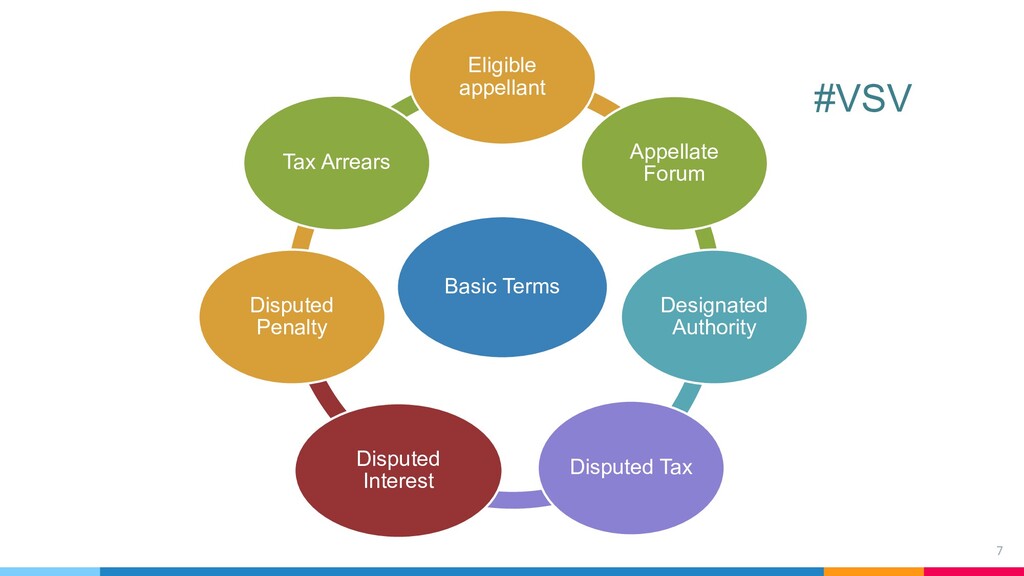

Guided by “Sabka Saath, Sabka Vikas, Sabka Vishwas”, the Finance Minister Smt. Nirmala Sitharaman had introduced a new No Dispute but Trust Scheme – ‘Vivad Se Vishwas’ in the Budget 2020 in the Lok Sabha on 5th February, 2020. Expectations are that the new scheme will work better than erstwhile similar scheme “The Direct Tax Dispute Resolution Scheme, 2016”, given the kind of cases that are in appeal.

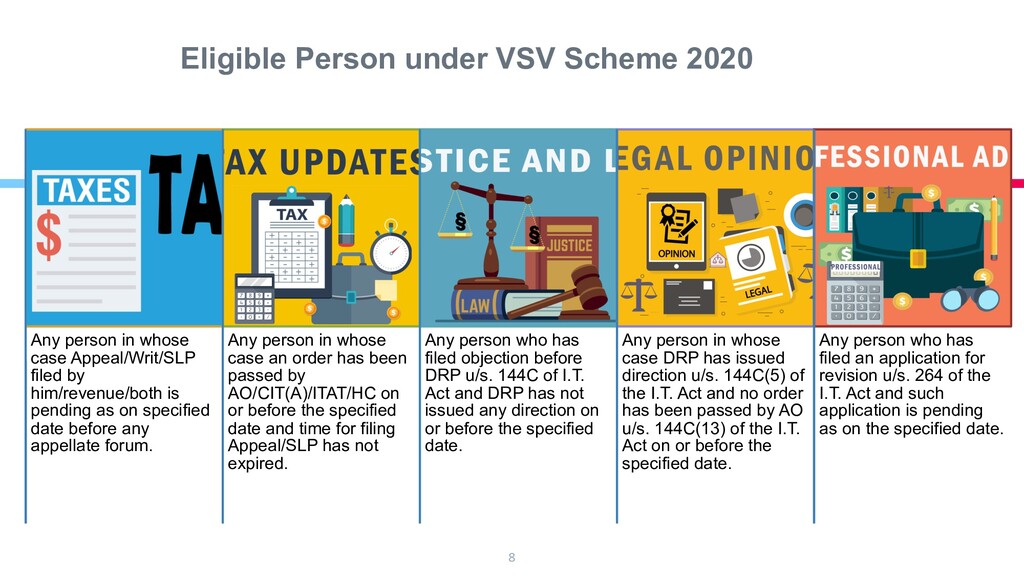

To know more:https://itatorders.in/blog/eligible-person-under-vivad-se-vishwas-scheme-2020/

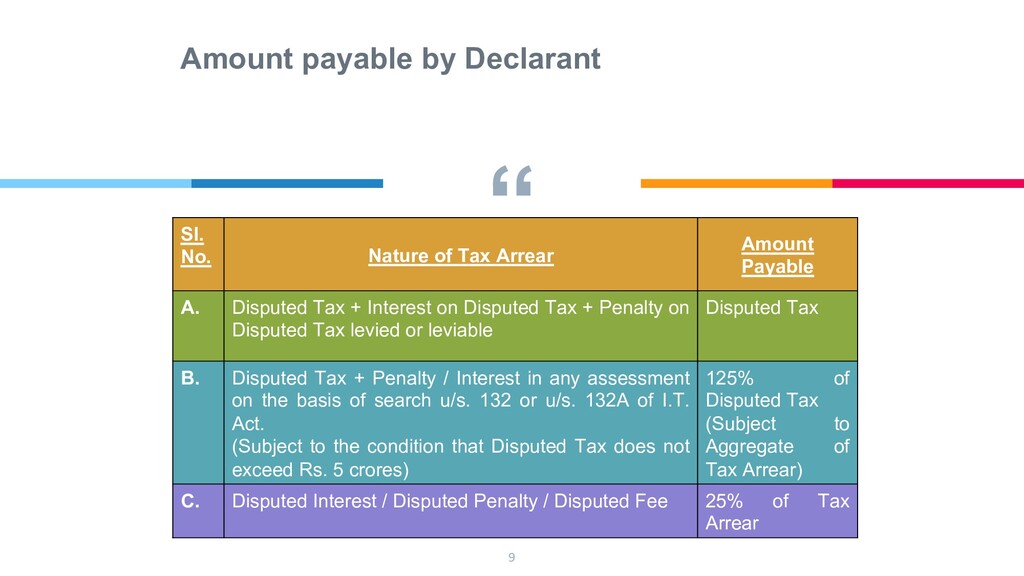

Get consultation under the VSV scheme and calculate your taxes: https://www.itatorders.in/vsvcalculator

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}