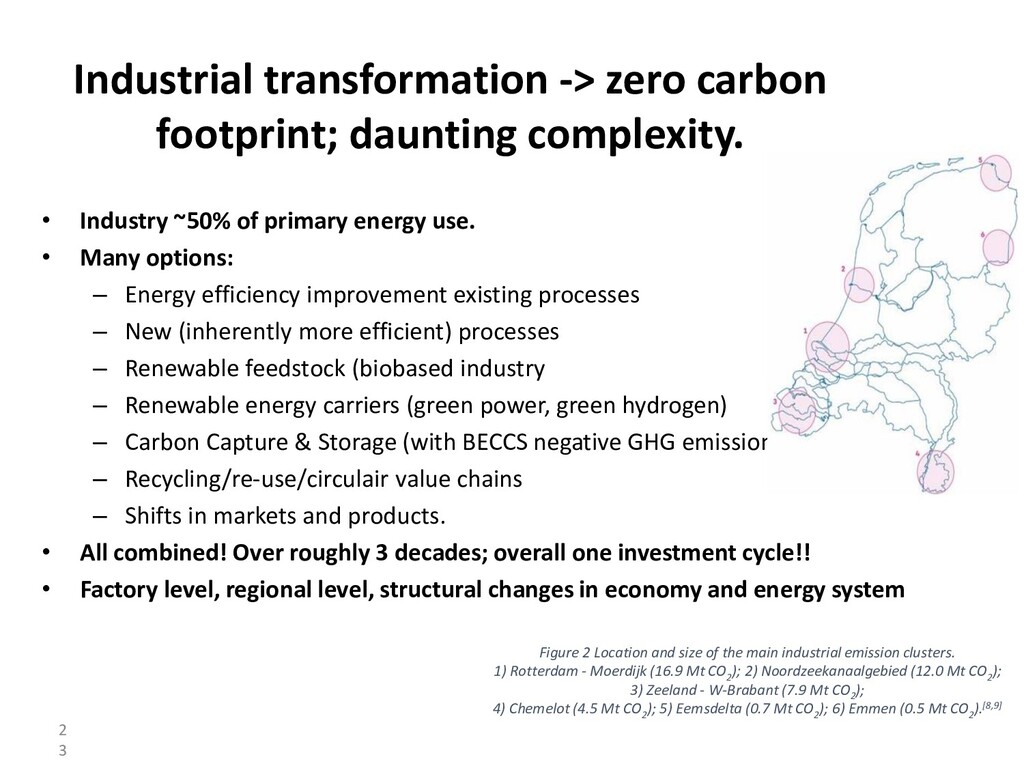

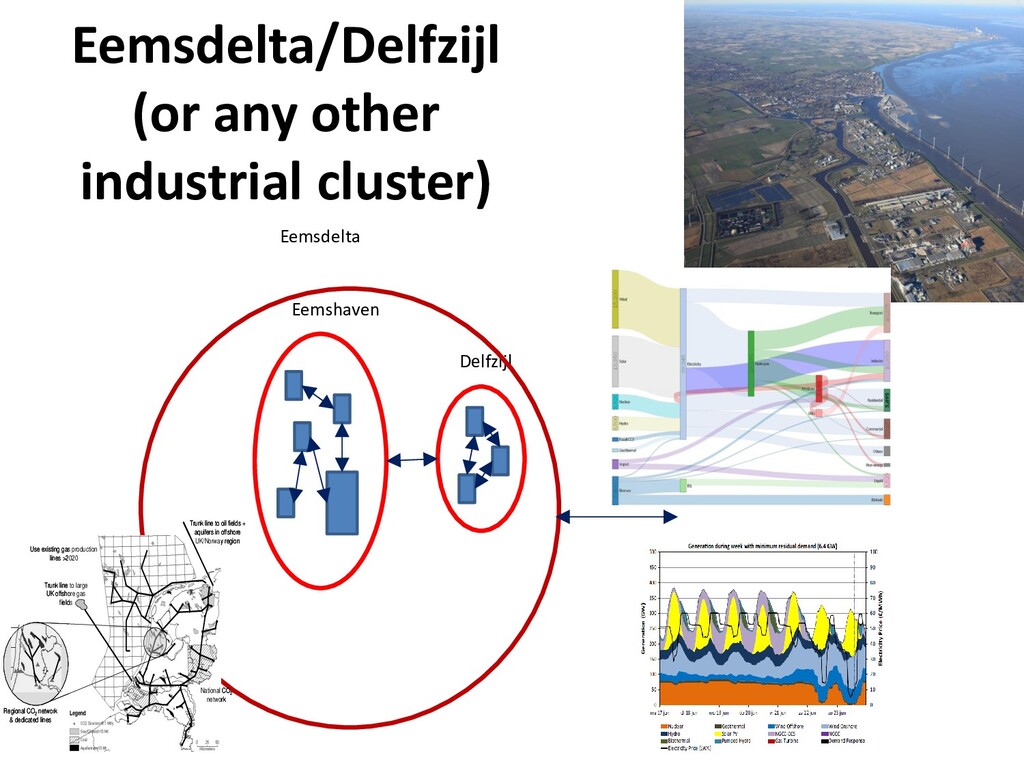

~50% of primary energy use. • Many options: – Energy efficiency improvement existing processes – New (inherently more efficient) processes – Renewable feedstock (biobased industry – Renewable energy carriers (green power, green hydrogen) – Carbon Capture & Storage (with BECCS negative GHG emissions) – Recycling/re-use/circulair value chains – Shifts in markets and products. • All combined! Over roughly 3 decades; overall one investment cycle!! • Factory level, regional level, structural changes in economy and energy system 2 3 Figure 2 Location and size of the main industrial emission clusters. 1) Rotterdam - Moerdijk (16.9 Mt CO 2 ); 2) Noordzeekanaalgebied (12.0 Mt CO 2 ); 3) Zeeland - W-Brabant (7.9 Mt CO 2 ); 4) Chemelot (4.5 Mt CO 2 ); 5) Eemsdelta (0.7 Mt CO 2 ); 6) Emmen (0.5 Mt CO 2 ).[8,9]

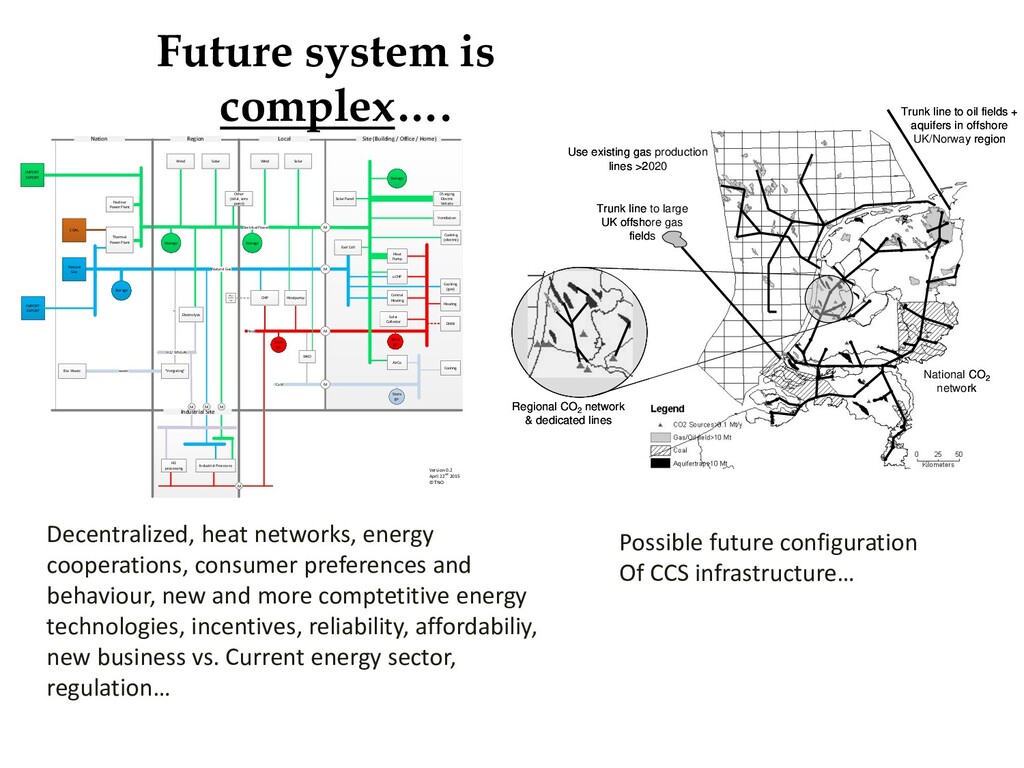

CO2 network Regional CO2 network & dedicated lines Use existing gas production lines >2020 Trunk line to large UK offshore gas fields Trunk line to oil fields + aquifers in offshore UK/Norway region National CO2 network Regional CO2 network & dedicated lines Use existing gas production lines >2020 Trunk line to large UK offshore gas fields Trunk line to oil fields + aquifers in offshore UK/Norway region

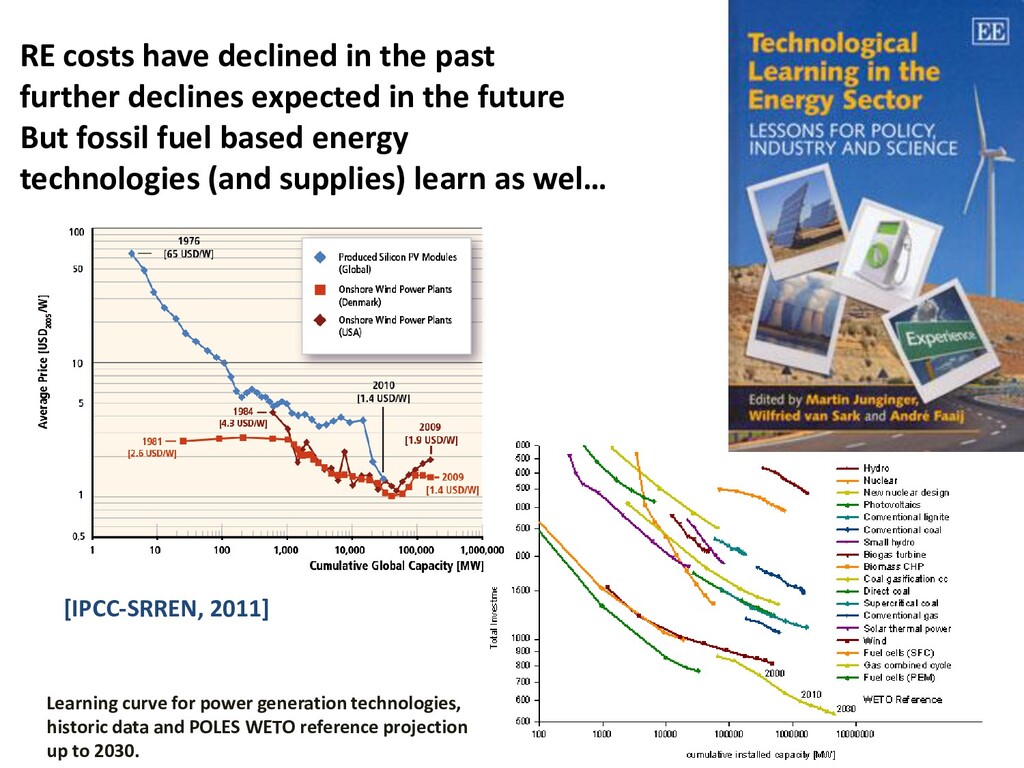

in the future But fossil fuel based energy technologies (and supplies) learn as wel… Learning curve for power generation technologies, historic data and POLES WETO reference projection up to 2030. [IPCC-SRREN, 2011]

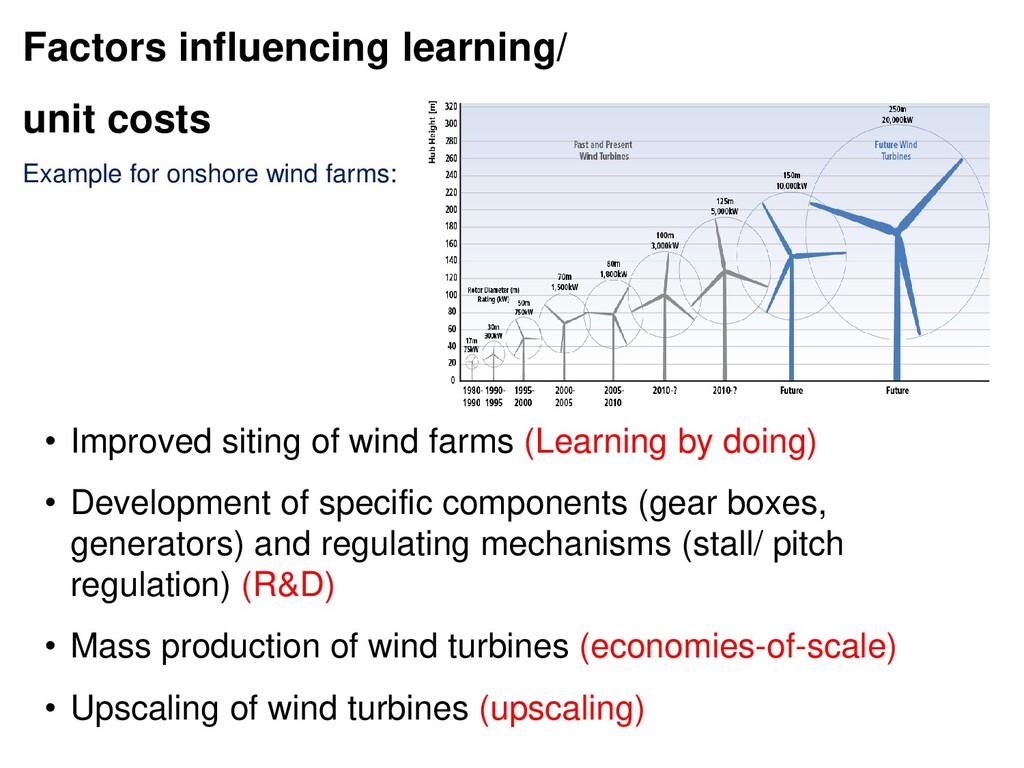

Development of specific components (gear boxes, generators) and regulating mechanisms (stall/ pitch regulation) (R&D) • Mass production of wind turbines (economies-of-scale) • Upscaling of wind turbines (upscaling) Factors influencing learning/ unit costs Example for onshore wind farms:

barrier for realizing the ambitious energy transition goals. • At the same time there is a substantial need for equipping existing energy professionals with up to date skills. • Required skills and knowledge change fast. • Increasingly interdisciplinary. 31 Major human capital agenda

Training Netwerk; applied on the energy transition of the North Sea Region (ENSYSTRA). 15 PhD researchers Technology, Energy system modelling Actor behaviour, Markets, Policy Integrated education program Many links between projects

of the Netherlands Rationale for the initiative: build a leading knowledge infrastructure to support ‘’the energy transition’’ at large; intermingling scientific and applied research across the board, energy education from vocational to post-academic and business development & entrepreneurship

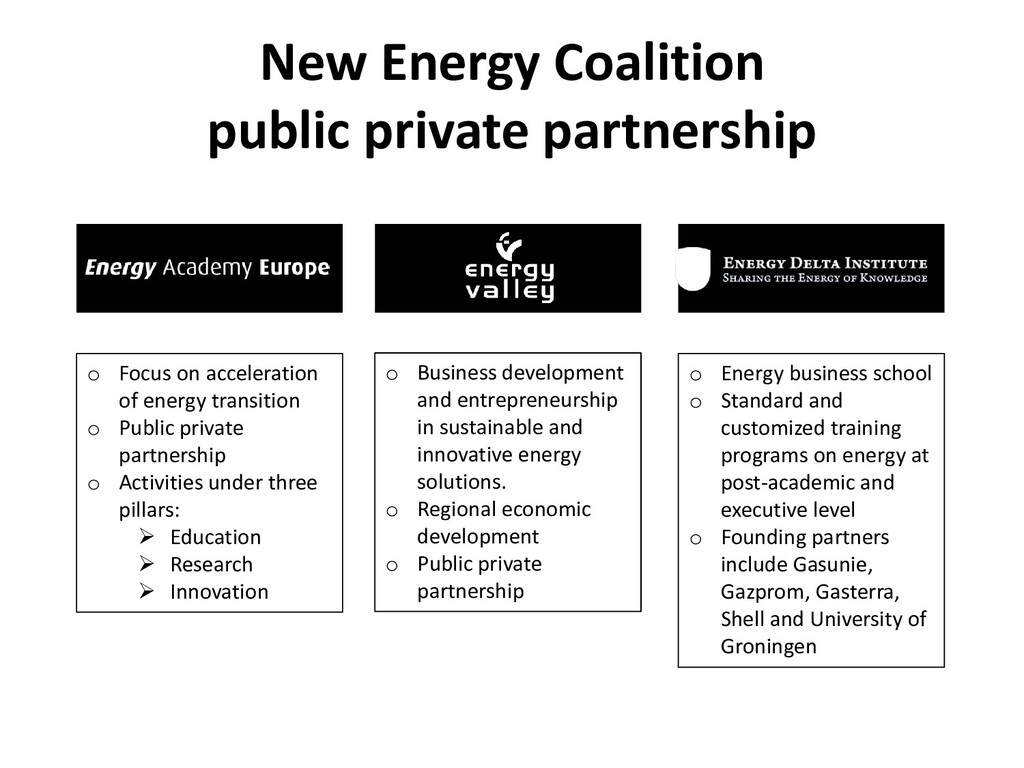

of energy transition o Public private partnership o Activities under three pillars: Education Research Innovation o Business development and entrepreneurship in sustainable and innovative energy solutions. o Regional economic development o Public private partnership o Energy business school o Standard and customized training programs on energy at post-academic and executive level o Founding partners include Gasunie, Gazprom, Gasterra, Shell and University of Groningen

Energy business is changing • New professionals needed from vocational to academic (and post-academic) level. • Research to support innovation and implementation; increasingly interdisciplinary. Societal needs and relevance

School • Universities and vocational education focused on energy • Research and innovation facilities (ESTRAC, EnTranCe, IDEA, Investa, Energy Venture Lab, Energysense) • Network • International, national and regional • Knowledge institutes, Business, Governments

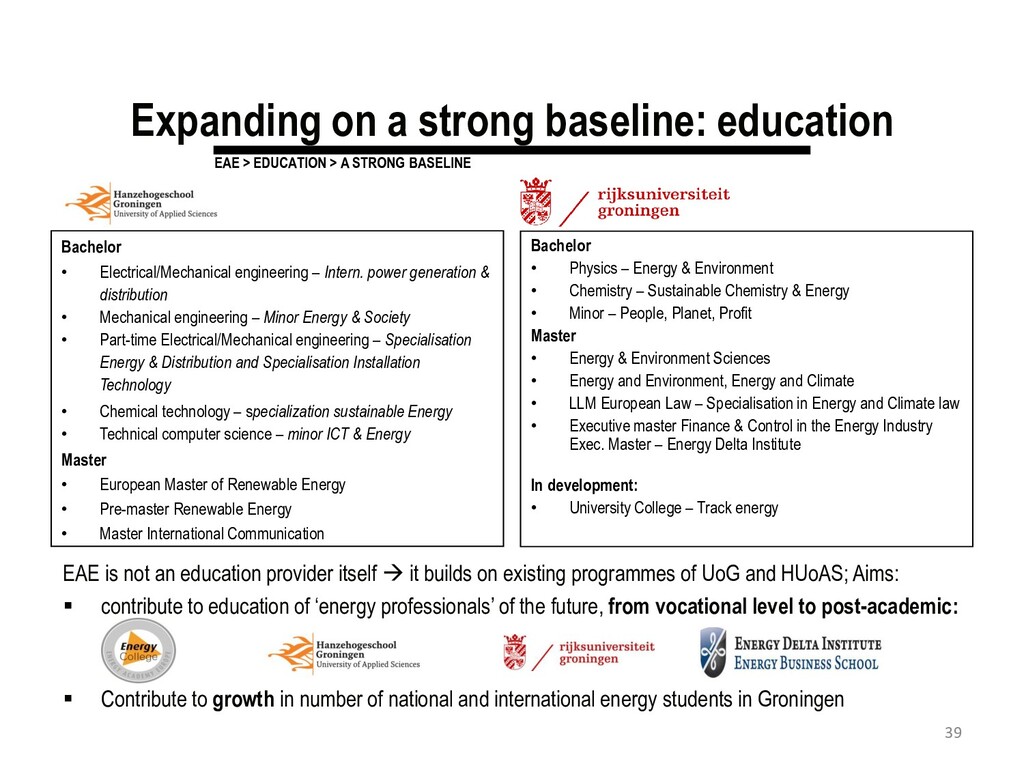

– Intern. power generation & distribution • Mechanical engineering – Minor Energy & Society • Part-time Electrical/Mechanical engineering – Specialisation Energy & Distribution and Specialisation Installation Technology • Chemical technology – specialization sustainable Energy • Technical computer science – minor ICT & Energy Master • European Master of Renewable Energy • Pre-master Renewable Energy • Master International Communication Bachelor • Physics – Energy & Environment • Chemistry – Sustainable Chemistry & Energy • Minor – People, Planet, Profit Master • Energy & Environment Sciences • Energy and Environment, Energy and Climate • LLM European Law – Specialisation in Energy and Climate law • Executive master Finance & Control in the Energy Industry Exec. Master – Energy Delta Institute In development: • University College – Track energy EAE > EDUCATION > A STRONG BASELINE 39 EAE is not an education provider itself it builds on existing programmes of UoG and HUoAS; Aims: contribute to education of ‘energy professionals’ of the future, from vocational level to post-academic: Contribute to growth in number of national and international energy students in Groningen

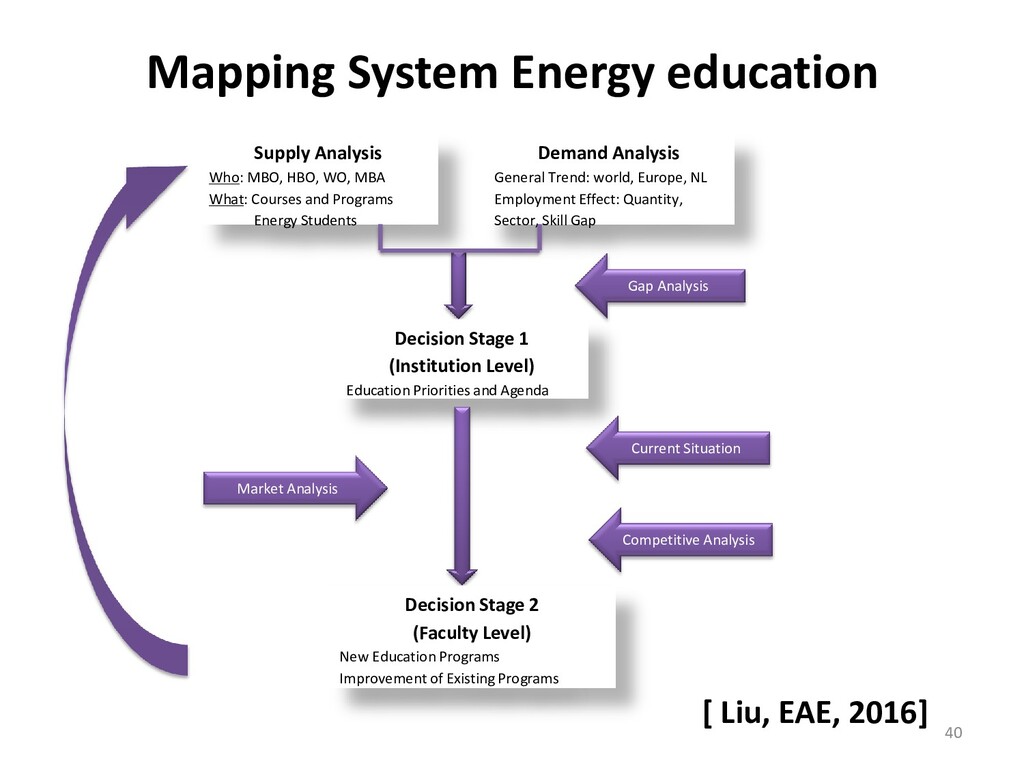

WO, MBA What: Courses and Programs Energy Students Demand Analysis General Trend: world, Europe, NL Employment Effect: Quantity, Sector, Skill Gap Gap Analysis Decision Stage 1 (Institution Level) Education Priorities and Agenda Current Situation Competitive Analysis Market Analysis Decision Stage 2 (Faculty Level) New Education Programs Improvement of Existing Programs [ Liu, EAE, 2016]

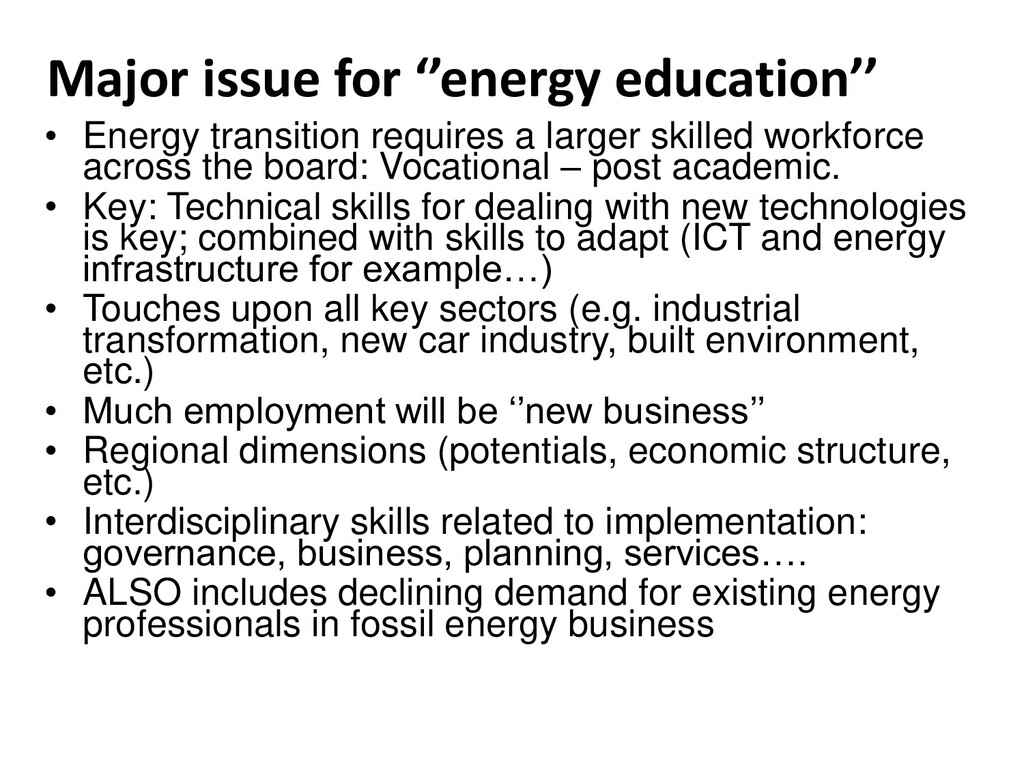

larger skilled workforce across the board: Vocational – post academic. • Key: Technical skills for dealing with new technologies is key; combined with skills to adapt (ICT and energy infrastructure for example…) • Touches upon all key sectors (e.g. industrial transformation, new car industry, built environment, etc.) • Much employment will be ‘’new business’’ • Regional dimensions (potentials, economic structure, etc.) • Interdisciplinary skills related to implementation: governance, business, planning, services…. • ALSO includes declining demand for existing energy professionals in fossil energy business

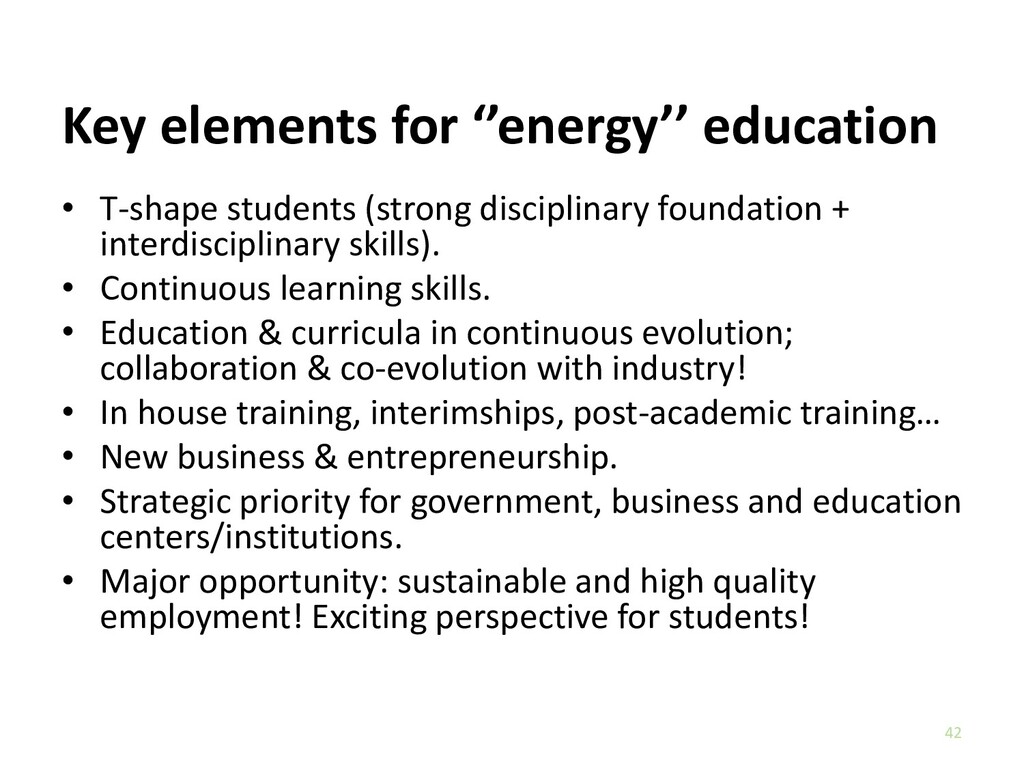

Continuous learning skills. • Education & curricula in continuous evolution; collaboration & co-evolution with industry! • In house training, interimships, post-academic training… • New business & entrepreneurship. • Strategic priority for government, business and education centers/institutions. • Major opportunity: sustainable and high quality employment! Exciting perspective for students! 42 Key elements for ‘’energy’’ education

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}