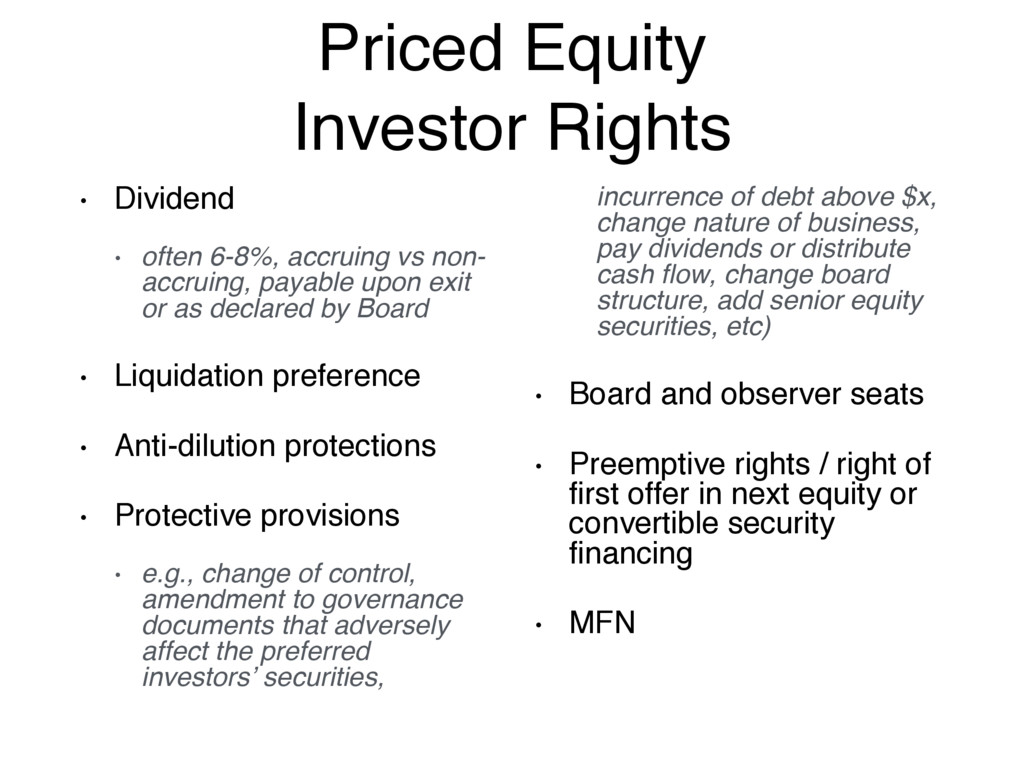

vs non- accruing, payable upon exit or as declared by Board • Liquidation preference • Anti-dilution protections • Protective provisions • e.g., change of control, amendment to governance documents that adversely affect the preferred investors’ securities, incurrence of debt above $x, change nature of business, pay dividends or distribute cash flow, change board structure, add senior equity securities, etc) • Board and observer seats • Preemptive rights / right of first offer in next equity or convertible security financing • MFN

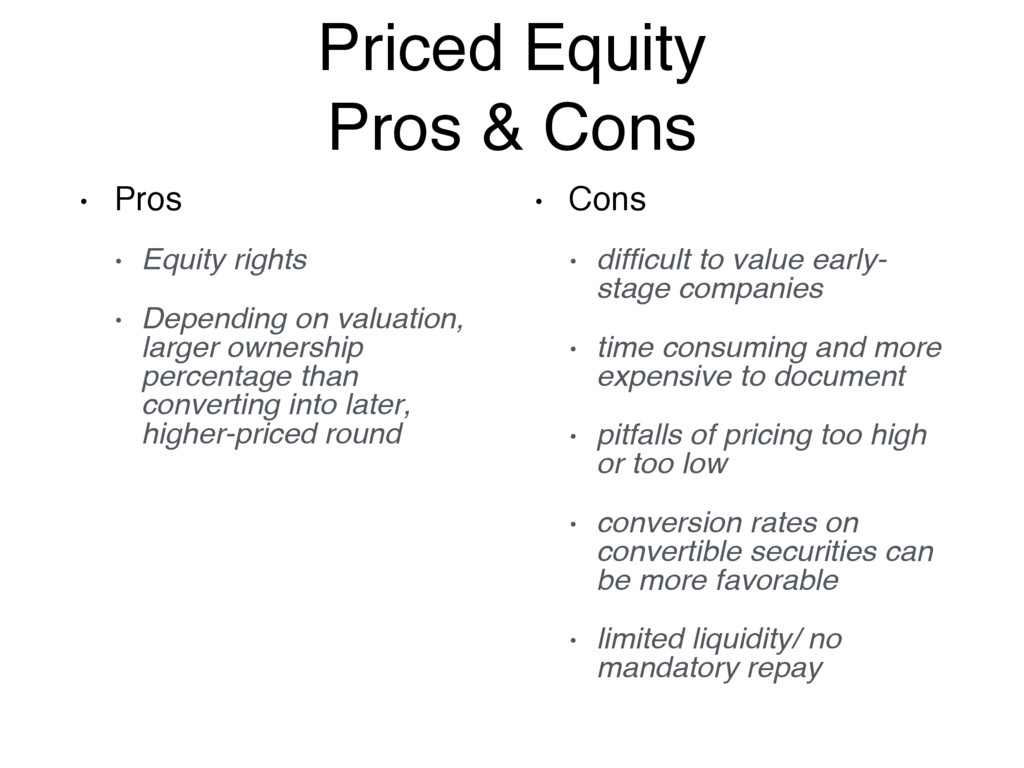

• Depending on valuation, larger ownership percentage than converting into later, higher-priced round • Cons • difficult to value early- stage companies • time consuming and more expensive to document • pitfalls of pricing too high or too low • conversion rates on convertible securities can be more favorable • limited liquidity/ no mandatory repay

• Interest rate (8%) • Term (12 – 18 months) • Discount (20%) – used instead of warrants these days • Conversion features • Conversion Cap • Liquidation Pref if early acquisition • Pre-negotiated common stock valuation at maturity

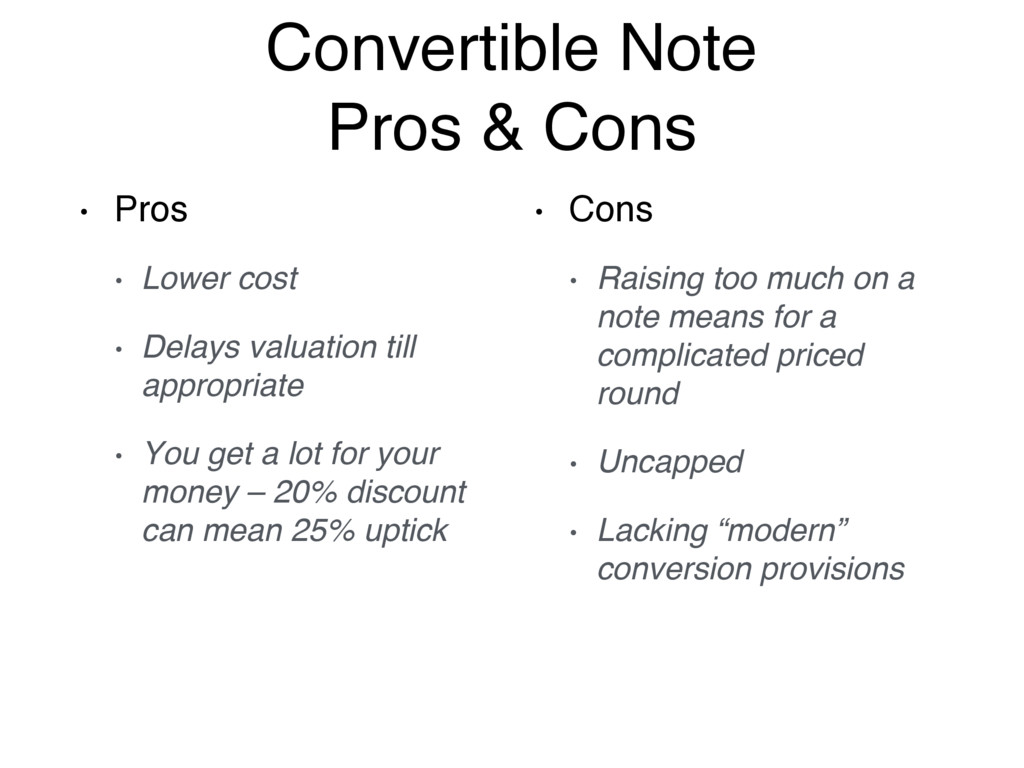

• Delays valuation till appropriate • You get a lot for your money – 20% discount can mean 25% uptick • Cons • Raising too much on a note means for a complicated priced round • Uncapped • Lacking “modern” conversion provisions

— Simple Agreement for Future Equity — as a replacement for Convertible Notes • Announced December 2013, created by YC partner Carolynn Levy, who also wrote the Series AA docs with Wilson Sonsini in 2008 • Designed to fix issues with convertible notes being debt, and regulations around debt, such as fixed term and market interest rates

financing in a short period • Relatively frothy environment — Demo Day, guaranteed matching funds, and other investor interest meant relatively little worry about closing a next financing in 3 - 6 months • Deals getting done on a handshake where the main question is amount of investment, not any other negotiation

inexpensive • Founder friendly • Low complexity makes it good for friends & family rounds • No liability on company books • Cons • Investors outside of SF unfamiliar with them • Limited investor rights • Open ended deal – no maturity date, no leverage

gets paid pack • Designed for founders that don’t (initially) want to go down the VC route • Cash distribution from revenue capped at 3x max the initial investment • “Our return model anchors on distributions from cashflow, not on rocketship rides. Our interest is in giving founders more control over their company and culture, not less. We focus all of our energy on helping our companies accelerate profitable growth, not on raising their next round of funding.”

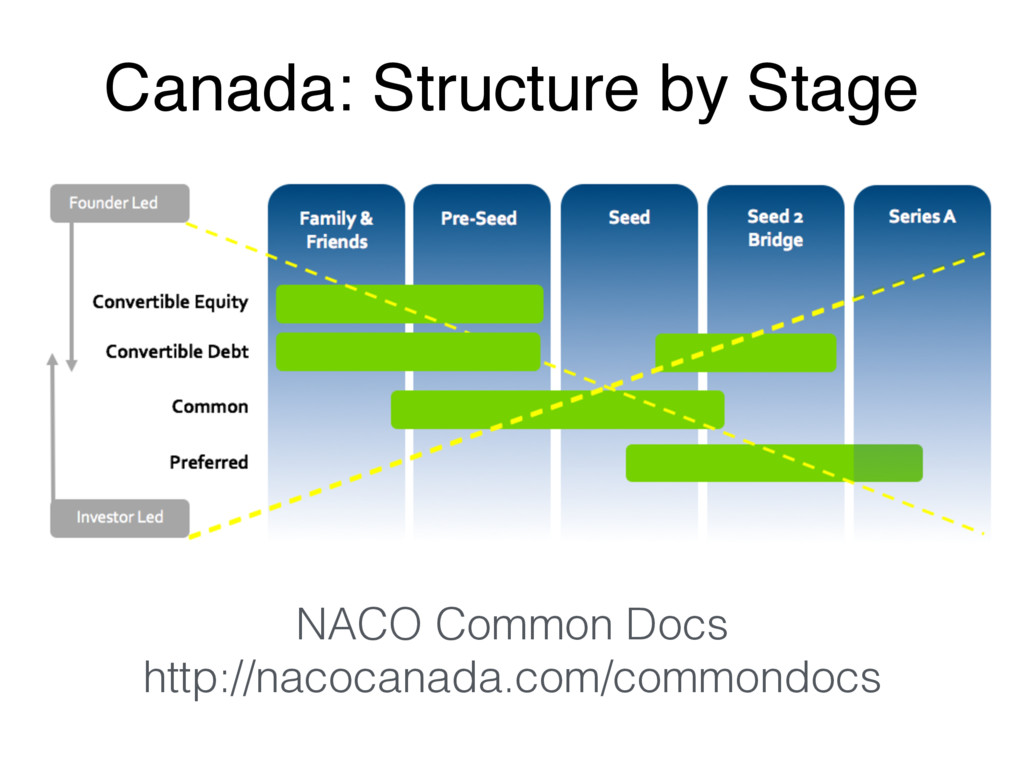

around early stage angel financing docs • If you search, you’ll find one MARS template, and lots of US sources • The Series Seed in the US were created in 2008 — Canada is roughly 10 years behind • Answering the question, what is common, what is market? | 16 NACO Common Docs

information, and place where people can ask questions • Term sheet templates, educational notes and case studies • Explainers • Resources • Frequently Asked Questions + community questions | 17 NACO Common Docs

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}