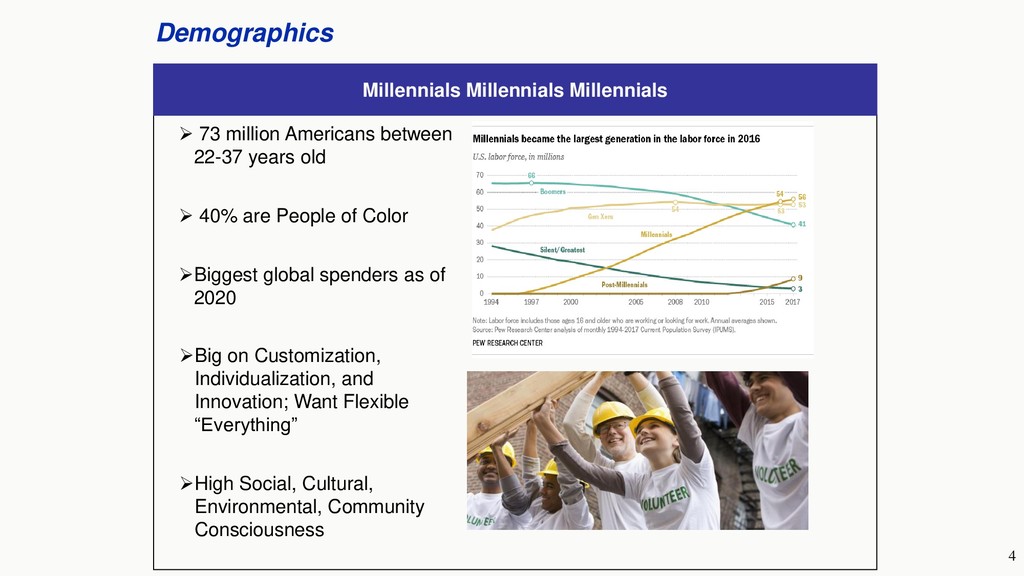

22-37 years old ➢ 40% are People of Color ➢Biggest global spenders as of 2020 ➢Big on Customization, Individualization, and Innovation; Want Flexible “Everything” ➢High Social, Cultural, Environmental, Community Consciousness

to 2010 ➢ 30% of world’s 7.5 Billion Population ➢ Will dictate 40% of consumer spending in early 2020s ➢ 48% of US’ Gen Z people of color ➢ Digital Everything – addicted to phones, screens – 92% smartphone ownership - 5 hours per day screen time ➢ Into auto-replenishment, home delivery, “plant-forward” diets

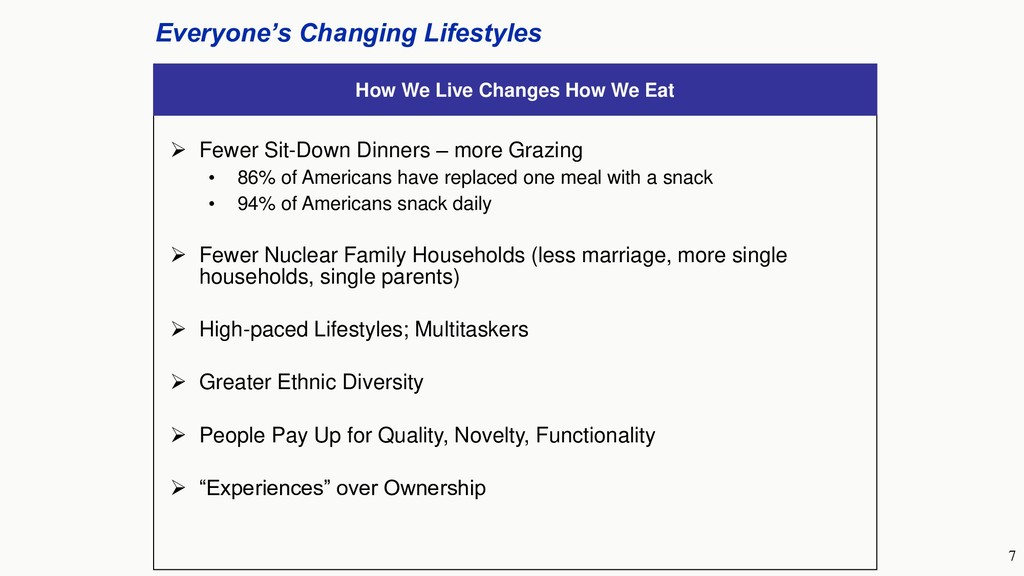

Eat ➢ Fewer Sit-Down Dinners – more Grazing • 86% of Americans have replaced one meal with a snack • 94% of Americans snack daily ➢ Fewer Nuclear Family Households (less marriage, more single households, single parents) ➢ High-paced Lifestyles; Multitaskers ➢ Greater Ethnic Diversity ➢ People Pay Up for Quality, Novelty, Functionality ➢ “Experiences” over Ownership

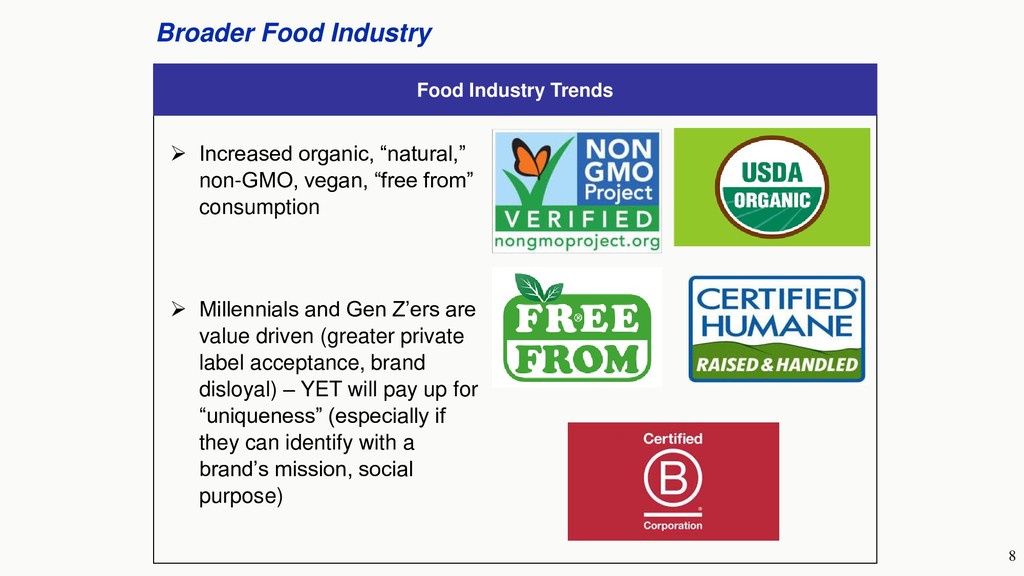

“natural,” non-GMO, vegan, “free from” consumption ➢ Millennials and Gen Z’ers are value driven (greater private label acceptance, brand disloyal) – YET will pay up for “uniqueness” (especially if they can identify with a brand’s mission, social purpose)

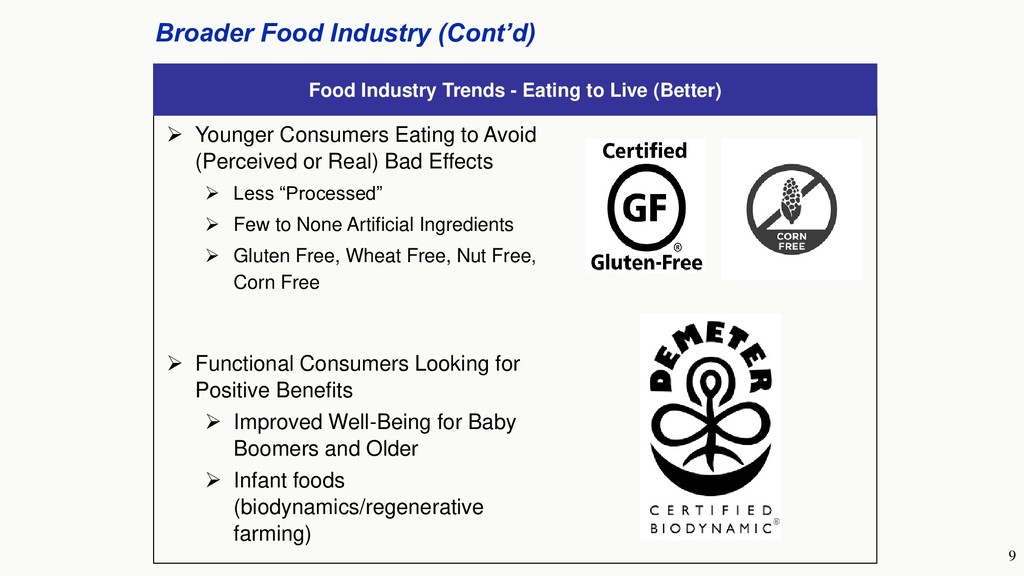

to Live (Better) ➢ Younger Consumers Eating to Avoid (Perceived or Real) Bad Effects ➢ Less “Processed” ➢ Few to None Artificial Ingredients ➢ Gluten Free, Wheat Free, Nut Free, Corn Free ➢ Functional Consumers Looking for Positive Benefits ➢ Improved Well-Being for Baby Boomers and Older ➢ Infant foods (biodynamics/regenerative farming)

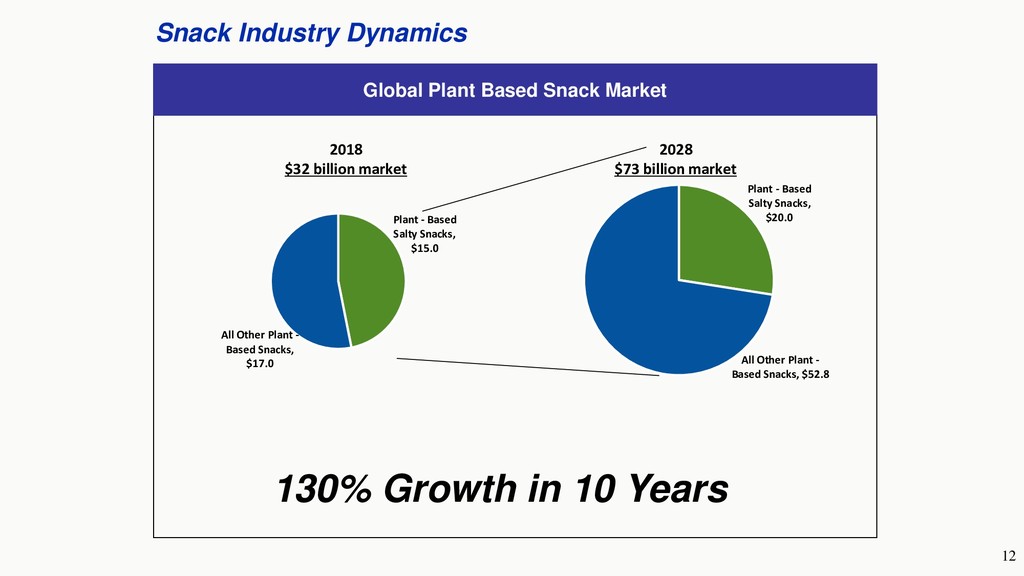

$32 billion market 2028 $73 billion market Plant - Based Salty Snacks, $15.0 All Other Plant - Based Snacks, $17.0 Plant - Based Salty Snacks, $20.0 All Other Plant - Based Snacks, $52.8 130% Growth in 10 Years

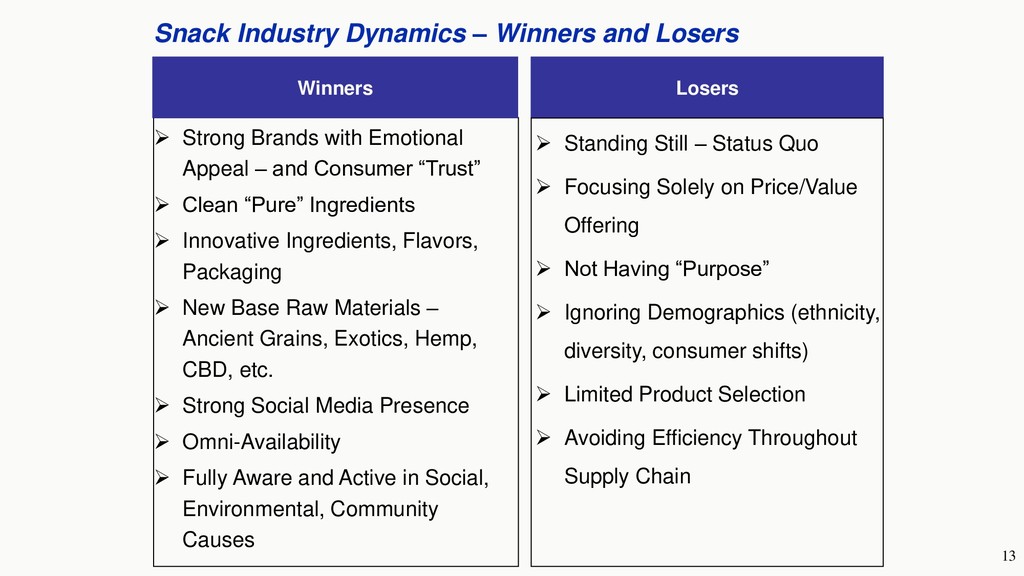

➢ Strong Brands with Emotional Appeal – and Consumer “Trust” ➢ Clean “Pure” Ingredients ➢ Innovative Ingredients, Flavors, Packaging ➢ New Base Raw Materials – Ancient Grains, Exotics, Hemp, CBD, etc. ➢ Strong Social Media Presence ➢ Omni-Availability ➢ Fully Aware and Active in Social, Environmental, Community Causes ➢ Standing Still – Status Quo ➢ Focusing Solely on Price/Value Offering ➢ Not Having “Purpose” ➢ Ignoring Demographics (ethnicity, diversity, consumer shifts) ➢ Limited Product Selection ➢ Avoiding Efficiency Throughout Supply Chain

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}