Crossing.” (Boston Globe) “Acquia is Moving to Boston from the ‘Burbs into a Space Double the Size.” (BostInno) “Boston Properties sells stakes in two Boston buildings to Norwegian sovereign wealth fund.” (BBJ) “Invesco Wins ‘War’ for Crosspoint’s 427,775 SF Seaport Package…Listing Could Top $180 Million.” (Real Reporter) Making Headlines... “Oxford Properties and JP Morgan complete purchase of local office buildings.” (Boston Globe) “Boston’s Seaport District held up as example of how to build a 21st century city.” (BBJ)

81,000 SF 93 Worcester Road Wellesley 80,000 SF 275 2nd Avenue Waltham 155,000 SF 175 Wyman Street Waltham 83,500 SF 275 Wyman Street Waltham 83,000 SF 191 Spring Street Lexington 150,000 SF 200 Wheeler Road Burlington 110,000 SF 78 Blanchard Road Burlington 84,000 SF 4 Burlington Woods Burlington 100,000 SF

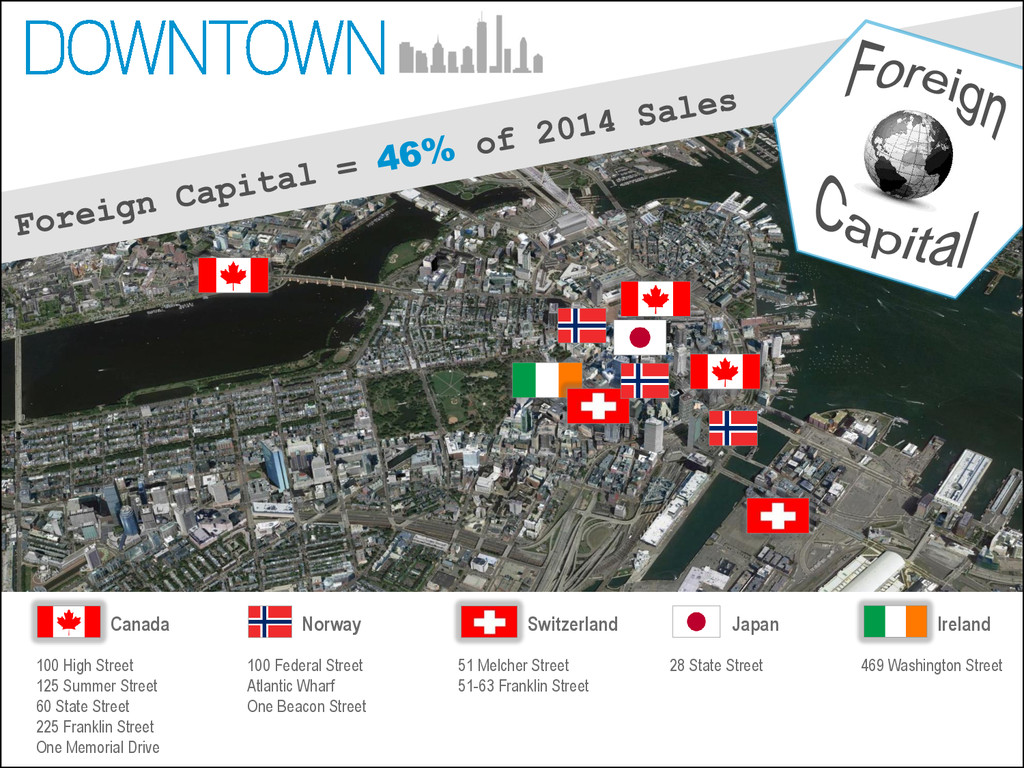

225 Franklin Street One Memorial Drive Norway 100 Federal Street Atlantic Wharf One Beacon Street Switzerland 51 Melcher Street 51-63 Franklin Street Japan 28 State Street Ireland 469 Washington Street

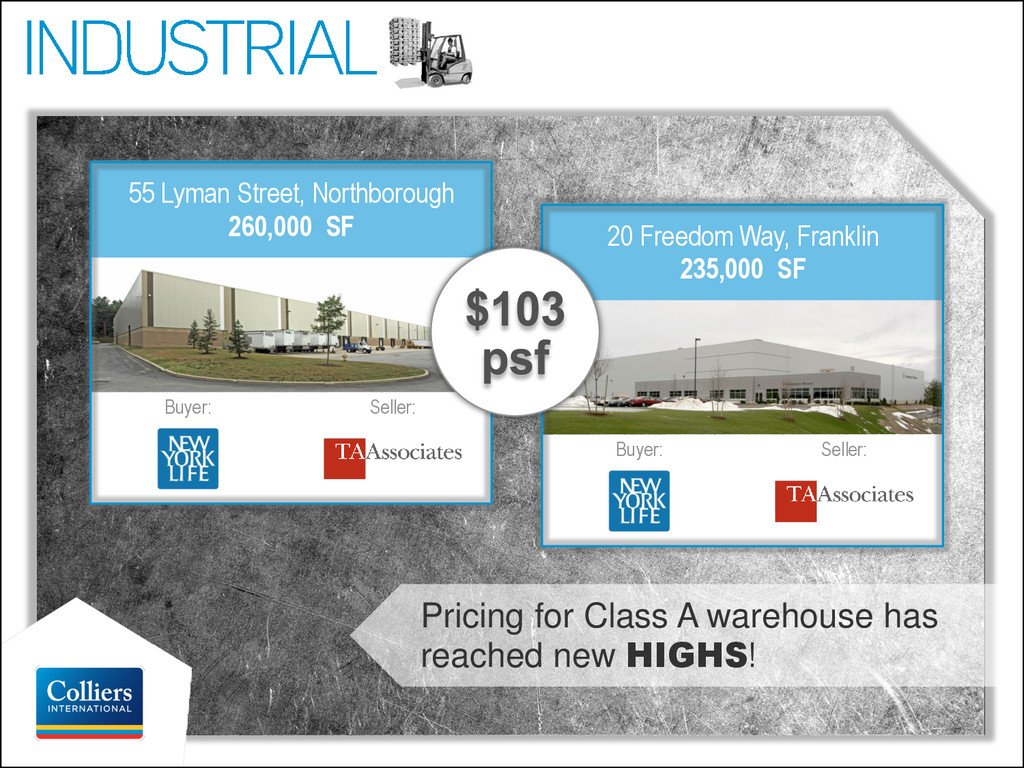

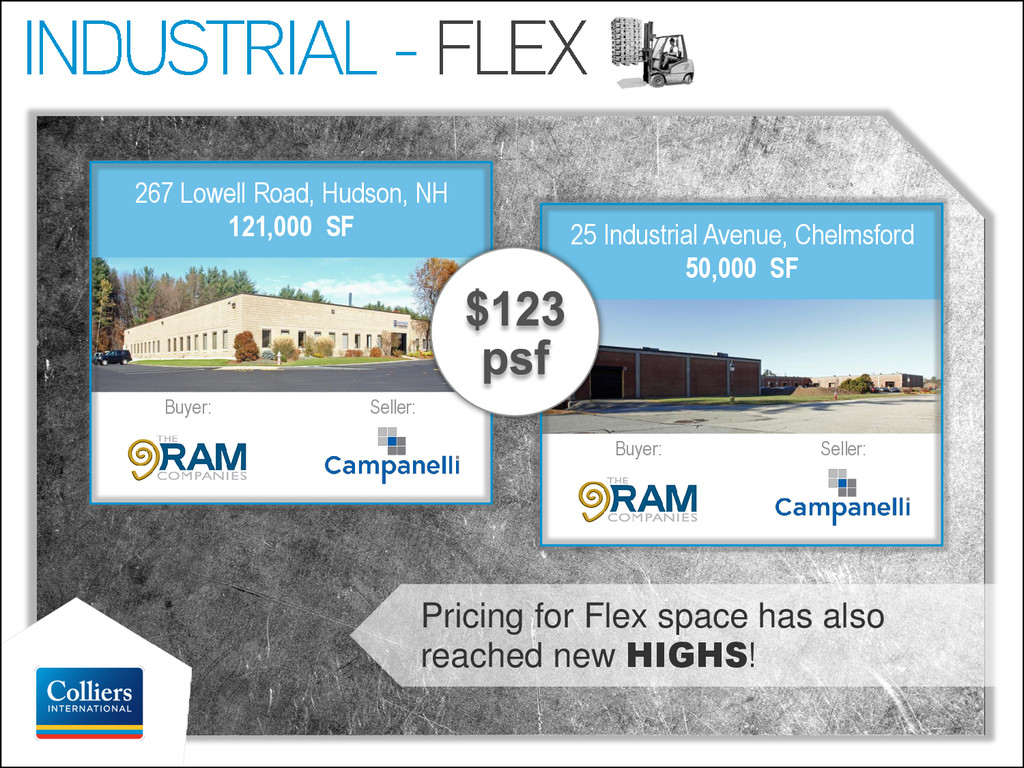

industrial! Even Class B, non-warehouse is being heavily pursued. New listing at 326 Ballardvale Street indicative of huge level of interest in the market! 326 Ballardvale Street Wilmington

industrial! Even Class B, non-warehouse is being heavily chased. New listing at 326 Ballardvale Street indicative of huge level of interest in the market! Pricing for Class A warehouse has reached new HIGHS!

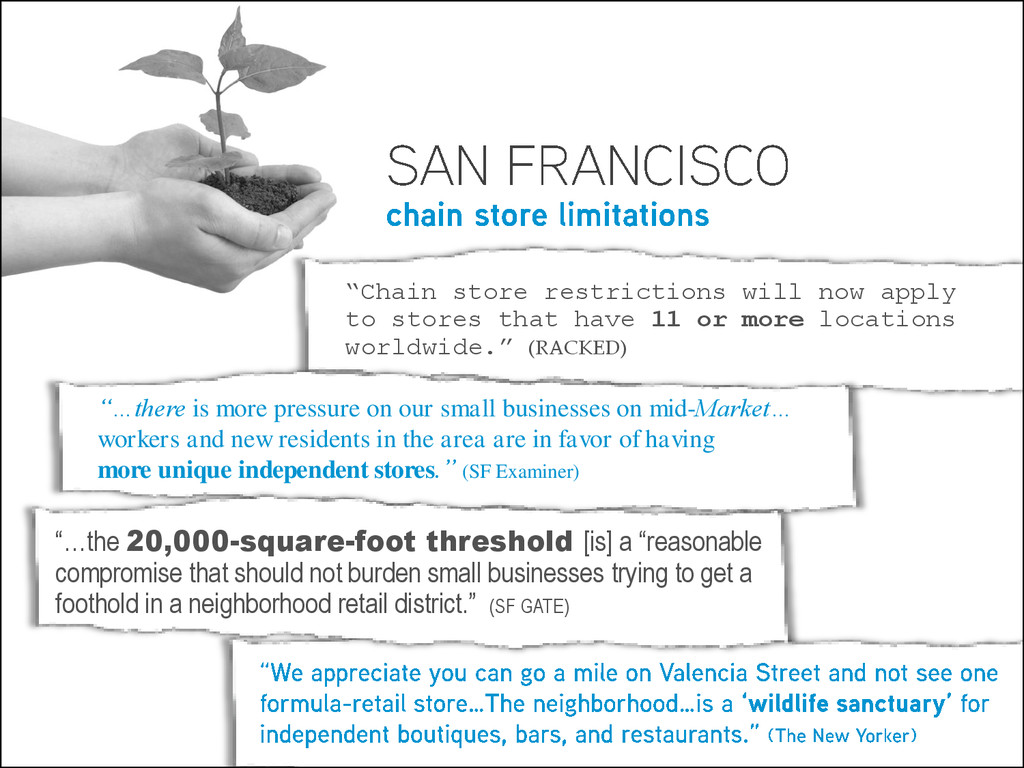

11 or more locations worldwide.” (RACKED) “…there is more pressure on our small businesses on mid-Market… workers and new residents in the area are in favor of having more unique independent stores.” (SF Examiner) “…the 20,000-square-foot threshold [is] a “reasonable compromise that should not burden small businesses trying to get a foothold in a neighborhood retail district.” (SF GATE)

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}