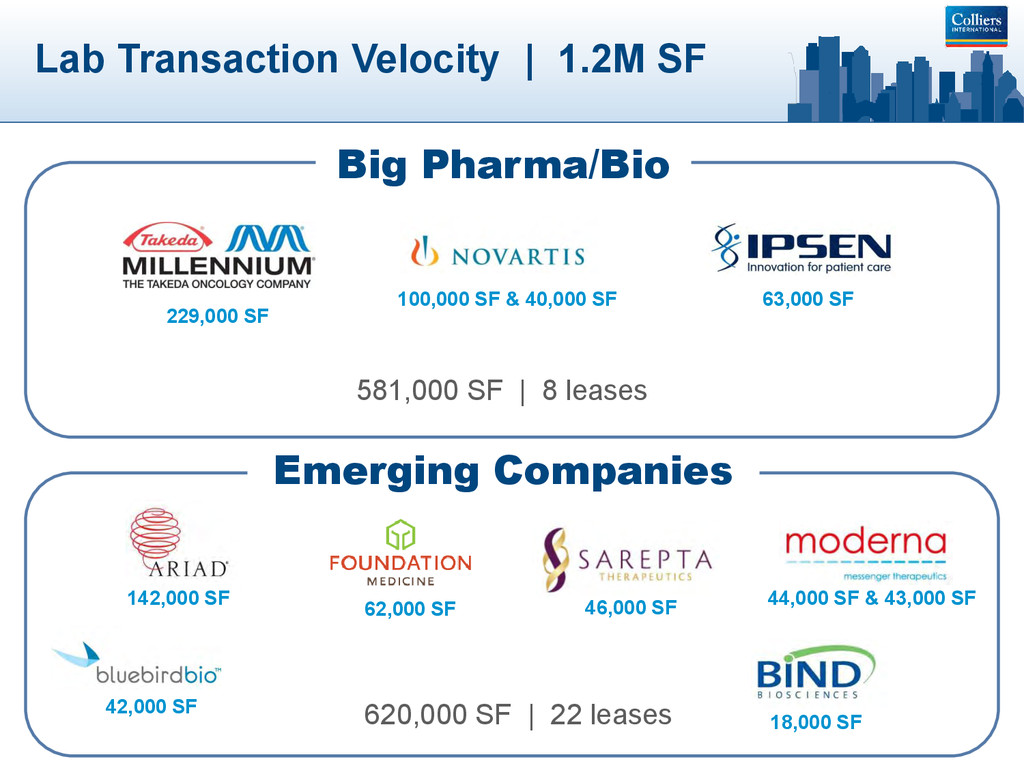

581,000 SF | 8 leases 620,000 SF | 22 leases 229,000 SF 100,000 SF & 40,000 SF 63,000 SF 142,000 SF 62,000 SF 44,000 SF & 43,000 SF 42,000 SF 18,000 SF 46,000 SF

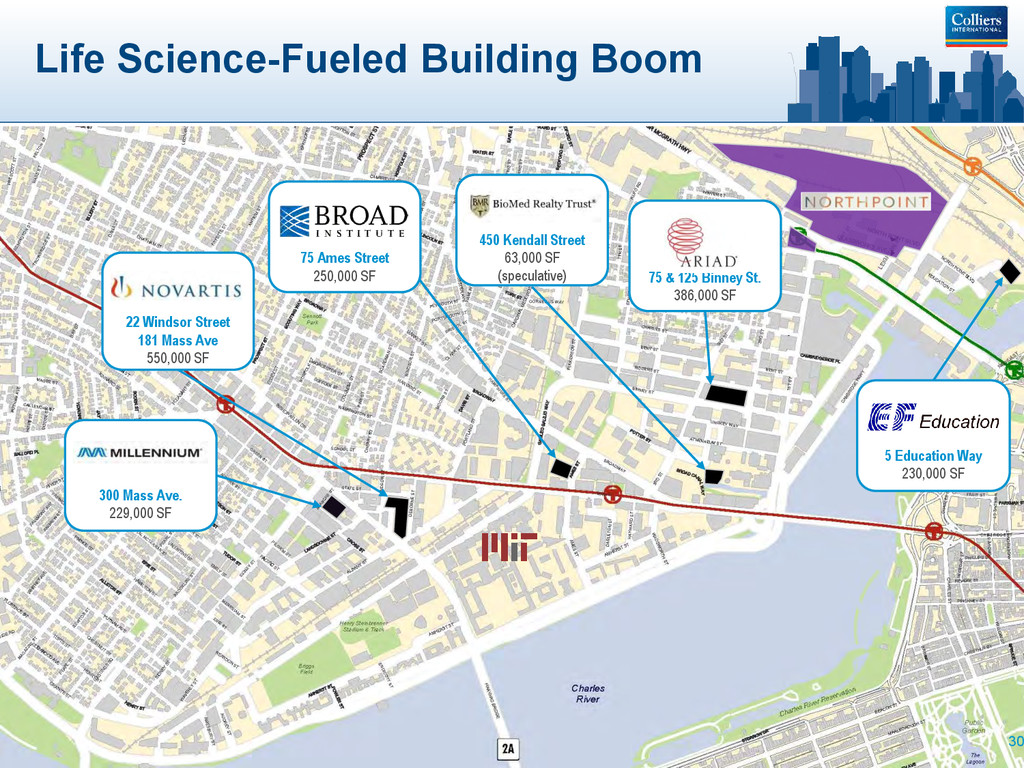

386,000 SF 5 Education Way 230,000 SF 75 Ames Street 250,000 SF 450 Kendall Street 63,000 SF (speculative) 300 Mass Ave. 229,000 SF 22 Windsor Street 181 Mass Ave 550,000 SF

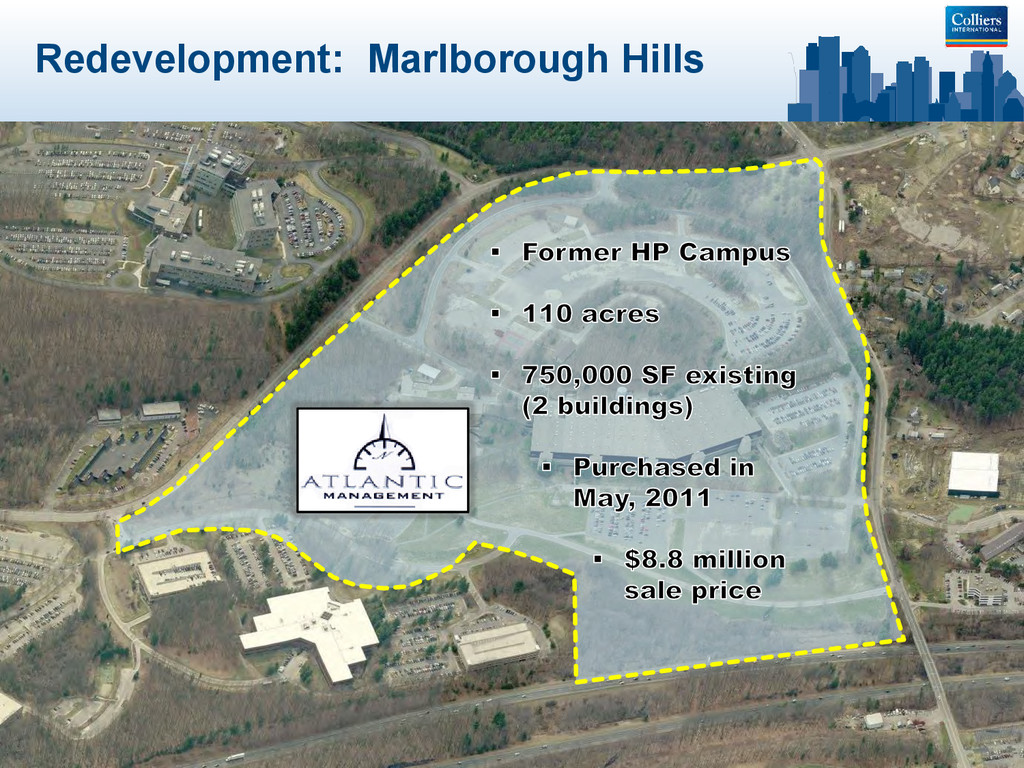

(Avalon) OFFICE / R&D 750,000 SF (2 buildings) 200,000 SF leased to Quest Redevelopment: Marlborough Hills RETAIL 50,000 – 70,000 SF (Restaurants, Shops, Small Grocer) HOSPITALITY 3 acres - 150 hotel rooms $17,000/key – Probable sale to Hilton

› Abundance of capital for all property types › But remaining gulf between core and non-core submarkets › Impact of rising interest rates on pricing › Banking on strengthening fundamentals

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

![Effingham Parc Apartments [352 Units] Rincon, GA](https://files.speakerdeck.com/presentations/8338d2a061a9013168711eceddceac98/slide_72.jpg){kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}