この資料では、**現代ポートフォリオ理論(MPT)**を基礎から分かりやすく解説し、投資においてリスクを抑えながら効率的にリターンを得る方法を紹介します。

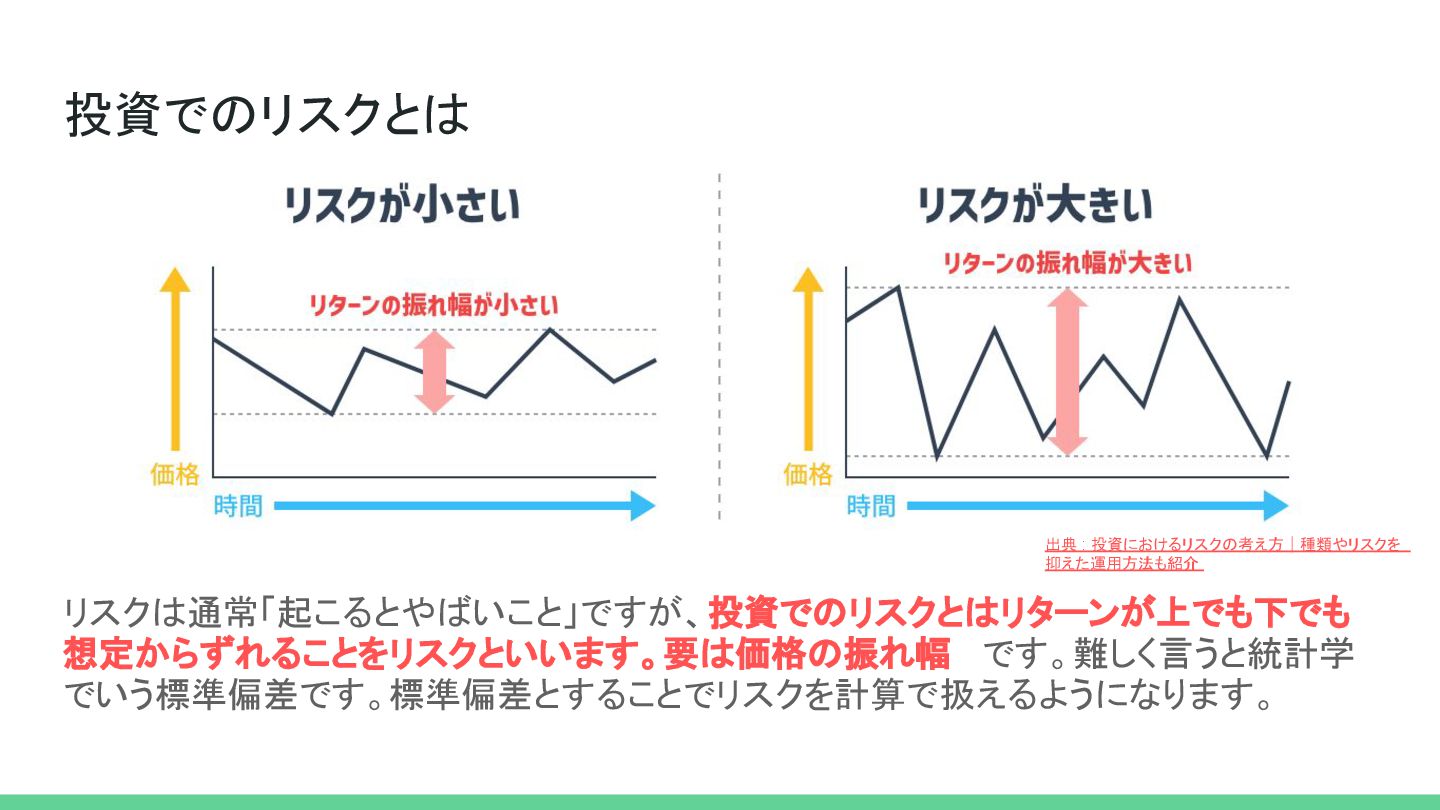

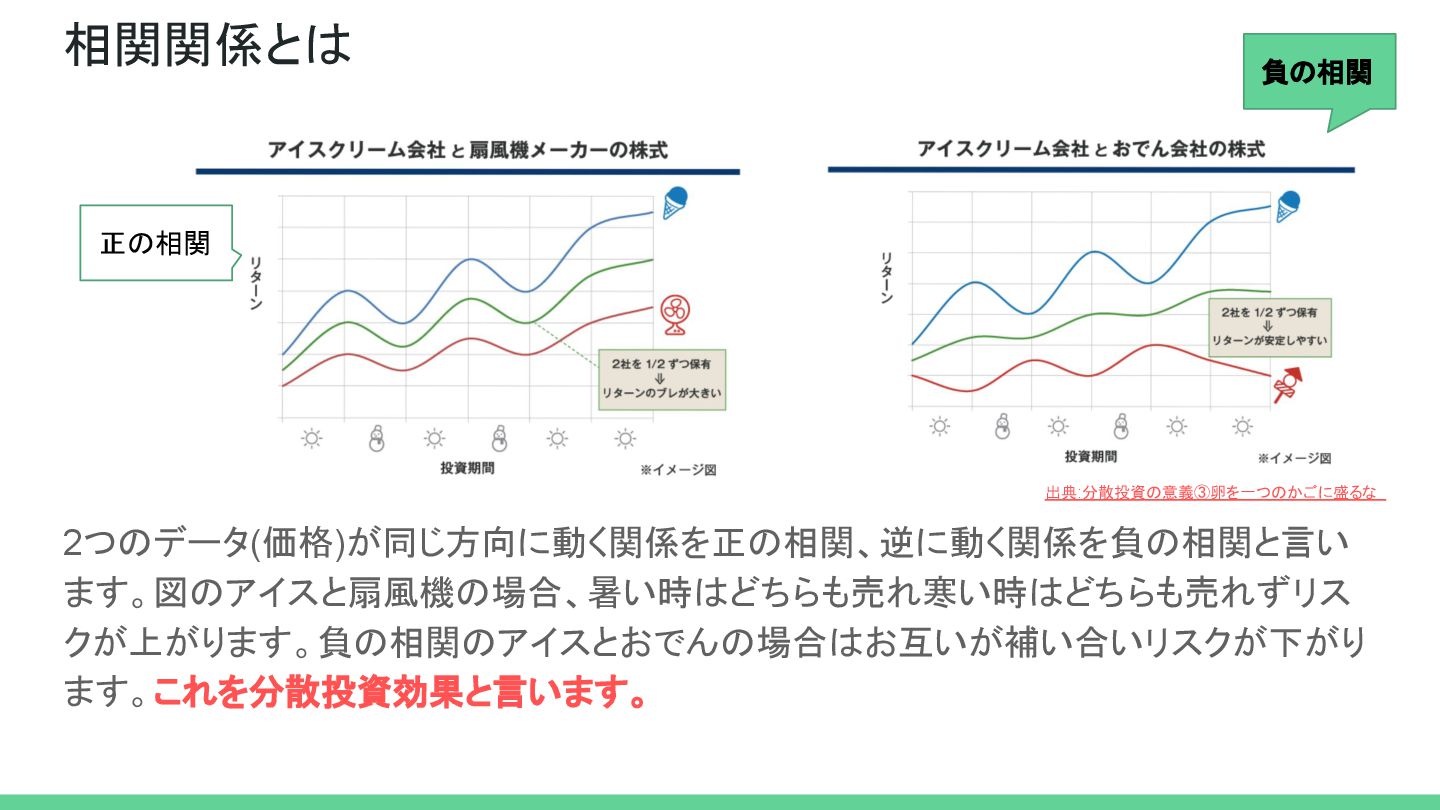

まず、投資での「リスク」とは何か、そして複数資産の値動きの関係(相関)が分散投資にどのように役立つかを説明します。次に、MPTが示す「効率的フロンティア」によって、最適なリスク・リターンの組み合わせを視覚的に理解します。

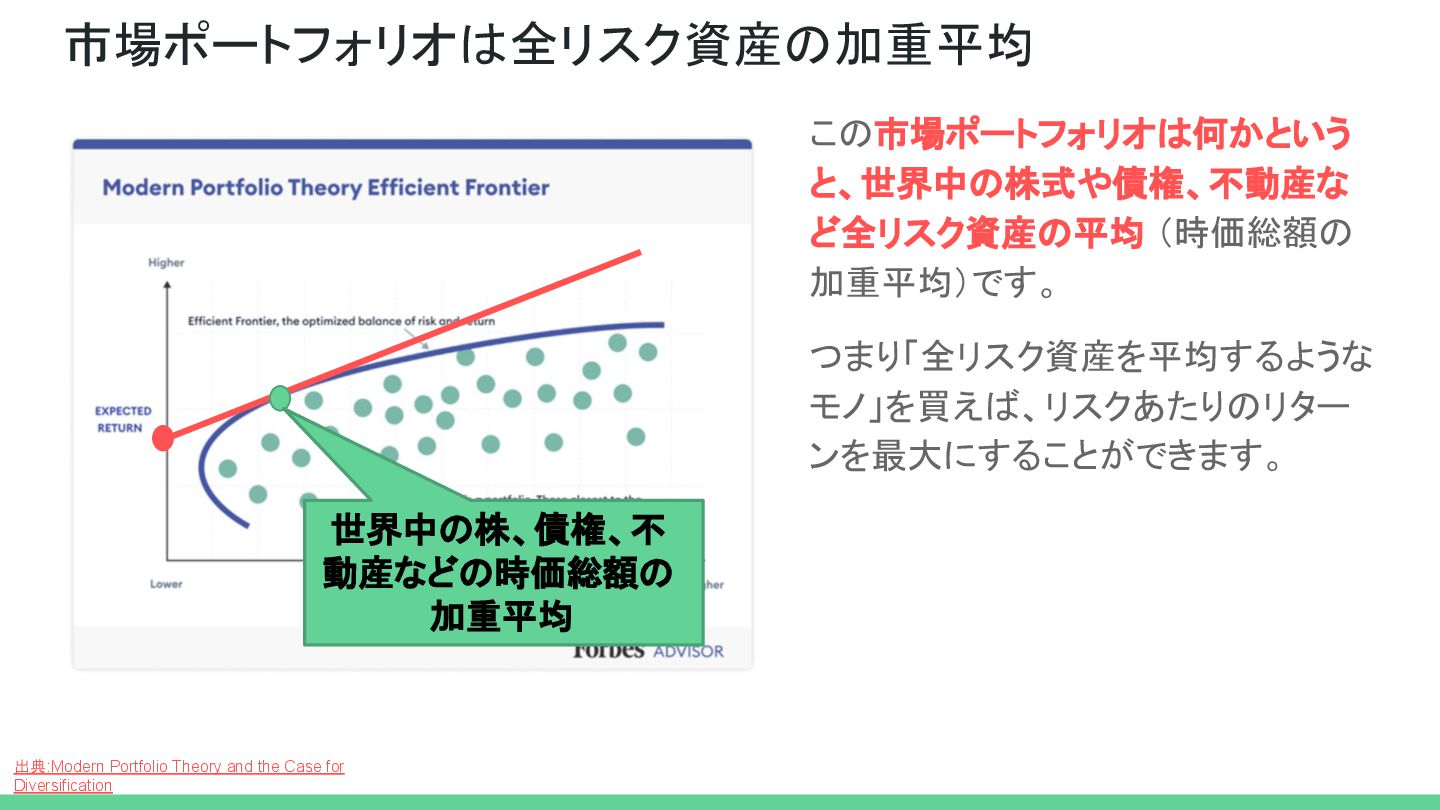

さらに、無リスク資産と効率的フロンティアの接点から導かれる**資本市場線(CML)と接点ポートフォリオ(市場ポートフォリオ)**を紹介し、理論的に最も効率的なポートフォリオとは何かを解説します。

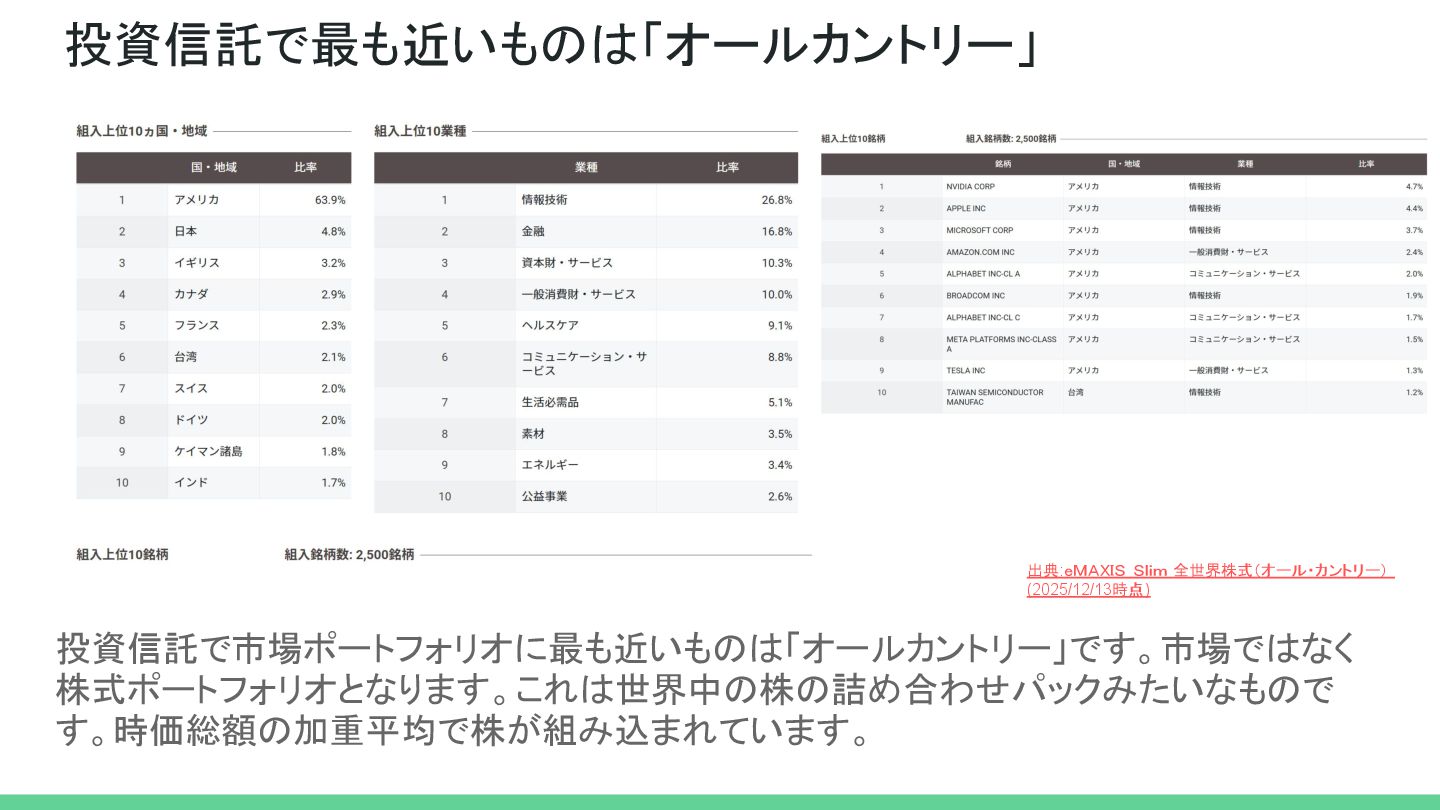

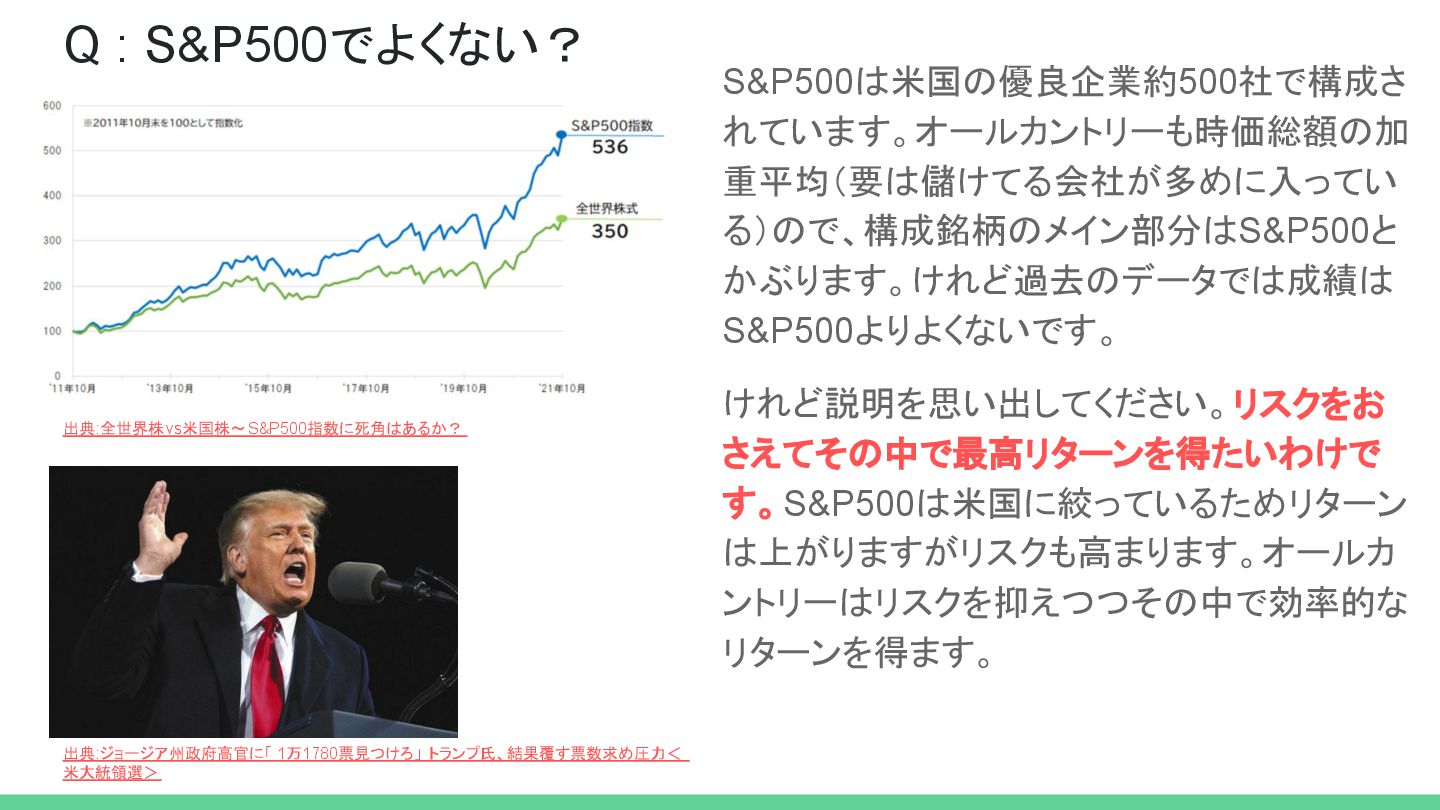

最後に、市場ポートフォリオに近い投資商品として、時価総額加重型の**全世界株式(オールカントリー)**を取り上げ、S&P500との違いや選択のポイントも説明します。

This document provides an accessible introduction to Modern Portfolio Theory (MPT) and explains how investors can achieve efficient returns while minimizing risk.

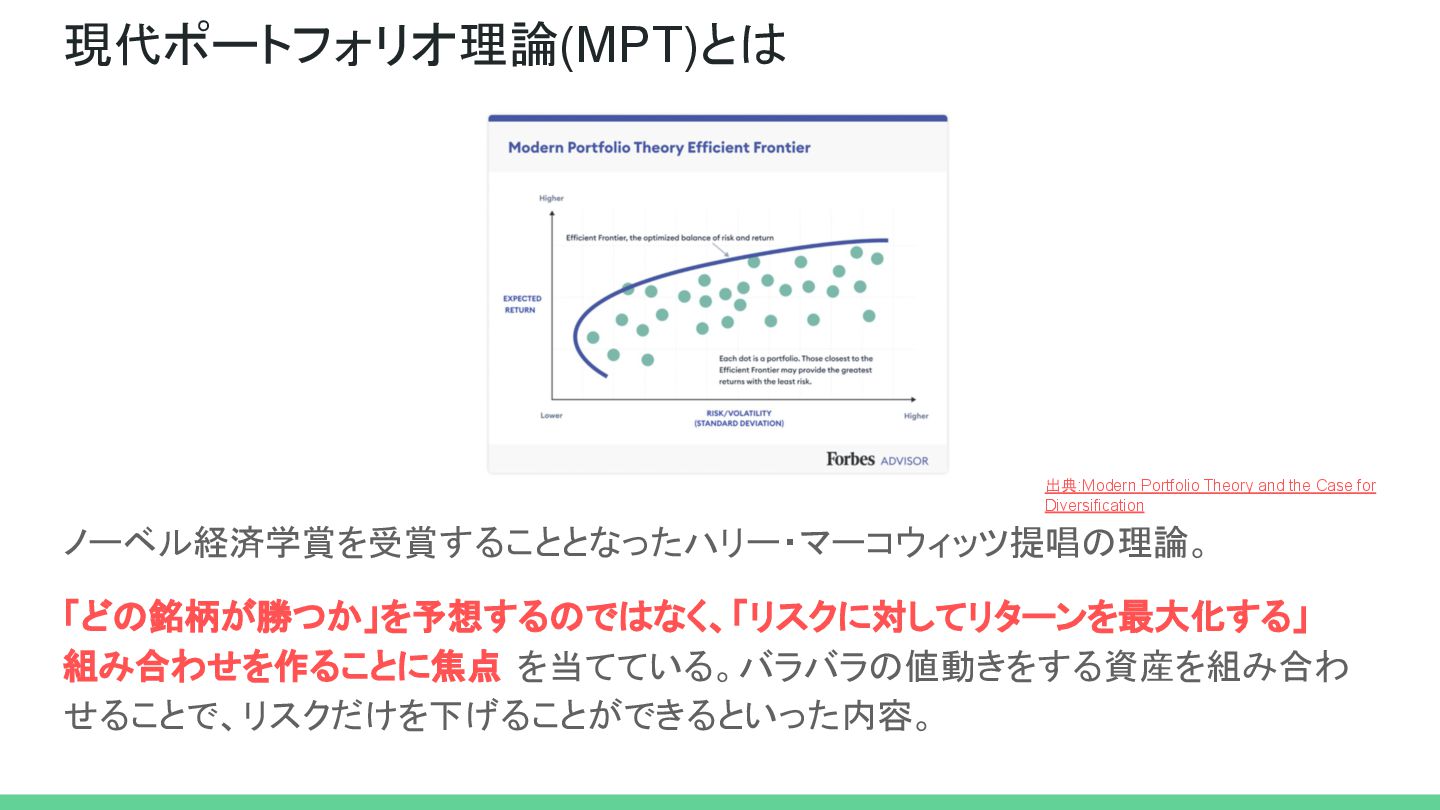

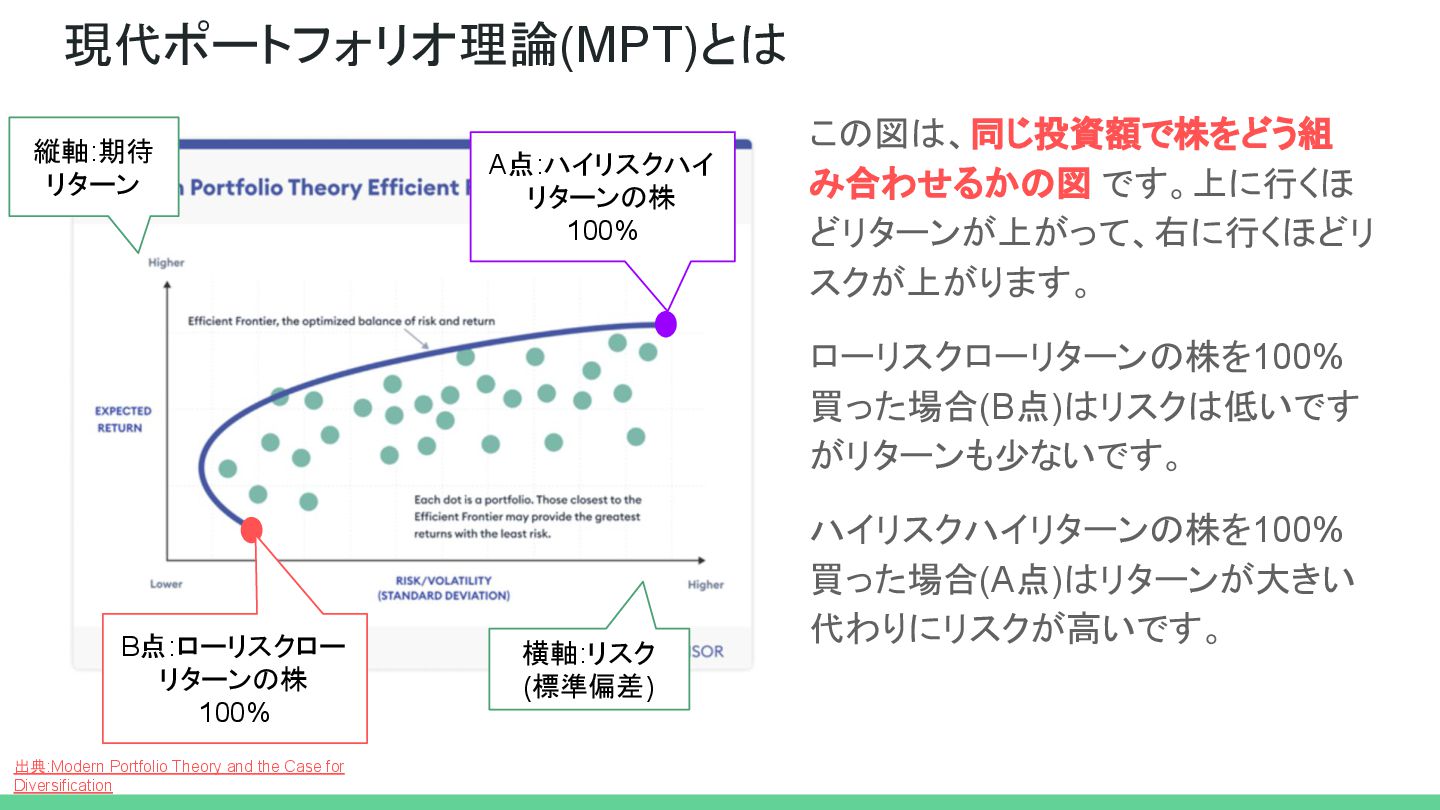

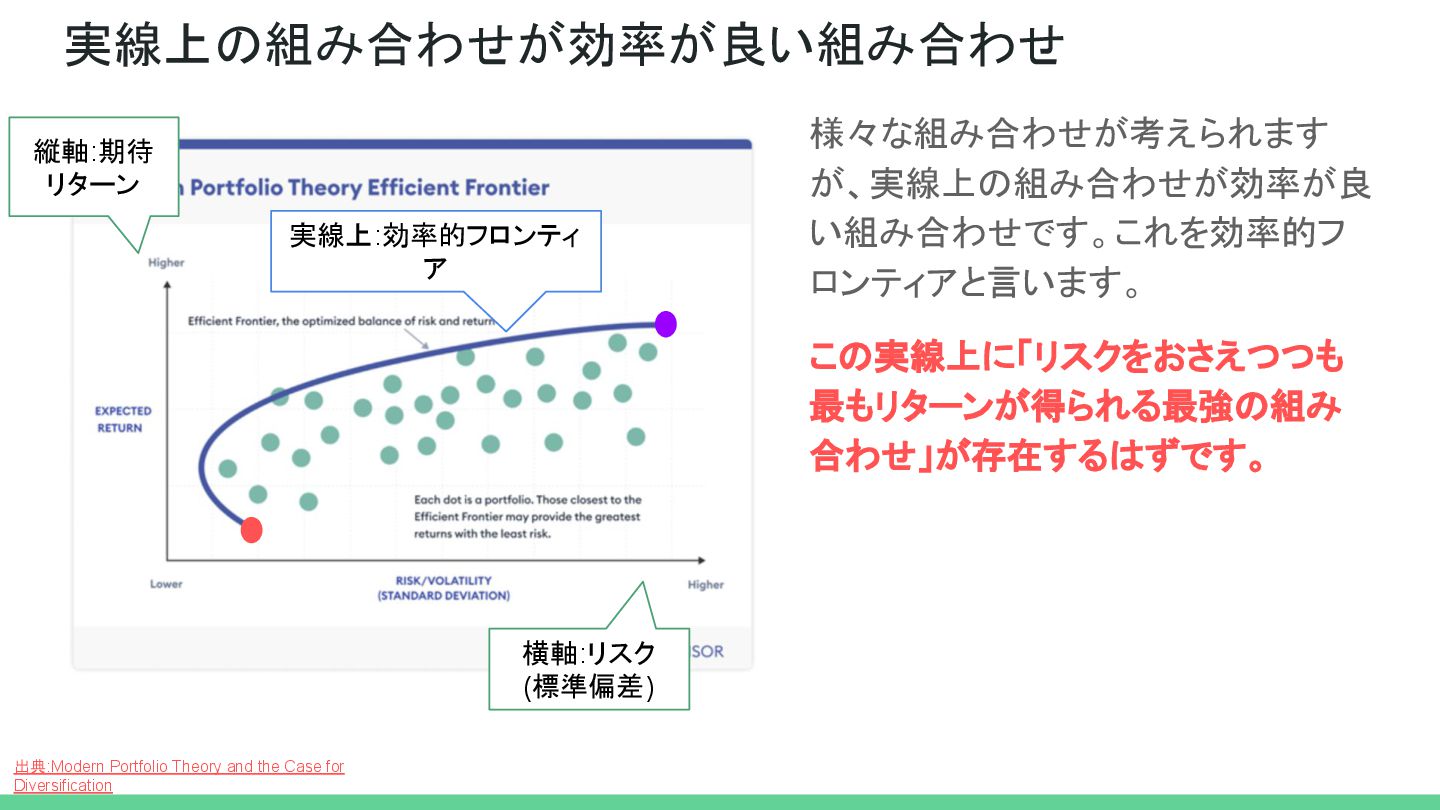

It begins by defining investment “risk” and illustrating how the correlation between different assets plays a key role in diversification. The concept of the Efficient Frontier is then introduced to show the optimal combinations of risk and return.

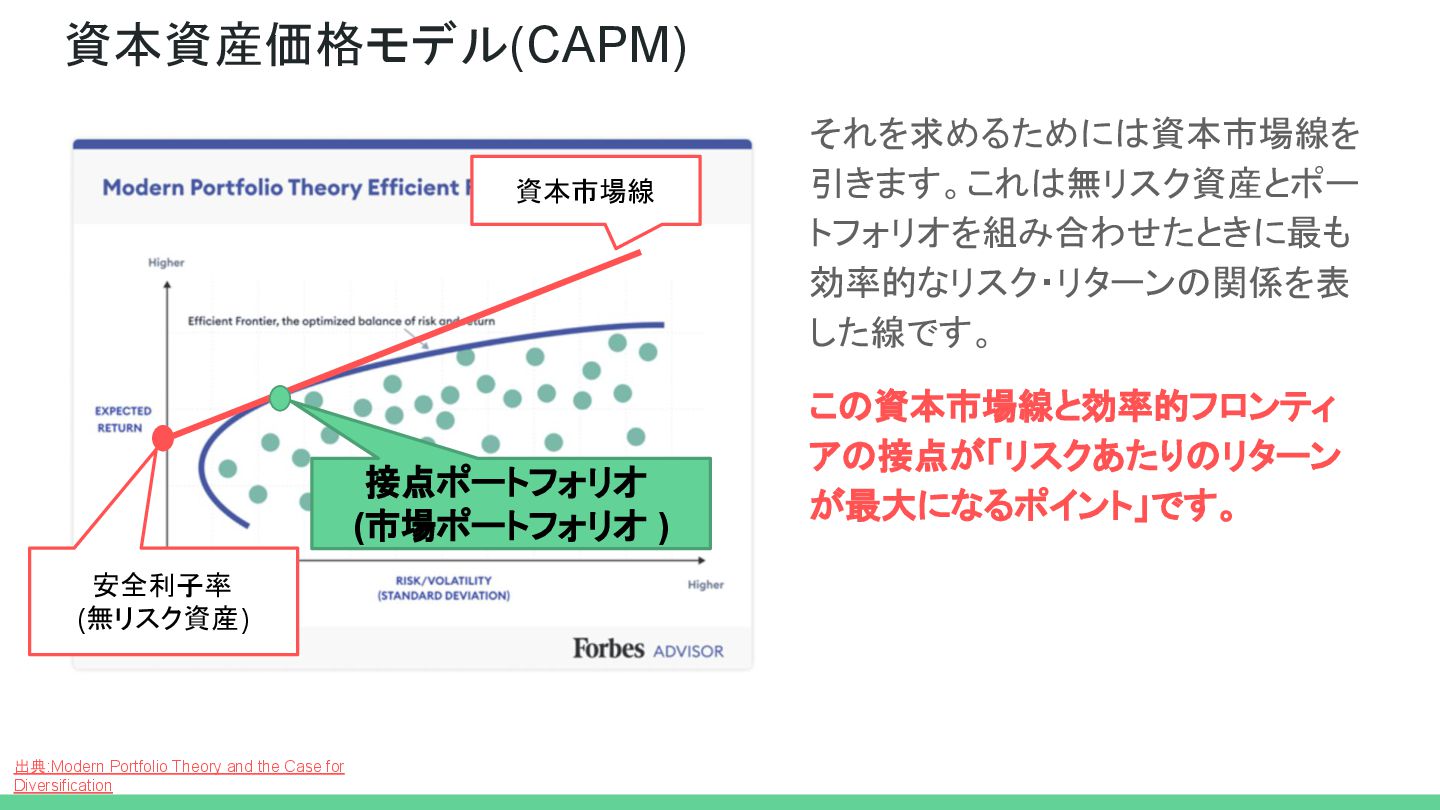

The document further explains the Capital Market Line (CML) and the Tangency Portfolio (Market Portfolio), which represent the theoretically most efficient portfolio obtained by combining risk-free assets with risky assets.

Finally, it highlights global equity index funds—particularly market-cap–weighted “All Country” funds—as practical investment vehicles that closely approximate the theoretical market portfolio, and compares them with the S&P 500 to clarify their different risk–return characteristics.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}