business The impact of sales is the profit at issue The variations can indicate assumptions need to be changed, or action may need to be taken (withdrawals, expenses, investments, reinsurance).

of New Business Impact of Reinsurance Profitability by Product Line, Demographic or Sales Office Profit is a collaborative effort Accessible Understood across organization Objectives and Goal Setting

with a substantial degree of approximations. Generally not divisible over time Approximations may not be understood Static – prevents analysis by product, sales office or demographic Different approaches by line of business

in later periods Illustrated with simple example Mortality as expected Withdrawals 50% of expected for 1st three quarters Expected values in Q4 based on artificial population

level reserves and earnings allows: knowledge discovery with regard to profitability and performance by product, sales office or client segment can lead to successful management action

expected rates For Analysis of EBS Product Structure and attributes Sales structure and attributes Client attributes Must be unitized to allow alternate aggregations

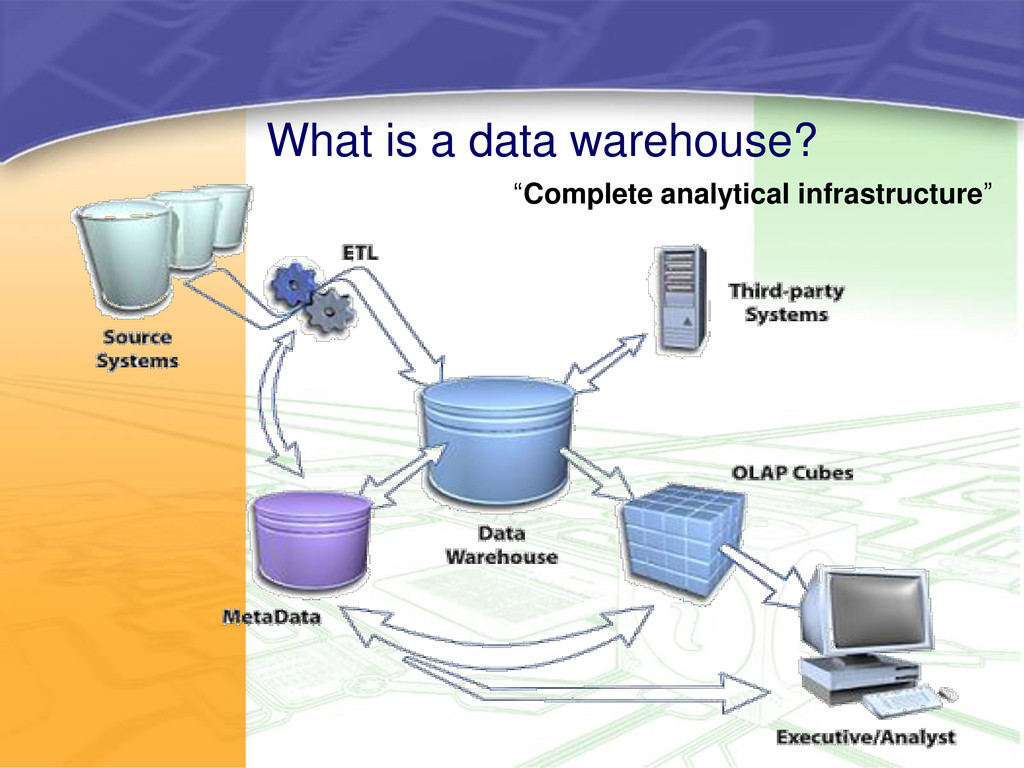

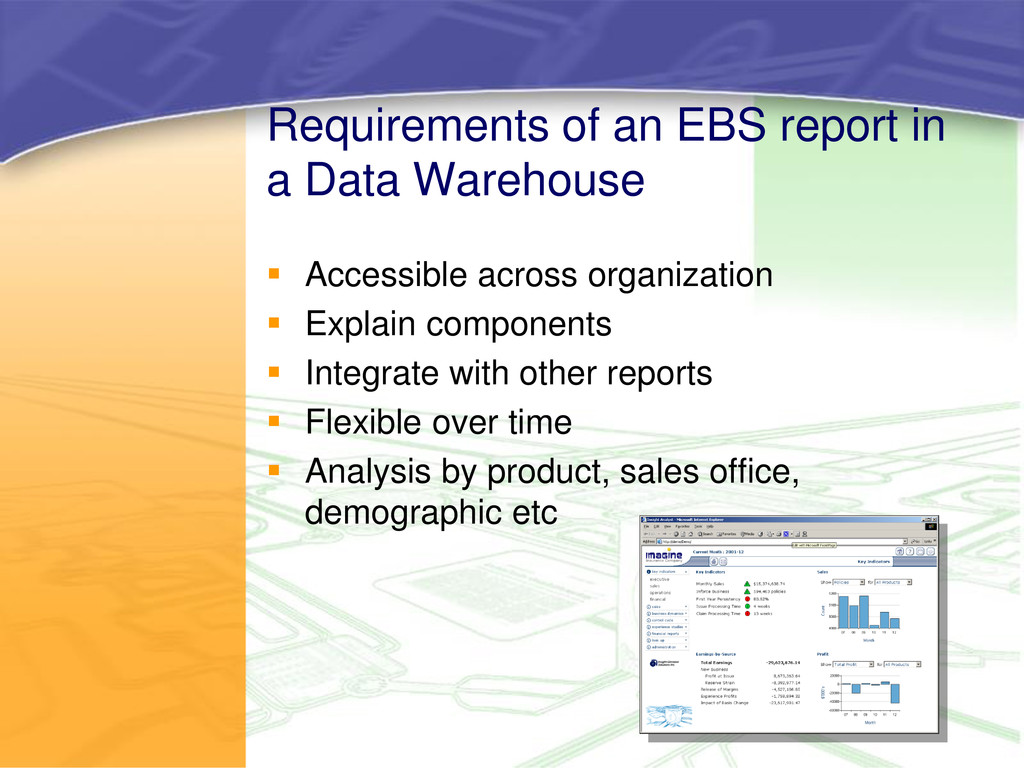

Accessible across organization Explain components Integrate with other reports Flexible over time Analysis by product, sales office, demographic etc

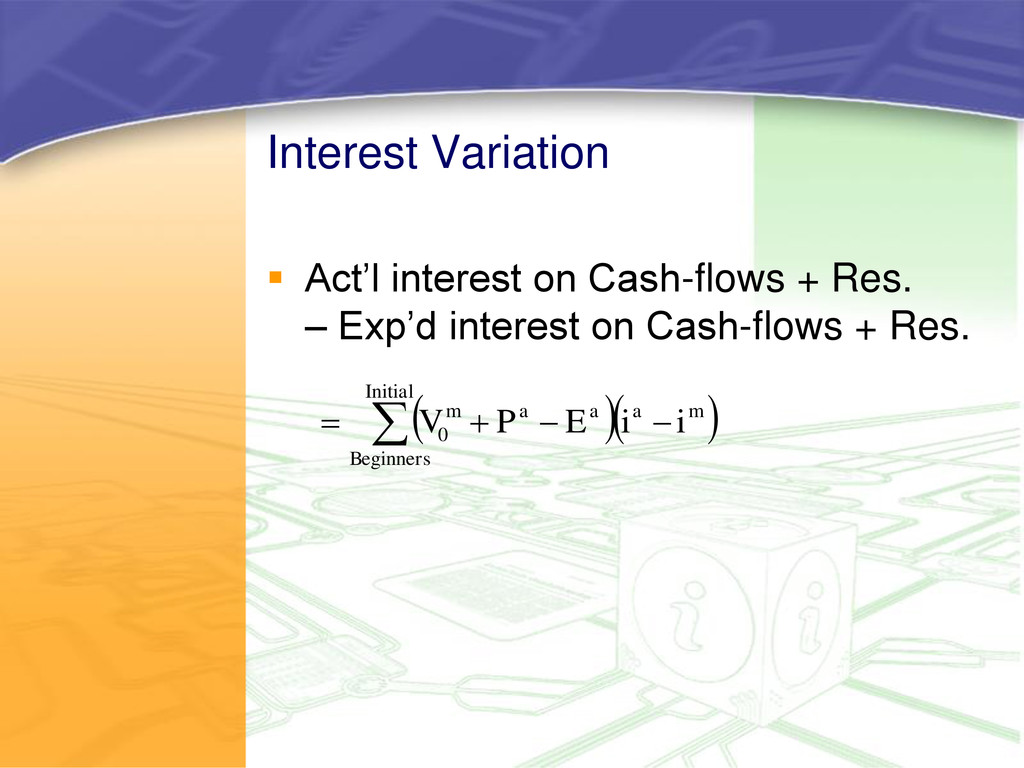

month of issue Reserves released as at month of exit Premiums and expenses at start of month, claims at end of month Monthly sources accumulated using Fund return

results are easily accumulated from quarterly results. Simple formula Reduces compounding and interaction Contingency sources are based on the immediate impact of the event

New Business Strain on Statutory Profit at Issue on Management Not at a “variable” point in the future. After the month of issue, policies are included in the “in-force” analysis of variations.

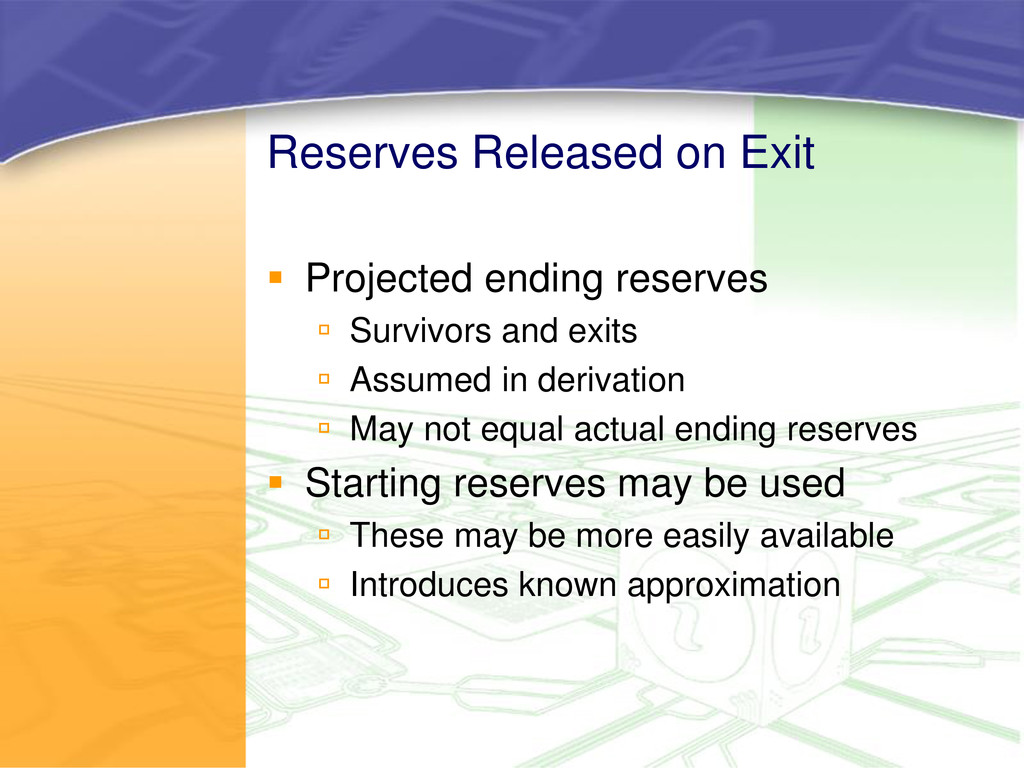

and exits Assumed in derivation May not equal actual ending reserves Starting reserves may be used These may be more easily available Introduces known approximation

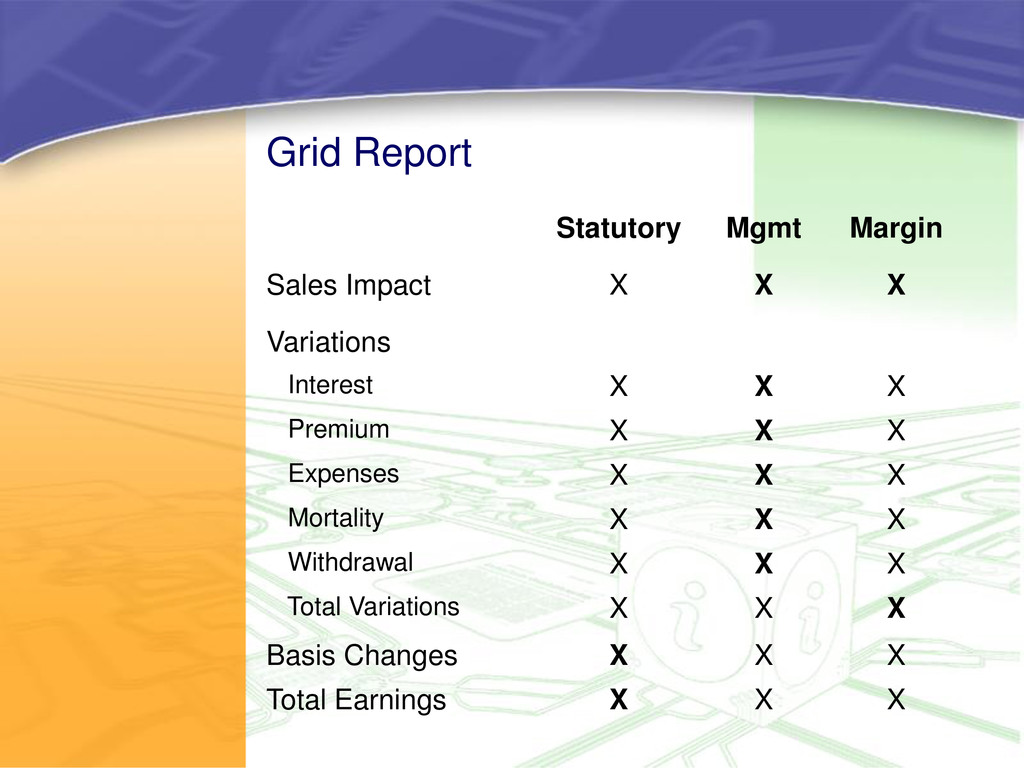

Variations Interest X X X Premium X X X Expenses X X X Mortality X X X Withdrawal X X X Total Variations X X X Basis Changes X X X Total Earnings X X X

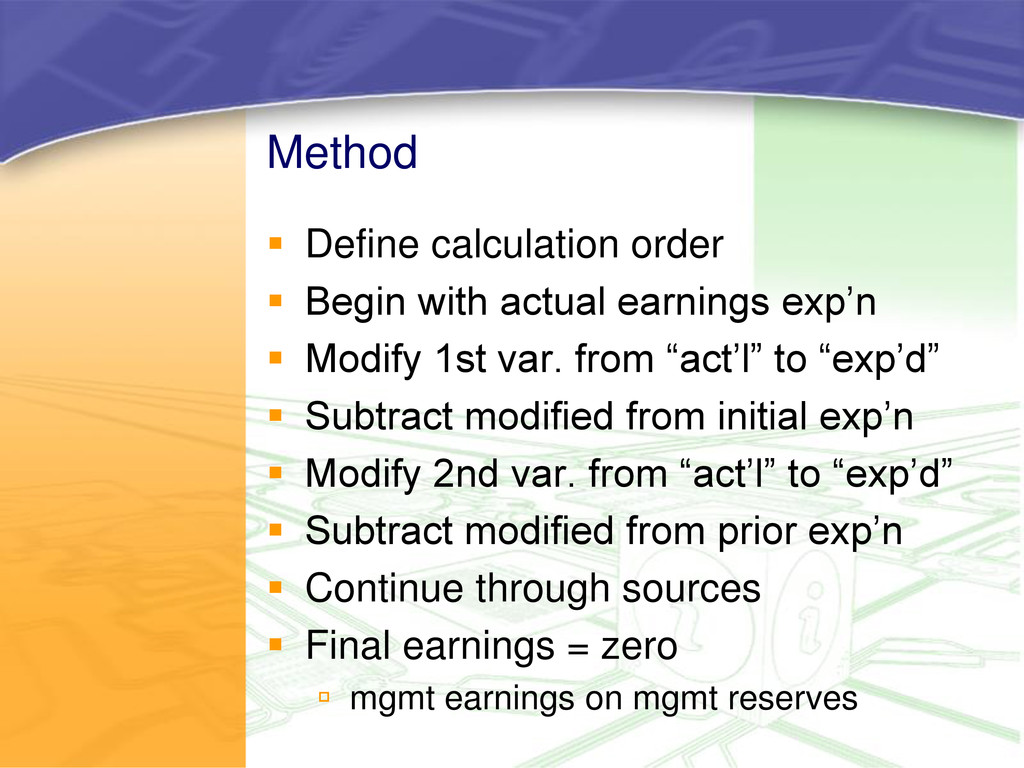

exp’n Modify 1st var. from “act’l” to “exp’d” Subtract modified from initial exp’n Modify 2nd var. from “act’l” to “exp’d” Subtract modified from prior exp’n Continue through sources Final earnings = zero mgmt earnings on mgmt reserves

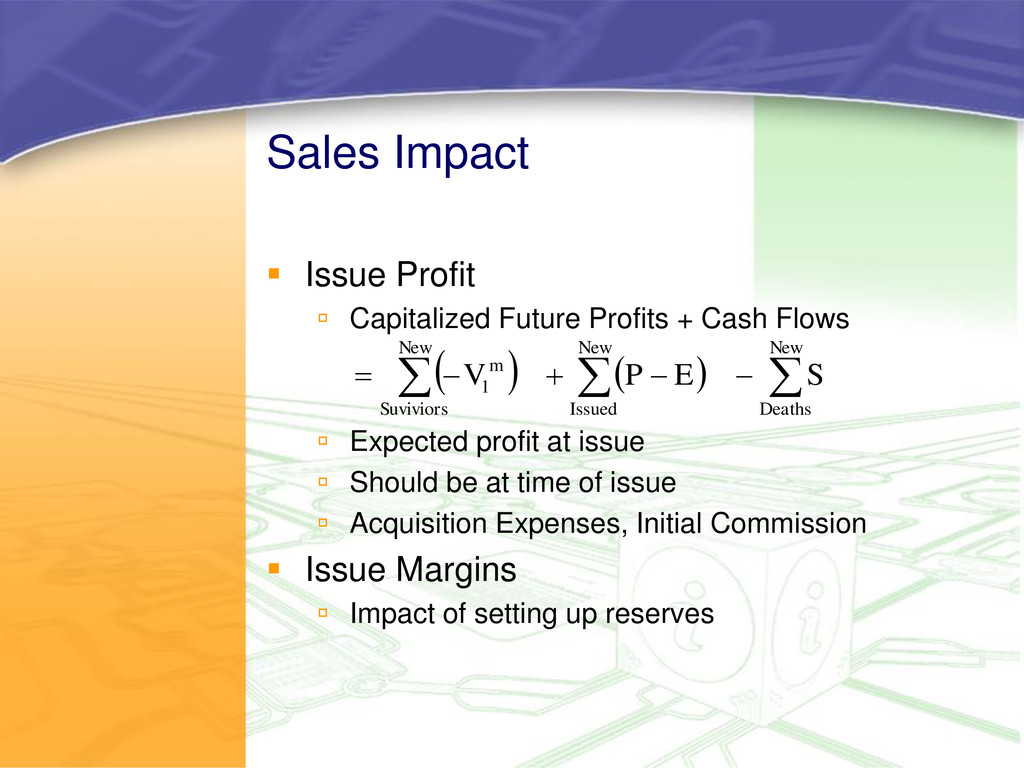

Cash Flows Expected profit at issue Should be at time of issue Acquisition Expenses, Initial Commission Issue Margins Impact of setting up reserves New Deaths New Issued New Suviviors m S E P V 1

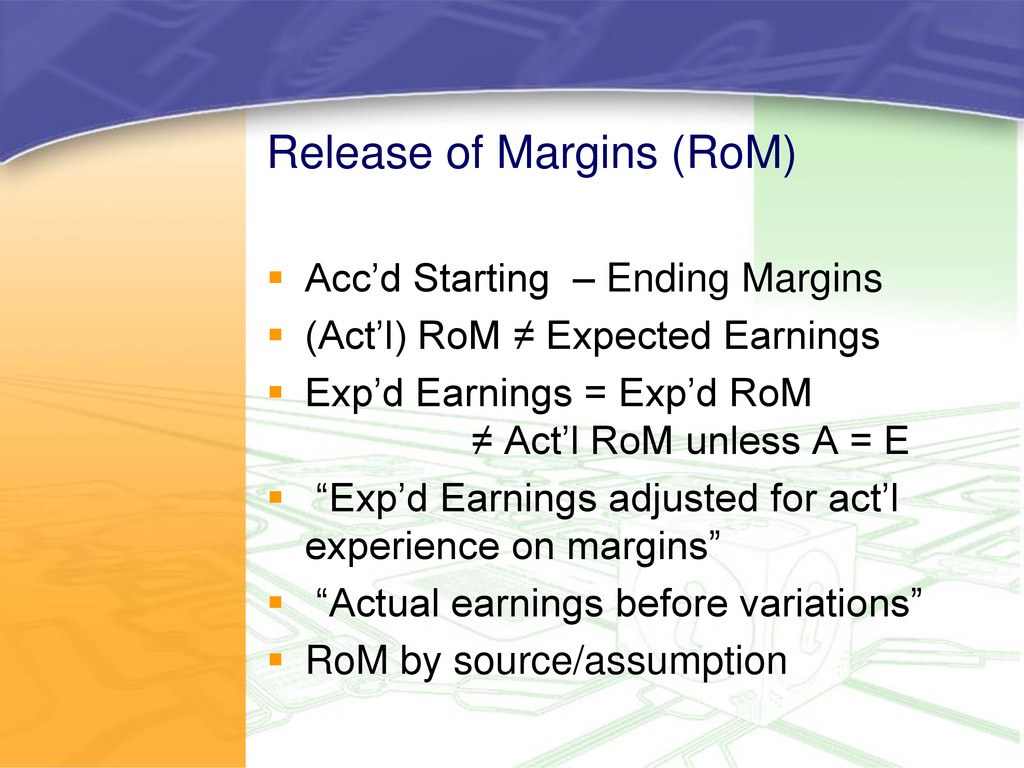

(Act’l) RoM ≠ Expected Earnings Exp’d Earnings = Exp’d RoM ≠ Act’l RoM unless A = E “Exp’d Earnings adjusted for act’l experience on margins” “Actual earnings before variations” RoM by source/assumption

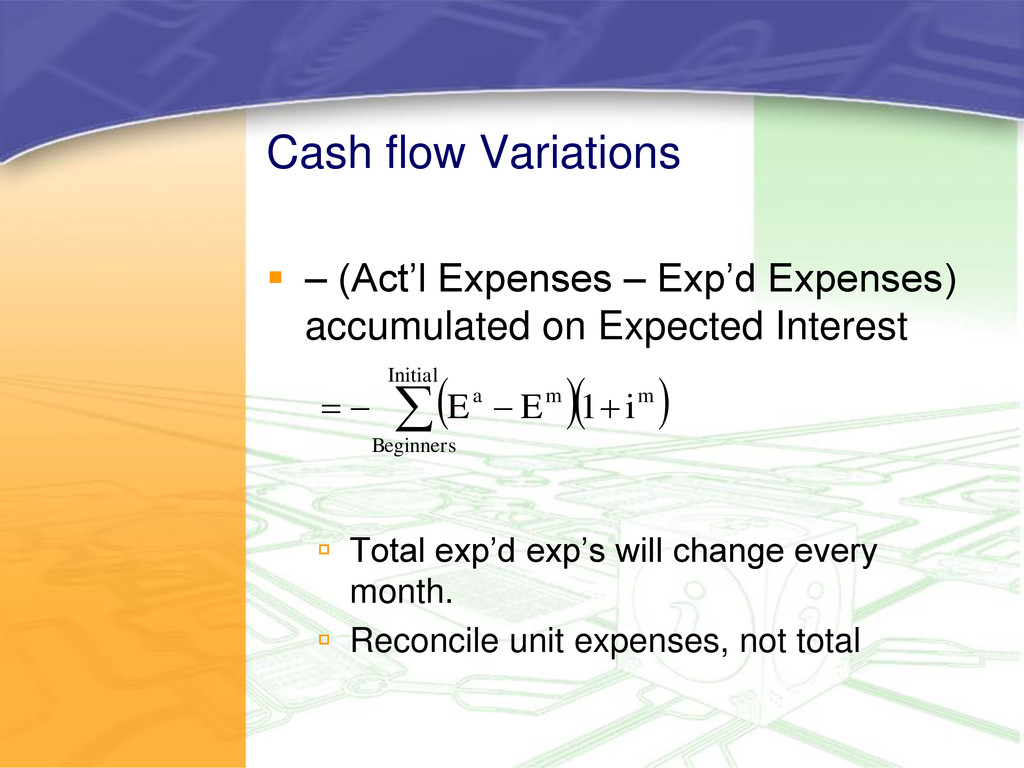

accumulated on Expected Interest Total exp’d exp’s will change every month. Reconcile unit expenses, not total Initial Beginners m m a i E E 1

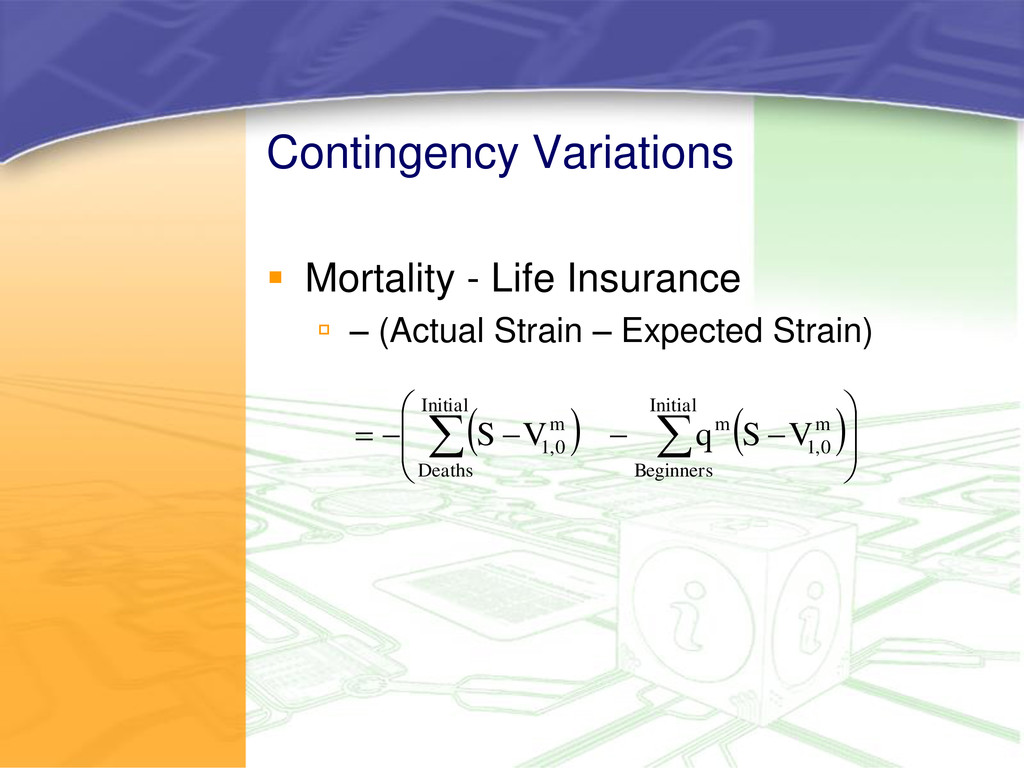

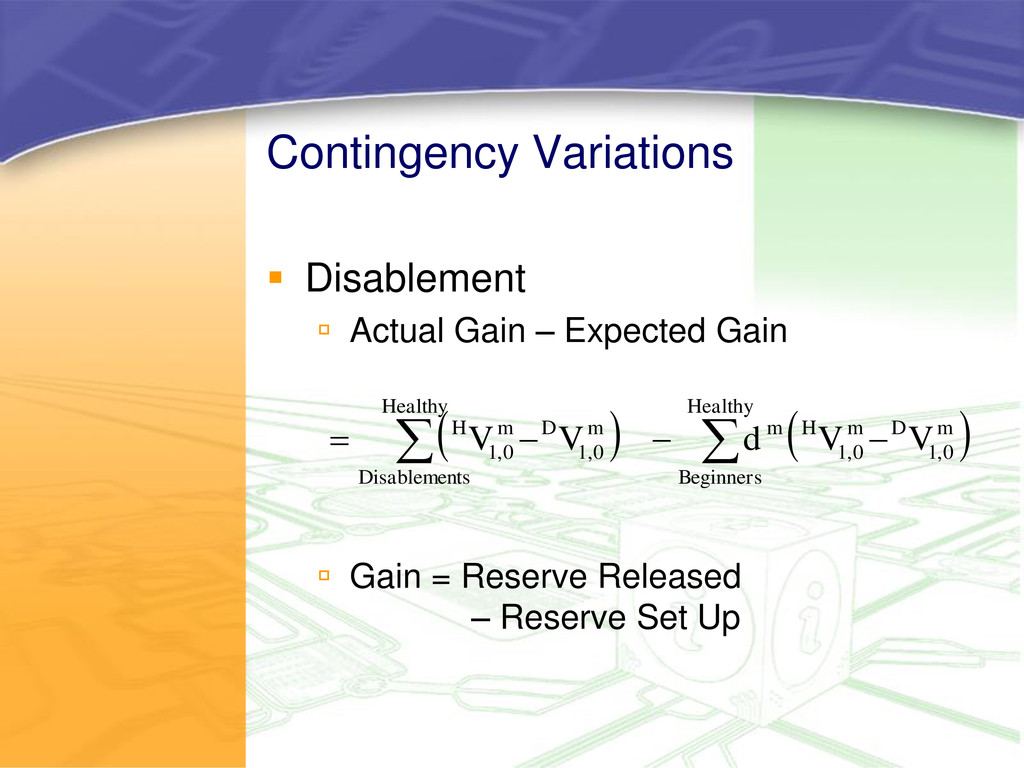

Gain = Reserve Released – Reserve Set Up Healthy Beginners m D m H m Healthy ts Disablemen m D m H V V d V V 0 , 1 0 , 1 0 , 1 0 , 1

Earnings No approximations necessary Known approximations due to data availability Magnitude can be estimated Modeling Variation Also acts as an error- check on the calculation or an order-check on approximations

Earnings on Actual Sales over the year. The difference between Original and Restated Planned Earnings is the impact of sales variations. Compare Restated Planned Earnings with Normal Profits (Issue Profit + Issue Margin + Release of Margins).

Continuous approach No approximations required Performance can be monitored over the year Meaningful explanation of results helps decision process

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

![Presenters Kevin Pledge [email protected] (905) 475 3282 x 1 John](https://files.speakerdeck.com/presentations/5013e3184667b300020457e5/slide_47.jpg){kind=link}

{kind=link}