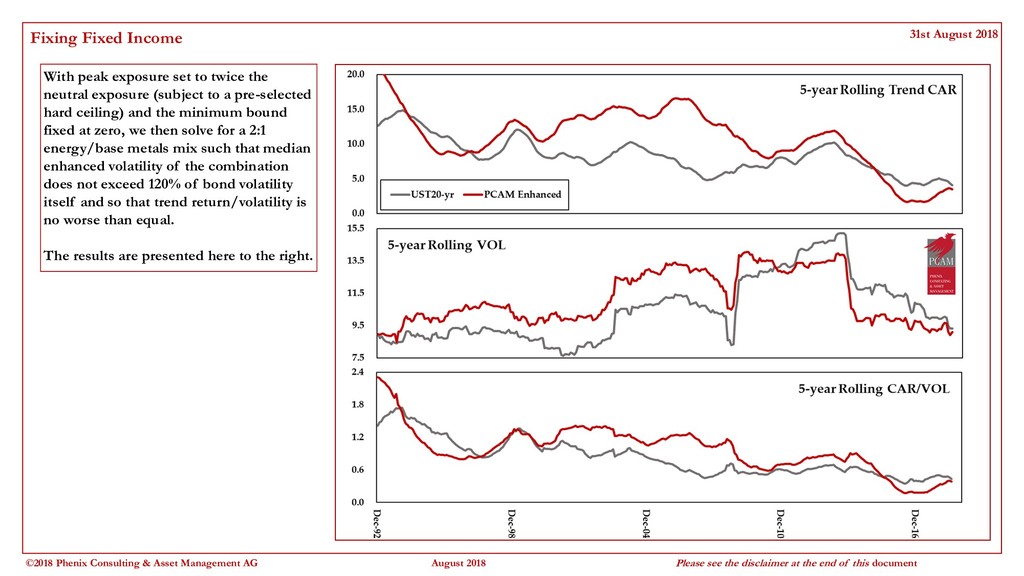

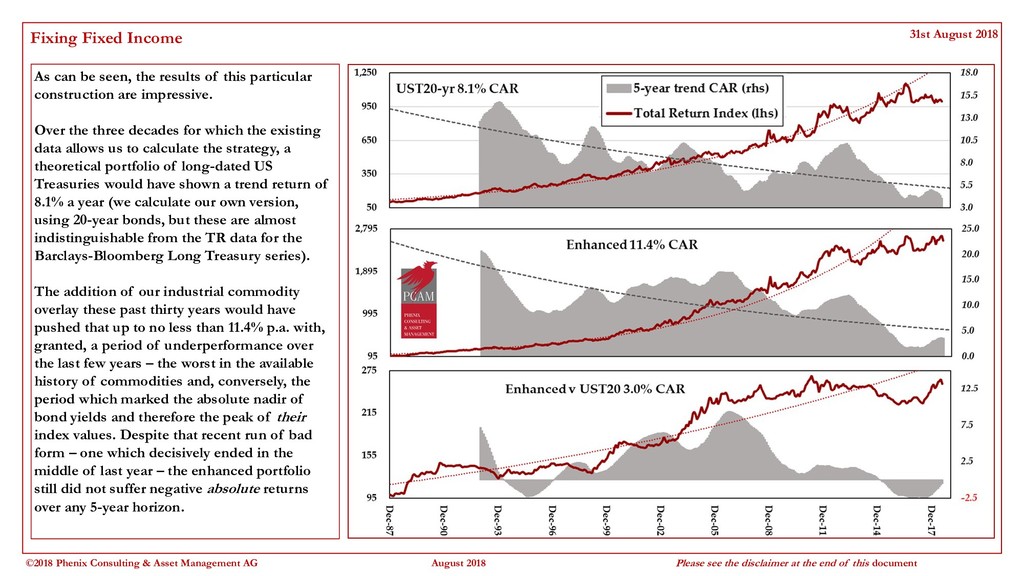

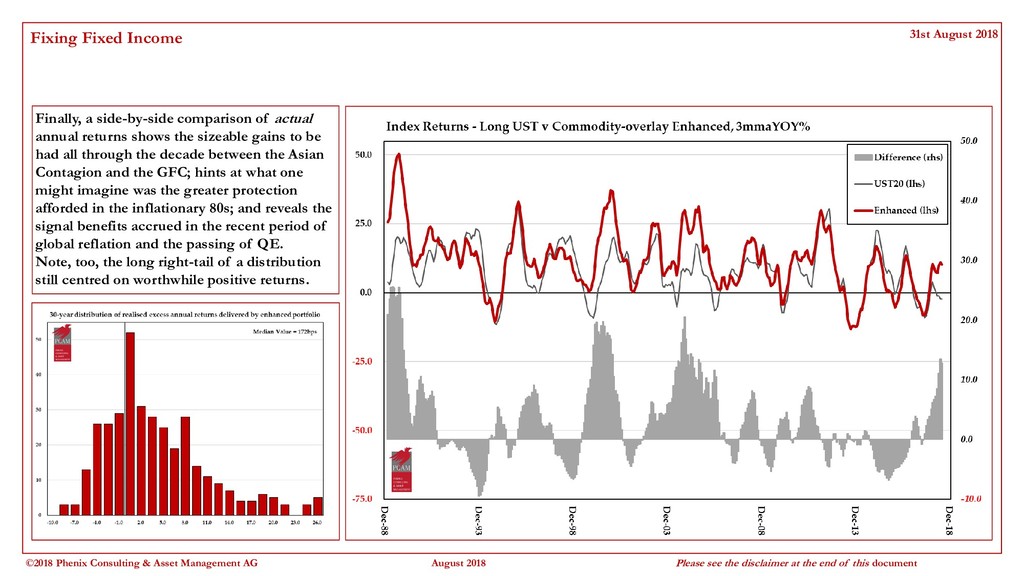

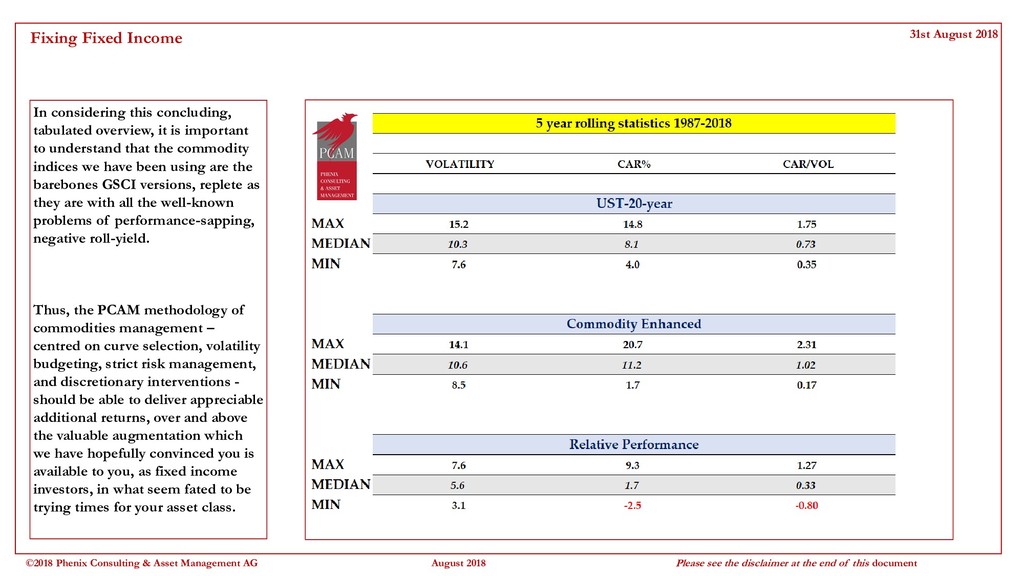

The true importance of commodities to an investor is their ability to insulate one's bond holdings from some of the more unfavourable influences upon them - notably a quickening of inflation and an acceleration in growth. Here, in outline, are the results of a detailed exploration of how the two may be dynamically combined to better ride the business cycle.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}