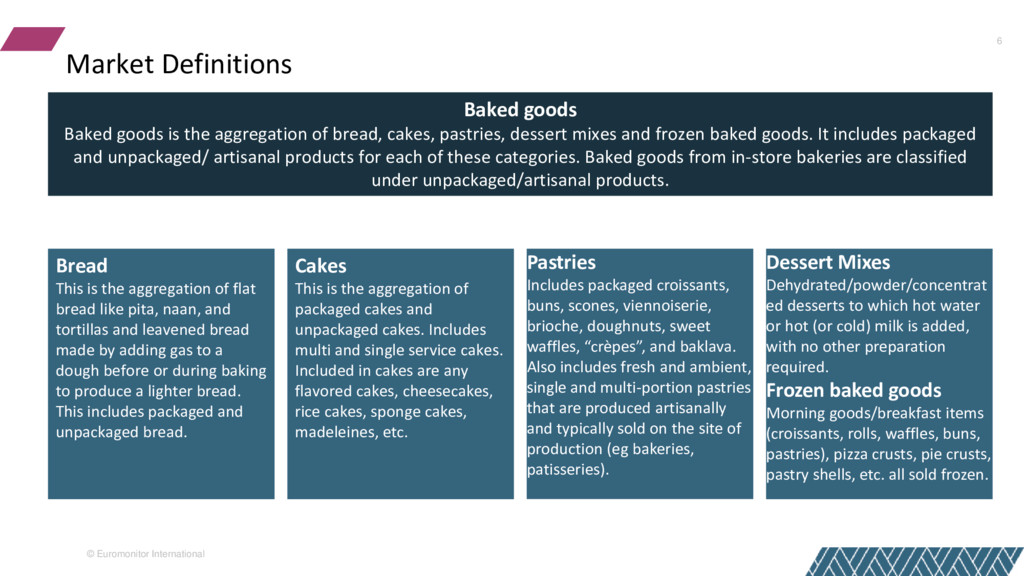

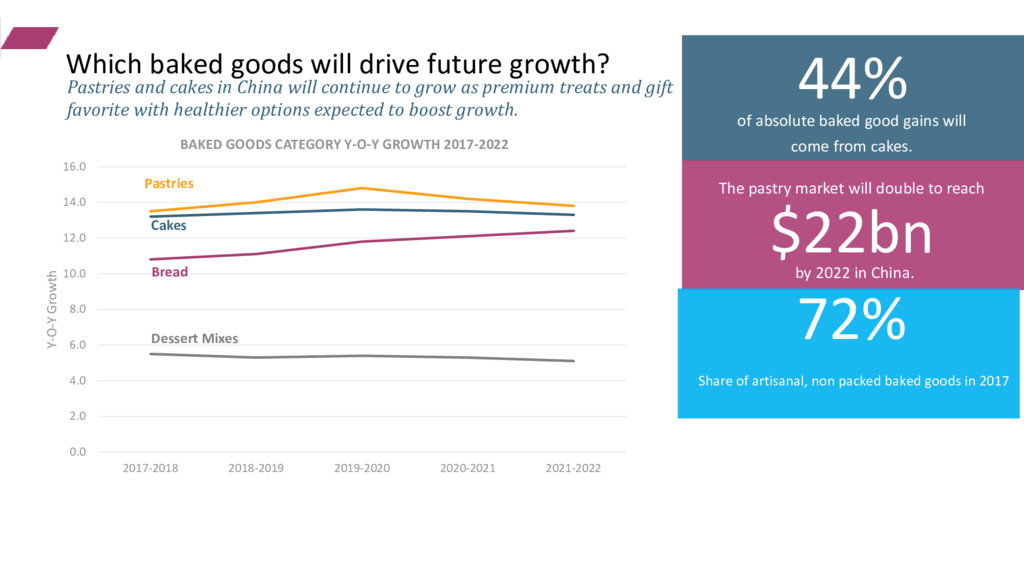

is the aggregation of bread, cakes, pastries, dessert mixes and frozen baked goods. It includes packaged and unpackaged/ artisanal products for each of these categories. Baked goods from in-store bakeries are classified under unpackaged/artisanal products. Pastries Includes packaged croissants, buns, scones, viennoiserie, brioche, doughnuts, sweet waffles, “crèpes”, and baklava. Also includes fresh and ambient, single and multi-portion pastries that are produced artisanally and typically sold on the site of production (eg bakeries, patisseries). Bread This is the aggregation of flat bread like pita, naan, and tortillas and leavened bread made by adding gas to a dough before or during baking to produce a lighter bread. This includes packaged and unpackaged bread. Cakes This is the aggregation of packaged cakes and unpackaged cakes. Includes multi and single service cakes. Included in cakes are any flavored cakes, cheesecakes, rice cakes, sponge cakes, madeleines, etc. Dessert Mixes Dehydrated/powder/concentrat ed desserts to which hot water or hot (or cold) milk is added, with no other preparation required. Frozen baked goods Morning goods/breakfast items (croissants, rolls, waffles, buns, pastries), pizza crusts, pie crusts, pastry shells, etc. all sold frozen.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}