and Adjustment: Sustainable Advantage Through Higher Network Volumes Robert Friedman. Xinyi Liu. David Seibert. Ethan Protas. William Butler. Katherine Kim. Nir Levy. Robert Friedman. Xinyi Liu. David Seibert. Ethan Protas. William Butler. Katherine Kim. Nir Levy.

Merchant engagement and terminalization. - Consumer awareness. - Ease of consumer adoption. - Breadth of compelling services. “ ” March 2012, “Commercial Launch of Mobile Payments Using NFC Enabled Phones” James Anderson, SVP Mobile Product Development

transaction volumes. √ Low Switching Costs - Easy account termination - High of availability of near perfect substitutes: + Debit, credit, and prepaid offerings of other financial institutions, e-commerce √ Imperfect Substitutes - Cash and check - 86% of current transactions √ Concentrated Industry - Consolidations and vertical integration by banks - 4 main competing companies hold 99% of purchase transaction market share WtP - Price - Costs - Industry profitability is directly driven by consumer spending. 86% 14% Paper Payments Electronic Payments

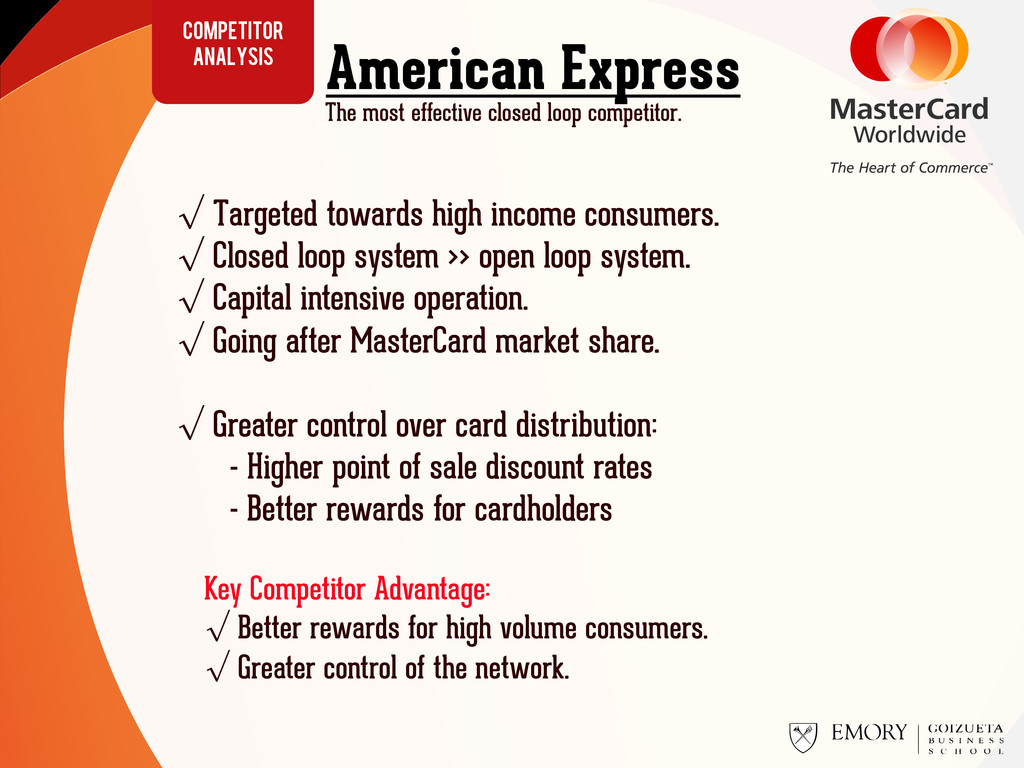

>> open loop system. √ Capital intensive operation. √ Going after MasterCard market share. √ Greater control over card distribution: - Higher point of sale discount rates - Better rewards for cardholders American Express COMPETITOR ANALYSIS Key Competitor Advantage: √ Better rewards for high volume consumers. √ Greater control of the network. The most effective closed loop competitor.

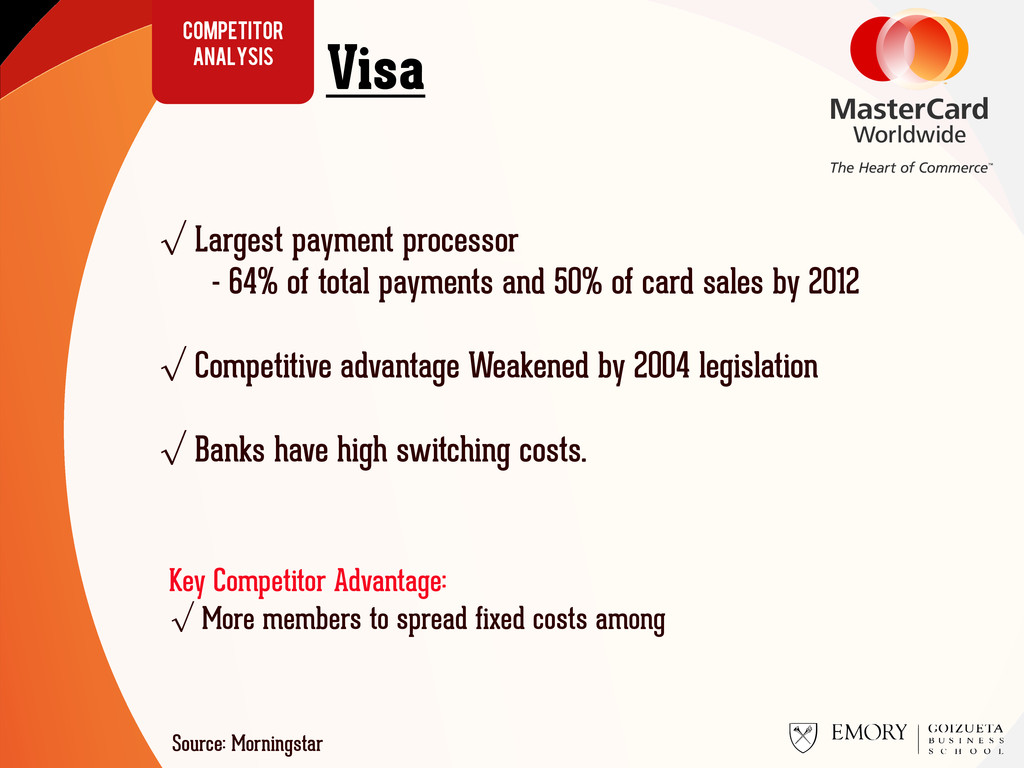

50% of card sales by 2012 √ Competitive advantage Weakened by 2004 legislation √ Banks have high switching costs. Visa COMPETITOR ANALYSIS Key Competitor Advantage: √ More members to spread fixed costs among Source: Morningstar

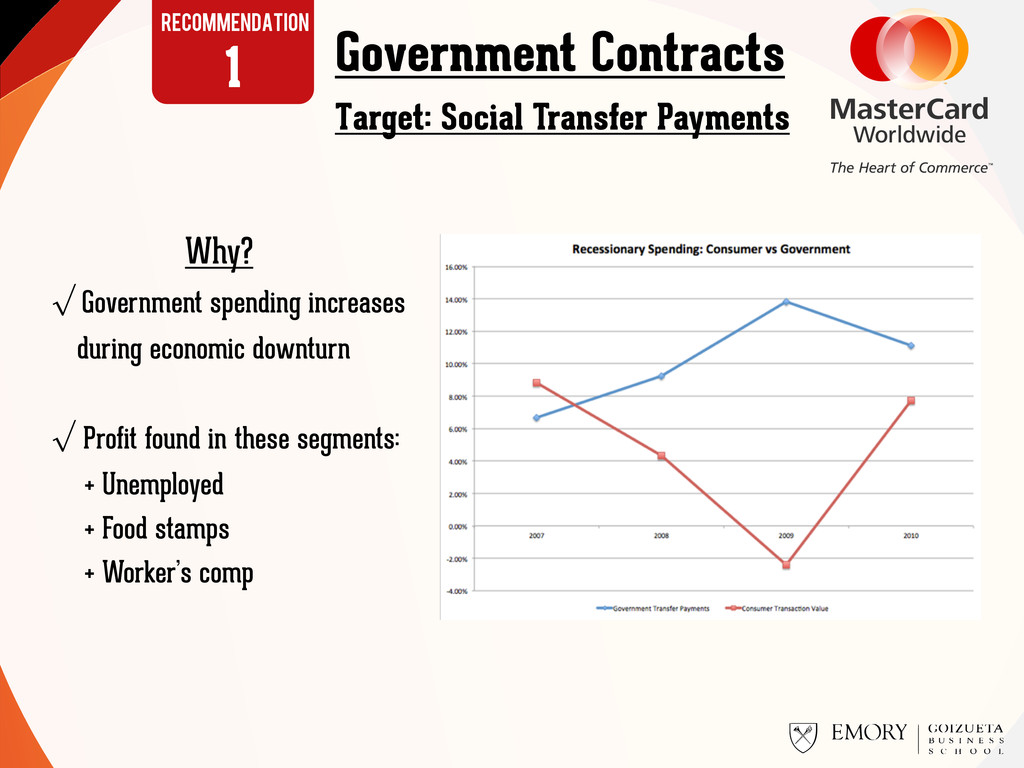

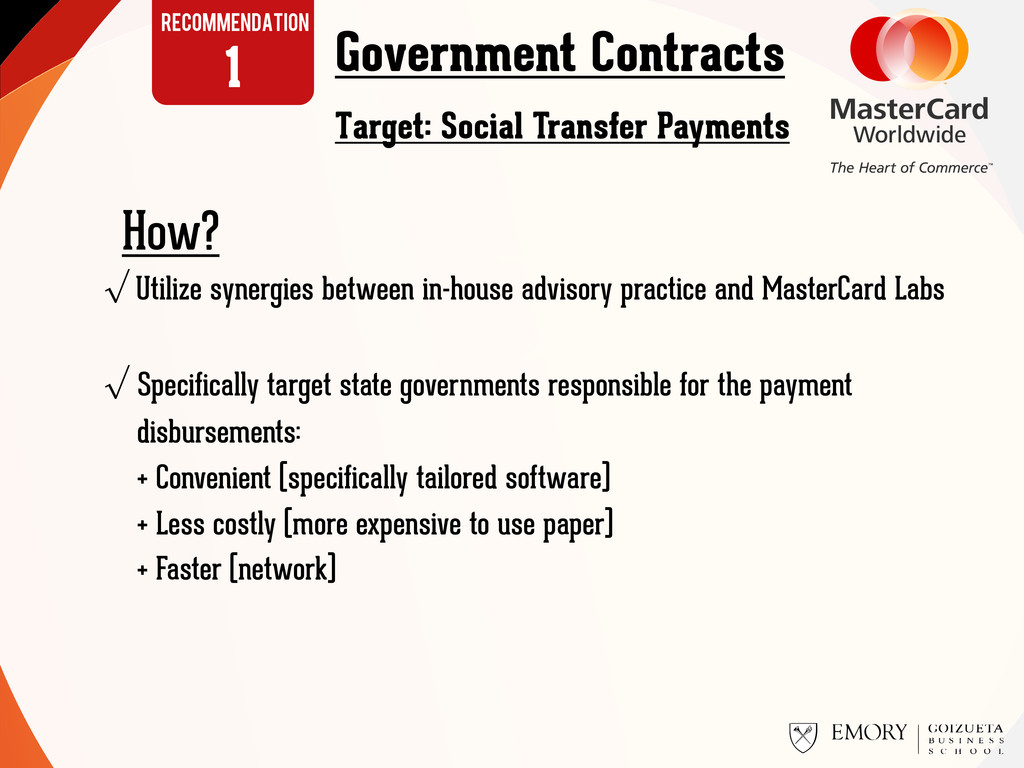

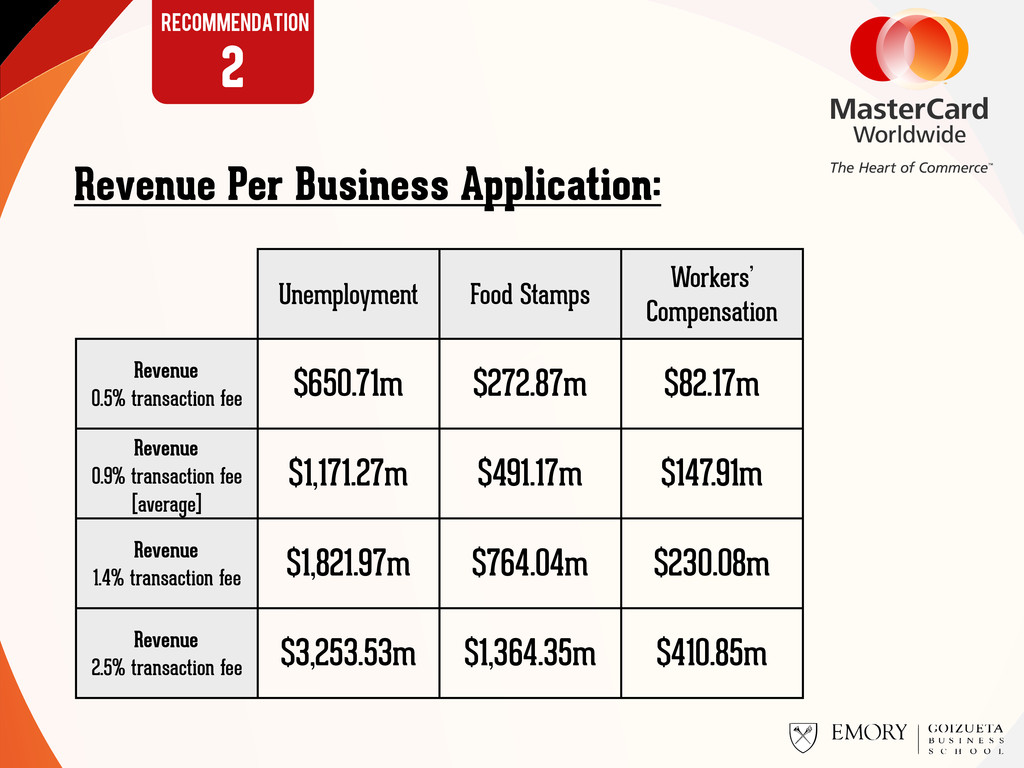

practice and MasterCard Labs √ Specifically target state governments responsible for the payment disbursements: + Convenient (specifically tailored software) + Less costly (more expensive to use paper) + Faster (network) Target: Social Transfer Payments How?

new Paypass card upgrades to existing card holders. Prioritize specific merchants: √ High volume traffic √ Exhibits benefits to consumers (convenience & time) Develop long term sustainable advantages: √ Exclusive contracts with merchants until 2015. √ Network effects- catch Visa off guard 2 recommendation $200/terminal 200k terminals

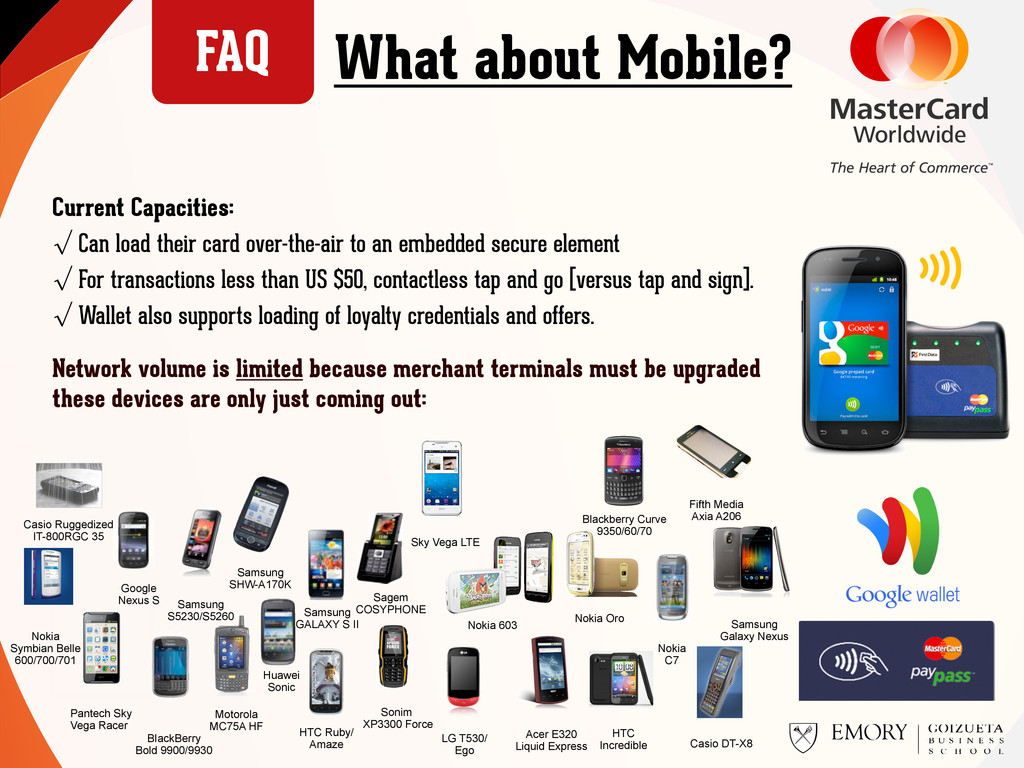

S5230/S5260 Nokia C7 Samsung SHW-A170K Pantech Sky Vega Racer Motorola MC75A HF Casio Ruggedized IT-800RGC 35 BIackBerry Bold 9900/9930 Nokia Symbian Belle 600/700/701 HTC Ruby/ Amaze Sonim XP3300 Force LG T530/ Ego Casio DT-X8 HTC Incredible Samsung Galaxy Nexus Huawei Sonic Blackberry Curve 9350/60/70 Nokia Oro Acer E320 Liquid Express Nokia 603 Sky Vega LTE Fifth Media Axia A206 Current Capacities: √ Can load their card over-the-air to an embedded secure element √ For transactions less than US $50, contactless tap and go [versus tap and sign]. √ Wallet also supports loading of loyalty credentials and offers. Network volume is limited because merchant terminals must be upgraded these devices are only just coming out: What about Mobile? FAQ

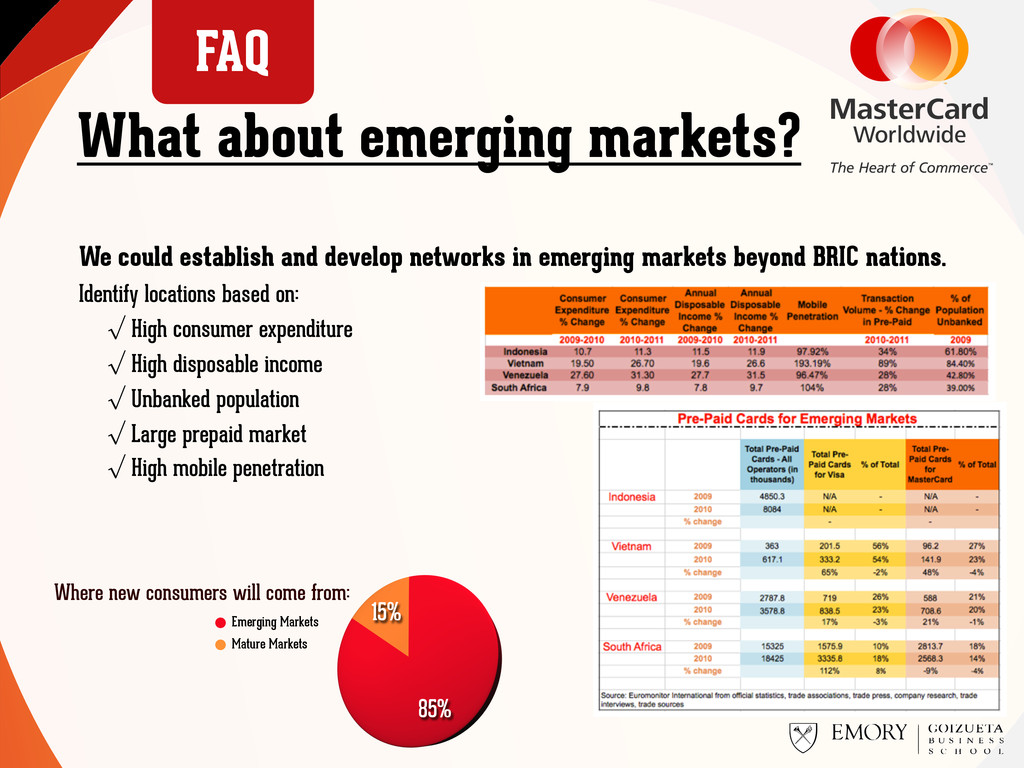

come from: We could establish and develop networks in emerging markets beyond BRIC nations. Identify locations based on: √ High consumer expenditure √ High disposable income √ Unbanked population √ Large prepaid market √ High mobile penetration What about emerging markets? FAQ

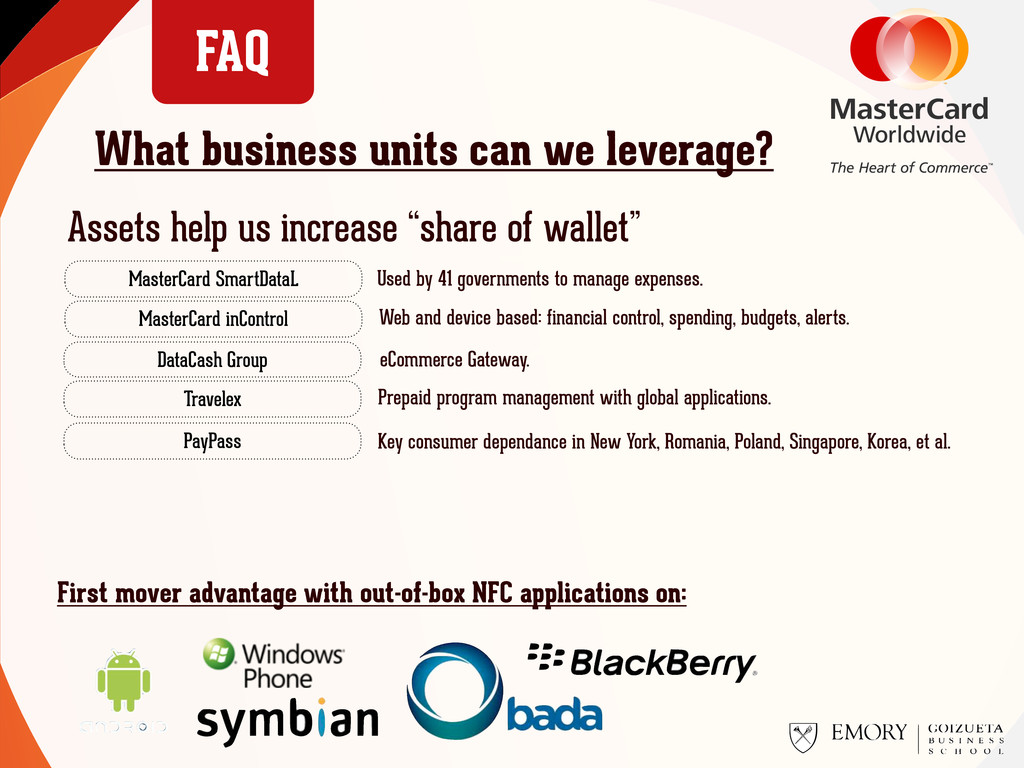

we leverage? Assets help us increase “share of wallet” Used by 41 governments to manage expenses. Web and device based: financial control, spending, budgets, alerts. eCommerce Gateway. Travelex Prepaid program management with global applications. PayPass Key consumer dependance in New York, Romania, Poland, Singapore, Korea, et al. First mover advantage with out-of-box NFC applications on: FAQ

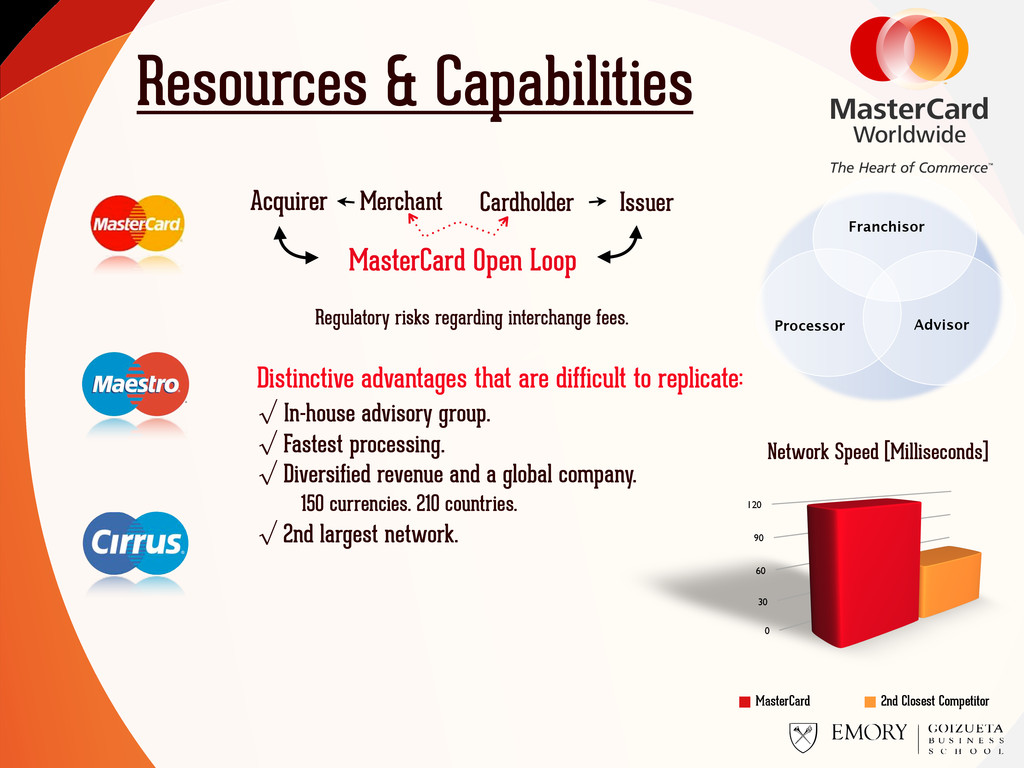

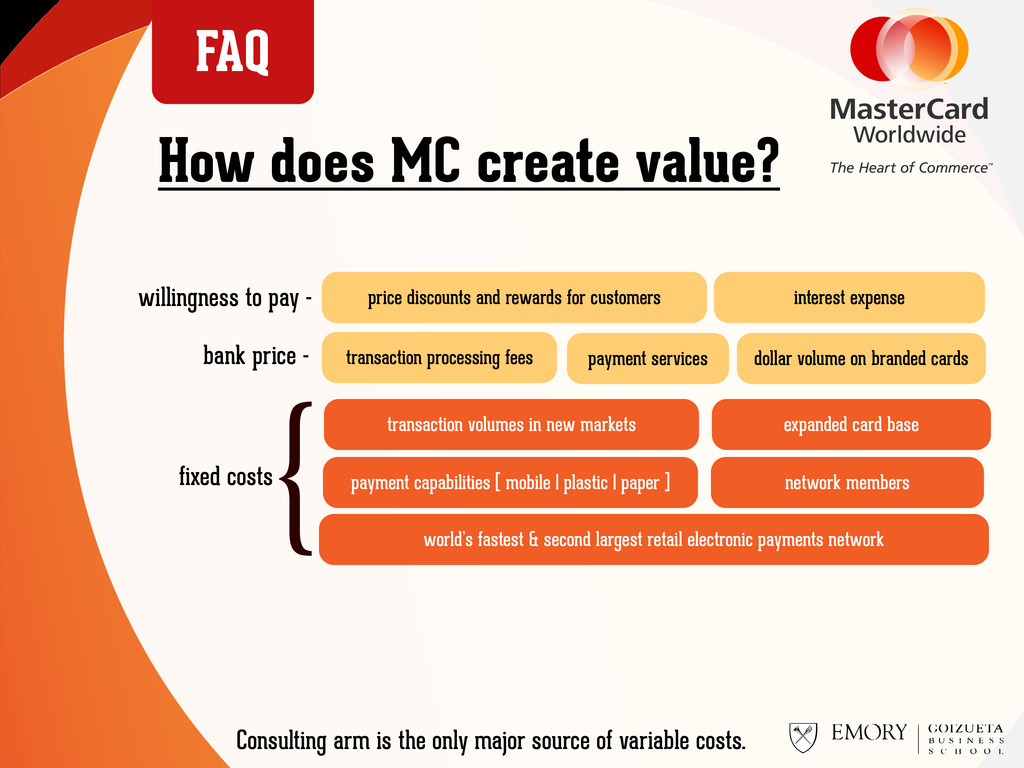

processing fees payment services dollar volume on branded cards transaction volumes in new markets expanded card base price discounts and rewards for customers payment capabilities [ mobile | plastic | paper ] network members willingness to pay - bank price - fixed costs { interest expense Consulting arm is the only major source of variable costs. FAQ How does MC create value?

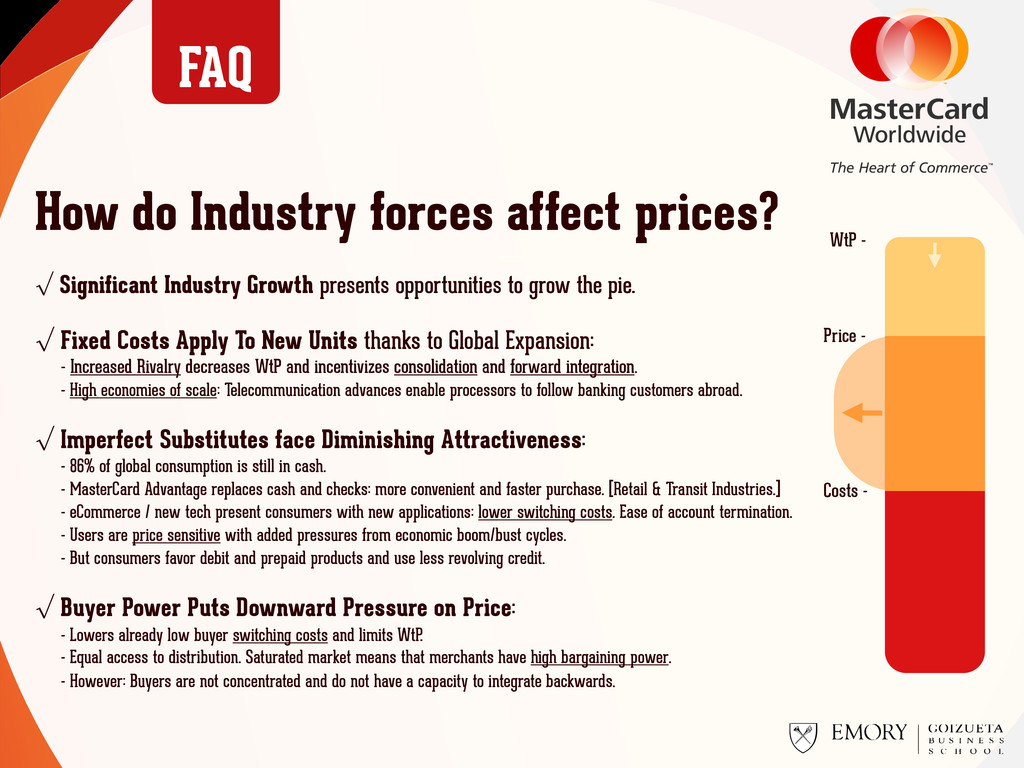

To New Units thanks to Global Expansion: - Increased Rivalry decreases WtP and incentivizes consolidation and forward integration. - High economies of scale: Telecommunication advances enable processors to follow banking customers abroad. √ Imperfect Substitutes face Diminishing Attractiveness: - 86% of global consumption is still in cash. - MasterCard Advantage replaces cash and checks: more convenient and faster purchase. [Retail & Transit Industries.] - eCommerce / new tech present consumers with new applications: lower switching costs. Ease of account termination. - Users are price sensitive with added pressures from economic boom/bust cycles. - But consumers favor debit and prepaid products and use less revolving credit. √ Buyer Power Puts Downward Pressure on Price: - Lowers already low buyer switching costs and limits WtP. - Equal access to distribution. Saturated market means that merchants have high bargaining power. - However: Buyers are not concentrated and do not have a capacity to integrate backwards. WtP - Price - Costs - √ Significant Industry Growth presents opportunities to grow the pie. FAQ

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}