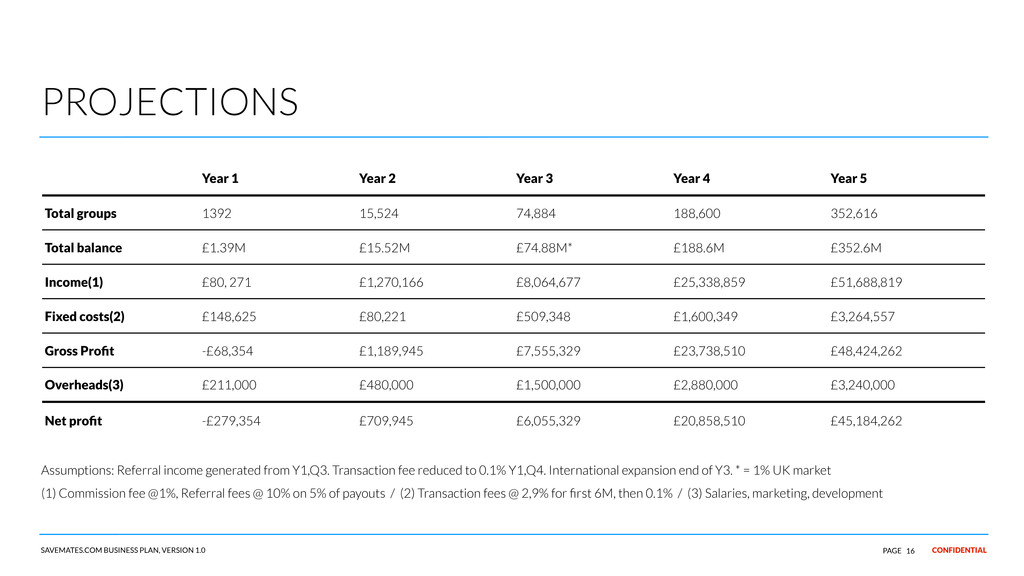

1 Year 2 Year 3 Year 4 Year 5 Total groups 1392 15,524 74,884 188,600 352,616 Total balance £1.39M £15.52M £74.88M* £188.6M £352.6M Income(1) £80, 271 £1,270,166 £8,064,677 £25,338,859 £51,688,819 Fixed costs(2) £148,625 £80,221 £509,348 £1,600,349 £3,264,557 Gross Profit -£68,354 £1,189,945 £7,555,329 £23,738,510 £48,424,262 Overheads(3) £211,000 £480,000 £1,500,000 £2,880,000 £3,240,000 Net profit -£279,354 £709,945 £6,055,329 £20,858,510 £45,184,262 Assumptions: Referral income generated from Y1,Q3. Transaction fee reduced to 0.1% Y1,Q4. International expansion end of Y3. * = 1% UK market (1) Commission fee @1%, Referral fees @ 10% on 5% of payouts / (2) Transaction fees @ 2,9% for first 6M, then 0.1% / (3) Salaries, marketing, development

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}