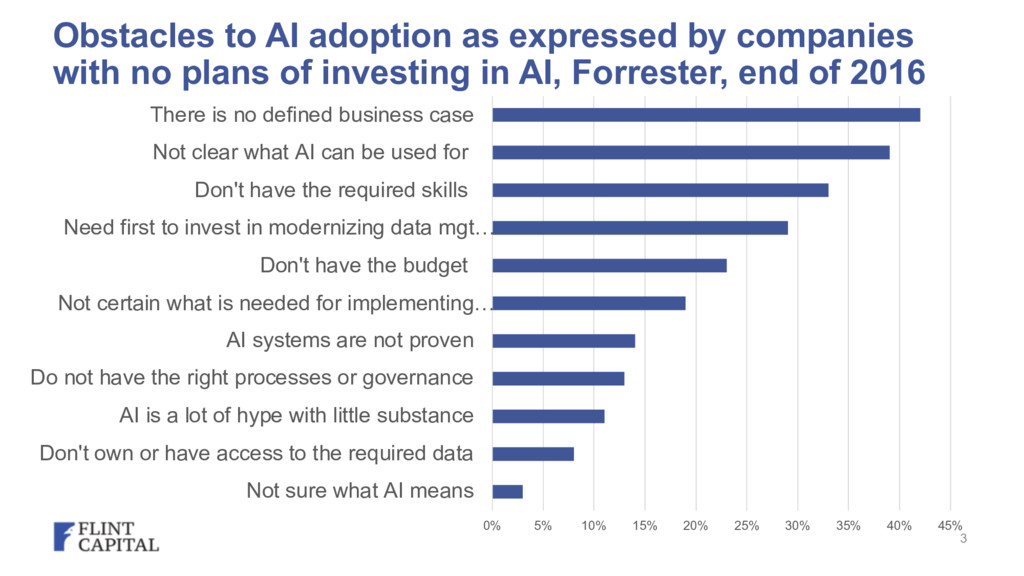

Not sure what AI means Don't own or have access to the required data AI is a lot of hype with little substance Do not have the right processes or governance AI systems are not proven Not certain what is needed for implementing… Don't have the budget Need first to invest in modernizing data mgt… Don't have the required skills Not clear what AI can be used for There is no defined business case Obstacles to AI adoption as expressed by companies with no plans of investing in AI, Forrester, end of 2016 3

learning: agents communicate with each other, micro-management scenarios are suggested • Learning from small data / knowledge transfer • Efficiency: selective activation, better simulations • Chasing stability that is required for wider/corporate adoption • Transparency and safety 5

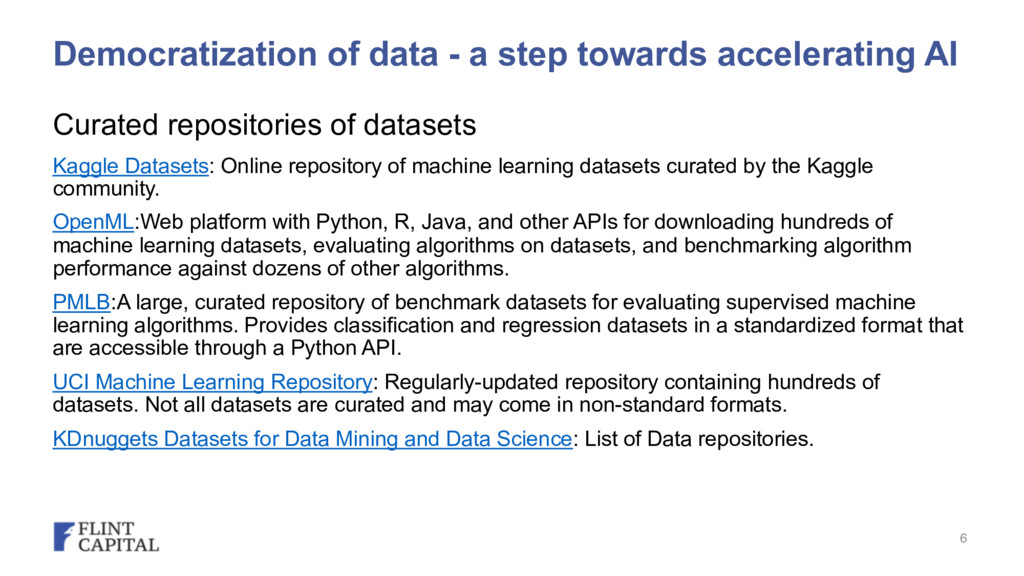

repositories of datasets Kaggle Datasets: Online repository of machine learning datasets curated by the Kaggle community. OpenML:Web platform with Python, R, Java, and other APIs for downloading hundreds of machine learning datasets, evaluating algorithms on datasets, and benchmarking algorithm performance against dozens of other algorithms. PMLB:A large, curated repository of benchmark datasets for evaluating supervised machine learning algorithms. Provides classification and regression datasets in a standardized format that are accessible through a Python API. UCI Machine Learning Repository: Regularly-updated repository containing hundreds of datasets. Not all datasets are curated and may come in non-standard formats. KDnuggets Datasets for Data Mining and Data Science: List of Data repositories. 6

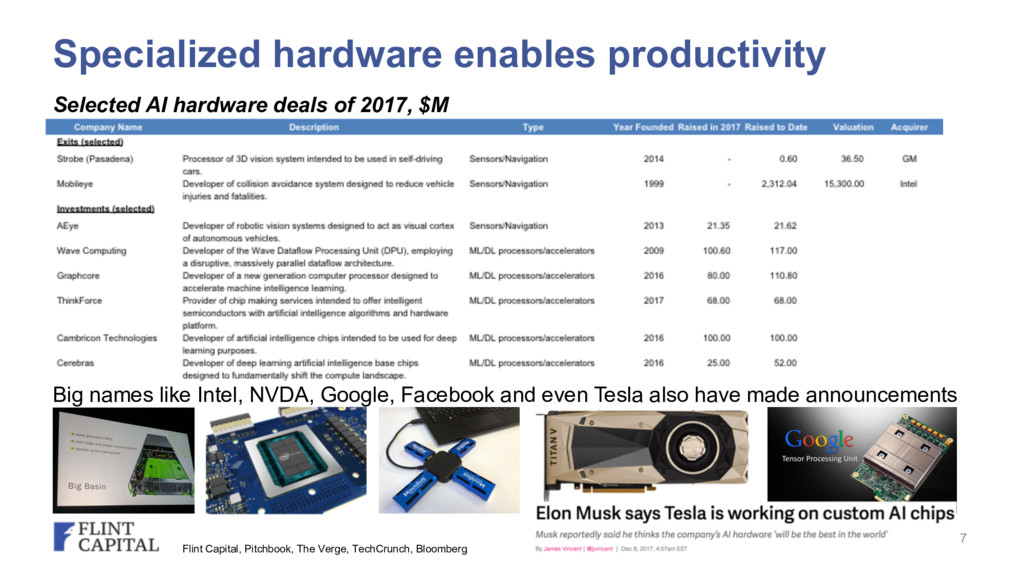

also have made announcements Flint Capital, Pitchbook, The Verge, TechCrunch, Bloomberg Selected AI hardware deals of 2017, $M Specialized hardware enables productivity 7

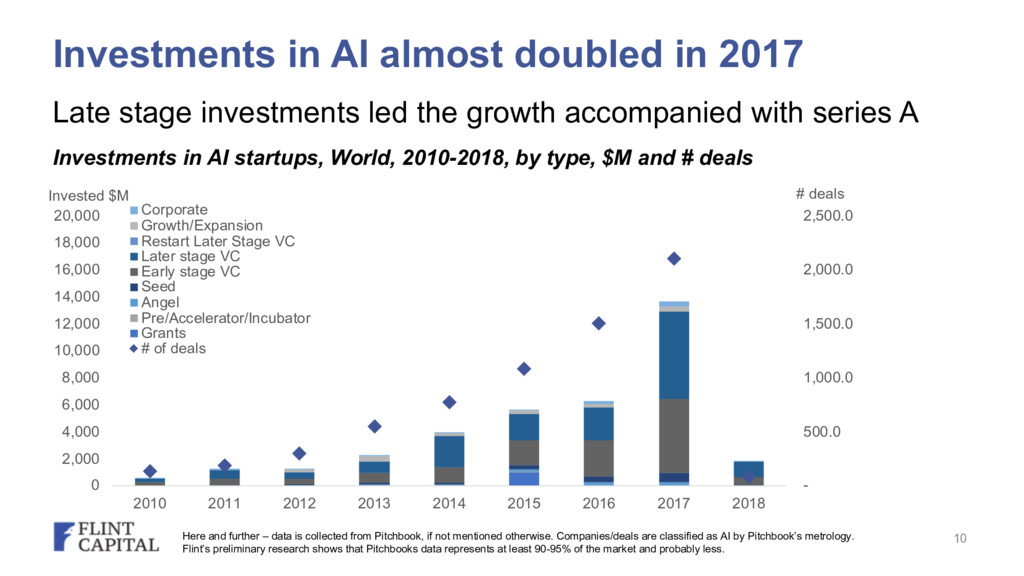

8,000 10,000 12,000 14,000 16,000 18,000 20,000 2010 2011 2012 2013 2014 2015 2016 2017 2018 # deals Invested $M Corporate Growth/Expansion Restart Later Stage VC Later stage VC Early stage VC Seed Angel Pre/Accelerator/Incubator Grants # of deals Late stage investments led the growth accompanied with series A Here and further – data is collected from Pitchbook, if not mentioned otherwise. Companies/deals are classified as AI by Pitchbook’s metrology. Flint’s preliminary research shows that Pitchbooks data represents at least 90-95% of the market and probably less. Investments in AI startups, World, 2010-2018, by type, $M and # deals Investments in AI almost doubled in 2017 10

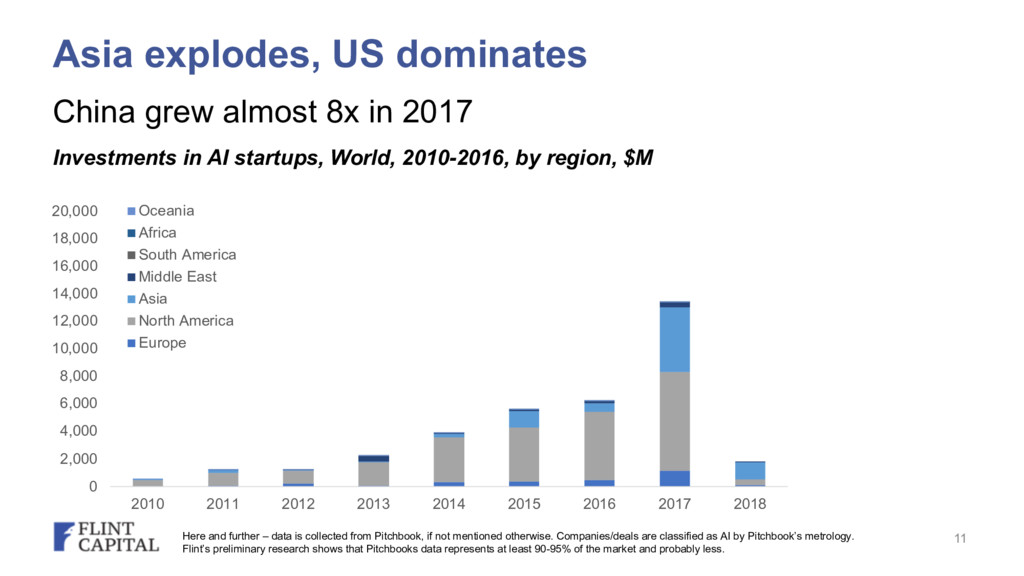

20,000 2010 2011 2012 2013 2014 2015 2016 2017 2018 Oceania Africa South America Middle East Asia North America Europe Asia explodes, US dominates China grew almost 8x in 2017 Investments in AI startups, World, 2010-2016, by region, $M Here and further – data is collected from Pitchbook, if not mentioned otherwise. Companies/deals are classified as AI by Pitchbook’s metrology. Flint’s preliminary research shows that Pitchbooks data represents at least 90-95% of the market and probably less. 11

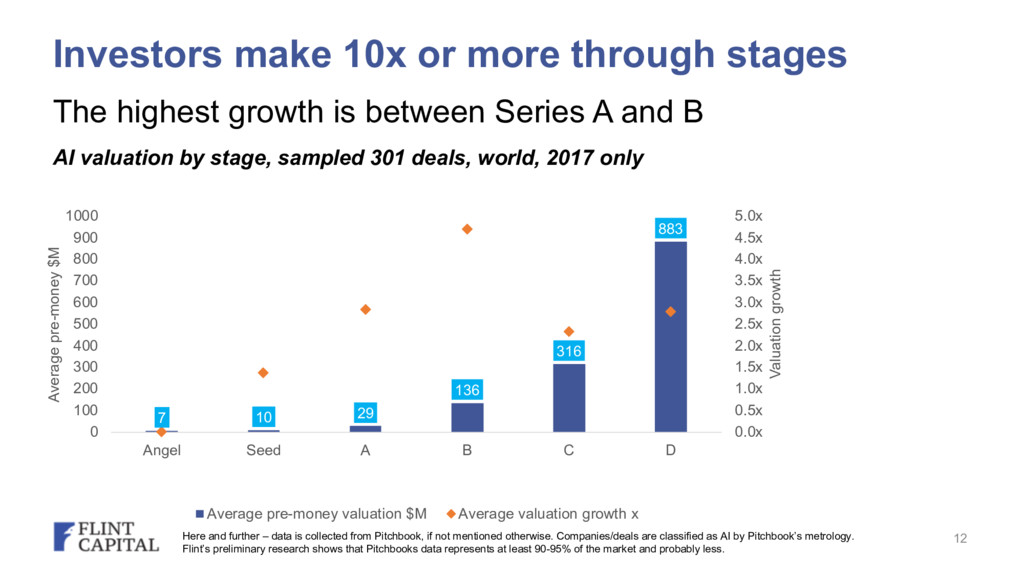

valuation by stage, sampled 301 deals, world, 2017 only 7 10 29 136 316 883 0.0x 0.5x 1.0x 1.5x 2.0x 2.5x 3.0x 3.5x 4.0x 4.5x 5.0x 0 100 200 300 400 500 600 700 800 900 1000 Angel Seed A B C D Valuation growth Average pre-money $M Average pre-money valuation $M Average valuation growth x Investors make 10x or more through stages Here and further – data is collected from Pitchbook, if not mentioned otherwise. Companies/deals are classified as AI by Pitchbook’s metrology. Flint’s preliminary research shows that Pitchbooks data represents at least 90-95% of the market and probably less. 12

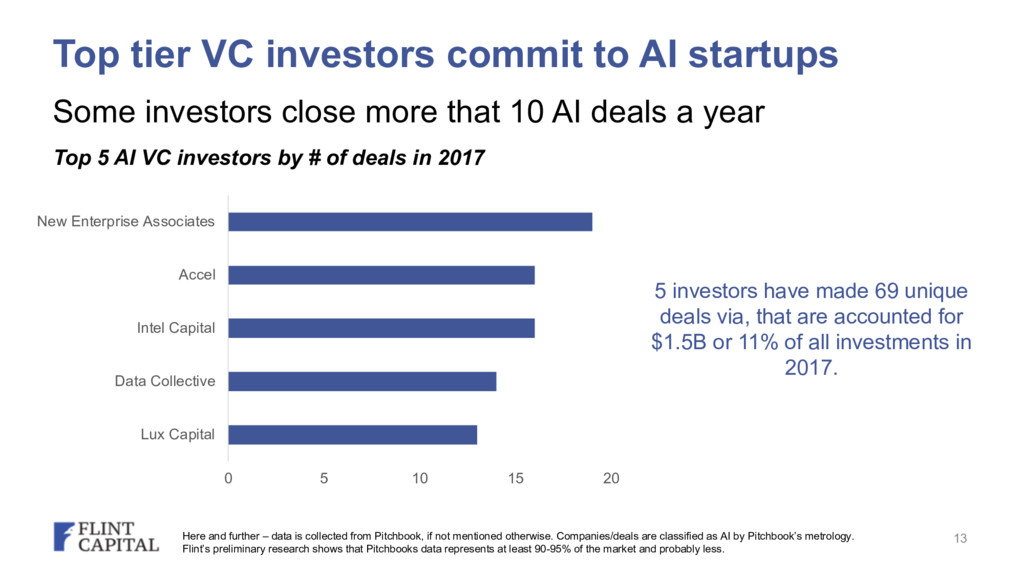

2017 Some investors close more that 10 AI deals a year 0 5 10 15 20 Lux Capital Data Collective Intel Capital Accel New Enterprise Associates 5 investors have made 69 unique deals via, that are accounted for $1.5B or 11% of all investments in 2017. Here and further – data is collected from Pitchbook, if not mentioned otherwise. Companies/deals are classified as AI by Pitchbook’s metrology. Flint’s preliminary research shows that Pitchbooks data represents at least 90-95% of the market and probably less. Top tier VC investors commit to AI startups 13

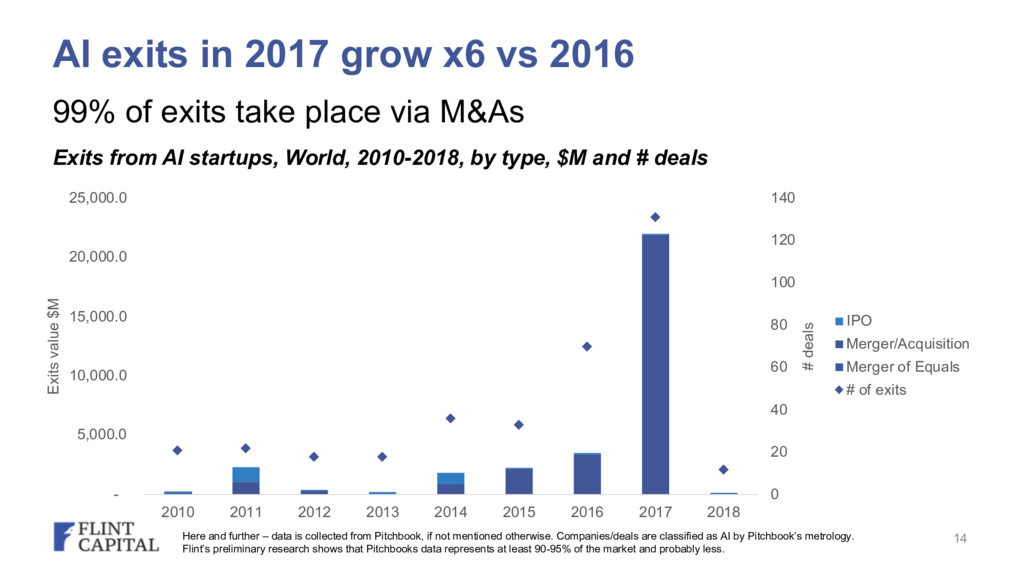

# deals 99% of exits take place via M&As 0 20 40 60 80 100 120 140 - 5,000.0 10,000.0 15,000.0 20,000.0 25,000.0 2010 2011 2012 2013 2014 2015 2016 2017 2018 # deals Exits value $M IPO Merger/Acquisition Merger of Equals # of exits Here and further – data is collected from Pitchbook, if not mentioned otherwise. Companies/deals are classified as AI by Pitchbook’s metrology. Flint’s preliminary research shows that Pitchbooks data represents at least 90-95% of the market and probably less. AI exits in 2017 grow x6 vs 2016 14

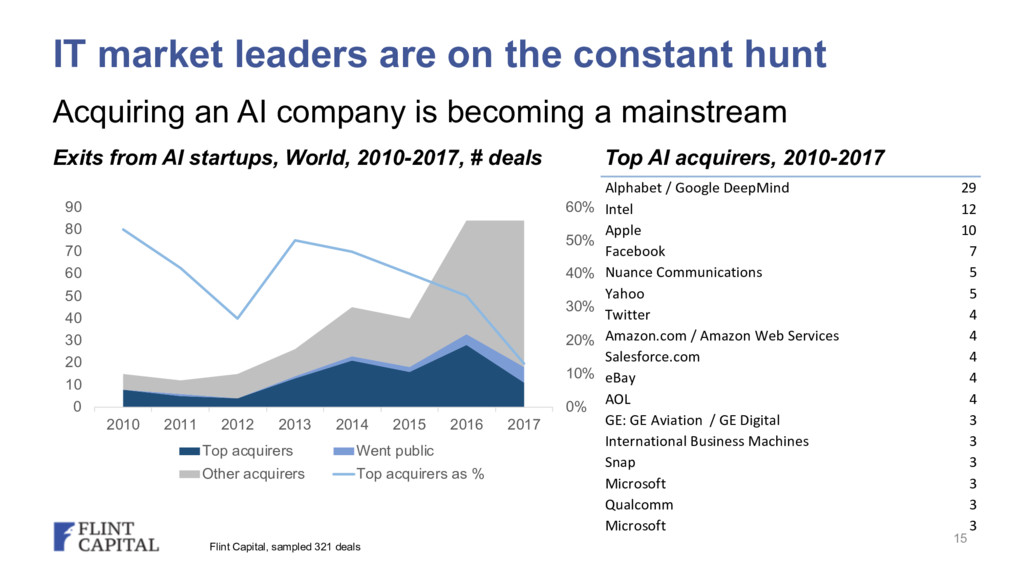

30 40 50 60 70 80 90 2010 2011 2012 2013 2014 2015 2016 2017 Top acquirers Went public Other acquirers Top acquirers as % Exits from AI startups, World, 2010-2017, # deals Acquiring an AI company is becoming a mainstream Flint Capital, sampled 321 deals Top AI acquirers, 2010-2017 Row Labels Count of Company Name Alphabet / Google DeepMind 29 Intel 12 Apple 10 Facebook 7 Nuance Communications 5 Yahoo 5 Twitter 4 Amazon.com / Amazon Web Services 4 Salesforce.com 4 eBay 4 AOL 4 GE: GE Aviation / GE Digital 3 International Business Machines 3 Snap 3 Microsoft 3 Qualcomm 3 Microsoft 3 IT market leaders are on the constant hunt 15

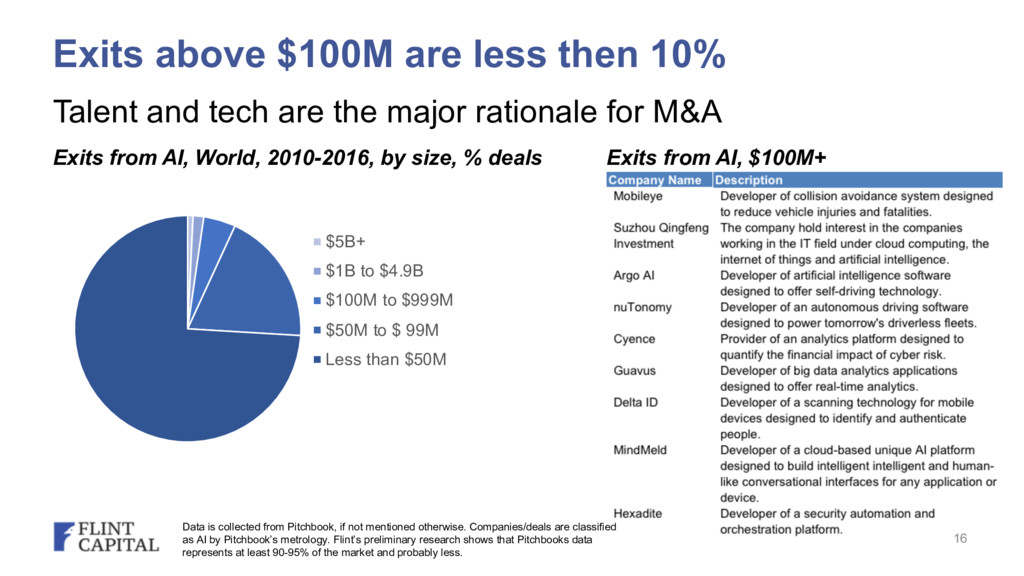

from AI, $100M+ Data is collected from Pitchbook, if not mentioned otherwise. Companies/deals are classified as AI by Pitchbook’s metrology. Flint’s preliminary research shows that Pitchbooks data represents at least 90-95% of the market and probably less. $5B+ $1B to $4.9B $100M to $999M $50M to $ 99M Less than $50M Talent and tech are the major rationale for M&A Exits above $100M are less then 10% 16

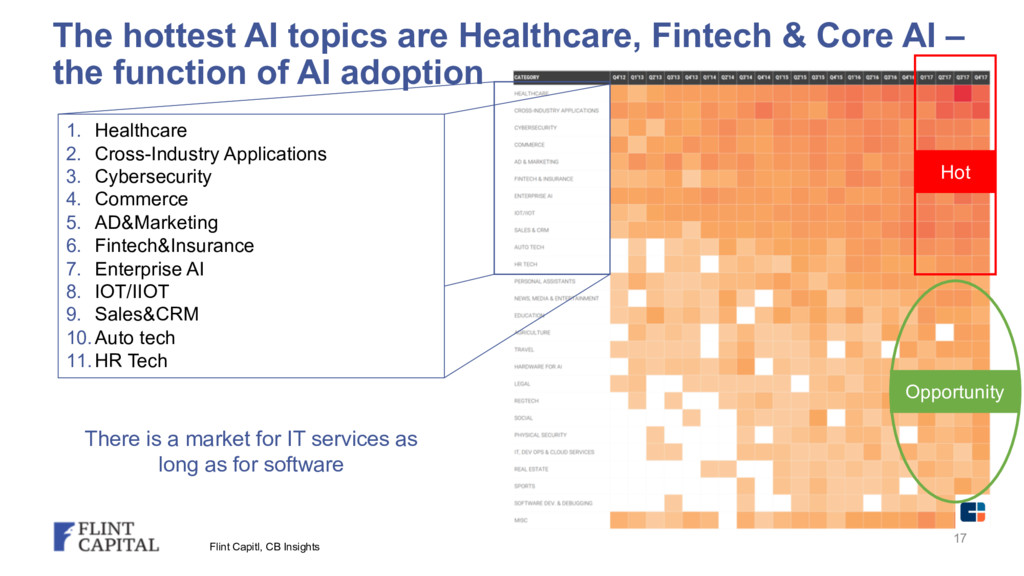

– the function of AI adoption 1. Healthcare 2. Cross-Industry Applications 3. Cybersecurity 4. Commerce 5. AD&Marketing 6. Fintech&Insurance 7. Enterprise AI 8. IOT/IIOT 9. Sales&CRM 10.Auto tech 11.HR Tech There is a market for IT services as long as for software Flint Capitl, CB Insights Opportunity Hot 17

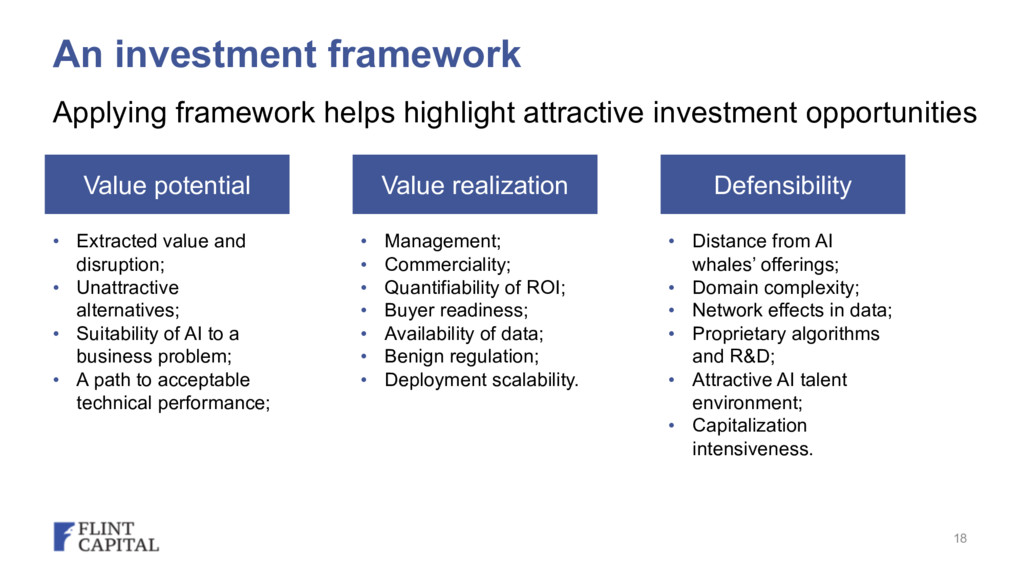

helps highlight attractive investment opportunities • Extracted value and disruption; • Unattractive alternatives; • Suitability of AI to a business problem; • A path to acceptable technical performance; • Management; • Commerciality; • Quantifiability of ROI; • Buyer readiness; • Availability of data; • Benign regulation; • Deployment scalability. • Distance from AI whales’ offerings; • Domain complexity; • Network effects in data; • Proprietary algorithms and R&D; • Attractive AI talent environment; • Capitalization intensiveness. 18

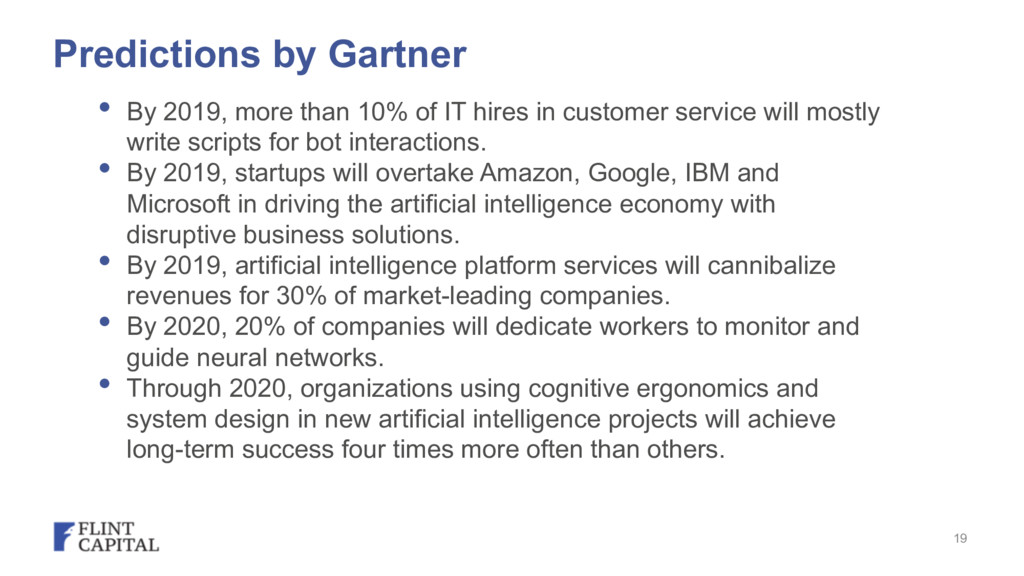

customer service will mostly write scripts for bot interactions. • By 2019, startups will overtake Amazon, Google, IBM and Microsoft in driving the artificial intelligence economy with disruptive business solutions. • By 2019, artificial intelligence platform services will cannibalize revenues for 30% of market-leading companies. • By 2020, 20% of companies will dedicate workers to monitor and guide neural networks. • Through 2020, organizations using cognitive ergonomics and system design in new artificial intelligence projects will achieve long-term success four times more often than others. Predictions by Gartner 19

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

![Thank you! ANDREW GERSHFELD [email protected] https://www.linkedin.com/in/andrewger](https://files.speakerdeck.com/presentations/5f44da48d8514a23a6e3db4771121299/slide_20.jpg){kind=link}