BMTC18: Closing Address: Christopher Shepard | Craft Brew News

Christopher Shepard will share industry insights and trends pertaining to craft beer in the U.S. As the senior editor of Craft Brew News, a publication by Beer INSIGHTS, Mr. Shepard is on the cutting edge of tracking craft beer’s growth.

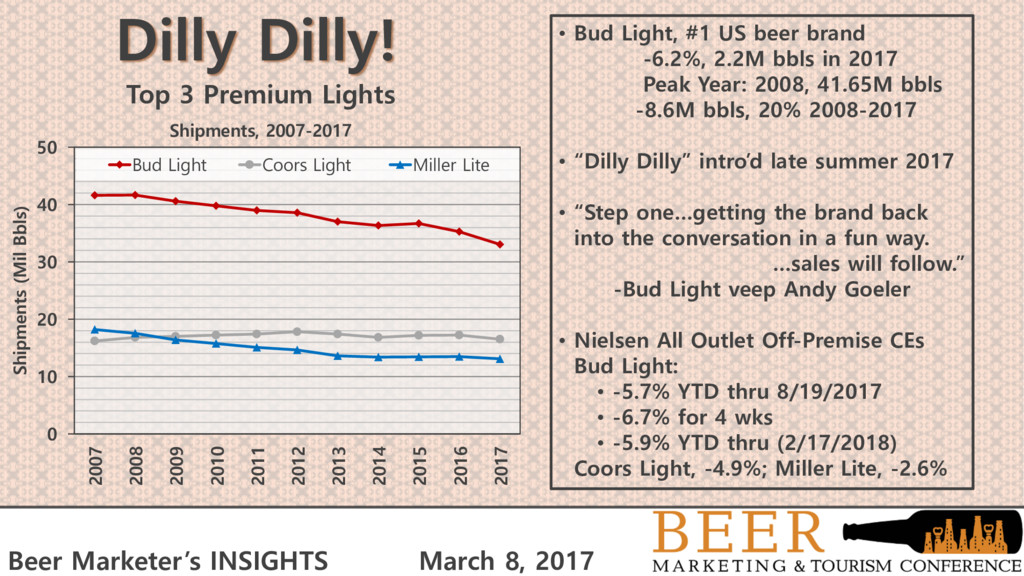

Beer Marketer’s INSIGHTS March 8, 2017 SUPER BOWL LII Biggest (beer) marketing event of the year NBC: 0:30 = $5.05M 1 brewer, 4 brands, 6 ads, 4 mins WSJ: AB spent >$533M since 1995, #1 buyer

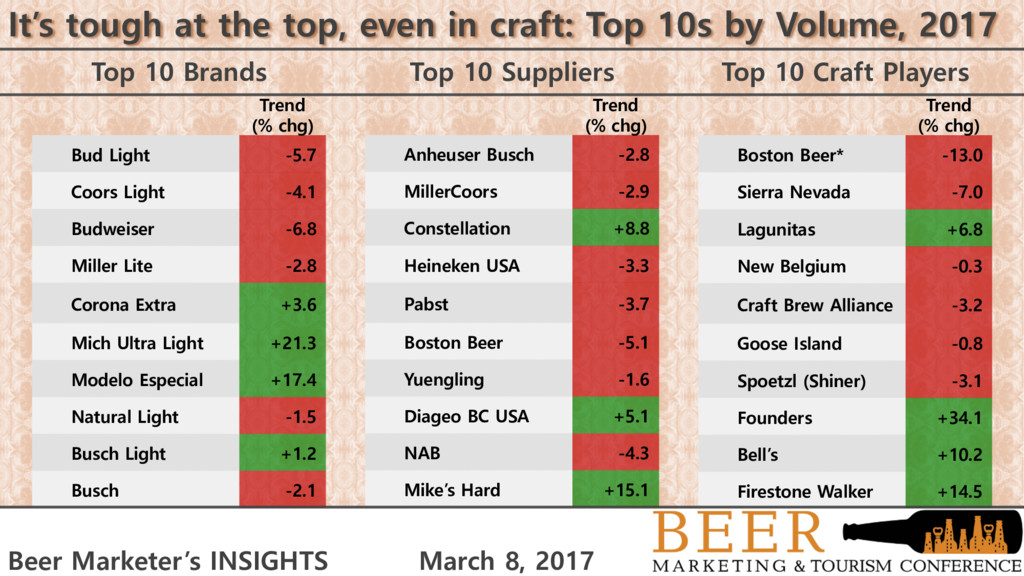

mainstream volume +50% +30% IRI multi-outlet + convenience, YTD thru 12/31/17; Beer INSIGHTS Seminar, NYC, 11/6/17 “We can’t sustain it unless some of us… ‘bust through the ceiling’…” “You’ve got to look at price.” - Mike Stevens Founders CEO/co-founder “We have to seek that mainstream beer drinker as our next chapter.” “never going to win…pricing game.” - David Walker Firestone Walker co-founder

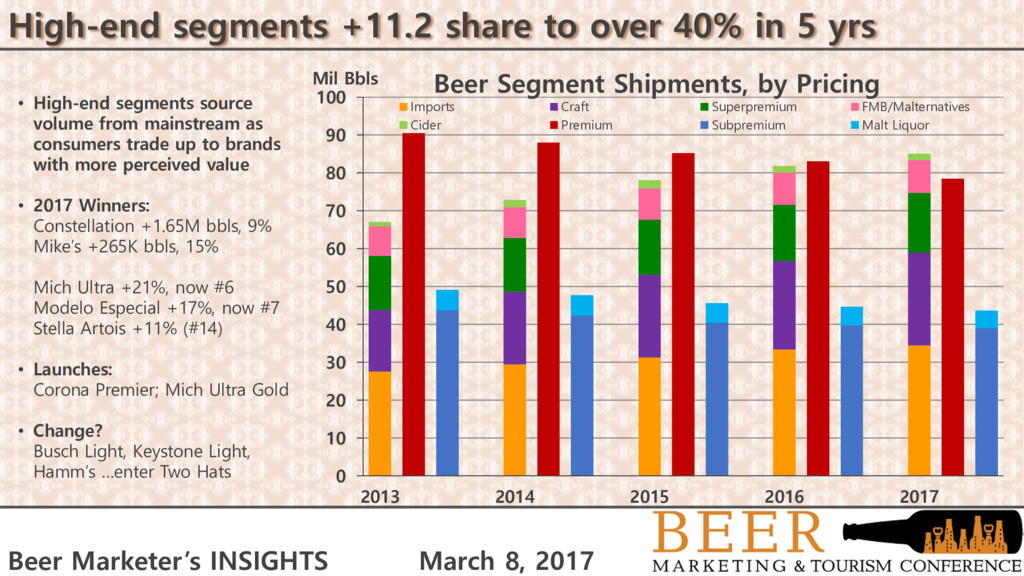

succeed: helping beer drinkers balance consumption with active lifestyles, for example • Yoga classes & running groups; local charities and business groups; tour groups & destination marketing • Built organically & require personal touch • Create strong bonds that can make all the difference • Brewers <100K bbls/yr: 12.1 mil bbls in 2017, +11% +7 mil bbls, 140% since 2012 +9.6 mil bbls, almost 400% in 10 yrs from 27.1 share of craft in 2009 to 48.3 last yr • Local bizzes face local problems: landlords, zoning boards, neighbors, banks... Small brewers build bizzes by building networks Beer Marketer’s INSIGHTS March 8, 2017

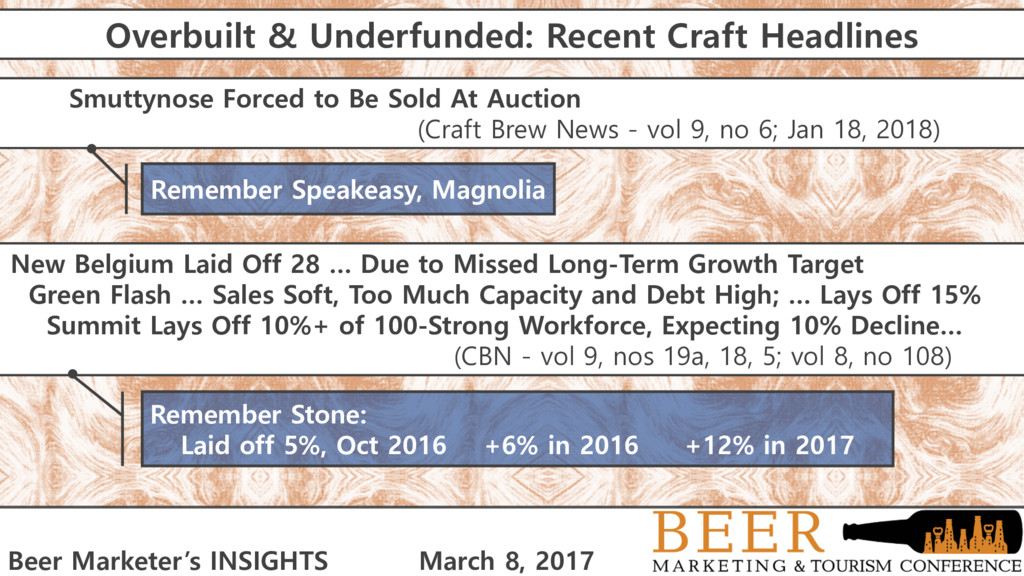

Sold At Auction (Craft Brew News - vol 9, no 6; Jan 18, 2018) New Belgium Laid Off 28 … Due to Missed Long-Term Growth Target Green Flash … Sales Soft, Too Much Capacity and Debt High; … Lays Off 15% Summit Lays Off 10%+ of 100-Strong Workforce, Expecting 10% Decline… (CBN - vol 9, nos 19a, 18, 5; vol 8, no 108) Remember Speakeasy, Magnolia Remember Stone: Laid off 5%, Oct 2016 +6% in 2016 +12% in 2017 Beer Marketer’s INSIGHTS March 8, 2017

bbls +54%, 700K bbls • Almost half of craft growth that year • US shipments +0.3%, 535K bbls that year • 2017, thru Nov +25%; Dec #???? Revisions? Reporting change? • BA: estimates +300-400K bbls due to differences in reporting, biz practices; survey sez: brewery visits lead to off-premise growth • Lack of clarity in non-3-tier volume (plus $$$$) has led to pushback Local is in. Taprooms are more in. But within the industry, it’s not quite that simple. Beer Marketer’s INSIGHTS March 8, 2017

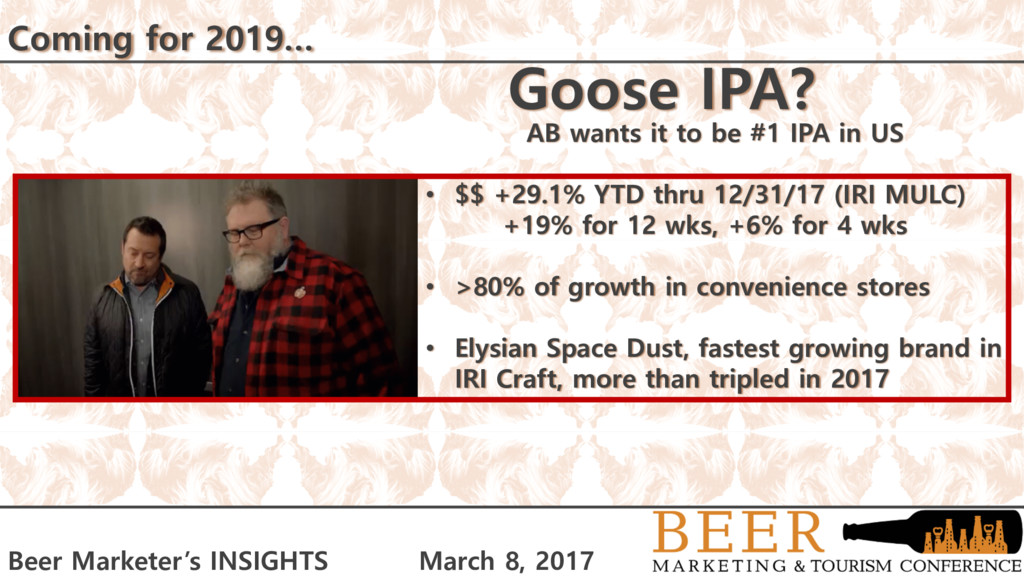

8, 2017 Coming for 2019… Goose IPA? AB wants it to be #1 IPA in US • $$ +29.1% YTD thru 12/31/17 (IRI MULC) +19% for 12 wks, +6% for 4 wks • >80% of growth in convenience stores • Elysian Space Dust, fastest growing brand in IRI Craft, more than tripled in 2017

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}